It often isn’t clear quite what the Labour Party means. Andrew Little is reported as follows:

Little said the banks needed to be “stiff-armed and told we’re not going to see, wholesale, farmers pushed off the land”.

His only argument for this sort of intervention – whatever it means in practice – appeared to be that

“We expose more New Zealand farm land to the risk of overseas ownership and I think that is a matter in which there is a national interest the Government should be alert to, and take action on.”

Which all sounds quite dramatic, and yet what follows seems like a rather damp squib.

A summit should be called and dairy cooperative Fonterra should be at the table. Farmers needed to agree on a long term plan for the cooperative to move its products up the value chain, even if that meant taking less cash out once the immediate crisis was over, to allow Fonterra to invest to generate better long term returns.

Government assistance should be provided to get farmers over the crisis, in a similar way to the help offered during drought, but it did not need to be any more than that.

So, apart from more talk, what is Labour actually proposing?

Keen as any individual bank might be to be rid of some of the more questionable exposures in its dairy book, it seems unlikely that banks, as a group, will be that keen on precipitating large scale exits from the dairy industry. Force one farmer to sell and there won’t be any material impact on the value of dairy farms more generally. Try to force several thousand to do so, and (a) it will be next to impossible to find buyers in the short-term, and (b) the value of the collateral banks hold could collapse. The Reserve Bank talked last week of an extreme scenario in which dairy farm prices fell by 40 per cent, but in an illiquid market like that for dairy farms there is no reason why land values should not fall by much more than 40 per cent if serious stresses were to develop. No one really knows what dairy land is worth in the longer-term (where will oil prices settle, where will the New Zealand real exchange rate settle are just two of the many relevant questions) but it is the sort of market where it is quite easy to envisage a severe overshoot. I’ve been tantalized for several years by parallels to some of the very illiquid mortgage-backed products in the US – not the ones that eventually saw huge defaults, but the ones where prices massively overshot in a climate of fear and illiquidity.

If each bank would prefer to be rid of some of its dairy exposures, each of them also knows that farm lending is going to be a major area of credit exposure in New Zealand for decades to come. It isn’t like lending to, say, a new industry which comes to nothing and goes away. If some individual farmers will leave the industry, the rural sector will still be around and collective memories can be powerful forces for good or ill. Banks were scarred by their experiences in the last major rural debt shake-out in the 1980s, and I doubt they will be eager to burn off goodwill among future potential clients. That doesn’t mean there won’t be forced sales, but it is hard to envisage the major rural lending banks rushing for the door (no matter how much unease the risk departments of bank HQs in Sydney or Melbourne or Utrecht might be feeling).

In some ways, a more concerning scenario for banks might be borrower panic. If enough farmers concluded that they were working for nothing and that there was no prospect of serious relief in the next few years they could, one by one, just choose to (try to) exit the industry. Of course, they’d still have to find buyers, but in a climate like that collateral values could collapse anyway. From the perspective of banks, it may be preferable if most farmers doggedly fight to stay on the land, allowing banks to make the calls on who to sell up and when, having regard to the potential impact on the rest of their national dairy portfolios. No individual farmers cares much about that.

But I still have no idea what, if anything, Labour is proposing the government or the Reserve Bank should do to “stiff arm” the banks, to prevent widespread sales. I’m pretty sure there are no existing legal powers that could appropriately be used for that purpose. Of course, behind the scenes all sorts of threats and pressures could be brought to bear, but surely that isn’t how we want to country to be run? So if Labour’s call means anything much they must be talking of new special legislative provisions. There was a great deal of resort to such measures in New Zealand during the Great Depression of the 1930s – allowing writedowns of loans, and of interest rates. Perhaps one could mount an argument for those interventions – on a basis of a totally unexpected collapse in the entire price level, an issue in macroeconomic mismanagement – but what would the case for intervention now be?

It seems pretty clear that any dairy debt losses are not likely to be large enough to threaten the health of the financial system – especially, as this is a slowly developing situation in which banks have plenty of time to bolster their capital buffers if that is required. And to bailout individual farmers, or the sector as a whole, would represent a material new source of moral hazard – a message to borrowers that they need not bear the consequences of their bad choices. That would only increase future demand for debt – in an industry that seems likely to continue to face considerable output price fluctuations

Of course, it may be that there is nothing much to Labour’s call at all – other perhaps than a desire to be heard. I’m not a fan of government assistance to farmers experiencing drought conditions – if managing weather risk is not one of the things farmers have to do, I’m not sure what is – but if Labour is talking of things only on that scale then I probably couldn’t get too excited. Then again, action on that scale doesn’t seem likely to make the sort of difference that would prevent “wholesale” exits and large scale increases in foreign land ownership.

Perhaps that “foreign land ownership” issue is really at the heart of Labour’s call. I’m not an absolutist on foreign ownership of land. After all, to be blunt, large scale English purchases of New Zealand land in the 19th century – even if mostly, individually, on a willing-buyer/willing-seller basis, did rather dramatically and permanently change the character of the country. But in the current situation we seem very far from that sort of risk. And in the shorter-term, the best hope for embattled farmers, and lenders, is the presence of a contested market of keen potential buyers.

And what of the call for a summit? It seemed like a pretty tired old suggestion, and it isn’t obvious what the role of the government is in such industry issues. We’ve heard endless talk over the years of “moving up the value chain” and farmers (the Fonterra owners) might reasonably be sceptical of the results to date. But summits about long-term industry strategy don’t seem that relevant to the issues of the current overhang of farmer debt.

Do I have any sympathy for indebted dairy farmers? Yes, to some extent. There are individuals and families involved, and the stresses – as in any struggling small to medium business – must be pretty intense and hard to cope with. It isn’t something those of us who spent our working lives as government officials never face. Then again, the upsides in the good years are also pretty extreme. Running a leveraged business is a high-variance operation.

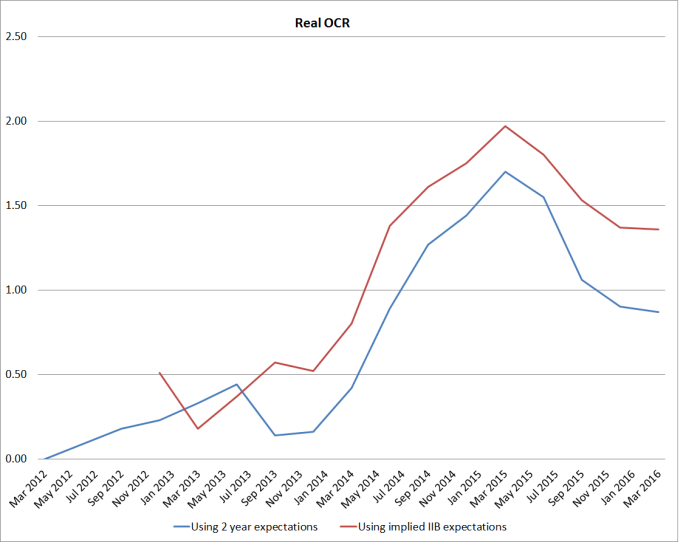

Cyclically, of course, farmers would be somewhat better off if we had a Reserve Bank that was doing its job better. With core inflation probably around 1 per cent, and real interest rates higher than they were a couple of years ago (and real retail rates probably higher than they were at the start of the year), there is simply no need for the OCR to be anything like as high as it is now. The OCR isn’t, and shouldn’t be, set with a view to supporting dairy farmers (or people in any other specific sector) but an OCR more consistent with the Bank’s own Policy Targets Agreement would (to a small extent) ease farmers’ financing costs and be likely to result in an exchange rate rather lower than it is now. We saw the impact of last Thursday’s surprise (itself mostly a timing surprise). It isn’t obvious that the OCR at present needs to be any higher than 1.5 per cent. At that level, we’d be likely to see the exchange rate quite a bit lower again, and every cent off the exchange rate raises the prospective payout to diary farmers, materially affecting prospective profitability of people in the industry. Not many farmers probably did contingency plans in which the TWI would still be above 71 even with WMP prices at current levels.

For the longer-term, if governments want to focus on more structural issues, there is a whole range of policy measures which help and hinder the dairy sector.

The ability to import large numbers of foreign dairy workers acts as a direct subsidy to the industry – holding down industry-specific wages rates – and has probably largely been capitalized into rural land prices. Water quality rules have been being tightened, but the ability to pollute, and pollute without paying, is another subsidy to the dairy industry. Subsidised irrigation schemes go in the same direction. None seems well-warranted.

And on the other hand, all tradables industries in New Zealand suffer from our very large scale immigration programme. Whatever monetary policy is doing, the resulting quite rapid growth in the population keeps upward pressure on the real exchange rate, driving up the price of non-tradables relative to the (largely fixed) global price of tradables. That makes it harder for firms operating here to compete in international markets, and helps explain why the per capita output of the tradables sector as a whole is no higher now than it was 10-15 years ago. We shouldn’t be reorienting our immigration programme around the short-term needs of particular industries, but the biggest single factor New Zealand has some control over that would help the dairy industry at present would be a lower exchange rate. A much lower immigration programme would, among other things, achieve that. It might also allow a more hard-headed longer-term conversation about some of those industry subsidies.