No, this is nothing to do with (say) Neil Quigley’s months-long spin and obfuscation from last year (eg here or here).

Decades ago, when the Commonwealth counted for more, the regular Finance Ministers’ meetings seemed to usually be held in some of the more exotic and picturesque of the member countries (these days, barely attracting any attention, they seem to be held in the margins of the IMF/World Bank annual meetings). The 1985 meeting was held in (then newly-admitted to the Commonwealth) the Maldives. New Zealand’s then Minister of Finance Roger Douglas attended.

In the mid 1980s one of the issues again wracking the Commonwealth was what to do about (former member) South Africa, still under the apartheid government that was reforming, if at all, very slowly indeed. In the late 70s there had been the Gleneagles agreement on sporting contacts but by the mid 80s economic pressure and possible sanctions (including forced divestment) were in view, and not just among Commonwealth countries. Pressure was building too on private sector firms and in 1985 a refusal by international banks to rollover South African government short-term foreign debt led to greatly intensified pressures.

The Commonwealth, of course, is and was a diverse grouping. Some member countries (New Zealand was one, but it was true of Caribbean member countries too) had almost no economic ties to South Africa. Others – small border states in particular – were very heavily dependent on South Africa (migrant labour remittances, access to imports etc). And UK firms collectively made up by far the largest source of foreign investment in South Africa. Getting any sort of common view was a challenge to say the least, even when all deplored the apartheid system and looked towards a future transition. The South African government and security forces were not known as soft touches. Neither, of course, was Margaret Thatcher.

The Commonwealth was never able to agree on any very serious package of economic sanctions, but just a few weeks after that Finance Ministers meeting, the Commonwealth Heads of Government, meeting in the Bahamas, did agree a fairly mild set of measures. A further round was adopted the following year. Probably like all sanctions policies, economic and political historians no doubt debate quite what role sanctions did, or might have had, in leading to the early 1990s transition.

Back in 1985, the then Reserve Bank Economic Adviser (until recently Chief Economist) Peter Nicholl took up a one-year IMF-sponsored secondment as Head of Economic Research to the central bank of the Seychelles, also an Indian Ocean Commonwealth member country. Peter tells the story thus:

One thing I did during the evenings and weekends there was write a political thriller called Sanctions in Paradise. It was set in the Seychelles so i didn’t have to make up the scenery, just observe it. There is a Commonwealth Finance Ministers’ Conference being held in Seychelles. I had attended a couple of those boring meetings so I knew how they were organized and run. The main item on the agenda was whether or not to impose economic sanctions on South Africa because of their apartheid policies. The idea of trying to write the story occurred to me when I read a report on a group of South African mercenaries led by Mad Mike Hoare that had flown into Seychelles three years before I went there to try and overthrow the government – they failed. But reading the report gave me the idea of the South Africans trying to disrupt the meeting.

Peter came back to the Reserve Bank of New Zealand, spent several years as Deputy Governor, then as Executive Director at the World Bank, before an eight-year IMF-sponsored stint as the first Governor of the Central Bank of Bosnia and Herzegovina. (He made an appearance on this blog last year, having written a column for his local newspaper in Cambridge on the Reserve Bank shambles.)

Peter’s email to me a few weeks ago went on

I only sent it to one publisher. I got a very nice letter back – but it was a rejection letter. I put the book aside. I then lost the computer it was on and forgot all about it. About 3 years ago my sister found a printed copy in a box of papers from my mother’s estate. My mother was a hoarder – fortunately for me in this instance. I thought that was an omen so I decided to get the book self-published.

He offered to send me a copy, in the hope that I might like it and give it a plug. Self-marketing isn’t always easy. He passed on a couple of enthusiastic comments from eminent economists, both of whom had “thoroughly enjoyed it”. one adding “I found your accounts of the different national positions on sanctions on South Africa to be fascinating and compelling. The plot was good, your knowledge of Commonwealth meetings was obviously first rate and your writing is really good” and the other suggesting it had been a great read and suggesting Peter write another book.

I’m quite a fan of political or spy thrillers, especially those written and set in bygone decades which capture some of the flavour of the times without the benefit of hindsight (on Tyler Cowen’s recommendation last year I devoured those, mostly from the 1930s, of English writer Eric Ambler).

Much of Peter’s book is written in the voice of a rather hapless Treasury secondee (doubling as the Minister’s speechwriter) in the office of the Minister of Finance, part of the small New Zealand party at the conference. Resemblances between the Minister of Finance character and Roger Douglas seem slight at best, but the PM does get a bit part and there might be a few more resemblances to David Lange there.

So what did I make of the book? It was pretty well plotted and so I enjoyed the story. Since the author knew both the local setting and the political setting (as he notes, he’d been to previous Commonwealth Finance Ministers meetings) there is quite a sense of authenticity about it. The political issues and tensions from the times were very real, and if I’m old enough to hazily remember them, younger readers might appreciate an undemanding dip into the political tensions of another time. And if the book seemed a little slow to get going (albeit there is a high-drama event on page 3), it gathers pace and ends with a plausible-enough plot twist that I really didn’t see coming. And while newly released, the circumstances of the writing, loss and recovery, mean it does treat real history as we live it – without the benefit of hindsight, knowing how things eventually turned out.

As a reviewer, I’d note that the plot was stronger than the character development – but then it is a political thriller, not claiming to be “literary fiction” – and the dialogue at times was a bit clunky. Oh, and in a few places an editor might have been helpful (I noted Peter slipped between talking of a Prime Minister and a President of South Africa – from 1984 it was President (P W Botha)). But, yes, it was an enjoyable read, and not at all bad for the price.

Yes, Peter sent me a free copy but it appears that you can buy it for $19.95 in paperback or $5.99 for the e-book. Orders appear to to be able to placed here although Peter suggested that anyone wanting to buy a copy could contact him direct at peterwenicholl@yahoo.co.nz.

When I stopped regular blogging in December I wrote

This is one of those issues that has really got my goat. (There won’t be any other return to blogging, although if I make a submission to the government’s belated independent review of Covid-era monetary policy I might put a link to that in a post.)

It is a nice summer evening in Wellington and would be a good time to be at the beach but….well…Wellington City Council…

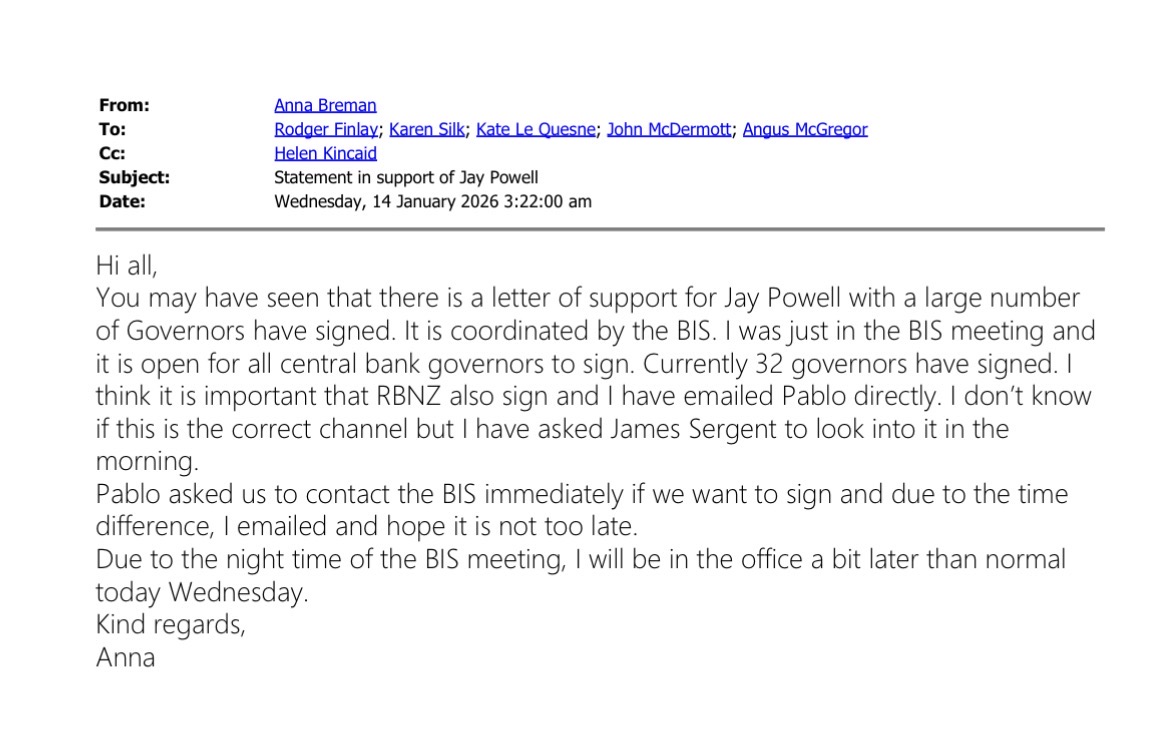

A month or so ago the new Governor of the Reserve Bank signed up to a public statement by a group of several other central banks (ECB, BOE, RBA, Riksbank etc) in support of the outgoing Fed chair, Jerome Powell, following his revelations of what appeared to be an attempt to intimidate him by Trump’s Department of Justice. Most of the world’s (operationally independent) central banks didn’t sign (14 central banks signed up, and among those who didn’t were – from among advanced countries – central banks of Japan, Israel, Czech Republic, Poland, and Chile). Nor, of course, did the non-independent central banks from advanced countries (Singapore, Taiwan).

One can debate the substantive pros and cons of the statement (eg was it wise, helpful, accurate and so on). But that isn’t my focus here. One can also debate the best way for countries to respond to Trump (my own stance would be much more openly critical than our government’s own timid approach). But again not my focus here.

Instead my focus is on the Reserve Bank Governor’s approach and response.

Shortly after the news emerged that she had signed on to the statement (on 14 January) I OIA’ed the Bank (and the Minister) for all relevant material, including on (for example) invitations to join, consultation within the Bank, and consultation across other government agencies/ministers. An hour or two later, the Minister of Foreign Affairs Winston Peters had a go at Breman, noting that there had been no consultation with MFAT and strongly suggesting that the Governor needed to stay in her lane, suggesting that the Bank had operational independence in various domestic areas, but not to go trespassing across foreign policy, as a government agency.

(Personally, my initial scepticism about signing had to do with the credibility of the Reserve Bank itself – if you wanted good central bank governance and accountability you would certainly not have looked to the Reserve Bank of New Zealand over the last couple of years (budget busting, active misrepresentation by the outgoing board chair, repeated attempts to mislead Parliament, and finally the appointment of a new chair who’d been not only an active part of all that but had initially been appointed to the board when he had a clear conflict of interest. Oh, and a Minister of Finance who prevailed on the Bank to change its – independent – bank capital policies. Should anyone in the US administration have cared enough, a New Zealand signature would have looked laughably hypocritical (even if the new Governor might have good intentions.)

As it happens, in this particular saga documents released today suggest that, for all his other faults, the Board chair was one of the adults in the room.

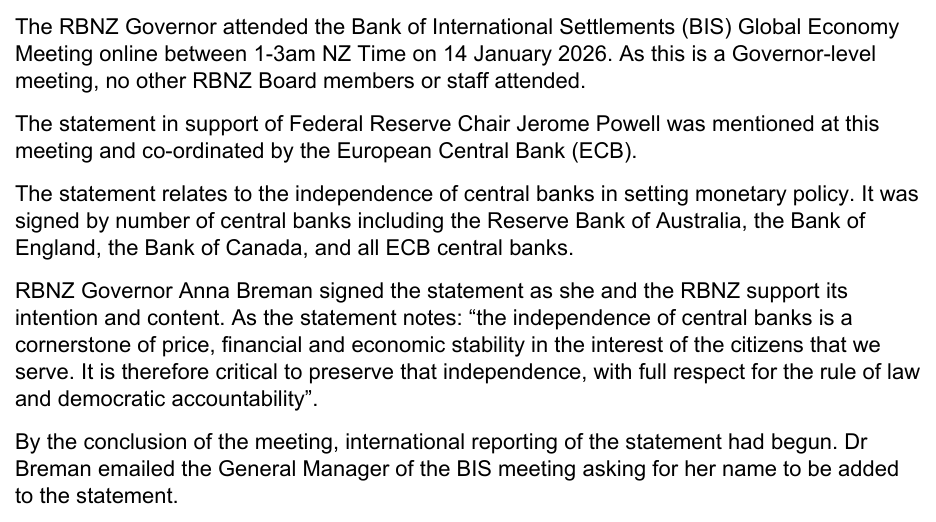

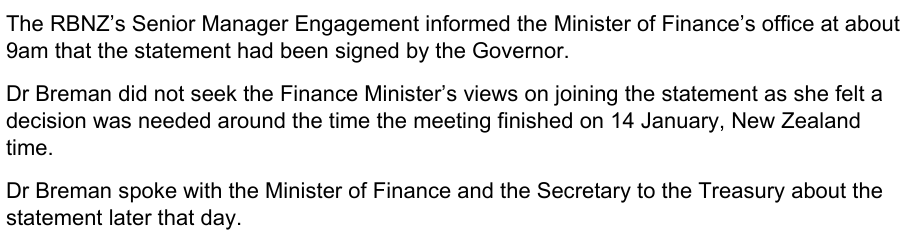

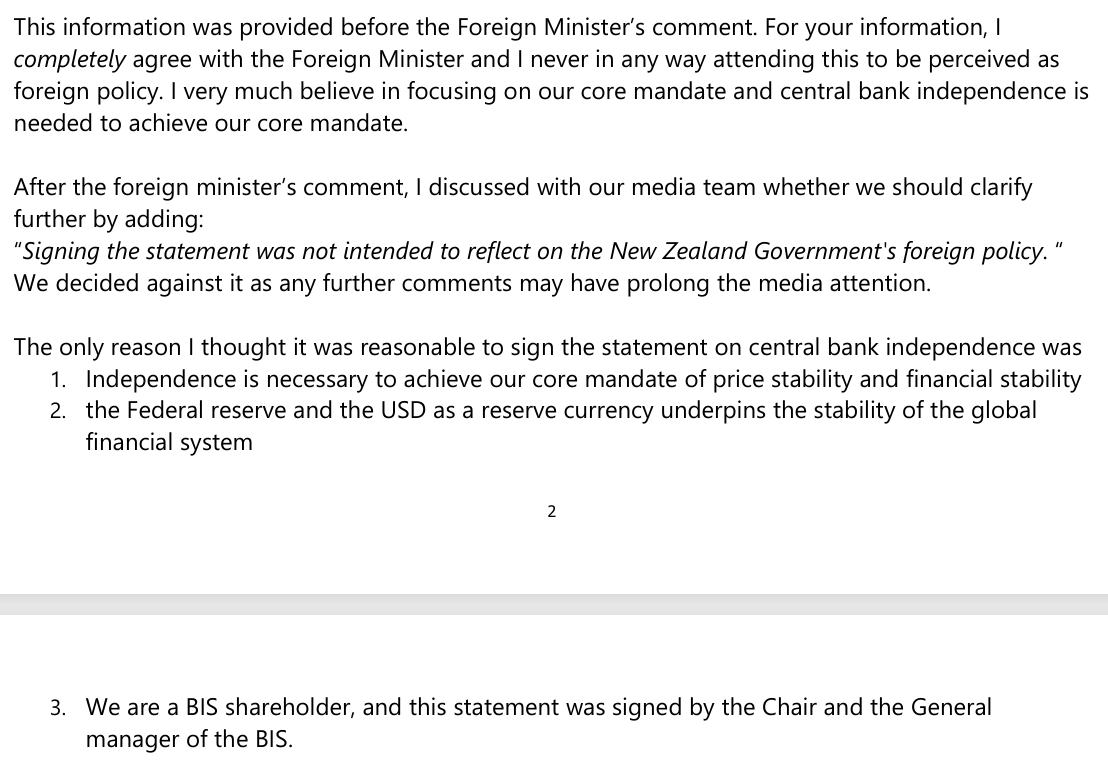

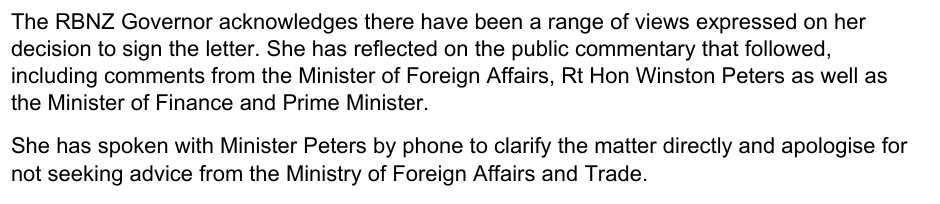

You may recall that the Governor claimed that she was under real time pressure to sign up to the statement (at an on-line BIS meeting held from 1 to 3am that day). And, being the middle of the night, she didn’t feel she should bother the Minister of Finance (for example). The Minister of Finance has since made it pretty clear that the Governor should have felt free to have rung. The Prime Minister also weighed in with a gentle rap over the knuckles. And the Governor has apologised to both ministers (Finance and Foreign Affairs) for having gone ahead without consulting them (and/or their agencies).

When you listen to the Governor’s rhetoric one of the attractive dimensions is the claim that she wants a greater degree of transparency. That is welcome, but once again she does not walk the talk.

That OIA request of mine was lodged on 14 January. The Official Information Act requires agencies to respond as soon as reasonably practicable. The deadline for my request is tomorrow (the Bank probably envisaged sending it at 5pm on Friday). But this afternoon a 39 page release appeared silently (no press release or anything) on the pro-active releases page. I happened to spot it only because I was checking up something else. The 39 page document is presumably what they will tomorrow treat as the response to my OIA. Were they actually committed to transparency they could have put the lot out just a few days after the request was received (the release consists of a summary statement, a long set of letters from members of the public in support or opposed to the Governor’s decision to sign up, and a set of emails mostly among a few senior managers and board members, with no substantive redactions). But when bureaucrats tell you they are committed to transparency, mostly it is only for occasions when it suits them, and that is no accountability at all.

I’ll use the “Summary background statement” to frame all that follows, since it is the story the Governor has apparently chosen now to tell.

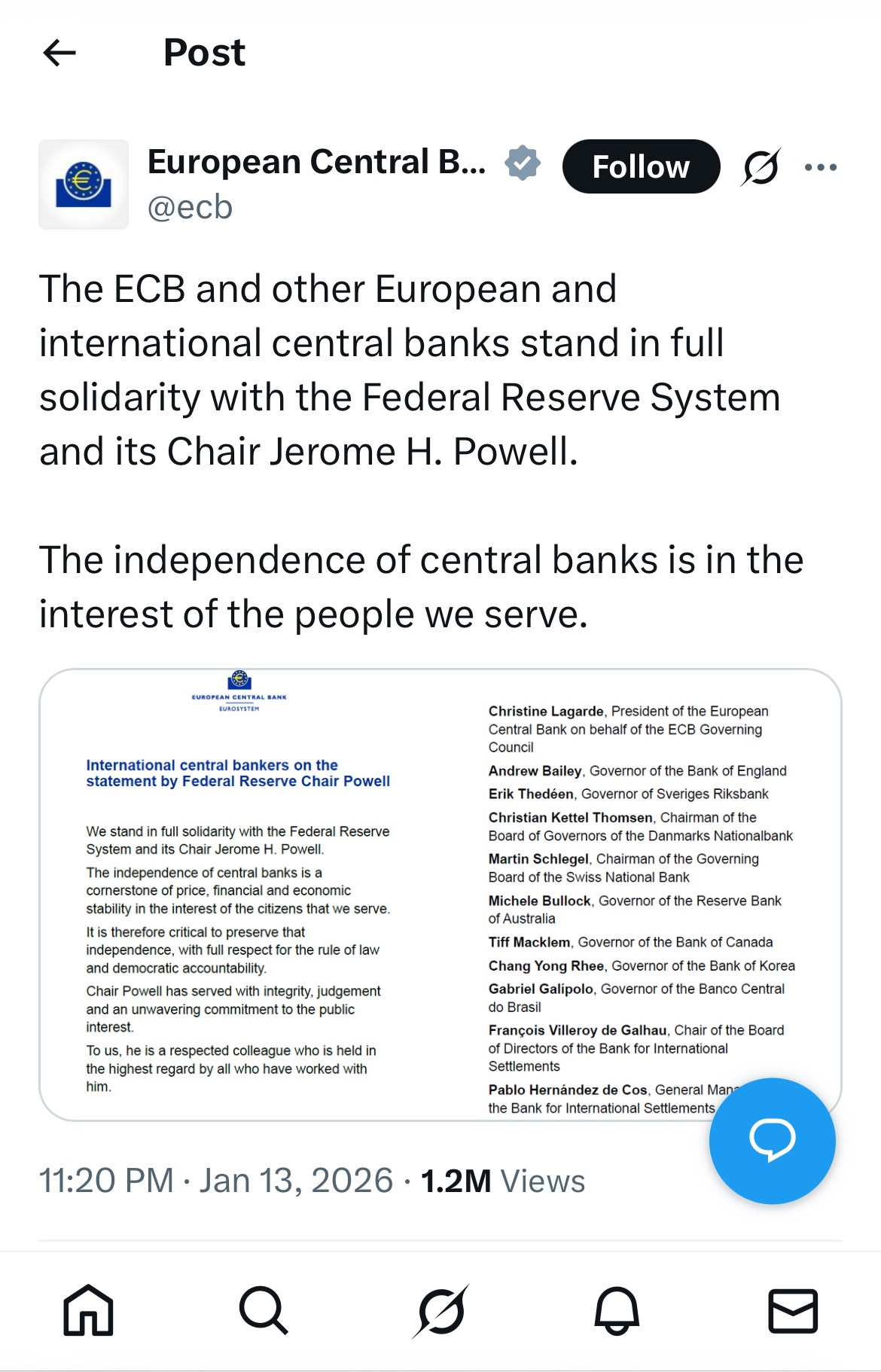

Which is fine, except all that it leaves out. What you would not know from this statement, or any comment from the Bank last month, is that the initial statement (9 central banks signing) had gone out a couple of hours before the BIS meeting (at 11:10pm New Zealand time). The ECB had it on its Twitter feed by 11:20pm

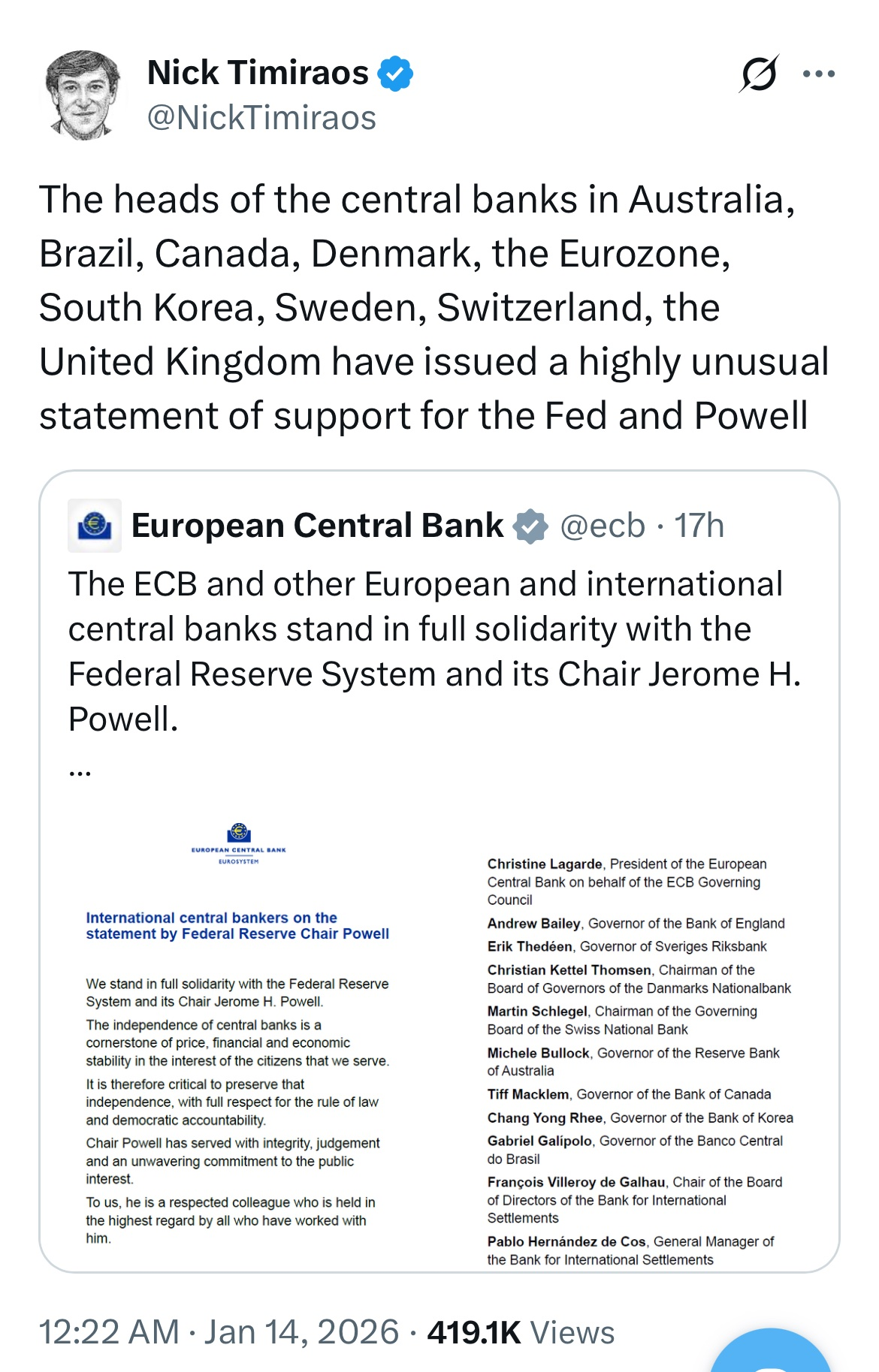

And, despite the Governor’s comment that “by the conclusion of the meeting, international reporting of the statement had begun”, in fact the WSJ’s chief economics correspondent had been tweeting about it by 12:22am

In this part of the world, the RBA had put the statement on its website at 12:30am NZ time

The statement had gone out, and was being reported on, before the 1am meeting even began.

There is no sign that the Governor or her staff were aware of any of this or (importantly) that they had even been invited to sign. My OIA request included any invitations to sign or correspondence with other central banks etc, and there is simply nothing of that sort in the response. The nine signatories will not have done so on the spur of the moment (there must have been exchanges over drafting, substance etc in at least the day prior to release, and probably at least some heads-ups within those individual central banks and perhaps to other government agencies/ministers. Some who were invited – one might guess the BoJ – apparently chose not to sign.)

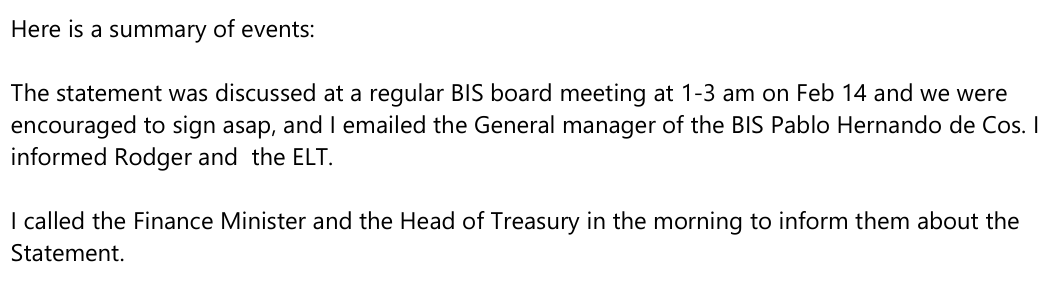

Apparently (from the Governor’s email to her staff at 3:23 that morning) in the BIS meeting it had been indicated that any central bank that wanted to was free to sign. The Governor notes that “I..hope it is not too late” for them.

There is simply no basis for her claim that there was anything so pressing she needed to act immediately. The statement had gone out already, she hadn’t been invited….but perhaps she wanted to associate with the “cool kids” central banking club? Why would she still be seeking to mislead the public like that?

What of consultation?

It turns out that she consulted no one at all. Not senior staff, not the Board chair, not the ministers, not the Treasury or MFAT. We’d been told previously that she had informed Finlay. It wasn’t then clear whether that was before or after she signed (bearing in mind it was the middle of the night there may have been no practical difference if she’d just sent an email).

Here is the email, sent nine minutes after her email signing up.

No sign of any consideration of pros and cons. No suggestion even of people who might need to be advised in the morning. Not even any mention to her colleagues that she’d consciously decided not to consult the Minister. No consideration of whether signing could have waited until morning.

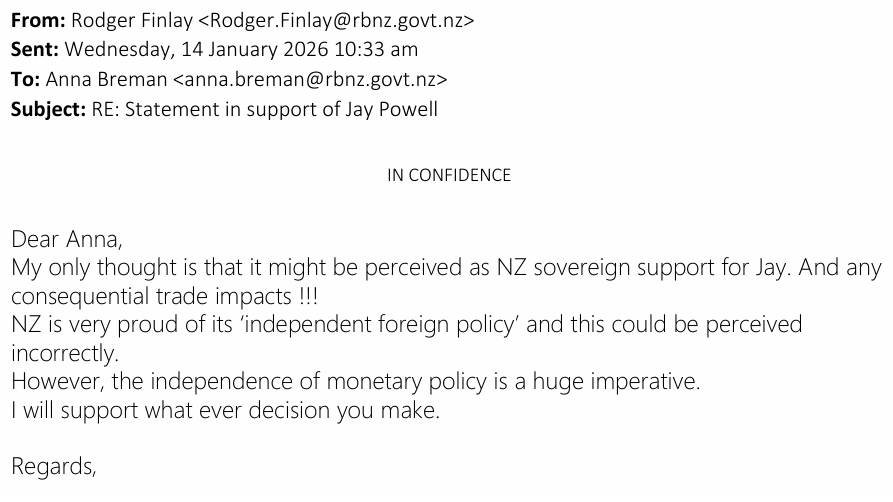

Quite a few hours later the board chair Finlay gets back to her

You can tell he is not exactly impressed and, again, the Governor’s statement spins things in her favour. He raises the foreign policy concern issues – exactly of the sort the Foreign Minister would later make in public. And while Breman is technically correct to say that “he supported her decision” it really reads a lot more like “what is done is done. too late now, but….you are my new handpicked Governor and of course I will back you”.

That he was hardly an enthusiastic supporter is also implied by a email to the Board the Governor sends out the following day, which includes this “I have discussed this with our Chair at length yesterday”. The “at length” really says it all. Finlay seems to deserve a rare “well done”.

And what of the rest of government. The official statement now says:

But in fact, even here the documents released suggest a less favourable story. Two of the Assistant Governors weigh in enthusiastically when they finally read the email (after 8am – don’t these senior people check their emails when they wake up?), only for one – a non policy guy – to suggest that perhaps “we should also give MoF a heads-up…..maybe MFAT” – maybe, when the boss has, hours ago, signed up to a statement by implication attacking the volatile US President. Karen Silk, the egregiously underqualified macro policy DCE then qualifies her enthusiasm with a belated “sorry, also agree with John – in particular MFAT just as an FYI”. She – the macro person – apparently didn’t think Treasury or the Minister were worth bothering about.

The Governor herself may still have been on her way to work at this point – she isn’t part of the email chain – but some comms people get on to telling the Minister of Finance’s office, but even then there is no record of them advising Treasury or MFAT. Quite when Breman spoke to Willis or Rennie isn’t clear although it seems to have been later in the morning (there is no email traffic relevant to these calls, either mooting them or reporting what was discussed).

The final set of documents released relate to an email to Board members from the Governor the following day.

She claims “we were encouraged to sign asap” but…..after all, she was a free agent. The statement itself had already gone out. It is simply extraordinary that the Governor – a new Governor, with probably (and understandably) little sense of New Zealand government ways or foreign policy perspectives – allowed herself to be rushed into signing up with the cool kids without consulting a single other person on her side, in the middle of the night. What, precisely, would have been the consequences of having said “it is the middle of the night here, I’ll talk to my colleagues in the Bank and elsewhere in government and get back to you by midday”? (In fact the statement on the ECB website still reads “Other central banks may be added to the list of signatories later on” although none have been added since later that first day.)

She concludes this email to board members this way

It betrays an almost incredible degree of naivete. The Bank – like many government entities – has some, quite defined, operational independence. It is however fully a part of the New Zealand public sector. The Minister of Finance appoints and dismisses the Governor, sets spending limits, sets policy targets etc. How did the Governor not think that her signing on might be seen by some as stepping across foreign policy boundaries? Being the middle of the night is no excuse – all manner of real crises can occur in the dark hours too. It was a serious rookie error.

Responses from only two board members are recorded, both formal and neither offering either support (or criticism)

And the Bank’s summary statement ends this way

Previous reports indicate that she had also apologised to the Minister of Finance.

As I said earlier, I’m not here to debate the pros and cons of the statement. My interest is in two things. The first is the apparent inexperience and rookie-error stuff of the new Governor, revealed in her actions and descriptions. Relatedly is how weak her management team seem – it took hours for any one of her top team to suggest that perhaps they needed to look others in government know, none of them raised the foreign policy/appearance issues, and none of them seem to have proposed a strategy to deal with the mess they found when they woke up (Silk, here, seems particularly culpable).

And then there is the spin still to this day. Why skip over the fact that you hadn’t been invited to sign up initially, or that the statement had gone out (and been reported on) well before the 1am meeting even started. Why suggest, in the summary statement, that the board chair had been more enthusiastic than the later documents really suggest. Why imply an urgency – to act without consulting anyone, having gone into a meeting apparently not even aware of the statement – that simply was not, in any substantive way there.

It is a pretty poor start from the Governor, not at all consistent with her statements about improving transparency. Perhaps it is an illustration of the old line that you can change the people but organisational cultures – good and (in this case) ill – can prove quite enduring.

She needs to up her game, and the board and Minister need to insist on it.

UPDATE (Fri): The OIA response came this morning (in substance the same as what the RB put out yesterday)

About 15 years ago (partly thanks to a couple of years at Treasury, partly to the financial crises in the US and Europe) I started to get much more systematically interested in New Zealand’s disappointing and underwhelming economic performance, and in economic and financial history more generally. And as our kids were growing I was thinking about what to do next. The idea of writing a blog (it was still the heyday of economics blogging) appealed, focused on New Zealand economic (under)performance issues – something I obviously couldn’t do as a public servant. The kids were going to grow up fast and I wanted to be around more for them. My wife got to a position in her career where we could live fairly comfortably on one income and fortunately that coincided with Graeme Wheeler’s desire to be rid of me. And thus, with that double coincidence of wants, this blog launched on 2 April 2015.

Those who’ve followed the blog from early days may recall that for several years I was often writing twice a day, often six days a week. I had fairly voracious interests and the blog found a surprising (to me) number of readers. It also became more Reserve Bank focused than I’d ever envisaged (productivity etc matters a great deal more).

From time to time I’ve thought about how long to continue and in what form. Frequency of posts dropped off, through some combination of circumstances, including poor health for much of the last five years (weird fatigue, including post-Covid, that came and went to some extent but never seemed to go away) and other commitments. I was fortunate enough to be appointed to the board of the (central) Bank of Papua New Guinea two years ago, which has proved to be a big time commitment, and introduced something of a six-weekly cycle to posting here.

On the 10th anniversary of the blog earlier this year, I noted

Circumstances change and I’ve got busier. I have occasionally thought about shutting it down and doing other stuff – I had an outline on my desk when the BPNG appointment came through of a time-consuming project I’d still like to pursue. For now, various circumstances and considerations mean I’m going to try to discipline my public comment more narrowly. There has been an increasing range of things I’d like to have written about but it wasn’t possible/appropriate. For this blog that will mean primarily Reserve Bank things, fiscal policy, productivity and not much else, which was the original intended focus.

And now the time has come to discontinue the blog, at least as a forum for regular economic and economic policy commentary/analysis. I certainly haven’t lost interest in the issues, and the economic and institutional problems, here and elsewhere, haven’t gone away. But there have been a couple of influences. As I noted in April there has been an increasing range of things I couldn’t really comment on. Some of that was about the senior role my wife has held this year (eg largely avoiding things – many – her minister was responsible for). But longer-term my BPNG role, where I now chair the board’s financial stability and related issues committee, has also come to act as a constraint: I don’t find it as easy to comment much on things like bank capital, CBDCs, exchange rate regimes, financial market regulation, payment systems, emergency liquidity provision, failure management (or the IMF). I’ve also become increasingly uneasy about writing on central bank governance and related issues, even when specific issues are very different by country. I’d have stopped months ago if it hadn’t been for the whistleblower whose disclosures to me helped us get closer to the bottom of the Orr/Quigley stories.

So those were some constraints. But at least as importantly is the question of opportunity cost. I could have kept on writing this blog in some form or another more or less indefinitely. But time isn’t unlimited, and having given this ten years plus, I might have ten good years ahead. There are other things to do and focus on. As just one example, thinking more seriously about New Zealand’s economic and financial history, including in a cross-country context.

And, mercifully, in recent months my health seems finally to have fully recovered. I’m back to walking, fairly fast, an hour a day and getting home not exhausted. It is a very nice change to have that energy back.

I’m not going into some sort of economics purdah, but I won’t be writing regular commentary etc here at all. I will leave the website in place, and may occasionally add a post on some interesting economics book I’ve read or an aspect of economic history that takes my fancy. Perhaps also I’ll weaken very occasionally if some current issue really gets my goat, but this post is about tying myself to the mast. My intent is to stop, and to stay stopped.

And if I’m writing shorter pieces much of it may be more oriented towards my fellow Christians. I do have another blog, and I have started writing there again in the last couple of months. I intend to keep on with that, and to read more deeply in theology, biblical studies, and related societal issues.

Anyway, thank you to the everyone who has read the blog over the last 10+ years. It has, mostly, been fun, and stimulating. Writing has often clarified my own thinking and it has been great to have had an audience. I’ve enjoyed interacting with a range of people through blog comments and private correspondence. And I’m not going anywhere.

It is the church’s season of Advent. In the first few years of the blog I’d often include some explicitly Christian material to end my final post each year. So here I’ll leave you with the words of one of my favourite Advent carols.

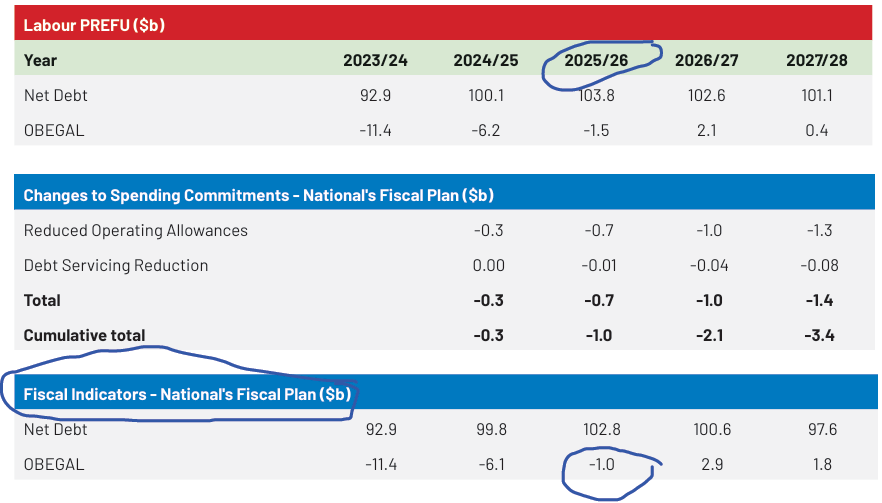

Back in the far flung days – well, really only just more than two years ago – the National Party went to the election with a fiscal plan under which the government’s operating deficit would have been more or less closed by now. This was the table from that plan.

And in case you are wondering, the PREFU projections that provided the economic base for National’s numbers still had a negative output gap of 0.9 per cent of GDP for the 25/26 year, so it wasn’t exactly a rosy economic scenario. But the deficit was to be more or less closed by now ($1bn for the full year is a bit under 0.25 per cent of GDP, and by the second half of that year – which we are almost in – presumably consistent with a tiny surplus).

There will be an update with the HYEFU next week, but in this year’s Budget – where the government last made overall fiscal decisions – the deficit for 2025/26 was forecast to be $15.6 billion.

Now, to be fair, going into the 2023 election National wasn’t exactly making much of the structural deficits they expected to inherit (I recall at the time noting that there were few or no references to the deficit in the fiscal plan document). And, thus, I guess they’ve been consistent. When the deficit turned out to be more embedded than they’d expected – Treasury having badly misjudged how much tax revenue the economy was generating – National chose not to be any more bothered. They simply chose, in both budgets so far, to do nothing at all about closing the deficits.

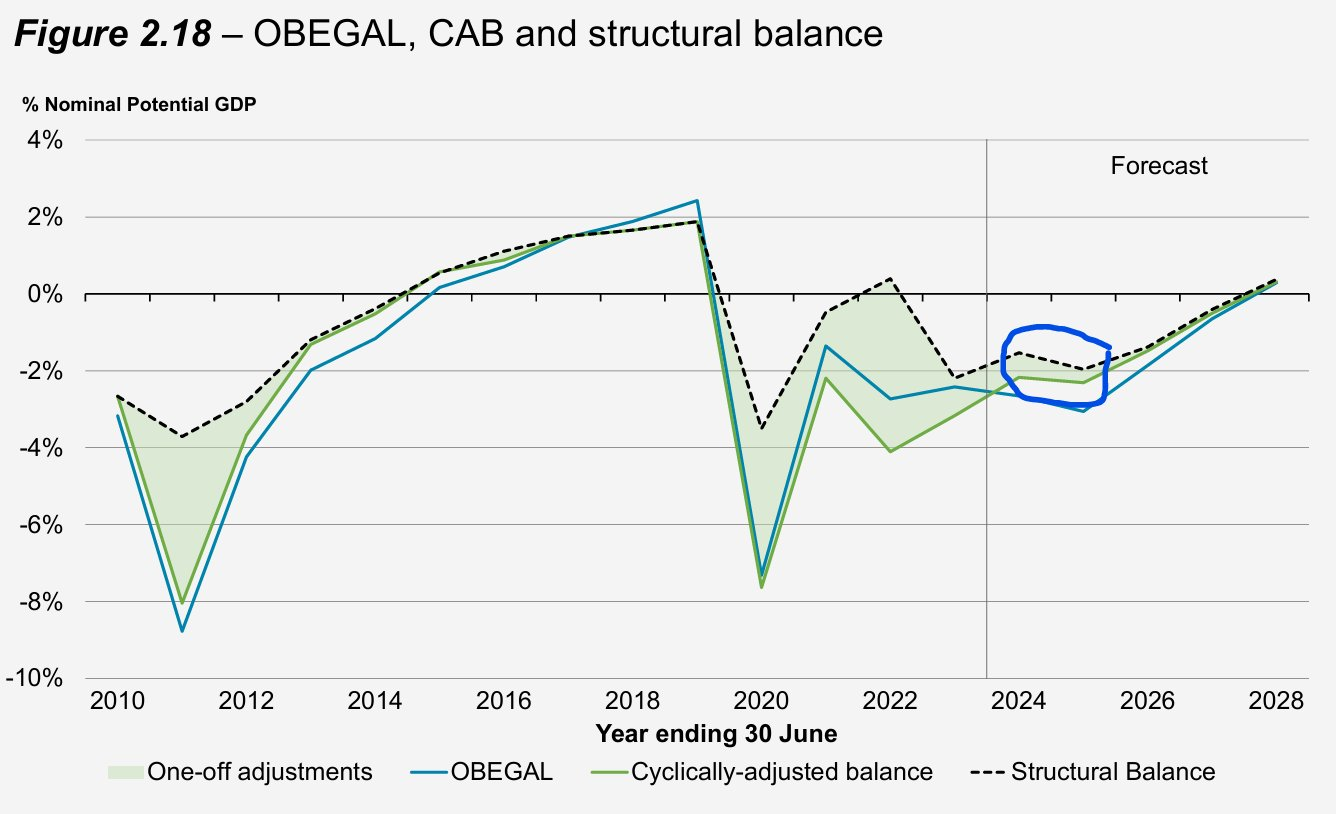

This had been apparent in Treasury’s analytical numbers. They publish estimates each year of the structural deficit – ie the bit not amenable simply to the cyclical state of the economy.

This chart was from 2024 budget documents

History is as it is (or, at least, is estimated to be). The medium-term future numbers are, under any government, just vapourware (Treasury uses the future operating allowances the then Minister advises them, which need not bear any relationship to what is actually done when the time comes). But what I’ve highlighted is the move from one year to another, for the fiscal year to which the Budget relates. Thus, in the 2024 Budget Treasury had an estimate as to how big the structural deficit had been for 23/24 and then, given the hard decisions ministers were making, and getting parliamentary approval for, a forecast as to what the structural deficit would be for 24/25. As you can see, in that Budget, the government chose – they had these numbers and associated analysis – to take steps that, taken together, slightly worsened the structural deficit.

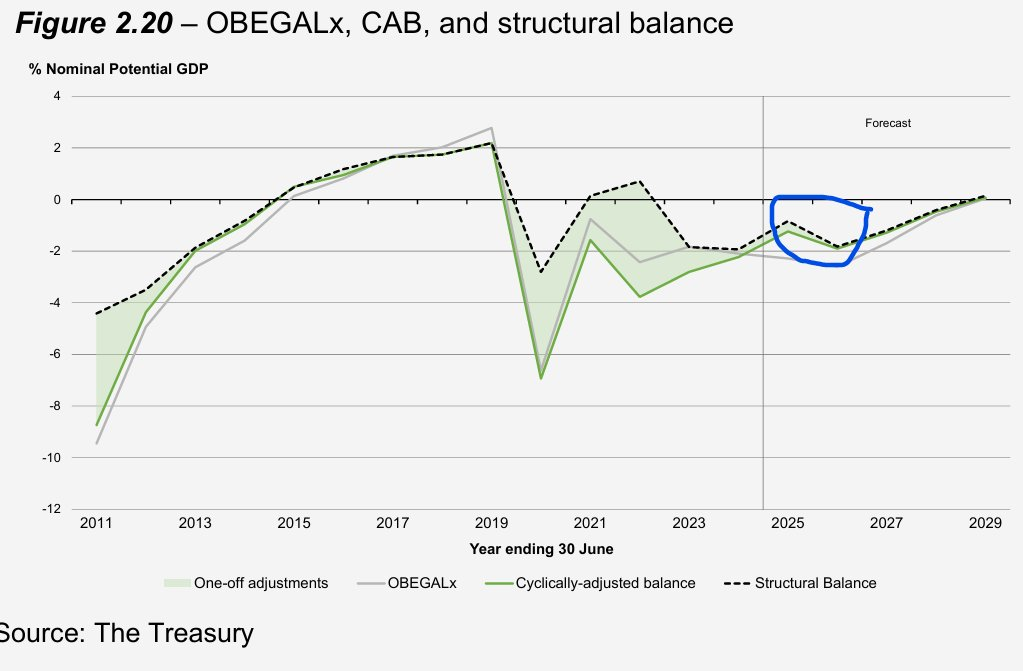

The picture from the 2025 Budget was much the same

For a second year in succession, this government’s Budget slightly worsened the structural deficit.

Of course, all the numbers are imprecise estimates, but they were the best estimates available to ministers when they made the Budget decisions.

And recall that a structural operating deficit is akin, in a family context, to borrowing to pay for the groceries even when the family’s employment and income position is pretty normal. A bad practice….for the family, and for the Crown.

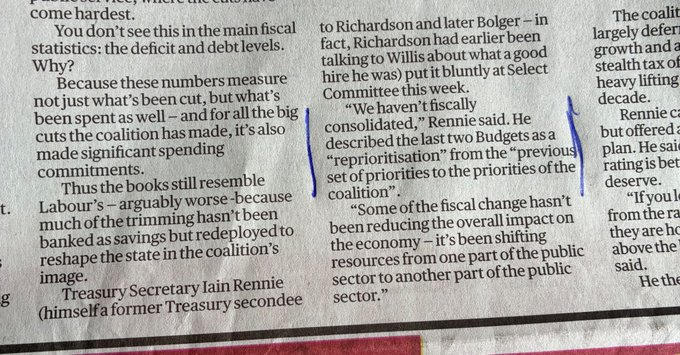

It was the Secretary to the Treasury himself who told FEC last week that there had been no fiscal consolidation under this government.

Things haven’t got radically worse in structural terms, but all this has come on the back on deficits under the previous government, and the ever-increasing ageing population fiscal pressures that Treasury has (among other people) warned about for years.

Of course, it hasn’t suited politicians on either side of the aisle to acknowledge Rennie’s point. The government has repeatedly suggested that their fiscal consolidation efforts have helped considerably in bringing about the large cuts in the OCR over the last 16 months, while the Opposition has been content to suggest that something akin to a “slash and burn” approach explains the weakness of the economy over that period. The numbers don’t back up either side – which surely their smarter people actually knew? – because there has been no fiscal consolidation. Sure, the government has cut some spending, but those savings have been (slightly) more than outweighed by new spending. Consistent with that. core Crown expenses as a share of GDP for 2025/26 were estimated at Budget time to be 32.9 per cent of GDP, up slightly on the previous year, and a full percentage point higher than the last full year for which Labour had been responsible. All those numbers are in the public domain, but….politicians……. (In the last full year pre Covid, by the way, spending was 28.0 per cent of GDP.)

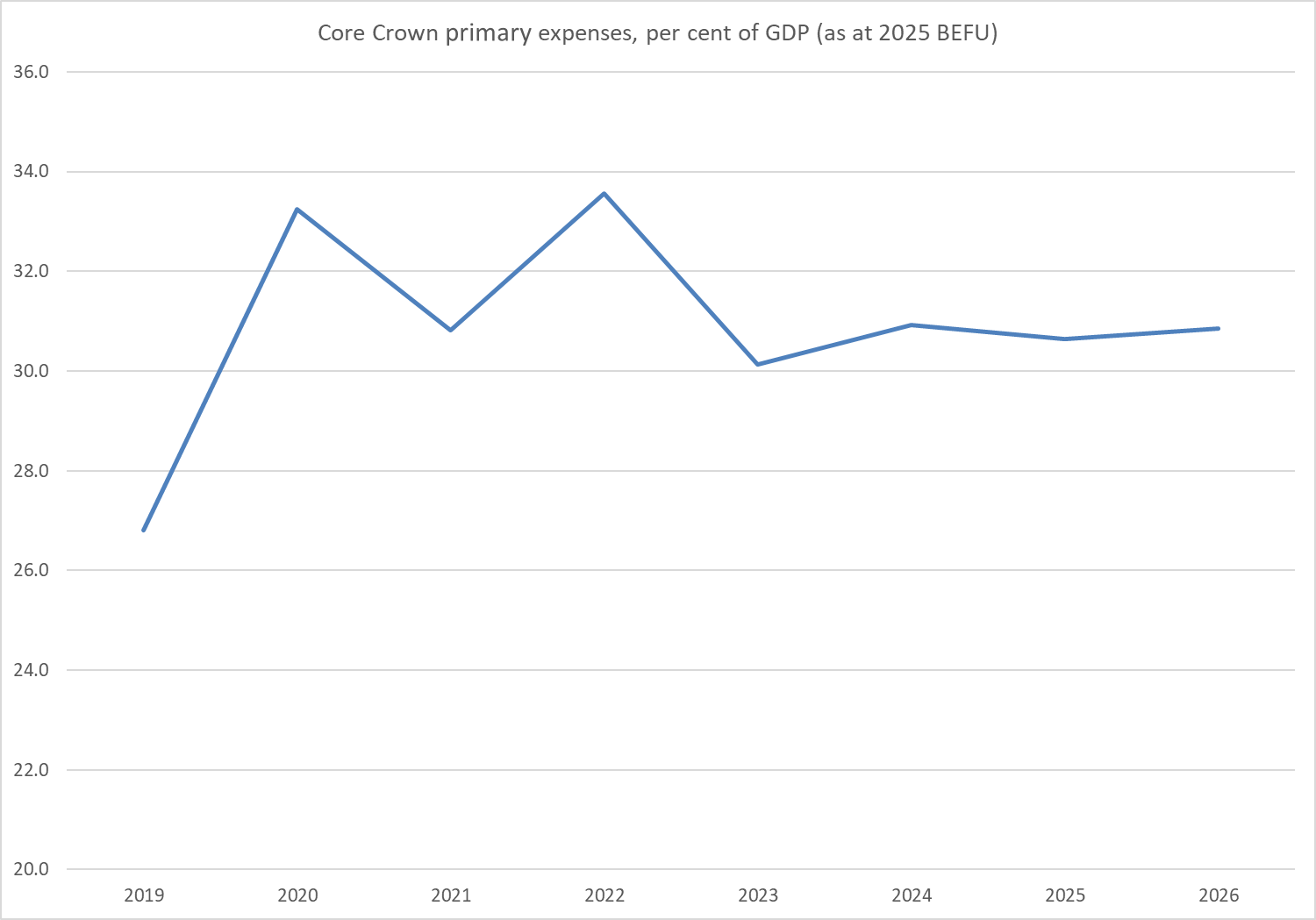

Ah, you might be thinking, but what about the interest burden run up by the accumulated deficits of recent years. Surely the incoming government was pretty much stuck with that, making overall expenditure cuts more difficult? And there is something to that, so in this chart I show primary spending (ie excluding the finance costs line from the core Crown expenses table).

It doesn’t really make much difference to the picture: primary spending is still a) far above levels for the June 2019 year (last pre Covid), and b) higher than in the last full year of the previous government, both as a share of GDP.

Spending levels aren’t really my focus. If governments want to spend more then so be it, provided they raise the taxes to pay for the spending. This government simply hasn’t done that, and so the structural deficits stay large, and have been widened a bit (an active choice, not a passive outcome).

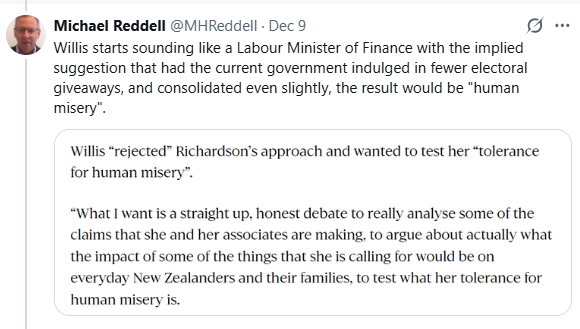

In the last couple of days there has been something of a spat between the current Minister of Finance, Nicola Willis, and her National predecessor Ruth Richardson. It seems there is to be a debate between them, after the HYEFU numbers come out next week. But if no one ever really expected Nicola Willis to take anything like a Ruth Richardson approach to public finances, her comments yesterday (as reported in The Post, still seemed extraordinary.

Can the Minister really have been serious in suggesting that any fiscal consolidation – and recall she did none – would have come only at the cost of “human misery”? Fewer film subsidies for example? Or cutting the Reserve Bank budget back a bit more? Or…… (and there is a long list of new initiatives, all choices)? Really?

I’m not overly interested in relitigating the Richardson record, particularly in 1990/91. One can mount an argument that by the time National took office in late 1990, there was already a primary surplus – itself usually sufficient over time to bring finances into order – with the high interest costs themselves somewhat exaggerated (in terms of real burden) by the persistently high inflation of the previous few years. And, as it turned out, even the return to headline surpluses took place sooner than had generally been expected after the 1990 and 1991 fiscal cuts (I was co-author of a Reserve Bank Bulletin article that attracted the ire of Michael Cullen for suggesting that surpluses might not be too far away, and even we were too pessimistic). All that said, fear of large credit rating downgrades was a major consideration at the end of 1990 and into early 1991, and the second failure of the BNZ wasn’t exactly confidence-enhancing. (Then again, the demographics were much less unfavourable back then – in fact quite favourable for the following decade or so, given low birth rates during the Great Depression.)

But whether or not the full extent of the fiscal adjustments back then were strictly necessary is beside the point now. We have much better fiscal data and analytical models, and we have substantial structural deficits on which the government has chosen to make no inroads at all, all while also doing nothing about the medium-term demographic pressures on government finances. The Minister is quoted in the Herald this morning as suggesting (in effect) that the lady’s not for turning, and that she is keeping right on with her borrow and hope strategy – hoping, no doubt genuinely, that one day something will turn up and the deficits she has chosen to run will just go away. If they don’t, we are on a path that – persisted with – takes us in the same direction as, for example, the UK, once – not that long ago – an only modestly indebted advanced economy.

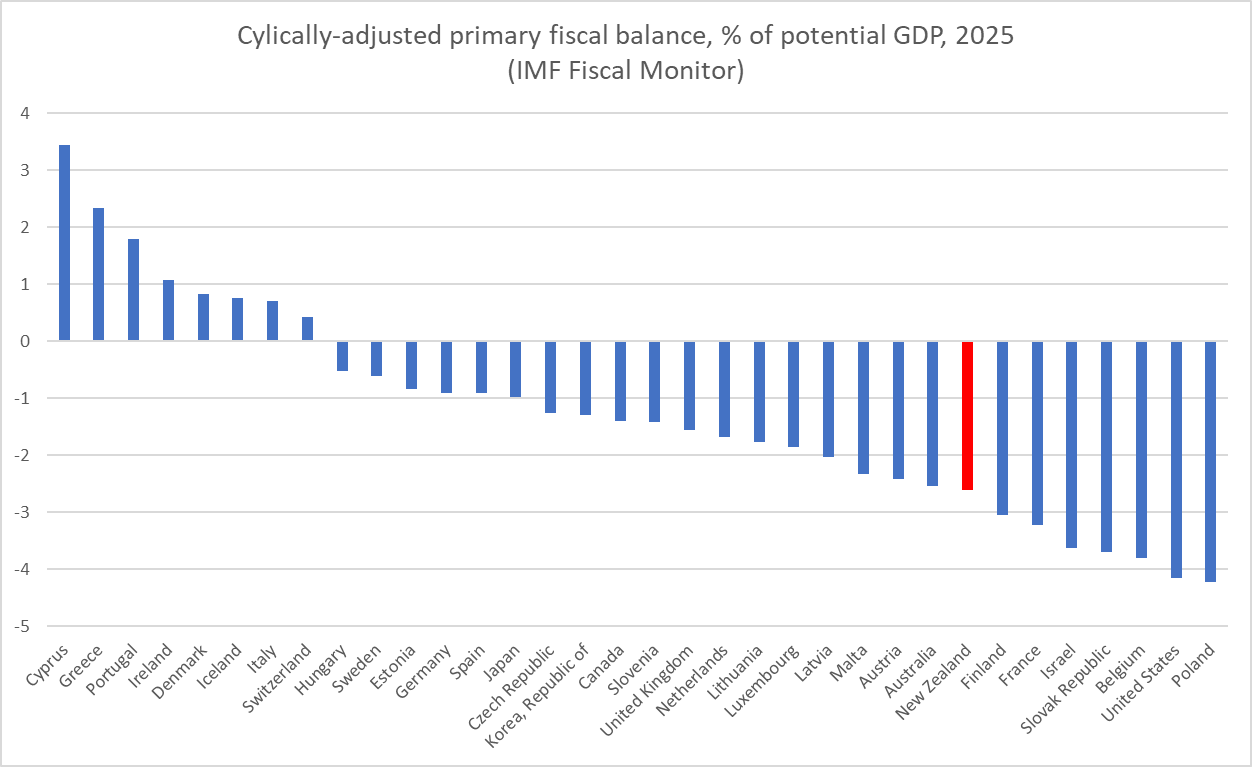

Cross-country comparisons of fiscal situations aren’t made easy by the way New Zealand presents its own data (useful for some purposes, but rendering comparisons hard). But twice a year the IMF produces a Fiscal Monitor publication with a range of indicators presented on a comparable basis across countries. This chart, using data from the October issue, shows the cyclically-adjusted primary balance for New Zealand and other advanced countries (these are overall balances, not operating ones). There are countries running larger deficits, but most advanced economies are running much deficits or even primary surpluses.

When it comes to deficits, the New Zealand government is choosing to do poorly on almost metric you choose to name (history, cross-country comparisons, expectations of the Public Finance Act). And it is choosing to do nothing about it. With an election year next year, not a time known for fiscal consolidation.

I had noticed reports that the Taxpayers’ Union was launching its own campaign on these issues, and the government’s fiscal fecklessness – choosing to do nothing about fixing a problem they inherited. I don’t have anything to do with that but while I was typing this a courier turned up with the props they are distributing to journalists and commentators. I’m sure we’ll enjoy their fudge.

Is it a fiscal fudge though? More like open and outright bad, and rather irresponsible, choices. We need something better.

A couple of weeks ago the editor of Central Banking magazine (something of an house journal for central bankers, and for whom I’ve done book reviews for some years) invited me to write a fairly full article for a non-NZ audience on the extraordinary events of recent months. The request/invitation was for a piece along the following lines:

“The aim would be to provide readers with an insight into how a highly respected institution (internationally, too) ended up in a position where both its top two officials were forced to resign and (perhaps) what steps could to be taken to redress the matter and restore the RBNZ’s reputation for sound governance?”

Having been so caught up in the unfolding detail, writing something like that proved to be a useful discipline, trying to stand back just a little and tell a story.

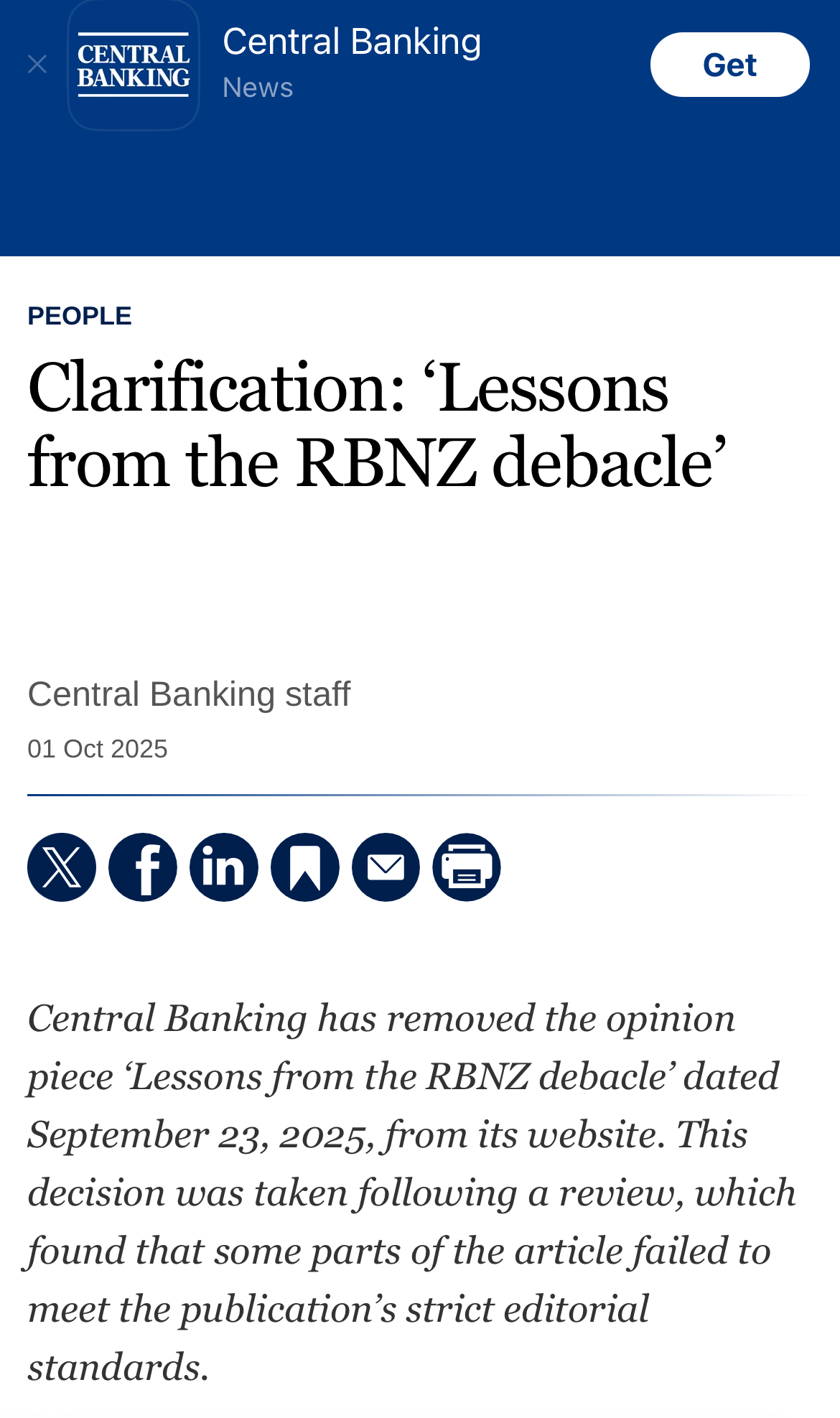

I wrote the article in the couple of days before we left on holiday, answered the follow up questions, and then Central Banking published the final version on their website yesterday morning (there is a paywall but registration should provide access)

[Link deleted as no longer relevant – see below]

There are only trivial differences between draft below and the final version, mostly the addition [UPDATE: by Central Banking] of various references/footnotes to the published version.

[UPDATE: Both I and Central Banking magazine have received demands to retract and apologise for the article under threat of legal proceedings by Adrian Orr, who appears to have objected to aspects of how his time in office, as a senior public figure and Governor of the Reserve Bank of New Zealand, was characterised. Central Banking has for now removed the article (link above) for further review. I posted the article here initially mainly to help readers who had had difficulty getting free access to the original via registration on the Central Banking website. As I’m currently travelling and cannot easily modify the text to make clear and extensively document a few points I have chosen to delete the article here as well.]

[FURTHER UPDATE 1 Oct: I have now been advised that there has been a “confidential settlement” between Orr and Central Banking magazine’s owner, under which they have agreed to remove the article permanently. The following statement now appears on the Central Banking website.]

UPDATE 21 October

I have decided that I will not republish the text of the article I wrote for Central Banking here, even with amendments. The piece had been written for an overseas audience, and through the sort of lens the magazine had requested. There is copious material on my blog on the events of the last two years, pre and post Orr’s exit, and more snippets have emerged in recent weeks. I hope at some stage to produce a NZ-focused summary account and analysis of those events.

UPDATE: 24 November

Among Orr’s claims has been that in my opinion piece I had alleged that he had “bullied his staff”. I was surprised by this claim. Several weeks ago I asked my lawyers to communicate with his to make clear that I had not made any such claim (and had not intended to do so and did not intend to do so now) and expressed my regrets if Mr Orr had read the text in the way suggested.

On two separate themes; aggregate fiscal policy, and the Investment Boost initiative.

Aggregate fiscal policy

Over the weekend for some reason I was prompted to look up the Budget Responsibility Rules that Labour and the Greens committed to in early 2017 (my commentary on them here). At the time, the intention seemed to be to fix in the public mind a sense that these two parties of the left would nonetheless be responsible and prudent fiscal managers (as I recall a fair bit of the more left wing parts of the bases of the two parties lamented the agreement for giving much too much ground to what might have been thought of as orthodoxy).

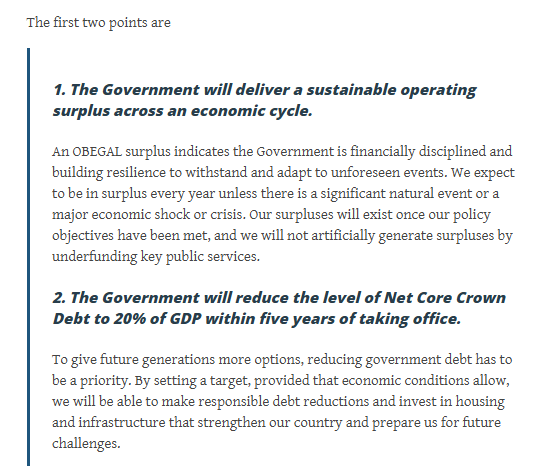

And what were they promising?

The debt measure they were using at time had been 24.6 per cent of GDP in June 2016.

To which one can only say, those were the days:

the last time there was an OBEGAL surplus was the year to June 2019, and neither government nor opposition now seem bothered by the forecast of another 3.4 per cent of GDP deficit in 25/26 (just the same as the latest estimate for 24/25). Under the current government, the preferred deficit measure has been changed, against Treasury advice, to make things seem less bad. The current government’s long-term fiscal objectives (in the Fiscal Strategy Report) still include maintaining on average “over a reasonable period of time” a zero operating deficit, but there is little practical sign it means anything to them (or that Labour now would be less bad)

core Crown expenses are projected to be 32.9 per cent of GDP in 25/26, up slightly from 32.7 per cent in 24/25, and down only a touch on the 33 per cent actual for 23/24. Back when Labour and the Greens made those 2017 commitments core Crown expenses were a touch under 30 per cent.

debt measures have chopped and changed (and the current government was stuck with the additional debt their predecessors took on, although have not hesitated to take on much more since). These days, net core Crown debt is about 42 per cent of GDP. The government’s long-term fiscal goal is stated to be getting into, and keeping that measure in, a range of 20-40 per cent of GDP, but even on their rose-tinted fiscal forecasts that measure is projected to be 45.5 per cent of GDP by June 2029 (NB, that will be seven years on from the end of Covid as a big budgetary item). Meanwhile, Labour seems uncertain whether they’d attempt to even keep this debt measure below 50 per cent of GDP.

A political party today that seriously pledged to do what Labour and the Greens promised in 2017 to do (and by 2019, net core Crown debt was below 20 per cent, OBEGAL was in surplus, and core Crown expenses were below 30 per cent of GDP) would almost certainly be slammed as dangerous, extremist, unrealistic etc. So far have things fallen, under Labour and under National.

Meanwhile, too many journalists still seem to accord some degree of seriousness to fiscal projections for the end of the forecast horizon (four years out, so currently the year to June 2029). When the date for the crossover point from deficit to surplus keeps getting pushed out (and more recently, the Minister’s definition changes to make things easier), people should eventually realise that there is little or no substance to these numbers. They might be generated by The Treasury, but they aren’t some sort of best unconditional forecast, but rather the best forecast conditional on whatever successive ministers tell Treasury will be their policy for several years ahead (the end of the forecast period always, by construction) being well beyond the following election). The problem is that even if ministers honestly believe what they tell Treasury at any point in time (and probably they mostly do), it isn’t then anything more than a statement of good intention, perhaps even wishful thinking.

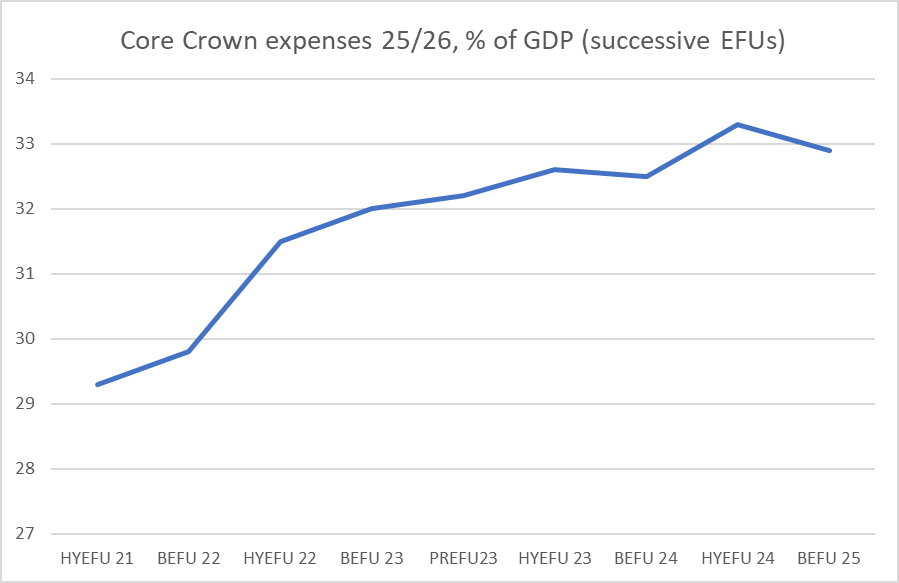

As an illustration of the point, consider this chart which shows projected core Crown expenses for 2025/26 as a share of GDP in successive Treasury economic and fiscal updates, going back to the end of 2021. The biggest further increases happened under Labour, but the line has continued to trend up under the current government.

Now, sure, further out the projections show core Crown expenses falling as a share of GDP, but that is sort of my point. Such projections are just vapourware. Exactly the same trend showed in the projections Treasury did under Labour (HYEFU21 to PREFU23 in this chart). It is easy, and perhaps appealing, to show such downward trends in future. It is quite another thing – politically rather than technically – to actually deliver. In both of the last two Budgets there has been plenty of hullabaloo (from politicians left and right) about expenditure cuts. But whatever the merits of those cuts, the bottom line remains that most of the proceeds have been used to increase other spending (some tax cuts last year)….and thus core Crown spending as a share of GDP is not actually falling.

Journalists, in particular (since politicians will politick), would be well-advised to ignore pretty much everything in the Treasury fiscal forecasts beyond the financial year to which the Budget actually relates (25/26 in this case), the year for which Parliament is actually being asked to make specific concrete appropriations. Most of the rest is vapourware.

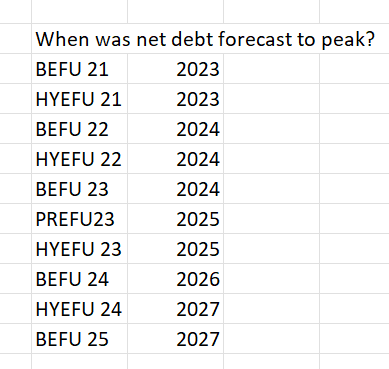

In a similar vein, here is a little table I stuck on Twitter on Saturday. The peak in net debt remains consistently two years ahead of whichever of five years’ Budgets one is looking at.

The government’s fiscal strategy seems to be not very different from that of the last couple of years of the previous government – do nothing about the long-term and in the short-term spend just as much as you possibly can without scaring the horses by blowing out the fiscal projections for net debt peaks and deficit crossovers too much in any one go.

Treasury are somewhat caught in the middle in all this. They have to forecast on the basis of fiscal policy as communicated by the Minister. That might be inescapable, but as I’ve argued previously in a PREFU context, maybe it would make sense to require Treasury to do a parallel set of forecasts showing the main fiscal variables on (a) unchanged tax rates (as at present), and b) maintaining the real per capita level of central government purchases (health, education, defence, Police etc) and the current programmes of transfers and income support. Those latter shouldn’t of course be treated as set in stone – efficiencies can be made, and different governments can have different priorities – but the expected cost if none of the expected deliverables are changed is still useful information, both for ministers (who may well already get something similar) and those seeking to hold them to account.

Investment Boost

Having been promised, by the Minister of Finance herself, “bold steps” in the Budget to address economic growth and productivity underperformance, in the end it all came down to a single measure, the so-called Investment Boost. In my quick post last Thursday I was mostly focused on the fact of the single measure and the rather underwhelming forecast change to our longer-term growth prospects (the level of GDP lifts by 1 per cent, not getting there fully for more than 20 years). [Note that this is quite similar to the then-estimated long-run effect of the 2010 tax-switch reform, which involved a switch from personal income to consumption tax and a slight increase in the corporate tax burden.] Considered against the size of gap between New Zealand average productivity and that of OECD leaders (60 per cent or more), it would represent little more than rounding error, even if the case for the new policy measure itself was strong.

I don’t envy IRD and Treasury having to come up with estimates of the economywide long-term impact of an intervention like this investment incentive. Their Regulatory Impact Statement is here, and it reports that while there have been various experiments with such policy interventions in other countries in fact there doesn’t seem to be much in the way of robust evaluations (and often these investment incentives have either been time-limited and/or applying to a materially more restricted range of assets than Investment Boost).

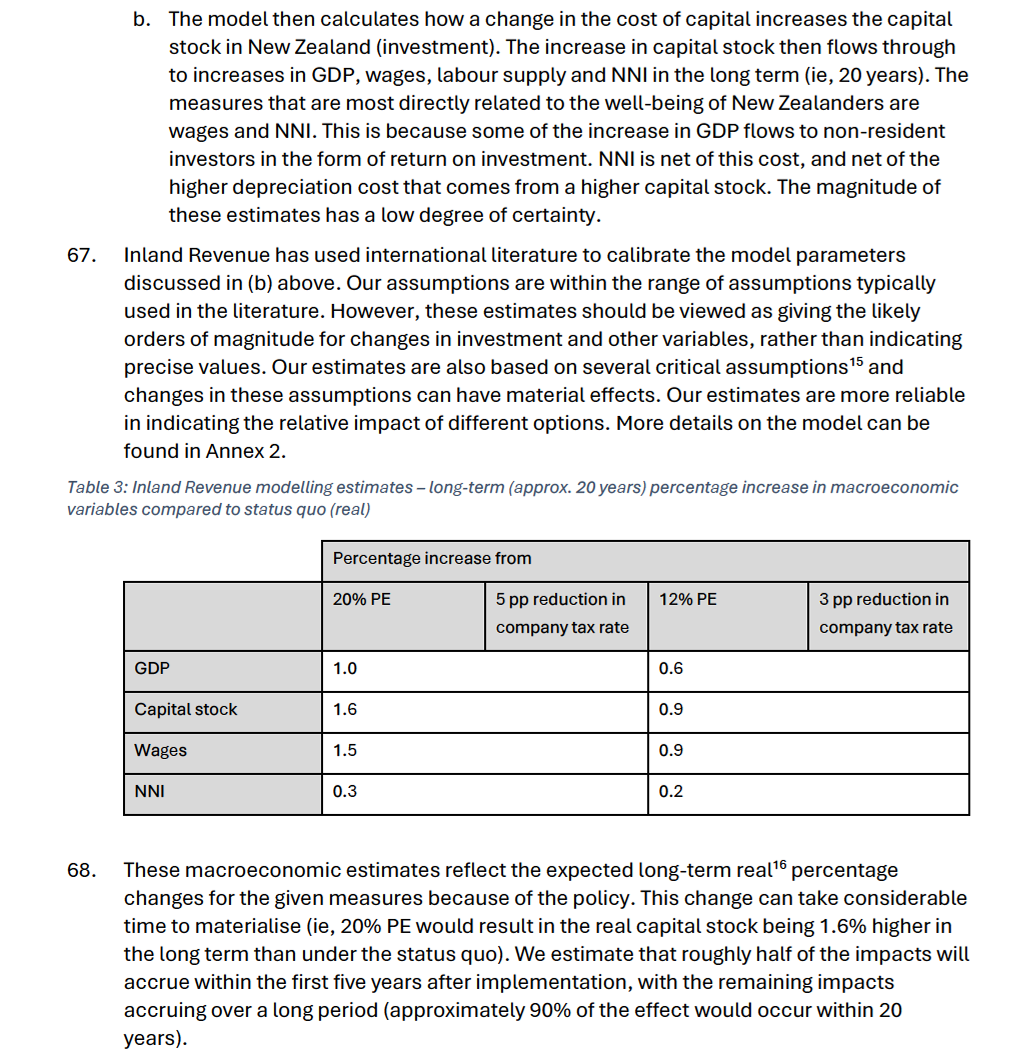

This is the bit of the RIS where they describe the economywide results

Note that in the new steady state (many years hence) GDP is 1 per cent higher than otherwise, and the capital stock is 1.6 per cent higher. Since it is stated (and both IRD and the Minister have confirmed) that the results include an increase in jobs/hours (increase in total use of labour), it is a bit difficult to see how there is likely to be any material increase in total factor productivity at all. Among the other oddities is that if total wages are rising by more than GDP, and yet the capital stock in increasing even more, the model must be generating quite a reduction in rates of return to capital. Why that is, and how plausible it is, I’ll leave to the specialists.

But perhaps more worthy of attention is that last line in the table. NNI is net national income (ie net of depreciation, and national= benefits to New Zealand residents, as distinct from “domestic” which is things generated in New Zealand, whether by New Zealand residents or foreign investors), and by far the best measure of the economic gains (or otherwise) to New Zealand. Note that NNI in New Zealand is currently about 80 per cent GDP, so – on this particular model – only 25 per cent of the lift in GDP flows through to economic benefits to New Zealand residents ((0.3/1)*0.8). Most of the GDP gains accrue to foreign investors (something IRD is certainly not hiding, but obviously wasn’t being advertised by the government). Now, to be clear, I am all in favour of facilating foreign investment, but as with almost any policy intervention the test is whether whatever benefits foreigners may pick up result in sufficient gains to New Zealanders. For interventions that cost NZ taxpayers’ lots of money (as this one does), gains to foreigners are not themselves a benefit. The question is whether they enable greater benefits for New Zealanders.

(Note that IRD makes the point that “the magnitude of these [absolute] estimates has a low degree of certainty”. But their best estimates are, presumably, what ministers had available to them.)

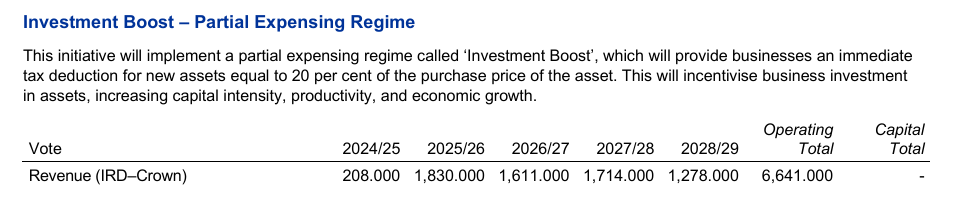

How large is the direct fiscal cost?

This is from the Summary of Initiatives document

Note that the cost in the early years is considerably higher than that by 2028/29. I presume that is reflecting the fact that for most investment the Investment Boost deduction is “just” changing the timing of the deduction (you get to write off 20 per cent of the cost in the first year, but then subsequent depreciation deductions over the remaining life of the asset are correspondingly reduced: for shorter-lived assets those reduced future deductions is significant once you are beyond the purchase year). In the RIS it is stated that that 2028/29 number is also the one they assume for the out-years (although presumably adjusting for inflation, and with a trend increase in the level of business investment – population growth etc).

And how much is $1278m per annum relative to net national income? Net national income, based on Treasury’s GDP forecasts, for 2028/29 is likely to be around $420 billion (80% of forecast GDP of $524bn), so the direct annual fiscal cost to New Zealand residents of this policy, once we get through the more expensive introductory phase, looks to be about 0.3 per cent of NNI. And that cost is being incurred every year, even though the NNI income gains don’t get up to 0.3 per cent for 20 years or more. Apply a discount rate of 8 per cent (as surely Treasury should insist on for what is a commercially-focused policy) and things could quickly look not overly attractive if a proper cost-benefit analysis had been done (it wasn’t). I guess there will be additional tax revenue on the additional GDP (tax/GDP is about 28 per cent), but again you don’t earn the tax until the real GDP benefits gradually flow through, while the fiscal cost is frontloaded. Time costs.

So perhaps the policy is net beneficial to New Zealanders (even if the scale is small). But is it an appropriate policy?

Reflecting on it further over the weekend, I’m not sure it is really either appropriate or particularly intellectually coherent. (I could add that I’m not greatly bothered by it being uncapped – so, for example, is the unemployment benefit which costs what it costs depending how many people end up unemployed, or interest deductibility etc. Government champions will no doubt add that since the point is to increase investment, if there is even more new investment than IRD/Treasury forecasts that is likely to be a good thing, not a bad thing. In some commentary I wondered if people realised that it is not a 20% grant, but rather a reduction in first year tax of 5.6 per cent of the purchase price (0.28*20).)

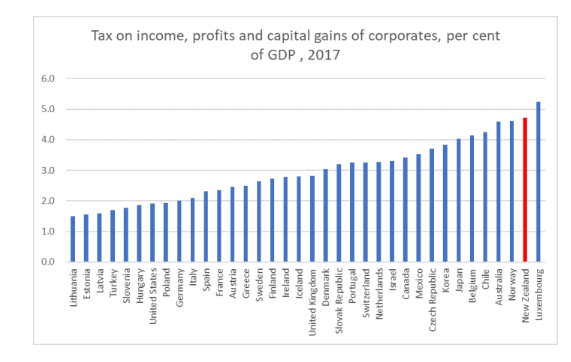

To me, there is little serious doubt that New Zealand has overtaxed business income. IRD show some of the cross-country comparisons, and they could have added this one (which is a few years old but was in the background documents for the Tax Working Group).

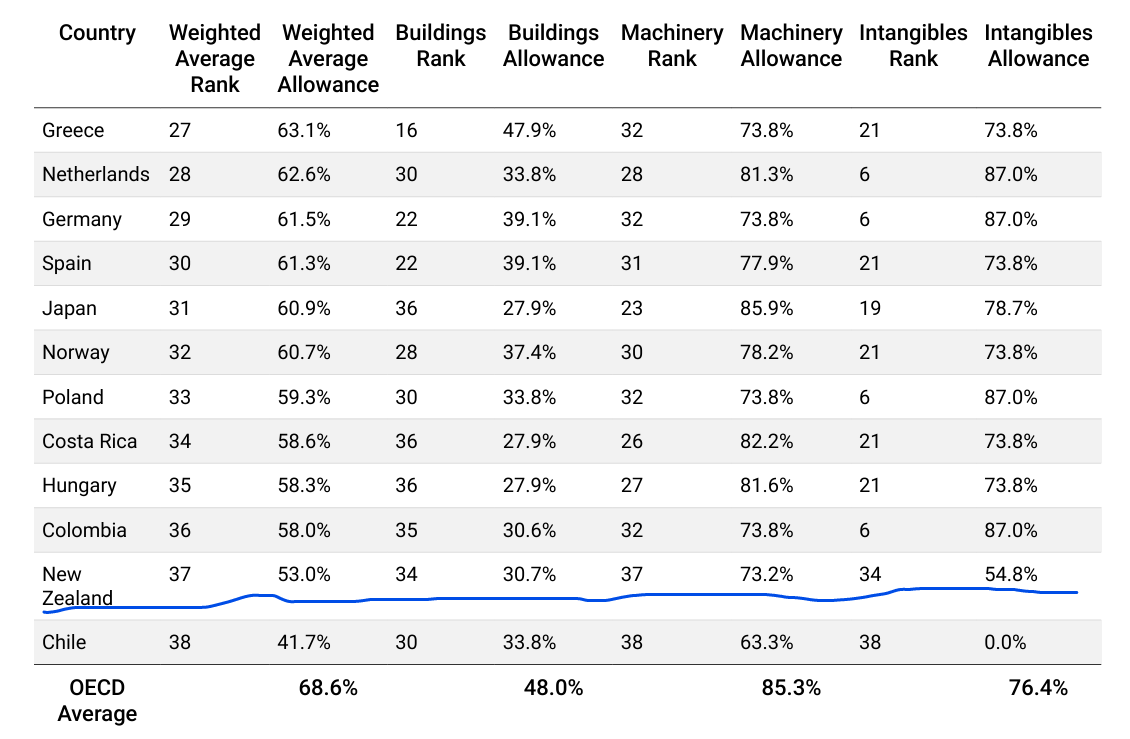

They could also have cited the Tax Foundation’s recent piece on capital cost recovery, depreciation etc. This was the bottom (worst) bit of their table for OECD countries showing the net present value of total write-offs over the life of an asset

Very few countries, for example, do as they should and inflation-adjust the value of assets to allow full real economic depreciation over the life of an asset.

But I’m still left uneasy about this particular Investment Boost initiative.

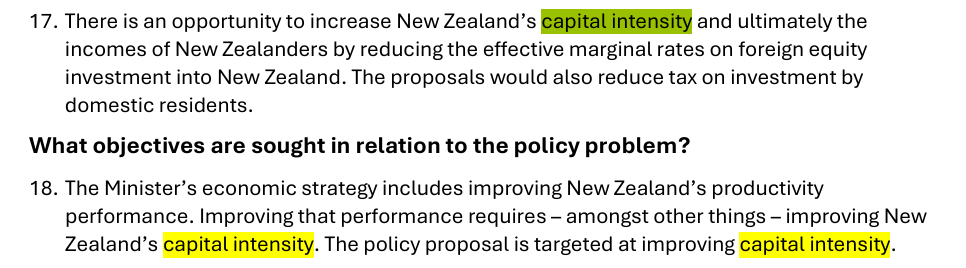

You hear a lot these days about “capital intensity” (lack thereof). For years, Treasury has talked up this rather mechanical growth accounting decomposition – business investment has been quite modest for decades, and so capital stock per worker has tended to lag – and this year ministers have taken to championing the line. And sure enough, from the RIS

There aren’t (in the views of ministers) enough capital assets, so we’ll offer an incentive (quite an expensive one) to encourage firms to have more capital assets.

The problem with this mentality – whether it is officials or ministers talking – is that it too easily fixates on symptoms rather than underlying economic causes. It never asks the question as to what is is about the New Zealand economy or its policy settings that means either New Zealand firms or foreign ones don’t seem to find that many profitable (after tax) opportunities available here (let alone look at what might be the best, or most cost-effective ways of addressing any issues thus identified.)

[Perhaps I should add here I’m old enough – as is Nicola Willis – to have been around when, a mere 15 years ago, New Zealand’s accelerated depreciation regime was scrapped – something signed off by the government (for which Willis worked at the time) and enthusiastically welcomed by Treasury (where I was working).]

Instead, there seems to have been a lurch to subsidise (one group of) inputs, even though outputs and outcomes are the things we should care about (much) more. Are more and more- highly-successful companies likely to also be engaging in more capital investment? Of course, but that is a different framing than one of “if we subsidise more capital goods will we see more highly successful companies?”

There are reasons to be ambivalent at best. For example, the goal of the policy appears to be more new investment (rather than higher GDP or NNI themselves), and thus you can get the subsidy for buying a new asset (or a used one from abroad), but not for buying an existing asset which some other might no longer need, or not be using as efficiently as your firm perhaps might. A whole new wedge is inserted, actively discouraging more efficient use of existing resources (TFP) in favour of subsidising more resources. Is that effect likely to be small enough not to worry about? Hard to tell, but (for example) very long-lived assets like factories and office buildings are caught in the net, and it is quite likely that a building won’t have the same best owner for its entire life. And what about vehicles? Some tradesman’s business fails and there is a vehicle to be sold – there is less likely to be a good recovery when a new or expanding business can get a subsidy on a new asset, but not on picking up an under-utilised existing one. And if, for small businesses in particular, there is an element of personal consumption in some business assets (be it the fancy ute or the higher-end-than-strictly-necessary laptop), lower rates of tax on business income would seem more likely to generate efficient outcomes than subsidising the purchase of capital assets. Again, perhaps small in the scheme of things, but not self-evidently an efficient approach.

Then, of course, there is the question of the intellectual coherence of the government’s approach to the taxation of business.

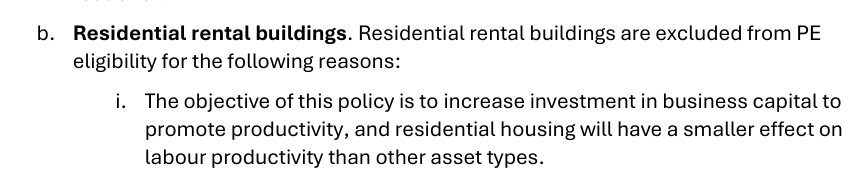

Last year, it was important (or so both government and Opposition believed) to remove tax depreciation from commercial buildings (otherwise the 2024 Budget numbers wouldn’t have added up), but this year new commercial buildings (including, according to the fact sheet, work already underway last Thursday) gets a 20 per cent deduction in the first year of purchase (absolutely huge upfront compared to the usual depreciation rates for buildings) – and since there is no clawback in reduced depreciation in later years, by far the biggest winners from this policy will be those adding new commercial buildings. So was tax policy last year correct – when it went one way on commercial buildings – or is correct this year, when it went quite the opposite direction? (And what was the net NNI effect of those two contradictory policy changes?)

Last year, the government also moved to reinstate interest deductibility in respect of residential rental property. The argument – which I supported totally – was that interest was and is a normal cost of doing business and as it was deductible for every other sort of company there were no good grounds for disallowing interest deductions on residential rentals. Firms need office, people need places to live, and in both cases owner-occupation will suit some but not others. So last year, residential rentals were a business like others, but this year……”residential buildings and most buildings used to provide accommodation are not eligible for Investment Boost – though there are explicit exceptions for some buildings such as hotels, hospitals, and rest homes”. Rest homes – you mean places where people live and are not owner-occupiers? I guess Rymans and the others will be happy, but where is the intellectual coherence? (And it is not as if the fact that depreciation is not allowed on residential rentals – itself a flawed policy- is a decent justification; after all, see above in respect of commercial buildings.)

Here is the main IRD/Treasury justification for excluding residential investment

As if the ultimate point was not improved household wellbeing, whether that arose via higher wages or lower real rental prices. And not a mention of last year’s policy stance, just officials and ministers again picking preferred types of capital assets.

I’m left rather ambivalent at best. There have been, and no doubt will be again (from whoever is in government) worse policies but this is simply a not very good one (despite the Minister touting apparent Treasury advice that there was something “optimal” about the 20 per cent). Had the government wanted to do something economically rational and rigorous around depreciation – see table above – it might have been better to have reinstated depreciation on buildings (residential and non) and inflation-indexed the depreciable values. But if it was coherent, it would have been a lot less catchy, since lots of machinery and software etc depreciates quickly and things like the inflation distortion matters less.

Finally, from a purely cyclical perspective, it isn’t impossible that there could be a larger short-term boost to demand and activity than implied by those long-term numbers.

Working back from the IRD cost estimate for 2025/26 ($1830m) and a company tax rate of 28 per cent suggests a base level of (covered) business investment of about $33bn. GDP is estimated at just over $450bn in 2025/26. Whatever the longer-term effects, perhaps there is reason to think the short-term lift to investment might exceed the long-term one: on the one hand, the enthusiasm effect among small businesses in particular (the policy seems to have gotten good headline reaction where it was presumably supposed to do so), and on the other, the risk/possibility that if there were to be a change of government after next year’s election this incentive could be wound back or abolished (the left would need money to fund their preferred initiatives, just as this government has – and the Greens, notably, have promised to increase company tax rates). If one were thinking of doing some capex in the next few years, the next 18 months or so might seem a particularly propitious time all else equal. A 10 per cent lift in business investment in a year would itself represent about a 0.7% lift to aggregate demand. At very least, and like all tweaky tool incentives, it will make for an interesting case study.

On Twitter on Saturday I indicated that there had been a mistake in my post from last Thursday in which I attempted to step through the Reserve Bank Funding Agreement issues. Making mistakes (there are two) is annoying and I don’t fully understand how I did it (probably too much haste). I can only apologise to readers (and acknowledge that it was a sentence in the Herald’s Thomas Coughlan’s article on the Funding Agreement that prompted me to go back and check). The central point isn’t affected: real spending in the next couple of years is hardly cut at all from levels authorised by Grant Robertson just before the last election.

As it happens, since writing that post on Thursday morning a couple of other relevant documents have been released by the Reserve Bank. So, and at risk of some repetition, I’m going to attempt in this post to cover the full ground, focusing under three headings:

the change in approved spending from one Funding Agreement (Robertson’s) to the next (Willis’s)

the change in actual spending, and

what seems to have gone on regarding last year’s Reserve Bank Budget and their bids for the new (just signed) Funding Agreement.

This post is long. I have a summary in six bullet points at the end.

From one Funding Agreement to the other

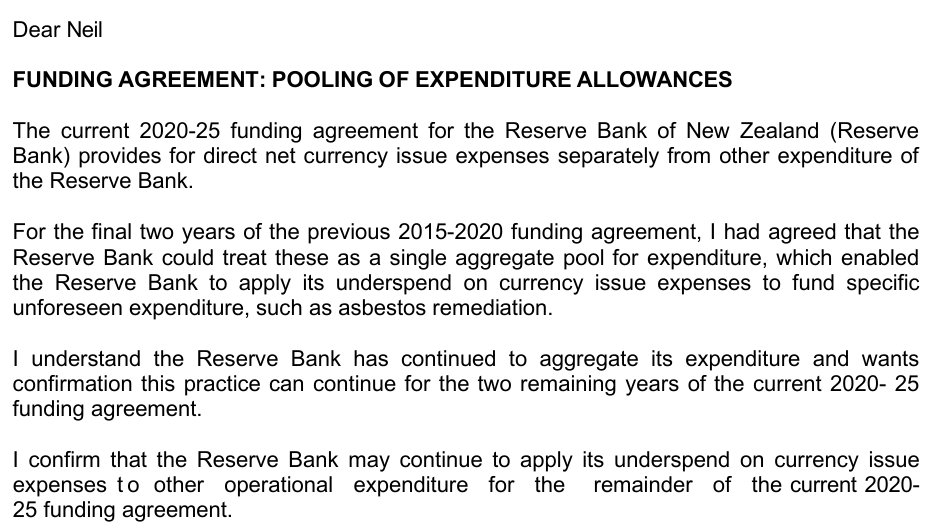

In the Funding Agreement for the period 2020-25, as varied by agreement with Grant Robertson in August 2023, two classes of operating expenses are separately provided for. A fairly large chunk of the Bank’s operating expenses (around $30m a year) is not covered by the Funding Agreement at all – for reasons good and less so. But of those that are dealt with by the Funding Agreement, the first class was what we might call “core” operating expenses (where $149.44m was the allowable expenditure for 2024/25) and the second is “net direct currency issue expenses” ($14.5 m for 2024/25).

In the new Funding Agreement released last week there is no longer a set of annual allowances for the currency issue expenses. Instead, under the “Excluded expenditure” heading there is provision for the Bank to spend up to $65m in total on this item over the full five years covered by the Agreement.

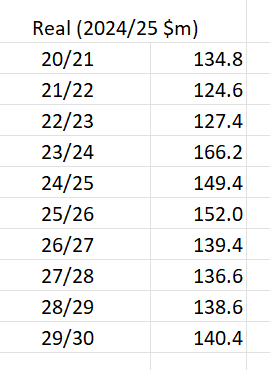

Consistent with that, in Thursday’s post I included this table, which covers the “core operating expenses” covered by the Funding Agrement in real, inflation-adjusted, terms, for the periods covered by the old and new agreements

As you can see, approved core operating expenses in the coming financial year ($152m) are actually a couple of per cent higher in real terms than those Grant Robertson had approved for the year ending in June ($149.4m). Over the remaining life of the agreement the numbers are lower (in 29/30 the approved allowance is 6 per cent below the level Robertson had approved for 24/25).

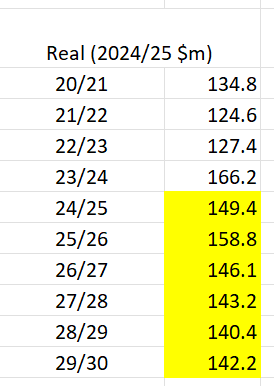

However, in the new Funding Agreement a number of new items are excluded from being counted against that spending limit. Thus, a true apples for apples comparison with approved spending levels under the old agreement would mean higher numbers for the 2025 to 2030 years. Only one of these new exclusions is quantified: an average of $5m a year for the next three years is allowed for implementing the new Deposit Takers Act (which has been being implemented gradually including over the last two years – it was part of the justification for Robertson revising up approved funding in August 2023). Other items aren’t quantified, including operating expenses associated with such potentially costly items as work on a Central Bank Digital Currency and those operating expenses associated with refurbishing or replacing the head office building. If we allowed another couple of million per annum for these other new exclusions (aiming to be conservative – low end – in our guesses), we might end up (illustratively) with a table like this

where, say, even in 2026/27 approved real operating spending would be only 3 per cent lower than the level Grant Robertson had approved for 2024/25.

Note too that the Bank’s actual and budget (for 24/25) spending on those net direct currency expenses over the five years of the last Funding Agreement was about $32 million. Although the new Funding Agreement does not provide annual limits for this item, it allows $65 million spending on it over five years in total – much higher than recent actual spending, and not very different from what was allowed in this component of the previous (2020) Funding Agreement (although note some unexpected inflation since 2020)

Overall, the new Funding Agreement doesn’t represent much fiscal restraint relative to the last approved levels by Grant Robertson in August 2023.

And it isn’t as if the Bank had been consistently abstemious over the years.

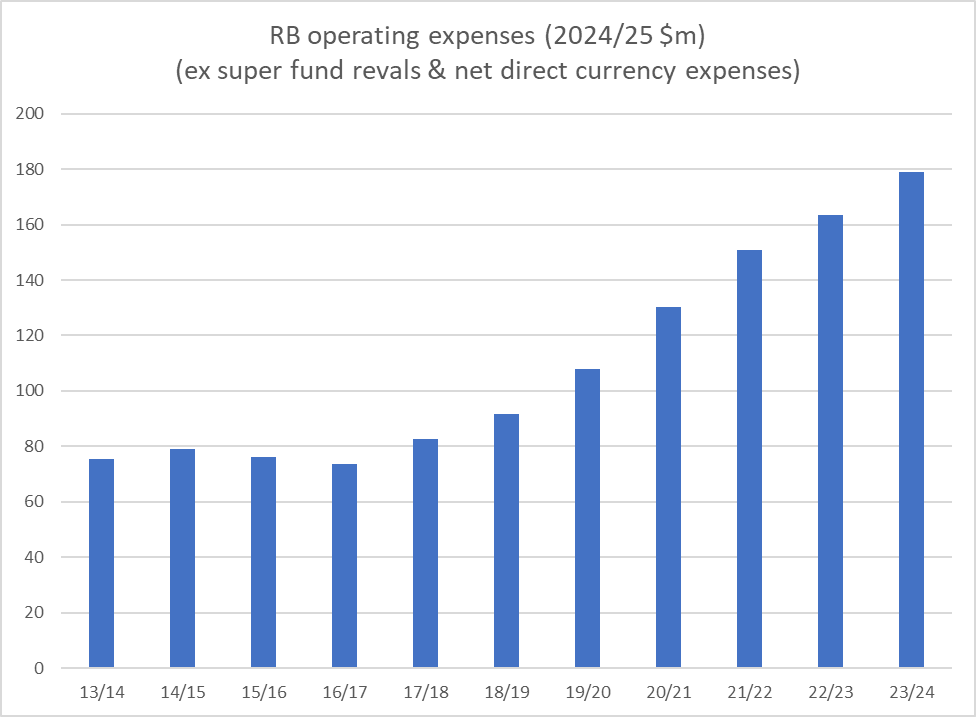

Because the definitions of what is and isn’t covered by Funding Agreements has changed over the years, it can be helpful to look at the trend in operating expenses, as disclosed in successive Annual Reports.

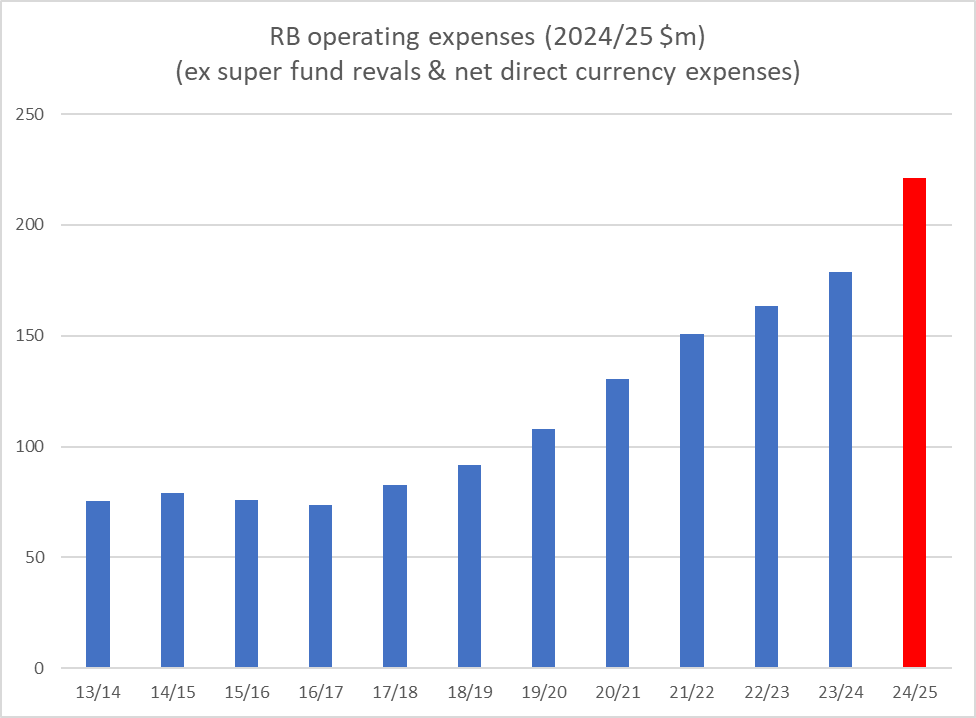

This chart shows actual total operating expenses in real inflation-adjusted terms (excluding actuarial gains/losses on the staff super fund, which aren’t controllable, and the net direct currency expenses item). Adrian Orr became Governor in March 2018 and real spending in 2023/24 (the last year for which we have actual data) was already more than twice 2017/18 levels.

Funding agreement vs actual and budgeted spending

The Funding Agreements cover five financial years. The Act is quite clear that when an amount is stated for each of those five financial years, that is the intended limit for that year. The Bank is not free to underspend in some years and overspend in others.

Note, however, that there is no direct disciplining mechanism. If the Bank overspends in total, or underspends in some years and overspends in others, there are no (automatic) consequences. And as I recall it, including my time on the senior management group at the Bank (long ago now), there used to be a practical view that small unders and overs in individual years weren’t too concerning, particularly so long as spending over the full five years stayed under the total allowed in the Funding Agreement.

The Bank discloses in each Annual Report how its spending on Funding Agreement items has aligned with the amount provided for each year in the relevant Funding Agreement.

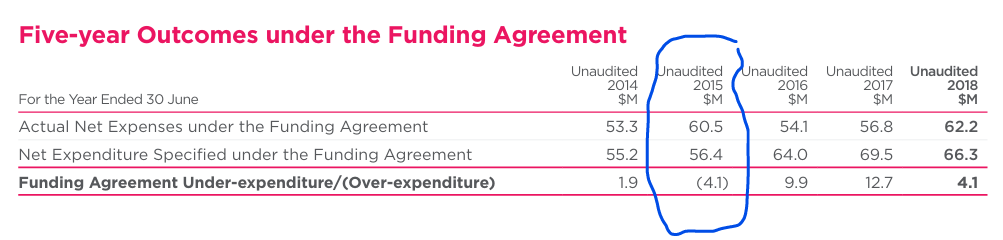

Here is an example from the 2018 Annual Report

This period happened to straddle two different Funding Agreements (and mostly Graeme Wheeler’s stewardship as Governor). Over the full five years, the Bank ran operating expenses below the Funding Agreement level. In 2014/15 they ran over the Funding Agreement amount, something that disconcerted management at the time (and prompted a round of redundancies and cost savings.

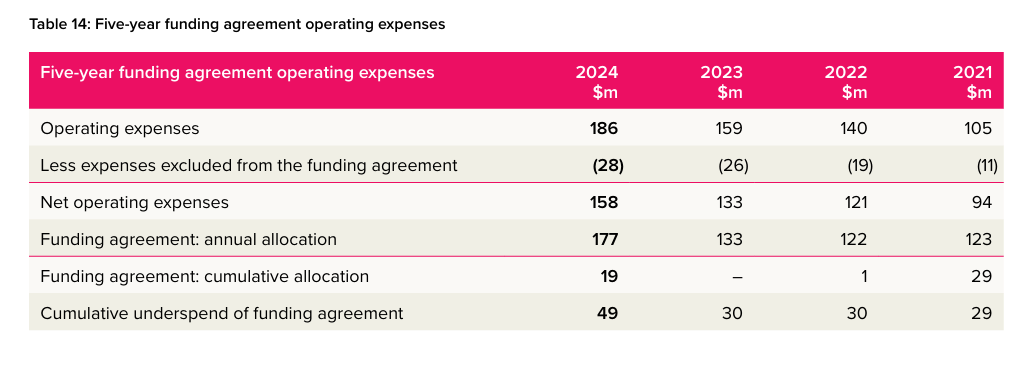

Here is a similar table from the 2024 Annual Report

Really big increases in operating spending had been allowed both in the original 2020 Funding Agreement and in the August 2023 variation that Orr, Quigley, and Robertson had signed just before the election.

You will note that in 2020/21 the Bank substantially underspent the Funding Agreement allocation (although operating spending under the Funding Agreement still increased by 13 per cent that year). In its 2021 Annual Report the Bank offers several factors as explanations for the underspend, but they mostly seem to come down to Covid (and a serious data breach the Bank experienced). I’m less interested in the specific explanations than in the final comment: “We expect this underspending to reverse in future years and the Bank to be within the five-year aggregate expenditure provided for in the funding agreement”.

Maybe that didn’t seem unreasonable at the time – Covid, after all, was out of blue for them (and all of us) – BUT (as noted above) the relevant provisions of the Act do not envisage or provide for carrying forward underspends from one year to the rest of the Funding Agreement period.

But then, as it happens, for the next two years, net operating expenses were almost bang on the Funding Agreement allowed amount (when the allowances for core operating expenses and currency issuance expenses were combined). But the Bank – management and Board – still seemed to think it was just fine to carry forward an underspend from years earlier. You can see that in the final line of the table.

You’ll also see in that table that there was a big increase (33 per cent) in approved Funding Agreement spending for 2023/24, made possible by the August 2023 variation. The Bank then underspent that allowance rather dramatically ($29m), even though they’d increased (funding agreement covered) actual operating expenses by almost 19 per cent in a single year. This was still a year (more than half of which occurred on the watch of the new government) in which they had increased actual FTE staff numbers by 91 (18 per cent). As for that delayed project spending, it doesn’t seem like great management and Board oversight given that they’d only got Funding Agreement variation approval as recently as August (ie already into the relevant financial year).

By the end of the 2023/24 year the Bank’s total (Funding Agreement) operating spending was a total of $49 million below the sum of the Funding Agreement limits for each of those four years. $19 million of that shortfall had occurred years earlier.

But what of it? Recall that under the Act, there really wasn’t discretion for the Bank’s management and Board simply to decide to shift large amounts of spending from one year to the next. (No one might have quibbled over a few million here or there – given the way the Funding Agreement system and legislation were set up – but…..this was $49 million).

And, by then, we had a new government, which had made quite a fuss in the election campaign around bloated public spending, and had started on cuts to most central government departments.

The Bank’s 24/25 budget, Statement of Performance Expectations, and 2025 Funding Agreement bids

Annual budgets are set by the Reserve Bank’s Board which now has full responsibility for the governance of the institution. The high-level budget numbers are published in a document, required by law, called the Statement of Performance Expectations. Last year’s was signed (by Governor and Board chair) on 21 June and included this table.

Here is the chart above updated for the Board-approved 24/25 budget

It was to be the largest percentage increase in core operating expenditure in any of the Orr (& Quigley) years (about 24 per cent in real terms).

The Bank does not report its budget on a Funding Agreement-consistent basis, but the proactively released Board minutes indicate that $31m of the operating expenses were on items not covered by the Funding Agreement. So $200 million was on item covered by the two Funding Agreement streams, up from $158m actual spending on these streams in 23/24 (the Board would not have had final 23/24 numbers when they approved the 24/25 budget on 20 June, but the estimates must have been pretty close).

How did this happen you might be wondering. After all, hadn’t the Minister of Finance handed down her overall government budget as recently as 30 May with a heavy, and very public, emphasis on expenditure savings and redirection of resources towards so-called frontline services? Those with access to the Minister might well ask her.

Perhaps you are wondering if the Board did all this 24/25 budgeting in secret, and the Minister of Finance simply didn’t know. But the numbers had to be included in the Statement of Performance Expectations (SPE) and the Minister had to be consulted on a draft of the SPE. In fact, the law says that a main point of the SPE is to enable the Minister to be involved

and the “how” is covered, among other sections, here

And it isn’t as if somehow the Bank overlooked the need to provide a draft to the Minister last year. The Board minutes for 20 June record that written comments (on the draft Statement of Intent and the draft SPE) had been received from both the Minister of Finance and Treasury and “had been incorporated”. There is no suggestion of any material difference of opinion, or of the Minister taking a harder line than the Board. It is really quite extraordinary…..coming just weeks after the expenditure saving and reallocating government budget. One of her agencies was going to increase spending by 25 per cent or so, in a single year.

What was the Minister thinking/doing? What was Treasury thinking/doing? (I have lodged an OIA asking for the comments from both of them on the draft SPE.)

Now, again if you were inclined to bend over backwards to excuse her responsibility you might note that the Minister of Finance could not formally stop the Bank’s Board setting the budget for 24/25 at any level it liked. The Bank has that degree of operational independence.

But…. she is the Minister of Finance and has a bully pulpit. Imagine if she’d told the Board “well, you can increase your budget by 25 per cent for this coming year if you like, but if you persist in doing so I will go public and excoriate you for a reckless and irresponsible use of public money, for operating in breach of the Funding Agreement, and for choices that are utterly out of step with the government’s wider fiscal priorities. Do we really suppose there’d have been a wave of public sympathy for the Board?

More directly, Board members are appointed by the Minister of Finance. Reserve Bank board members cannot be dismissed at will, only for cause. But the Reserve Bank Board chair’s term was due to expire on 30 June 2024. It had been widely assumed that, having been in place for many years, he’d be replaced by the new government. Being responsible for an egregiously large budget increase might have been just another reason to replace Quigley. Instead, Willis reappointed him, and as if to add insult to injury she announced that puzzling reappointment on 20 June, the very day the Board confirmed that huge operating expenses budget, that she’d had every chance to comment on.

Like many, I was genuinely mystified last June when Quigley was reappointed. Now that one realises (a) the timing and b) the huge budget increase he was overseeing I’m simply flabbergasted.

(Note that the 2024/25 Budget was so out of step with the Funding Agreement provisions/levels there would appear to have been – perhaps still would be – good grounds for the Minister to dismiss board members for cause (not one of them having recorded a dissent when the budget was adopted).)

Now, as a final effort towards trying to understand what she might have been thinking, perhaps the Minister was advised by the Board and management that the Bank was simply utilising the underspends from earlier in the Funding Agreement period. The Bank was claiming (see table above) that they had $49m up their sleeve. Add $49m to the Funding Agreement allowances of $149.4m for 24/25 core expenses and $14.5m for 24/25 net currency issuance expenses and you get $212.9m. Perhaps it looked as though the Bank’s big new budget ($200m on Funding Agreement items) was actually less than was allowed.

If the Bank claimed as much to the Minister, we might (at a pinch) excuse her. She is busy and you might assume the board of your central bank was giving you honest advice and an honest interpretation of the Funding Agreement and Act. But……she has an entire department of her own, The Treasury, supposedly expert in such stuff. And they should have told her in no uncertain terms that neither the Funding Agreement nor the Act envisaged carrying forward substantial underspends from past years to allow lots more spending in later years. To be consistent with the Funding Agreement, the Bank’s total (funding agreement covered) operational expenses could be no more than $163.5m in 2024/25. Not $200 million.

Why weren’t they (apparently) doing those basics properly? It is clear that they had seen the draft SPE and the Board minutes record regular senior-level engagement with Treasury (a couple of Treasury DCEs often attended a session with the Board, and sometimes the Secretary herself). They’d been overseeing the advice on the government budget, probably putting pressure on numerous departments to deliver savings. And yet the Bank’s Board adopted a budget with a 25 per cent or so increase in operating spending, and nothing seems to have been said or done.

All of which brings us to the 2025 Funding Agreement (bids and final settlement).

The Minister had written a Letter of Expectation to the Board chair in April stating, among other things,

The messaging seems pretty consistent with what the Minister had been saying in public (see references to the “fiscal sustainability programme”)

Here it is helpful that late last week the Bank finally get round to proactively releasing the Board minutes for the September quarter of last year. You may recall that in the paper to the Cabinet committee on the new Funding Agreement the Minister indicated that

This submission was approved at a meeting of the Board held in Auckland on 29 August late year. The minutes record as follows

It is quite explicit there that they had bumped up the 24/25 budget massively – using some illegitimate argument about carrying forward past underspending – not just to clear out some backlog one-offs, but providing a baseline for their bid for operating spending for the following five years. You’d think perhaps we were still in the era of Grant Robertson budgets. And although it is easy to focus on Adrian Orr as Governor, these bids – and the budgets – were the responsibility of the board, and particularly its chair, Neil Quigley.

But there are still puzzles. For example, note that in the paragraph above the one I highlighted the minutes record the Board’s understanding that “the Minister of Finance’s expectations for the funding proposal are met, including that multiple options for achieving savings are provided”. What, one is left wondering, led them to think that what they were bidding for had met the Minister’s expectations (presumably as conveyed not only in that April Letter of Expectation but in regular engagement with top Treasury officials)?