The CPI data out yesterday were not good news.

Annual headline inflation was, more or less as expected, down, but at around 6 per cent is miles from the 2 per cent target midpoint the Reserve Bank’s MPC has been required to focus on delivering. Much more importantly, core inflation measures show little or no sign of any reduction.

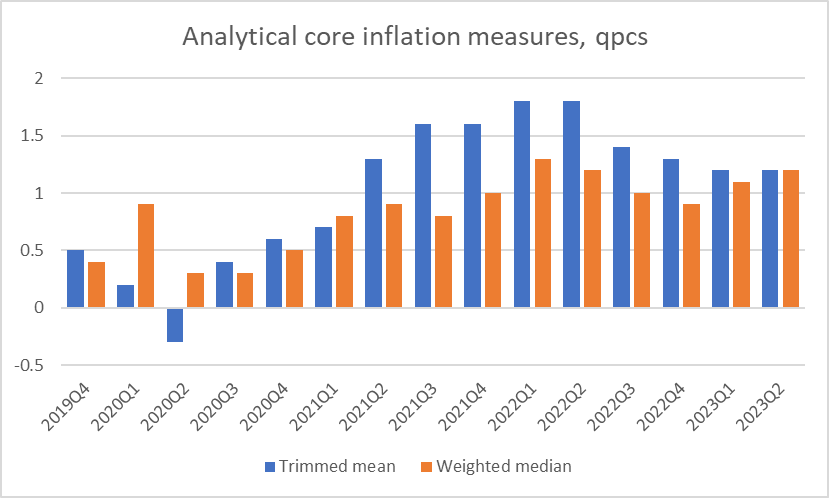

Six months ago I had been intrigued by this chart

It looked as though a reasonable case could then be made that core inflation had peaked a year earlier and was now falling (albeit still far too high).

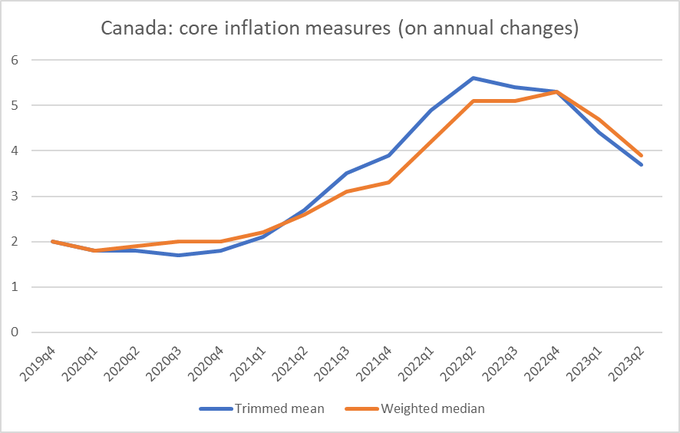

But jump forward to today and the chart now looks like this

If it still suggests a peak at the start of last year (at least on one of the measures), it is no longer a picture of (core) inflation falling now. (NB: You cannot put much weight on the absolute level of the numbers shown here because for some, unknown, reason SNZ persists in doing the calculations on not seasonally adjusted data, which can materially affect the level of quarterly estimates.)

If you look at a range of exclusion measures (CPI ex this, that or the other), the quarterly picture for Q2 looks a little more promising (but analytical measures such as those above are increasingly used for a reason).

On an annual basis, a whole bunch of measures centre on core inflation of perhaps just over 6 per cent.

Focusing on just two big individual price movements, the CPI ex petrol is up 7.1 per cent for the year, and the CPI ex international airfares is up 5.7 per cent.

The contrast between New Zealand

and Canada (where the central bank has the same target as ours) is striking

Rightly or wrongly, the Canadian central bank last week still judged it appropriate and necessary to raise its policy interest rate.

Over the period since the OCR was introduced, the New Zealand policy rate has typically been a lot higher than Canada’s (for the same inflation target since 2002): the median difference has been 1.5 percentage points. At present, the difference is unusually small even though our inflation numbers look quite a bit worse than Canada’s

If you think Canada is an obscure comparator, the story is, if anything, a bit more stark relative to the US where core inflation measures have also been falling.

And yet having chosen – and it is pure discretionary choice by the MPC – to review the OCR last week, just a few days BEFORE the infrequent New Zealand inflation data was released, the MPC then declared itself “confident” things were on track to get inflation back to target with policy rates at current levels.

Given how wrong they (and most other central banks) have been over the last three years, it is difficult to know how any bunch of monetary policymakers, with any self-knowledge and introspection at all, can declare themselves “confident” of anything about inflation outlooks. But what could possibly have led our lot to such a conclusion a week BEFORE the (quarterly only) inflation data? Once again, it isn’t looking great for them……and I guess it will be fingers crossed at the RB that the quarterly labour market data out early next month are much weaker. But the best official monthly data we have don’t seem that promising.

(As a reminder, it is not too late to apply to become a member of the Monetary Policy Committee although it is unclear that genuinely able people would be that keen to join a body led by underqualified uninterested people and where any genuine insight or challenge is unlikely, on the evidence to date, to be welcomed.)

I’ve always been reluctant to suggest that the MPC, or even Orr, were partisan. Mostly, they just seem not very good, something shown up more starkly in challenging times, and prone to questionable self-serving spin (even in front of Parliament). But since the May MPS I have started to wonder, and the nagging doubt was reinforced last week.

The Minister of Finance brought down the government’s annual Budget on Thursday 18 May. The Reserve Bank’s Monetary Policy Statement was a few days later, on Wednesday 24 May. I was travelling so most of my scattered comments were on Twitter.

On a current affairs show on 20 May, the Minister of Finance claimed that the Budget would not add to pressures on inflation or monetary policy.

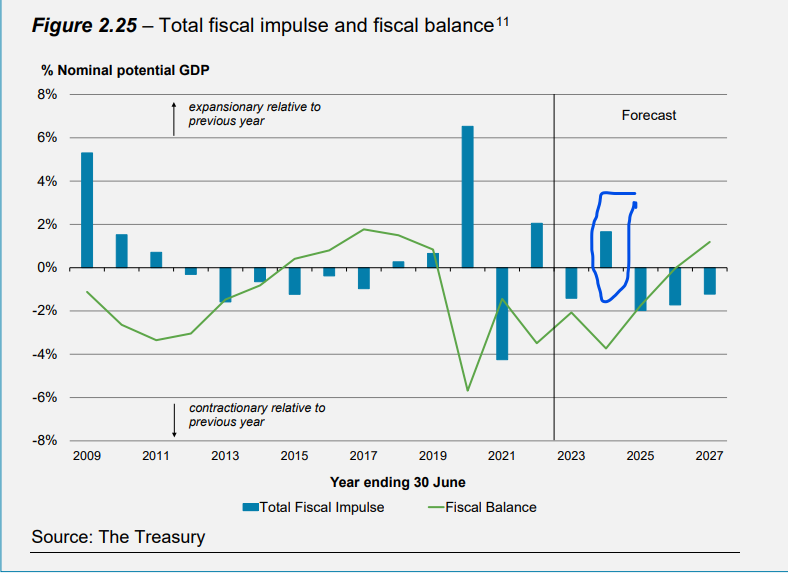

This was utterly at odds with the material published by The Treasury. Treasury estimates and publishes a series for the “fiscal impulse”. This measure was designed specifically for the Reserve Bank to give a sense of how, particularly over the forecast period, fiscal policy choices were going to be affecting demand and inflation pressures.

All else equal a falling deficit or rising surplus act as a bit of a drag on inflation, and vice versa for rising deficits or falling surpluses.

This chart was from the Treasury HYEFU published last December and incorporating the government’s then fiscal plans, as formally advised to the Treasury. As you can see, for each of the forecast years, the estimated impulse was negative (the overall accounts were still expected to be in deficit for most of the period, but the projected deficit was shrinking). At the time, most monetary policy interest would have been on the (highlighted) 23/24 year – showing a moderate negative impulse – since it was the period that monetary policy choices would most affect (and anything beyond 23/24 was little more than vapourware anyway, with an election in the middle).

This is how the same chart looked in the May Budget documents (Treasury’s BEFU)

For the key year – the one for which this Budget directly related – the estimated fiscal impulse had shifted from something moderately negative to something reasonably materially positive. The difference is exactly 2.5 percentage points of GDP. That is a big shift in an important influence on the inflation outlook – which in turn should influence the monetary policy outlook – concentrated right in the policy window.

My point is not to debate the merits of the Budget (political parties will differ on that) but to highlight the macro implications of aggregate fiscal choices as estimated by The Treasury, and how utterly at odds with the Treasury’s analysis the Minister’s spin was.

Ministers – and perhaps campaigning ones – will say whatever suits them, whatever relationship (or otherwise) what suits bears to hard analysis and advice.

But one of the key reasons why societies have chosen to delegate the operation of monetary policy to autonomous central bankers is that the central bankers are thought more likely to operate without fear or favour, calling the data and events as they calmly and professionally see it. So, you’d have thought, with a Monetary Policy Statement a few days after the Budget one might have expected some serious detached analysis of the updated Budget fiscal numbers, as they affected demand and inflation. Either citing the Treasury’s estimates or perhaps presenting analysis explaining why the Bank thought the fiscal influence might be different than the Treasury did (the latter using a framework designed specifically for monetary policy purposes). After all, in their previous MPS, MPC minutes had explicitly noted that “members viewed the risks to inflation pressure from fiscal policy as skewed to the upside”.

Central bankers, including particularly at our Reserve Bank, have long avoided taking a stance on government spending and revenue choices. Mostly, they also avoid taking a stance of deficits and surpluses. Those are political choices, and particularly in modestly-indebted countries (like New Zealand) it doesn’t greatly matter to monetary policy whether the budget is in deficit or surplus. It matters way less whether one has a high spending and high taxing government or a low spending or low taxing government, and so it is rare – and appropriately so – for the Reserve Bank to be commenting on either spending or revenue choices. What matters (about fiscal policy) in updating the inflation outlook is changes in the discretionary component of the fiscal deficit/surplus (basically, what the fiscal impulse is trying to capture). This snippet (from a Bollard-years MPS) captures the general approach.

But how did the MPC treat things in the May 2023 MPS, coming just a few days after that very big increase in the expected fiscal impulse for the immediately approaching year, at a time when inflation (core and headline) was way outside the target range and the OCR had had to be raised aggressively?

The only uses of the terms “fiscal” or “fiscal policy” (“fiscal impulse” doesn’t appear at all) are in this paragraph from the minutes. Even here – even that final sentence – it is consistent minimisation.

But these are the only references. In the one page policy statement, there is no link drawn from fiscal choices to the inflation outlook, and only this rather odd (for a central bank) detached observation: “Broader government spending is anticipated to decline in inflation-adjusted terms and in proportion to GDP.” So what, one was left wondering…..unless the Governor and his colleagues had taken to playing politics, perhaps to help out a Minister and his colleagues who seem more disposed to the Governor’s way of doing/saying things than, say, the Opposition parties (who openly opposed his reappointment) might be.

Perhaps it wouldn’t even be worth highlighting if this were the only such reference. But it isn’t, by any means. Recall, there are no references in the body of the document to fiscal policy, fiscal impulses, fiscal deficits, OBEGAL, or changes in any of these. But there is a whole section devoted specifically to government spending, on top of the couple of references I’ve already quoted. And the focus there is not on the horizon relevant to May’s monetary policy choices, or the inflation outlook over the next 12-18 months but over the “medium term”, when who knows which government will be in charge and what their spending preferences and priorities will be.

It is quite right that their projections – which simply use Treasury numbers as a base – have real government consumption and investment spending (the bits they publish numbers for) flat for the next several years.

That might raise some interesting issues, including for supporters of the current government who favour lots of government spending (is it really consistent with your values that per capita spending is going to fall quite sharply?, would it prove politically sustainable? and so on).

But it is of almost no relevance to monetary policy. And omits really major bits of the fiscal story (on the spending side, all of transfers and finance costs, and all of the revenue side). Central banks should be mostly interested in shocks to the deficit/surplus outlook. But not, this year, it appears the RBNZ.

The Bank and the MPC seemed to minimise any story about the fiscal contribution to the outlook for inflation and monetary policy (you know, things like inflation still being outside the target range, even with a high OCR, for protracted periods. Those fiscal impulse charts/numbers don’t get a mention. But neither do simple stats like the fact that in December’s HYEFU, on then government plans, Treasury thought the OBEGAL deficit for 2023/24 would be 0.1% of GDP. By May’s Budget, government plans meant a forecast deficit that year of 1.8% of GDP. These are really big changes, playing down to near-invisibility by our supposedly non-partisan independent MPC.

It was all brought back to the front of mind last week when, out of the blue, this observation appeared in the OCR statement

Broader government spending is anticipated to decline in inflation-adjusted terms and in proportion to GDP.

If you relied on Reserve Bank commentary, you’d just never know that, in the period current monetary policy choices are directly affecting, discretionary fiscal policy choices (overall balance and all that) had added, quite considerably, to inflation pressures in this year’s Budget. It doesn’t take much to guess which line the Minister of Finance will have preferred – and it isn’t the one that actually aligns with the Bank’s own responsibilities.

I am really reluctant to believe that partisan positioning is at work, even if (if it is happening) “just” for institutional self-protection reasons. But I find it difficult to see a compelling alternative explanation for the MPC’s approach to fiscal analysis and fiscal impulses in the last couple of months.

Perhaps the Opposition parties will view the Reserve Bank more charitably. But on what has been put before us, there is no reason for them to do so.

I would like to see the Treasury model what our economic growth figures would have been if government spending had remained flat throughout the past six years. My guess is that NZ would have had zero economic growth or worse. I suspect that the voracious spending appetite of Robbo (with admirable support from Tory Whanau et al) now represent our only hope for future economic growth. Go Robbo!

Nominal spending by local and central government in NZ typically seem to increase by circa 10% per annum. This means that the size of central and local government doubles every 7-8 years in nominal terms. Three cheers for Robbo! Collectivism is, after all, kindness.

Lastly, I finally found out what is driving increases in Non-Core government spending. ACC costs are to go up $5bn over the forecast period. I suppose we shouldn’t be concerned about this, because ACC is Non-Core government spending. In addition, given Robbo’s gorging is probably the only engine of economic growth in our country now, it would be churlish of me to quibble about what he is spending my money on…

LikeLike

Reblogged this on Utopia, you are standing in it!.

LikeLike

I disagree pretty much entirely with your analysis Michael.

Since May we’ve seen the economy grow slower than the RBNZ forecast. Capacity pressures have eased materially and look set to continue to ease. Inflation expectations indicators have fallen, as have a range of inflation measures. And monetary and credit conditions have materially tightened with retail loan (and deposit) rates higher and credit metrics very subdued. Additionally, we’ve seen a material fall in forestry and dairy prices and while housing has stabilised, that’s all its done, down 25% from its high in real terms. Credit aggregates are near zero across all sectors and down in real terms, M1 money growth has collapsed, and new credit intermediation is at decade lows with stress tests meaning banks simply cannot lend. And loan fixings are only about 1/2 way through with credit stress metrics in lower collateral lending beginning to pick up.

So yes, disinflation right now is dominated by goods, but it always is. Goods prices are less prone to inertia, are less subject to annual changes (eg local authority rates, education and health charges) and are more likely to be priced to market. Given the level of household debt, and short dated mortgage fixings, the RBNZ is in much firmer control today than it was in the Bollard years.

In time, these core metrics will come down and given what’s happening, there’s really no need to panic and over react.

LikeLike

Never is the right time to “panic and over react” (of course). But whether there has yet been sufficient policy reaction to be comfortably confident about a prompt return to 2% is an open question, bearing in mind that total monetary tightening has been materially less this time than in past warranted RB tightening cycles.

As I note of the RB/MPC, I don’t think anyone has a great basis for being too confident on their view of inflation or the requisite mon pol through this episode.

We’ll see.

LikeLike

Well, I am spending a good deal of time breathing over the monetary and credit aggregates. In the past, the RBNZ provided very little data on money and credit and it was darn hard to understand what was going on in the banking system, which gave the banks a huge advantage in understanding the economy. Not anymore. The data published since late 2016 gives us a fantastic insight into the structure of money and credit in the economy and how monetary policy is transmitting.

What we clearly observe is that the rise in interest rates is still only about 1/2 way through feeding into household, business and farm income statements. The cost of funds is rising rapidly as debt is re-priced and the share of household disposable income being absorbed by interest payments is rising rapidly, it will be around 10% of disposable income by mid-2024. That’s up from a low of 4.5% in March 2022 and around 6.5% currently. That’s a huge drain. Additionally, given bank stress tests, and the impact of the CCCFA, banks are stress-testing new lending at yields >9% which is causing them to truncate lending, we can see in the data that high DTI lending has stalled but if you look at credit broken down by borrower gross income, essentially the median income earners and below are being cut out of the credit market. Credit growth has stalled. Again this is a huge difference from the Bollard years when people had shorter duration mortgages, banks were more than willing to term out P&I structures, or move to IO, or to extend credit against rising house prices. Today, not so much…

The next shoe to drop is impairments. It is clear in the data on agriculture that farmers are drawing credit facilities, shifting from P&I to IO and delinquency rates are beginning to climb. Centrix is also seeing credit stress emerging in uncollateralised lending. To become a delinquent on your home loan in NZ takes some doing, and it wont occur in the initial stages of tightening. But as alternative sources of capital drain, we will see a lift in impairments, and it could become quite non-linear, especially if unemployment rises.

What matters here isn’t whether inflation is 6% or higher – as Cakeface comments – we know this. What matters is what the policy response is. Policy is unequivocally tight. The evidence is everywhere to be seen. We are seeing inflation expectations survey’s coming down hard and inflation will follow along.

Maybe Adrian made a policy mistake in 2020, but then at the time pretty much everyone went along with it. No point correcting a mistake by making another one.

LikeLike

“We’ll see.”

No, we’ve seen.

The annual rates of non-tradable inflation, in order and by quarter, since (and including) March 2022: 6.0%, 6.3%, 6.6%, 6.6%, 6.8% and now 6.6% for the June 2023 quarter. (interest.co.nz)

RBNZ policy has been an unequivocal, unmitigated, categorical and complete failure. Mr Orr is incompetent.

It must be time for some Lord Keynes:

“Lenin is said to have declared that the best way to destroy the capitalist system was to debauch the currency. By a continuing process of inflation, governments can confiscate, secretly and unobserved, an important part of the wealth of their citizens. By this method they not only confiscate, but they confiscate arbitrarily; and, while the process impoverishes many, it actually enriches some. The sight of this arbitrary rearrangement of riches strikes not only at security, but at confidence in the equity of the existing distribution of wealth. Those to whom the system brings windfalls, beyond their deserts and even beyond their expectations or desires, become ‘profiteers,’ who are the object of the hatred of the bourgeoisie, whom the inflationism has impoverished, not less than of the proletariat. As the inflation proceeds and the real value of the currency fluctuates wildly from month to month, all permanent relations between debtors and creditors, which form the ultimate foundation of capitalism, become so utterly disordered as to be almost meaningless; and the process of wealth-getting degenerates into a gamble and a lottery.

Lenin was certainly right. There is no subtler, no surer means of overturning the existing basis of society than to debauch the currency. The process engages all the hidden forces of economic law on the side of destruction, and does it in a manner which not one man in a million is able to diagnose.”

LikeLike

No doubt that he should have been ousted. But it is always possible that something close to enough has now been done (and enough forecasts have been completely wrong in recent years that we should be modest about the strength of our own indiv views)

LikeLike

I broadly agree with Peter about the direction of our economy, except that I think the economic fundamentals of the New Zealand economy are far, far worse than he outlines.

Judging by our 8.5% current account deficit, I would estimate that our trade weighted exchange rate is 10 – 20% overvalued. In essence, our living standards are currently 10 – 20% higher than they should be, relative to our trading partners. Most likely, our currency will crash when we are downgraded by the ratings agencies. Of course, ratings downgrades typically eventuate years after they should, judging from the events of 2008. We cannot wait for these agencies, before we act, and rebalance our economy.

What has caused us to have the worst current account deficit in the world is the crowding out of the private sector economy, due to the almost doubling in the size of central and local government in nominal terms over the past six years. The dead weight economic losses from this massive increase in public sector spending have destroyed New Zealand’s productivity and potential economic growth rates. I sense that we are either on the verge of an enormous economic collapse, or the economy will grind down next 5 to 10 year period, eventually reaching an even lower point than an economic crash would deliver. In my opinion, I sense that we have a terrible choice of an economic crash now, or die by 1,000 cuts over the next decade…

The advantage of having an economic crash soon is that we would be forced to rebalance our economy now, before more damage is done. The advantage of a slow grind down is that events may magically change, somehow allowing the economy to turn around, without the painful crash, but likely with a lower endpoint.

Confident predictions of the future are the most disreputable of public utterances, but personally, I don’t see many good options. Too many mistakes have been already made. For example, Zero Covid nutjobs closed the borders for the best part of three years, and vandalized New Zealand’s long-term productivity.

I’m don’t know whether the RBNZ should raise the OCR any more, or not. The economy is collapsing in front of our eyes. Irrespectively, my view is that fiscal policy is our main problem. Central and local government expenditure needs to be cut. I hope National and ACT, if they win the election, will do this.

LikeLike

Indeed, quite a change in public sector demand so fingers crossed private sector demand simmers down a touch.

Think it roughly right 33% off households have mortgages: touugh times ahead but hopefully they/”we” muddle through.

My pick: you don’t go from near zero risk free rates to near 6% risk free rates without creating risks….!

LikeLike

Nice final observation. Of course, we’ve been that way before, with really big increases in short-term rates. Perhaps the difference this time might be that credit growth has never been exuberant in recent years, with the attendant deterioration in lending stds that we saw in the mid 80s and again in the mid 00s (notably finance companies, but also some bank lending, notably dairy)

LikeLike

Think the H2’20 through H1’22 credit cohort might start to show a few cracks soon: the banks might have stressed at higher than initial fixed rates, but not at the latter combined with the ex post spike in general living costs. Fingers crossed any credit stress is contained at the fringes.

I’m always surprised there is relatively little main stream commentary on the level/change in credit spreads – given how the flow of credit underpins the flow of real activity.

The stock market is interesting but it is also a relatively basic game: you win or you lose it. Clean cut. Easy.

But when credit markets crack, you don’t know who will take the loss, when and where. Not easy.

LikeLike

Thank you Mr Reddell for opening what is a Pandora’s box of possibilities.

Fiscal drivers of inflation include local government , their spending and rate demands. They have even created their own CPI to justify the substantial increases ,

Services , some of which with little positive economic value have also grown along with with the growth in regulation ensuring use of these services. A wage price spiral has started.

The tradable economy is waning . Forestry lamb wool ,the staples of the past are rapidly becoming just that the past!

Manufacturing has largely disappeared offshore and much of that remaining is subsidised .

( Weta workshops etc)

New Zealand’s problem is our lack of real productivity. The oft quoted concept that agriculture will save NZ is wrong.

There are just not enough farms and farmers left.

Most have been regulated and taxed out of business.Many of those who remain are reliant on Carbon credits which have little financial stability credibility, or real value to NZ!

And manufacturing has already largely disappeared offshore.

Almost all that sustains the NZD is ,as seen in the past ,is NZ mostly having had highest interest rates in the OECD. We get what we pay for.

The NZ balance of payments (which seldom has been worse)used to be of interest to financially literate decision makers but now it is barely mentioned.

To reboot NZ now is work of a Herculean proportions.

I am concerned for the future of my family!

LikeLike

As a guy with a mortgage im always keen to listen to the announcements to analyse alongside and OCR changes.

The main reason for this is because I believe that central banks use OCR changes as strong ways to manipulate spending and words in the announcements as soft ways to manipulate spending.

I see OCR increases as carrying economic risk, but the announcements (while less effective) are free of risk.

Therefore i found it very odd that the last time they increased the OCR, it was accompanied by an announcement pushing in the opposite direction.

Ive been racking my brain, trying to understand why they announced that it was going to be the last increase required, because this statement effectively undoes part of the OCR increase as people will be less fearful of subsequent increases and spend accordingly.

The only good reason i can come up with is that it’s political; either in support of the ruling party who presided over the economy as it got in this mess or to try to appease the current powers to try to keep his job.

If that’s the case, this action will be very damaging to a lot of people in order for one person or party to try to keep their position.

LikeLike