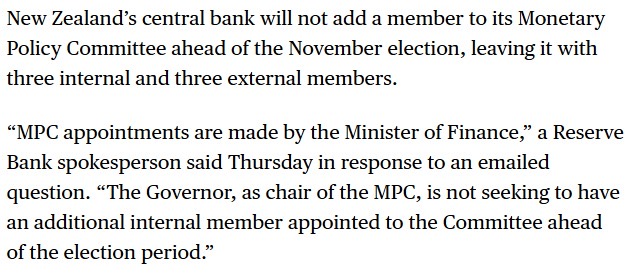

A month or so ago the Reserve Bank announced the appointment of a new Assistant Governor (a deputy chief executive) responsible for its financial stability functions. That must have prompted a Bloomberg journalist to ask what was happening to the vacant position on the Monetary Policy Committee (given that, previously, Geoff Bascand and then Christian Hawkesby as holders of that role had also been on the MPC). Later that day a story appeared which had this snippet (which someone had sent me)

I gave it a bit of attention at the time on Twitter but had seen no follow through.

So I was pleased to see an article in the Herald this morning reporting an interview that Jenee Tibshraeny had done with the Governor where she asked Breman just what was going on. And got some not-very-satisfactory answers, that don’t put the Governor or the Board (or perhaps the Minister too) in a very good light, and (incidentally) suggests that the Bank was not being entirely straight (to say the least) with Bloomberg when they asked last month.

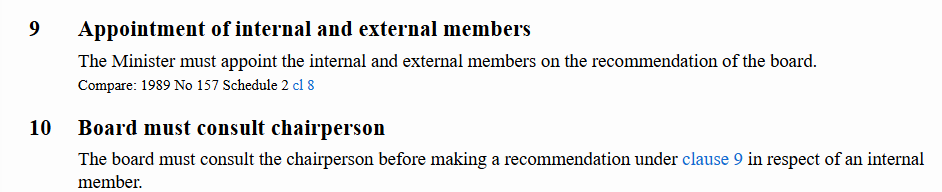

The Reserve Bank Act is pretty clear about MPC appointments. The Minister of Finance appoints MPC members, but does so (only) on the recommendation of the Bank’s Board. The Governor is a member of the board, but formally also has to be consulted in her role as chair of MPC before recommendations are made in respect of internal members (people who directly work for the Governor).

There is no minimum term of appointment (which could be a weakness in some circumstances, but the law is fairly new and is what it is).

In the short history of the MPC, a temporary appointment has already been made once, back in early 2022 (after the chief economist had left and before another permanent appointment was made to that role)

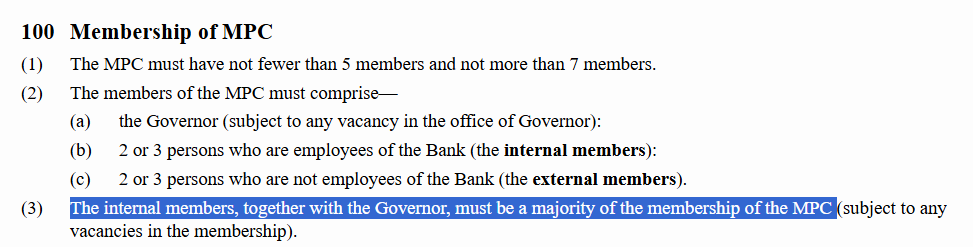

And, as importantly as all this, the Act is specifically clear that there must be a majority of internal members on the MPC

NB: In the event of a tie the Governor does have a casting vote, but this provision is explicitly about members not about votes.

Again, one can debate the merits of requiring an internal majority, but it was a choice Parliament made only quite recently (within the last decade). And if someone dies, or resigns with no notice, vacancies can’t be filled overnight (presumably the point of the bit in brackets at the end of 100(3)), but……there has now been a vacancy on the MPC since Adrian Orr resigned (his resignation having taken effect from 31 March 2025). That is now 16 months ago.

The Governor seems to have been totally at sea when Tibshraeny asked her what was going on. She is quoted as saying that “I don’t know if it’s possible to have a temporary position. That’s apparently what’s happened before [see above] so I’m just looking into that”.

But she has been in the role of eight months now, she chairs the MPC (so you might suppose she’d have made herself familiar with the statutory provisions, especially when leading changes to make voting more of a thing on the committee), and had apparently been comfortable with her spokesperson a month ago telling Bloomberg she had no intention of seeking to fill the position before the election.

Now, even the comment she had had provided to Bloomberg was at best misleading (since the responsibility for recommending MPC members rests with the Board – chaired by Rodger Finlay – not with the Governor, let alone the Minister), but it also seems quite at odds with what she was saying to Tibshraeny when interviewed the other day.

And what on earth did the election have to do with it? There is a well-understood convention (repeated in this Cabinet Office circular for this election) about not making significant permanent appointments to commence in the period starting from three months prior to the election. (Thus, in the Reserve Bank case, back in 2017 there was an – almost certainly illegal – appointment of an acting Governor because a new permanent Governor could not be appointed to start in the weeks either side of the election.)

But the pre-election window begins this week, and the MPC vacancy has existed since March last year. Christian Hawkesby left his job (as Acting Governor and substantive head of financial stability) eight months ago, and even that permanent appointment of a Head of Financial Stability was announced more than a month before the pre-election window. And, as the Governor (and Board) presumably now appear to know/remember, temporary appointments (say, 6-12 months) are perfectly possible in this case (and, in any case, since it is the appointment of an internal – not appointed by the Minister to the day job in the first place – it was difficult to see how an MPC appointment was likely to be particularly politically contentious).

The Governor appeared to be caught on the hop in her interview last week (pretty bad when the Bank had already made those comments to Bloomberg) because the Herald article suggests that after the interview a “Reserve Bank spokesperson” was sent out to tidy up after the Governor.

Of which a number of things can be said:

- The Board has no authority to simply leave a vacancy indefinitely (the law explictly requires an internal majority),

- The appointment of a permanent Governor was made in September last year (and at the same time it was announced that Hawkesby was leaving the Bank),

- There was nothing, at any stage, to stop a temporary appointment (whether of the chap who was filling in for Hawkesby as head of financial stability or – since he was a lawyer – some other senior economics/markets person),

- The person who was acting as head of financial stability was appointed to the permanent role a month ago now. Either he could have been appointed to the MPC straightaway (eg the Minister confirm it was her intention to so appoint) or, very belatedly, a temporary appointment could have been made. In fact, the Bank told Bloomberg they weren’t looking to make an appointment now, but now say “there is a process underway”.

The Minister of Finance is reported (briefly) in the article, noting that “it has been the practice for successive governments to exercise restraint in making significant appointments in the pre-election period, which begins on 7 August”. Which is factually correct, but largely irrelevant in this context given a) the vacancy has been there for 16 months, and b) there is both authority and precedent for a temporary appointment. You have to wonder, though, what Treasury, paid as official monitors of the Reserve Bank, had been doing all this time about simple matters like ensuring that the Bank and the Board complied with the law, putting up nominations enabling the Minister to make an appointment.

Does it matter greatly? Perhaps at one level, not so much. But the law isn’t just there as a suggestion but as a set of obligations and responsibilities, and the Board seems to have deliberately flouted one of its responsibilities in this case. Laws imposing duties and responsibilities on government agencies need to be observed punctiliously. As it is, one recent OCR decision was made only by the Governor’s casting vote, a vote she would not have needed to (or been able to) deploy had the Board and the Minister done their job and ensured an internal majority of members. There have been all-too-many “pretty legal” things from the Bank and its Board in the last few years (whether misleading Parliament, misleading the public, OIA obstructionism, knowingly blowing the previous Funding Agreement spending limits, purporting to consult on proposed physical cash requirements which it had no legal authority to insist on, and so on). And misleading journalists – as appears to have happened on this issue with Bloomberg – isn’t exactly a way to build and restore confidence in a troubled institution.

On the substance – the vacant MPC seat – we are left wondering what is going on. Presumably Angus McGregor is not going to be appointed (could easily have been done or signalled already if he was). His predecessors had been on MPC but then they’d all had an economics background and he’s a lawyer. There don’t seem to be that many obvious current internal possibilities – one might be Adam Richardson, now director of financial markets (who’d been the acting MPC appointee back in 2022). Or perhaps there are other plans. It is still hard to believe that the Governor has done nothing about Karen Silk – surely the most underqualified central bank DCE responsible for macroeconomics and monetary policy anywhere in the advanced world – and perhaps there are plans afoot. Perhaps she is contemplating hiring someone as (eg) Adviser to the Governor with the strong New Zealand macro perspective that neither she nor Silk has? We don’t know but the current situation is unsatisfactory – the board, apparently with her acquiescence, is wilfully choosing to ignore the legal requirements, and a journalist (and thus the public) seems to have been knowingly misled as recently as a month ago. And, as recently as a few days ago, the Governor herself was unable or unwilling to give a straight answer to what should have been a pretty straightforward questions (about an unsatisfactory situation).

And, if I have been inclined to absolve the Minister of primary responsibility, she has formal responsibility for the Bank, she has the full resources of The Treasury at her disposal, and the Board chair was personally appointed by her (and just last week she appointed a deputy chair

Yeah right.