I’ve never really been persuaded that it is a good idea for public servants to be giving speeches, unless perhaps they are simply and explicitly explaining or articulating government policy. If they are, instead, purporting to run their own views or those of their agency it is almost inevitable that we will be getting less than the unvarnished picture and more than a few convenient omissions. Public servants still have to work with current ministers after all.

The thought came to mind again when I read a speech given last week by Struan Little, now a “chief strategist” at the Treasury but until recently a senior Deputy Secretary (and actually Acting Secretary for a time last year). The speech was to some accountants’ tax conference, under the heading “The role of the tax system in addressing New Zealand’s intertwined fiscal and economic challenges”. All else equal, you might suppose that lower taxes would be more likely to be part of dealing with the productivity failings and perhaps higher taxes might have some role to play in closing the gaping fiscal gaps. It isn’t clear that Treasury necessarily sees it that way. They seem quite keen on raising taxes generally, especially on returns to capital.

(To be clear, I’ve been on record for some time picking that whoever is in government over the next few years the GST rate will rise, but that is prediction not prescription – and I’m not a senior official. Somewhat oddly, in his speech Little claims that “there are no simple options to raise substantial merit over the shorter term” when, whatever the merits of such a policy, raising GST is certainly simple.)

Now, I guess it was a tax conference, but it was slightly odd that not even once was it mentioned how much spending has increased in the last few years. Core Crown operating expenses were 28 per cent of GDP in the last full pre-Covid year (to June 2019) and in this budget were projected to be 32.9 per cent of GDP this year (25/26), slightly UP on last year. The current structural deficit, from the same budget documents, was projected to be about 2 per cent of GDP. I guess officials always need to have tools to hand if politicians want to go the higher tax route but it isn’t obvious that the scope of expenditure savings has been exhausted (or even much begun perhaps outside core departmental operating costs, which generally isn’t where the big money is).

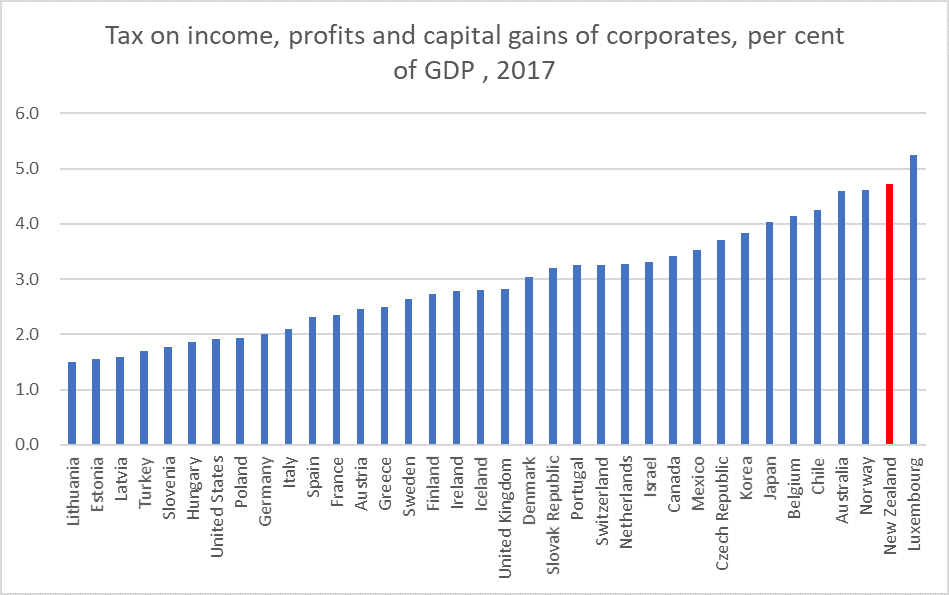

Remarkably also, there is no mention at all in the speech that New Zealand’s company tax rate is among the highest in OECD countries. In the literature, the real economic costs of company taxes are generally found to far exceed those of other main types of tax. There is no mention either that New Zealand has long taken one of the highest shares of GDP in corporate tax revenue.

That chart is a few years old now but the OECD data are very dated and the most recent I could find on a quick search was for 2020 (when, unsurprisingly, we would still have been well to the right on this chart).

Instead what we got is a straw man discussion, claiming that life (and literature) have moved on and that now everyone agrees the tax rate on returns to capital should be positive. In practice no one has seriously argued in the New Zealand debate that capital income should generally be taxed at zero, notwithstanding some literature suggesting that on certain assumptions a zero rate might be optimal. Where there is debate is a) how high that rate should be, and b) what should count as taxable (capital) income.

Now, to be fair, on a couple of occasions Little suggests that we need to cut taxation on returns to inward foreign investment (because of our imputation system the company tax rate falls most directly on foreign investors), but then never addresses the issue as to whether or why our income tax regime should treat foreign investors more favourably than domestic investors and what the implications of that might be.

Treasury has, of course, long been keen on the idea of a capital gains tax. Little repeats an estimate from the Tax Working Group some years ago suggesting that such a tax might raise 1.2 per cent of GDP per annum but then never bothers engaging with the fact that the largest source of (real) capital gains in recent decades has been in housing, and that the reform programme of the current government is supposed, at least according to the Minister responsible (if not to his boss) to be lowering house prices, and (presumably) making sustained and systematic real capital gains on housing/land a thing of the past.

Little champions the somewhat-strange Investment Boost subsidy introduced in this year’s Budget, and yet (of course) never notes that the biggest returns (by a considerable margin) to that subsidy are for investment in new commercial buildings. The very same sector that the government (perhaps over Treasury objections) increased taxes on last year, when it barred tax depreciation on commercial buildings. Where is the coherence in that? Or in the fact that Investment Boost offers a subsidy to rest home operators but not to providers of rental accommodation? But I guess Treasury wouldn’t really want to comment in public on any of that. The Minister would certainly not have been keen on them doing so. He never offers any thoughts either on why subsidising a specific input – as if capital goods are some sort of merit good – is preferable to lowering the tax rate on returns to whatever combination of inputs firms find most profit-maximising.

We also get the same (now decades-old) line about housing being tax-favoured while never noting either a) that the story of New Zealand in recent decades has been too little housing (& urban land) not too much, or b) that the largest tax advantage by far in respect of housing is to the owner-occupiers with no debt. Perhaps Treasury favours taxing imputed rents (with suitable deductions including for mortgage interest) but if so there is no hint of it in the speech (something for which the Minister would no doubt be grateful).

And there are tantalising but concerning lines suggesting Treasury might favour rather arbitrary distinctions between returns to different types of capital. Thus, there is mention late in the speech of possibly in future reducing tax on “productive capital investment” (which then does Treasury regard as “unproductive” ex ante), there is a reference at one point to taxation on “physical capital”, without being clear as to why physical capital returns should be treated differently than returns on intangible capital. And perhaps potentially most concerningly there was this line: “a coherent approach would not necessarily mean taxing all capital [returns to capital?] at the same rate, since not all capital is the same”. What, one wonders, does Treasury have in mind there? After all, not all human capital is the same either (you are different than me) but our tax system treats all financial returns to it much the same anyway (or so it seems to me; perhaps I’m missing something).

There are some fair points in the speech. Little notes that our system “penalises certain types of saving when inflation is high”, which is true but understates the point: even 2 per cent inflation results in such distortions, and they apply to borrowing (when interest is deductible, which it generally is for business) and depreciation, not just to returns on fixed interest assets. These distortions have been known for many decades, and yet there seems to be no momentum – political or bureaucratic – to address them, whether by changes to the tax system or to the inflation target.

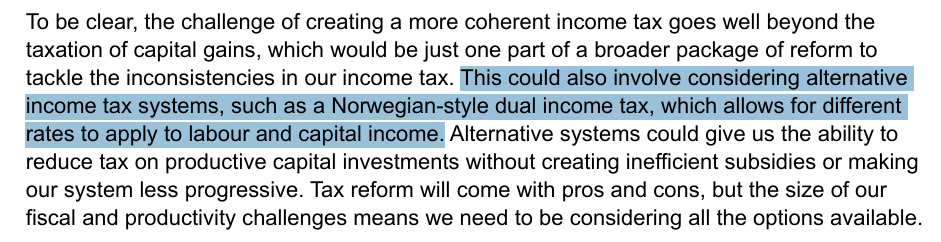

And there was a paragraph late in the speech that I very much welcomed.

I’ve long been keen on a Nordic approach and it was an option noted by the 2025 Taskforce back in 2009. But what chance is there that the bureaucrats might support such a change? When I was involved in tax debates IRD was quite resistant to any cuts to business tax rates arguing (with little or no evidence) that many taxable profits were rents – returns above the cost of capital – and that taxing them came at little or no cost. And if by some chance a new generation of officials has emerged, what chance ministers (whichever main party is in government) being that bold. Another growth-supportive option that might have warranted mention in that paragraph would have been work on the possibility of a progressive consumption tax.

As I noted at the start of the post, I’m not sure senior officials really should be making speeches other than to represent the policy of the government of the day. They simply can’t add much, or any sort of unconstrained perspective. The free and frank advice has to be for ministers. That said, perhaps at some point it would be useful for Treasury to publish some research/analysis outlining what sort of tax structure would, in its view, be most conducive to supporting a much faster rate of productivity growth in New Zealand. It is unlikely that tax system changes could ever represent any sort of panacea but insights into the mental models of the government’s premier economic advisers could still be useful. Since it isn’t impossible that the answer might be much lower taxes (and thus spending) than at present, you could even put some constraints around the exercise: if you (or your political master) needed to raise 27 per cent of GDP in tax, which mix of taxes and tax rates would be most consistent with helping enable a materially faster rate of productivity growth.

A couple of months ago the Minister of Finance announced that Anna Breman had been appointed as the next Governor of the Reserve Bank. Breman takes office on 1 December, conveniently (and sensibly) just after next week’s final Monetary Policy Statement for the year. Given the very long summer holiday the MPC gives itself, it does give her plenty of time to get her feet under the desk, get to know staff, get a bit familiar with the New Zealand data and issues before she gets to chair her first MPC and deliver the first Monetary Policy Statement on her watch. (Quite where the bank capital review is getting to isn’t clear: there was talk of publishing decisions before the end of the year, which could mean either before 1 December (in which case she has no formal say) or afterwards in which case she and rest of the Board will be making important decisions within weeks of taking up the role, in a field in which she doesn’t seem to have any particular background.)

Just a few days after the position became vacant in March I noted

Having noted that there seemed to be no ideal or compelling candidate in any of the lists of domestic names that had started to emerge, that remained pretty much my view in the abstract through the many months it took for an appointment to be made.

When Breman’s appointment was announced I was overseas on holiday. A few media outlets asked me for initial comments, including Radio New Zealand’s Morning Report who I tried to put off but eventually agreed (“live from Ravenna” – former capital of the western Roman empire – had a certain wry appeal to me). The comment I’d made to them that it was 43 years since an internal person had been appointed Governor appeared to have piqued their interest. The interview and associated report is here.

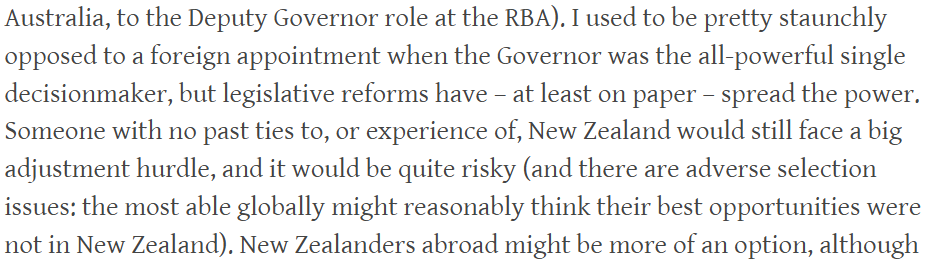

I noted that while on this occasion it was clearly necessary to go for an outsider, it was a poor reflection on the Bank, its board and senior management, over decades that it had been so long since the last internal appointment (Dick Wilks in 1982 who was then pushed into an early retirement by Muldoon), and that one dimension of successful organisations (anywhere) tended to be the development of talent and succession planning such that most (not all by any means) top appointments came from within. Among central banks, the Reserve Bank of Australia is a striking contrast. I also noted that, for example, two successive foreign appointees as Secretary to the Treasury (very unusual appointments in themselves) had not exactly proved to be stellar success stories.

There were reasons for each outside appointment as Governor – and I’m not debating the merits of any of them individually here – but the accumulated track record should be concerning. (And one of the challenges for Breman and the Bank’s board over the next few years will be building a strong second tier such that in five years time there is at least one, ideally more, credible internal candidates if Breman decided, whether for professional or family reasons, it was time to return to Europe.)

But if that backdrop is a concerning structural issue, my more immediate issue picked up the same concern I’d raised in abstract back in March: going offshore for a Governor who has no background or familiarity with New Zealand was a risky call. And if I’d contemplated a possible foreign Governor back in March I guess I’d probably have mainly thought in terms of someone from culturally and politically similar countries (Australia, Canada, UK), and Sweden is at an additional remove.

In terms of the technical side of monetary policy that isn’t an issue – Sweden has been a longstanding inflation targeter (I still have and use the nice glass plate a visiting Swedish parliamentary delegation gave me when they came to learn about the way we, who pioneered formal inflation targeting, did things decades ago) and the independent review of monetary policy done almost 25 years ago was conducted by Lars Svensson, a leading Swedish academic and later a member of Riksbank’s Executive Board (who made himself unpopular by openly expressing minority monetary policy views, which were – in my assessment – largely right). But monetary policy doesn’t operate in a vacuum – there is the context of the specific economy, of the specific political system, and of the place and record of the central bank itself. Perhaps as importantly, these days monetary policy is only one limb of what the Bank does. Much of its staff resources are now devoted to financial regulation and supervision, and that doesn’t appear to be a field in which Breman has any particular experience (for example, the Riksbank is not responsible for those functions).

So from day one it seems quite a risky appointment. I might be less worried if (a) the Reserve Bank were a high performing stable institution, b) there was a strong and respected second tier in place (who for some reason didn’t want to be Governor or who weren’t quite ready, and/or c) the appointee was a star.

As has become increasingly clear as this year has gone on, neither a) nor b) held, and (for all his faults and limitations) the departure of Christian Hawkesby only highlights how weak the top tier Breman is inheriting will be. There are two key second tier policy roles – Hawkesby’s day job (financial stability) is filled by a low profile acting person, and the macro/monetary policy side which is overseen by Karen Silk, who has such a limited background it is almost inconceivable she could have held such a role in any other modern advanced country central bank.

But nor is there any sign at all that the incoming Governor is a star. She sounds as though she probably has the temperament for the job (a person who knows her spoke quite highly of her on that score) but beyond that it isn’t clear that she is much more than a boilerplate MPC-member economist, without (it appears) that much executive management/leadership experience (let alone change management and institutional transformation). And, of course, there is no background in financial stability or regulation. She seems to have had a perfectly respectable career in the Swedish Ministry of Finance, a few years running the economics group of a Swedish bank, and then six years on the Executive Board, all against an academic background that, again while perfectly respectable, wasn’t focused on macroeconomics, financial markets, financial stability and regulation etc. She didn’t seem to have had particularly high visibility in international central banking or monetary policy circles.

One of the great things about the Riksbank is how transparent they are about monetary policy – materially more so than the Reserve Bank of New Zealand MPC, and arguably a touch beyond the optimum. Not only do Executive Board members seem to give a fair number of on-the-record speeches but all their contributions to the formal monetary policy deliberations are published verbatim. So when I got back from holiday I took some time to read pretty much all I could find from Breman. Since I didn’t previously know much more about her than her name I was genuinely curious. Some top-notch people, with distinctive perspectives, have served on the Executive Board over the years (with people brought in for full-time roles, such that it is more feasible to have mid-career people appointed than to our part-time non-executive MPC roles).

I was particularly interested in how she had contributed to monetary policy deliberations through the Covid and post-Covid inflation periods. It was a real test for central bankers, and frankly most did not show up well (which is why most – but not all – advanced economies ended up with the worst outbreak of core inflation in decades). As regular readers will know I have also long championed accountability for central bankers – real accountability with consequences, the quid pro quo for the considerable delegated power MPCs (and similar entities like the Riksbank Executive Board) wield. Other people got things wrong too, but central bankers took the job (and attendant pay and prestige) to stop outbreaks of inflation happening. If things go really badly – and they did – there should be, at very least, a strong presumption against reappointment. In fact, things went worse in Sweden than they did here – with core inflation peaking in excess of 9 per cent

And what were Breman’s contributions during this period? They were solid workman-like pieces (& her speeches were probably better than the – very few – Reserve Bank ones) but there were no interesting insights or angles, and no material (let alone votes) suggesting that her instincts or mental models were better than average – in a central bank that delivered a core inflation record worse than the average advanced country central bank. (And it doesn’t even look as though they got out the other side any better than we did – the Riksbank’s latest negative output gap estimate is very similar to the Reserve Bank’s for New Zealand.)

And so, at least on the monetary policy side, it looks like a case of a boilerplate central banker failing upwards – not at home, but promoted to the top job in an underperforming remote area of the world. Is it like being banished to the colonies in days gone by? Perhaps she’ll do just fine as MPC member and chair, but nothing in that record back home suggests we are getting, for example, a policy leader or distinctive thought leader. And is there really no price for failing so long as you are in good company?

Aside from being an outsider, it really isn’t clear what strengths she brings to the position. Perhaps under the previous government her evident enthusiasm for central banks wading into climate change issues might have been a selling point (she was last year a member of the steering committee of that central bank talk shop the Network for the Greening of the Financial System). The Riksbank apparently even puts restrictions on holding Australian state government bonds in its reserves portfolio on climate change grounds. But one had hoped that under this government they’d have been looking for a strong focus on the core statutory functions of the Bank.

One point of hope might be her expressed commitment to transparency. At the press conference she held with Nicola Willis – which featured some odd lines, including Willis claiming “we are opening a new chapter in New Zealand’s history” – there was the superficially encouraging line about how she (Breman) intended that “transparency, accountability, and clear communication will guide all the work we do”. On the monetary policy side we might look for some serious moves towards greater transparency. It isn’t her call alone, but she will over time control the appointments of the executive members of the MPC – and an earlier test will be what she does there – and it is clear that at least one non-executive member, Prasanna Gai, favours greater transparency. The Swedish experience, which she spoke positively about in a speech earlier this year, should be one of those considered seriously.

Her instincts then may be broadly sound, but a) there is no sign that she is a star, b) the culture of defensive non-transparency (transparent when it suits, obstructive when it doesn’t – I’m still engaged with the Ombudsman over charges the RB made for releasing information several years ago that should have been released – was in scope – in 2019) appears to have become quite deeply entrenched in the organisation over the last couple of decades. And much about the Reserve Bank is controlled not by the Governor but by the board – which never used to matter much but has been in the driving seat since the new legislation came into effect in 2022.

Which brings me back to the title of this post. One might have more basis for initial confidence in a little-known outsider if that person was selected/nominated and appointed by people who themselves commanded respect and had developed a track record of building (or requiring) a high-performing, lean, open, transparent, and accountable institution. But this appointment was made by Willis who had displayed spectacularly bad judgement in reappointing Neil Quigley as board chair last year, who did nothing about the board’s very bad budget calls last year (she and her officials seem not to have been aware for months), and who stood by for months while the board obstructed any clear sense of the circumstances surrounding the resignation of the previous governor. How much confidence can anyone have in a person nominated by the Quigley-led board, selected when the board was at is embattled and defensive worst, and when that board has shown no sign of having regretted anything about the way they’ve done things? The same board that really really cannot stand critical scrutiny – who instead of engaging or replying were responsible for management’s insistence to an overseas magazine that published an article critical of the Board’s record that the magazine should withdraw it and apologise for having published it. Whose acting chair – of a public agency, allegedly committed to transparency and accountability – celebrated (in writing) when the article was taken down. We are supposed to believe that these people share the incoming Governor’s stated commitments on those scores? Or to have confidence in the Minister who has sacked none of the board members, and has still not replaced Quigley as chair? They are albatrosses around Breman’s neck, no matter how good she might actually and eventually prove to be.

Way back in those RNZ remarks in September I noted “She could prove to be an excellent call. Time will tell.” We must all hope she is. The rebuilding of the Reserve Bank matters and we deserve better than we have had. Senior Reserve Bank officials have gone on record as (belatedly) recognising that confidence and trust in the Bank has taken a hit – a pretty severe one in my view. But rebuilding is going to be a tall order, the more so with such a discredited board – and would be so even for someone with excellent credentials and connections. How much more so for Breman.

For the first six years of the newly-created statutory Monetary Policy Committee the external members were conspicuous by their silence. While their charter (agreed with the Minister of Finance) allowed them to speak openly we heard almost nothing from any of the three of them (and of course no disclosure of views or thinking in the minutes of the MPC either). The contrast with models like the central banks in the United States, Sweden, and the UK was stark.

This year there has been some sign of progress, albeit only from one of the members (whose approach may not be terribly popular with his MPC colleagues or – though they have very limited say – the Reserve Bank Board). The member in question is Prasanna Gai, a professor of macroeconomics at the University of Auckland and someone who spent the early part of his career at the Bank of England (and has had various other central banking involvements since). On paper he appears by far the strongest of the externals (and probably more so that at least of the internals), even if there is something less than ideal about having someone serving at the same time as an MPC member and on the board of the Financial Markets Authority. We also know nothing directly about his view on the state of the economy or much about his thinking about policy reaction functions etc, although we can deduce from his two recent speeches that he is probably the key player in the rather heavy (over)emphasis on uncertainty from the MPC in the last six months.

I wrote a few months ago about Gai’s published views (to be clear, from before he became an MPC member) on how Monetary Policy Committees should be functioned and governed. That post was shortly after his first speech

But in the last few weeks there have been two more sets of (fairly brief) remarks, and things have improved somewhat. In their email notification of upcoming speaking engagements, Bank management has noted that the two events were coming up, and the texts of the two sets of remarks are on the website (although you get the impression the Bank might be unenthused because they have not emailed out links, leaving people to remember to go and look for them, or otherwise to stumble over them).

The first of those sets of remarks was about uncertainty (mostly in the light of the US tariff situation), delivered to (it appears) an academic audience in Melbourne a few weeks ago. In those remarks, which were expressed reasonably abstractly, Gai could most reasonably be read as suggesting that the trade policy uncertainty was having a material macroeconomic effect on New Zealand and that fairly bold monetary policy responses were appropriate. I put some comments about those remarks on Twitter, which are in a single document here

While welcoming the fact of the speech, I was a bit sceptical of the argument. But then the good thing about policymakers laying out their thinking is so we can scrutinise, challenge, and engage with those arguments.

Gai’s most recent set of remarks was to some forum run by the Ministry for Ethnic Communities (one of those entities whose continued existence casts severe doubts on government rhetoric about cost-savings and lean efficient bureaucracy – but that isn’t Gai’s fault). There is more about uncertainty (in fact the remarks carry the title “Navigating the Fog – A Tryst with Economic Uncertainty”) although he takes the issue rather wider than the US tariffs stuff. I still wasn’t entirely persuaded, especially by the sentence I’ve highlighted.

Faced with the unknown, and already in the midst of a downturn, economic actors hesitate, delay investments, and reduce engagement. We see this in NZ surveys like the QSBO. Paradoxically, this cautious behaviour, while individually sensible, creates a self-fulfilling cycle. Caution reduces economic activity, which deepens uncertainty, leading to even more caution. Economists call this the “uncertainty trap.” It locks the economy into stagnation. By avoiding risk, we inadvertently create the very uncertainty we seek to avoid. This cycle of inaction feeds into a broader macroeconomic malaise, where growth stagnates, prices become sticky, opportunities are missed, and innovation slows. When everyone waits, nothing moves.

No doubt we can all agree in wishing away a fair amount of avoidable uncertainty (probably most people in New Zealand would count the US tariff uncertainty – regime uncertainty from day to day – in that category) but uncertainty is a part of life and always been. Perhaps it is greater in the short to medium term in democracies and market economies (absolute dictators can, although perhaps rarely do, provide greater certainty about some things over those horizons) so it seems a bit odd to suggest that people dealing with uncertainty is somehow problematic, or even creates uncertainty itself. There is more stuff along these lines in the remarks.

But my main interest in this set of remarks was the section headed “What Can Policymakers Do?”. He seems to think they can and should do a lot. I suspect he is far too ambitious (including on fiscal policy where he observes “At the same time, fiscal policy must step into its own strategic role — by investing through uncertainty and setting the stage for deep microeconomic reform. Where private actors hesitate, public action creates space — catalysing investment in innovation, skills, infrastructure, and housing8. And, like monetary institutions, fiscal policy must be guided by intellectual clarity, coherence, and long-term commitment.”)

But again, my main interest is monetary policy. He writes

In other words, central banks must set the tone for the economic conversation. Their words, emphasis, and structure condition how millions of decisions unfold. They must illuminate the path ahead, not merely comment on the prosaic.

Transparency – describing the macro-landscape by publishing monetary policy statements and modelling scenarios – is helpful, but not enough. What really matters is the capacity to guide expectations. This requires intellectual rigour, deep technical expertise, and the agility to challenge conventional thinking. How we think, rather than who said what, is the essence of credibility when uncertainty is high.

It is important to remember that central bankers wield unelected power7. Direct engagement—through public speeches and testimony before Parliament—brings clarity to uncertainty. Speaking directly about how we think, and what would change our minds, provides analytical accountability that complements procedural channels that chronicle debate – such as meeting records and monetary policy statements. When we open the doors of our policy reasoning to scrutiny, the fog clears and trust builds.

There is good stuff there (and in that footnote 7, which I’ve not reproduced, he refers readers back to the paper he wrote pre-appointment (see above), observing “some of those lessons are relevant for New Zealand”).

He is clearly laying down a marker here advocating for a materially greater degree of transparency from the New Zealand Monetary Policy Committee. The incoming Governor – about whom I will probably write later this week – went on record at her appointment announcement as favouring greater monetary policy transparency (unsurprisingly given that the Swedish central bank has substantively the most transparent monetary policy decision-making etc model anywhere). But you have to suspect it is going to be an uphill battle in an institution with a deeply rooted culture (not specific to any particular Governor) of favouring transparency only when it suits, whereas real transparency and accountability are about openness even when it hurts).

I’m all in favour of much greater transparency (and the new Bank of England MPC model looks as though it could provide a good model). But there is an important distinction between transparency that makes a difference to macroeconomic outcomes and that which largely supports heightened accountability. Perhaps the two should overlap but they rarely do. It isn’t obvious, for example, that the central banks that are much more open, including about differences of views and models among members, or whose MPCs had deeper stores of technical expertise among their membership, did any better at all – in terms of inflation outcomes – through the dreadful inflation resurgence of the early 2020s than, say, the Reserve Bank of New Zealand’s MPC did. But in those countries with greater transparency we know a lot more about the views of individual members and their thought processes and are thus better positioned to assess whether perhaps some are less guilty than others. Individual accountability is, thus, a serious possibility.

My impression is that Gai is much more optimistic about the scope for enhanced transparency to make a macro difference. In a sentence before the block of text I quoted he says “when uncertainty is high and the channels of transmission are weak, communication takes on greater importance”.

Well, perhaps, but only if the central bank has something meaningful to say, otherwise it just ends up as cheap talk. No doubt we can all agree that central banks should always and everywhere indicate that if (core) inflation looks like going off course they will respond accordingly. That is a (much) better place than we (advanced world fairly generally) were in 50 years ago, but it isn’t really much help in grappling the high levels of uncertainty firms and households actually face at times, most of which isn’t about monetary policy. Central banks can’t add much of any use on where US trade policy may go, let alone how other countries might or might not respond. Or whether (let alone when) the AI stock market surge will prove to be a bubble that will burst nastily. Or whether China will invade Taiwan. Or, to be more pointed and winding the clock back five years, what would happen to policy regimes around Covid (lockdowns, border closures etc) – surely the most extreme, perhaps inescapable, example of policy uncertainty in recent times. Central banks generally couldn’t get the macroeconomics right even when the policy uncertainty began to diminish (see inflation outcomes and generally very sluggish interest rate responses). The ability to “illuminate the path ahead, not merely comment on the prosaic” seems very limited in practice in most circumstances. (I think back, for example, to the early days of inflation targeting in New Zealand: we aimed then to be very transparent, and had a Governor who was a strong retail communicator, and yet if we consistently held out a vision – sustained low inflation and a fully-employed economy – we had no certainty to offer as to what it would take or when the payoff would be seen. Bigger central banks that went through similar dramatic disinflations generally found themselves in the same boat.)

But to conclude, it is great to have an MPC member putting his thinking on record (even in this case it is still mostly about processes/structures than the specifics of how the economy and inflation might unfold). Perhaps some journalists might ask him about the speech and seek to tease out his ideas. We all benefit when those wielding power – unelected power in this case as he rightly notes – put their ideas out for information, scrutiny, and debate. Perhaps some other MPC members might think of taking up speaking opportunities that come. Perhaps Gai, who has dipped his toe in the water with a couple of brief sets of published remarks, might consider a fuller version at some point?

When it comes to Long-term Insights Briefings (LTIBs) I sympathise with the public service, I really do. The requirement to produce these documents was introduced by the previous government in fiscally expansive times (core government agency staffing growing rapidly). Even then, it was a fairly flawed idea but if agencies were awash with cash I guess they might as well try to do some analysis. These days, even if the fiscal deficit is not being cut, core government department spending is under considerable pressure, and we have a track record in which the LTIBs that have been produced have rarely added much value. I gather the current amendments to the Public Service Act will eliminate the requirement to produce LTIBs but…..for now government department CEs and acting CEs still have to comply.

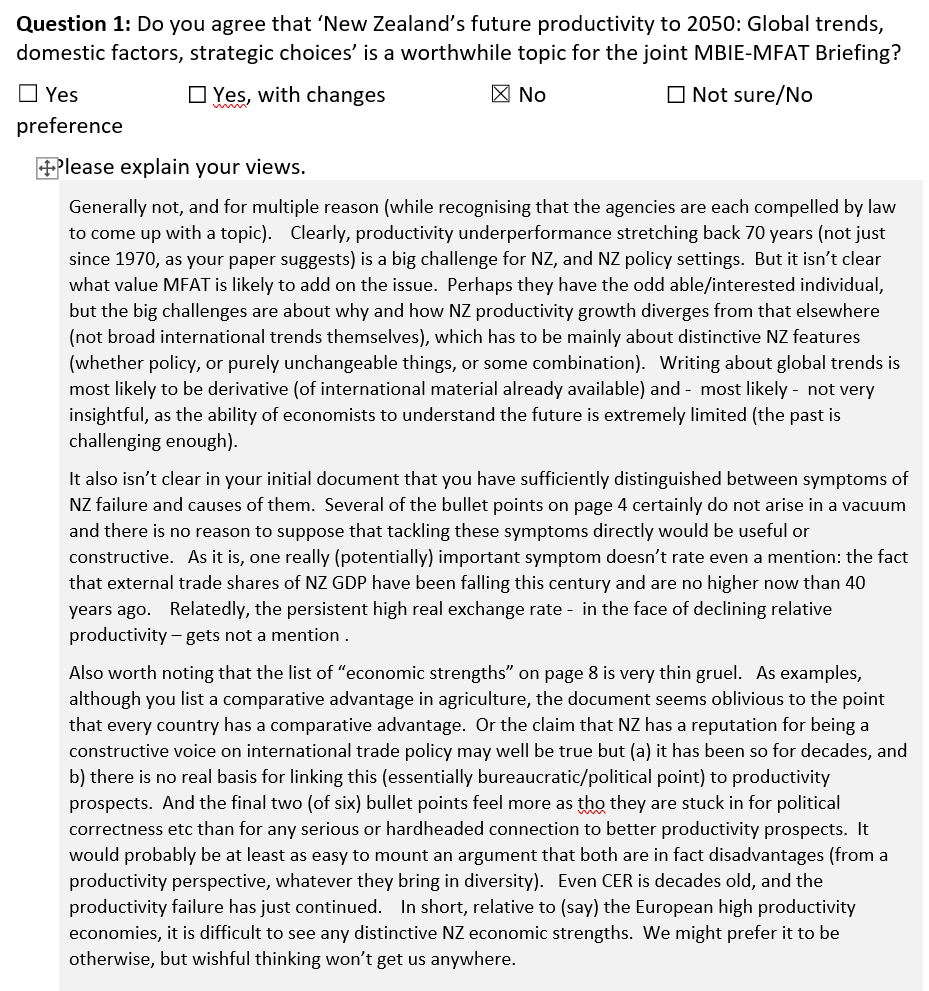

A year or so ago MBIE and MFAT decided to get together and produce a joint LTIB this time round. As the law requires they consulted on the proposed topic

I put in a short but fairly sceptical submission on the topic

Anyway, the bureaucrats have beavered away and last month come up with a draft LTIB (on which submissions close next Monday). They must have refocused their efforts somewhat following consultation on the topic as it is now presented this way.

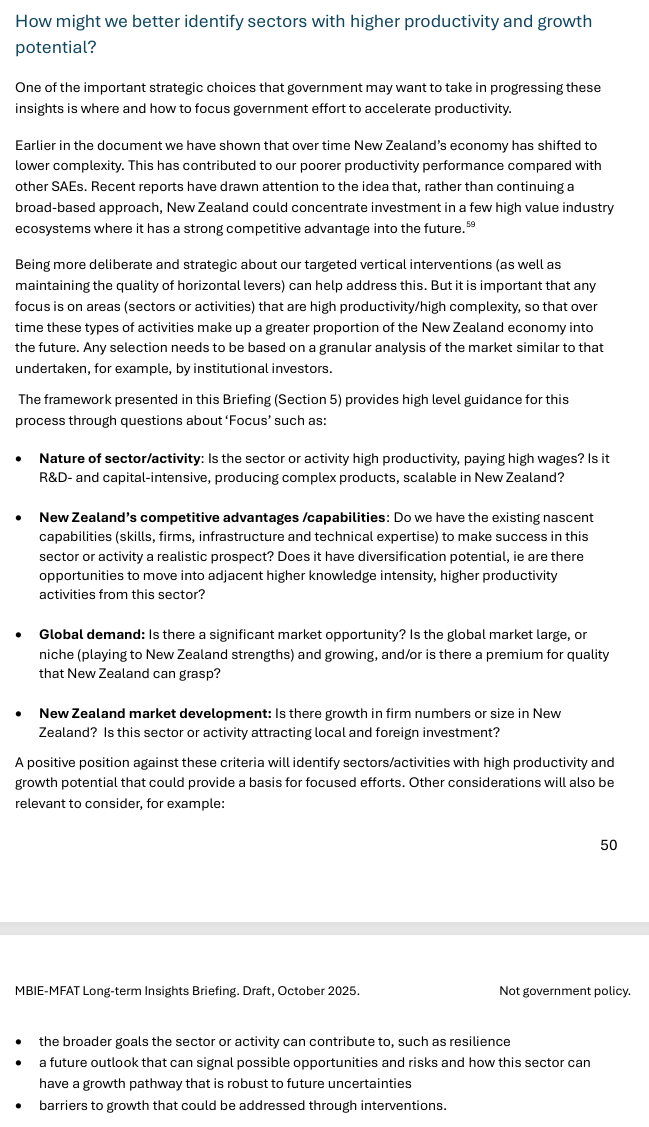

Having made a submission last year they’d included me on their general email inviting submissions on the draft. I’ve been away and otherwise busy and hadn’t really intended to even look at the thing, but there was another reminder yesterday so I took an initial look. It was the “accelerate the growth of high productivity activities” that prompted me to look a little further: the focus apparently was not economywide productivity and policy settings but the sort of “smart active government” stuff MBIE has long championed, involving clever officials and politicians identifying specific sectors to focus on and specific interventions to help those sectors. And, of course, lots of preferential trade, investment, etc agreements (the ones MFAT likes to call Free Trade Agreements). On a day when the dysfunctions of our public sector were on particularly gruesome display it seemed even less appealing and persuasive than usual. In a month when the government had been a) buying a rugby league game, b) increasing (again) film subsidies, and c) subsidising expensive New Zealand restaurants (via the Michelin corporate welfare), all in the name apparently of “going for growth”.

So I decided to sit down and read the draft document after all. It isn’t that long (45 pages or so excluding Executive Summary, glossary, references etc), reflecting no doubt the fact that LTIBs are a compliance cost for agency CEs rather than really core top priority claim on resources. Before reading it I heard on the grapevine last night of a smart person who had opened the document, read the first page, rolled their eyes, and closed the document again. But I persevered….and there is 25 minutes of my life I won’t get back.

Sadly, but perhaps not surprisingly, the draft report is unlikely to be any use to anyone looking for illumination rather than support (the old two uses of a lamppost line).

On New Zealand, we get a fairly long list of symptoms of our relative economic failure, but no serious attempt at analysis of the causes. If you don’t understand the causes, including the roles (positive or negative) of past policy interventions/choices, it is really difficult to see how you tell a compelling story about solutions, unless the document is just a prop for a longstanding predetermined narrative and set of policy preferences.

They then introduce a series of four small advanced economy “case studies” – a page each on Denmark, Finland, Ireland, and Singapore. Not only do they not engage with a really important difference between New Zealand and these countries – ie extreme remoteness – but there is no attempt to understand what drove the successes of these economies either. In each case there is a list of types of interventions that have been or are being used in these countries but no effort at all to assess what role (positive or negative) these interventions have played in contributing to medium-term productivity growth. It certainly isn’t impossible that some might have been helpful, some will almost certainly have been harmful (just consider the range of interventions our governments have tried over the decades), and perhaps many will have just been ornamental or redistributive – not really making much difference at all to the productivity bottom line. And I’m pretty sure that not once in the entire document is there any suggestion of the possibility of government failure, capture etc.

Then the draft report moves on to four domestic case studies (this time roughly two pages each), looking at the dairy industry, space and advanced aviation, biomanufacturing, and the Single Economic Market (mostly Australia but also beyond) with a focus on sector-specific interventions. None of it seems to display any scepticism, only a sense that we (governments) haven’t been sufficiently focused or willing to persist with particular sector supports. Strikingly, in the dairy “case study” there is no mention of the rather large role the government played in enabling the creation of Fonterra, and how the results have, to put it mildly, not exactly lived up to the promised hype.

And the whole document ends with a question that shouldn’t even be being asked by government departments.

But perhaps it is all music to the ears of governments that like specific announceables from week to week? (Whether MBIE or MFAT like those specifics is another matter – quite possibly not, but their mindset and fairly shallow analysis in documents like this helps provide cover for governments more ready to paper over symptoms, toss out some cash to favoured firms/sectors, and avoid insisting that the hard structural issues are identified and addressed).

And this sort of stuff helps keep lots of officials busy and feeling useful.

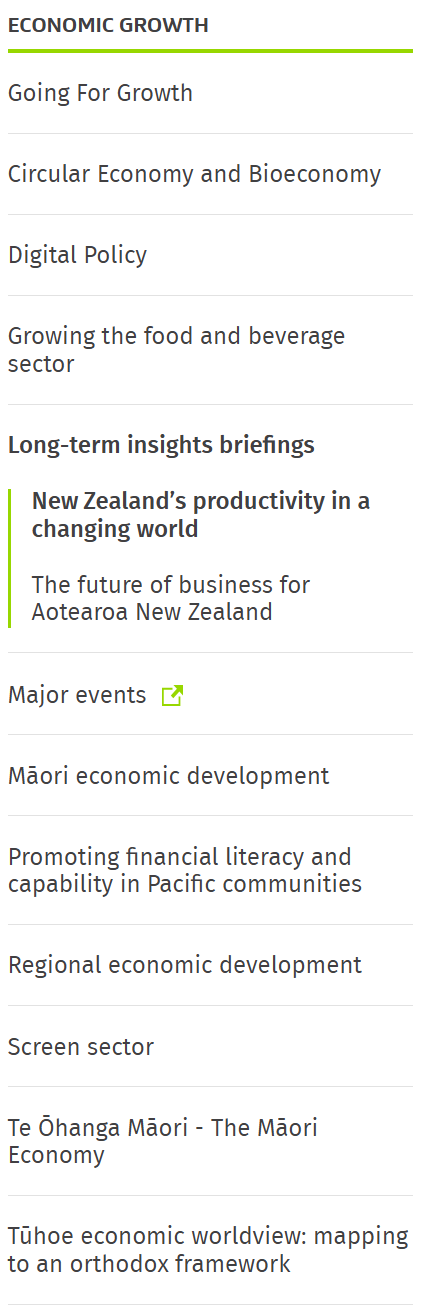

To any MBIE/MFAT readers, no I won’t be submitting, but I’m sure you get the gist. The sooner the LTIB requirement is removed from the law the better, but eliminating that won’t change the mindset. As far as MBIE is concerned, my ongoing unease was only reinforced when on the page with the consultation document on it, this was the list of tabs/items down the side of the page under the heading “Economic Growth”.

We were away for a month and it has taken time to work through the backlog that inevitably builds up over such a mid-year absence. In the meantime, a fair bit more detail has emerged about the Orr/Quigley/Willis saga, between various OIA responses to me, one I’ve seen to another person, a bit more on the Bank’s extravagant new Auckland premises, the Bank’s Annual Report, and the pro-active (but very belated) detailed disclosures about the Orr golden payoff (other OIA responses are still being slow-walked by the Bank). And, of course, we’ve had the announcement of the new Governor and the, perhaps predictable and certainly appropriate, notice of resignation by the temporary Governor (and substantive Deputy Governor). I may eventually get to writing about some of that material, but I have updated my timeline of the Orr/Quigley/Willis saga where relevant.

The Reserve Bank isn’t exactly, in the jargon, a “learning organisation”, but more akin to one determined never to acknowledge a mistake (in a field in which, with the best will in the world, uncertainty means mistakes are pretty much inevitable). The last of the old guard – the Orr team – was at it again last week. Orr may have gone months ago, but Christian Hawkesby (who was the DCE responsible for monetary policy throughout the Covid period itself) is serving out his last few weeks, the other foundation MPC member (Bob Buckle) left just a few weeks ago, and no one expects the manifestly unqualified Karen Silk, the Orr DCE responsible for monetary policy for the last few years, to survive much longer. (There is the old and problematic board too, but monetary policy isn’t their field.) But the face of the latest effort in defence was the chief economist, another Orr groupie, Paul Conway (among many, the line that sticks with me was his closing remarks at the Bank’s early March conference, about having “lost a much-loved Governor”). Time is moving on but they seem determined to defend the Orr legacy, in which they’d all played greater or lesser parts. Specifically, the hugely expensive and risky LSAP.

There were a number of pieces released last Wednesday (links to them all here), headlined by a speech in Australia by Conway, supplemented by some comments from Conway in a Herald article on the Bank’s case (that really the LSAP paid for itself and, what’s more, it is really hard to assign any blame). Of the Bulletin article, “Pandemic lessons on the monetary and fiscal policy mix” by a couple of staff economists I haven’t got much to say: it is wordy and despite 10 pages of references offers little or no insight on the issues or the institution. Perhaps the only line in it that really caught my eye was a heading that claimed that fiscal and monetary policy “Coordination is an intricate and dynamic challenge”, a claim which not only seemed quite wrong, but also at odds with the thrust of Conway’s comments on that issue in his speech (where he seemed, rightly in my view, to be suggesting that what was needed was independence in operations, but keeping each other informed, and exchanging views on what works, what limitations there might be etc). As it ever was, but perhaps now institutionalised in that the Secretary to the Treasury is a non-voting member of the MPC. (Of course, the Treasury is also charged formally with monitoring the performance of the Bank, but the last 18 months suggests how hopeless they’ve been in that role.)

The centrepiece of what the Bank released last week is an Analytical Note by some of their researchers and some IMF staff which uses a model developed at the IMF to attempt to show that really the LSAP was a great success – macroeconomically and that it paid for itself (notwithstanding the $11 billion or so of direct losses incurred). It is a more elaborate version of the framework used by the IMF in a brief early note attached to their 2023 Article IV report (and talked up at the time by the former Governor as offering the “proper story” not some “piecemeal accounting story”), a piece whose claims I unpicked in a post at the time (link a couple of lines up).

So much money has been lost by central banks in the Covid QE interventions – in countries across the advanced world – that too many of those institutions, and their institutional allies (places like the IMF), now seem determined to try to prove a very weak case, that it was really all worthwhile (a case only made harder given the inflation mess that many advanced countries then went through, and which we are still living with the aftermath of). The effectiveness of generalised QE in government bonds – as distinct from specific interventions in dysfunctional markets – has been debated for 10-15 years now but my prior going into Covid was pretty much that of the eminent UK economist Charles Goodhart who in a Foreword to a book I reviewed some years ago (book completed just prior to Covid) opined that in his judgement:

“the direct effect on the real economy via interest rates, with actual or expected, and on portfolio balance, was of second-order importance, QE2, QE3 and QE Infinity are relatively toothless”.

It seemed to be pretty much the Reserve Bank’s approach then too (see this substantive interview with Orr in August 2019, and even just prior to the launch of the LSAP the then chief economist was quoted as playing down the likely impact of such policies), with an explicit preference from the Governor to use negative interest rates (as in Europe and Japan) instead.

I don’t want to bore readers with an interminable critique of all the papers (having already run various posts – eg here in response to some of their earlier claims – over the years of my scepticism that this big asset swap – all it was – made much useful difference to anything, to justify the risk and losses the Bank incurred for the Crown).

So I’m going to work backwards, responding to some of the easier-to-rebut assertions, and only at the end coming back to specific concerns about the particular model they are using in support (recall the distinction between support and illumination).

First, some Conway claims reported in the Herald article

“Conway said it was difficult to isolate the impact of a single tool the Monetary Policy Committee used at a time the Reserve Bank and Government were throwing a lot at the economy to keep it buoyed. He also recognised the collective response caused prices to soar. However, he cautioned against people assuming money printing was largely to blame for the economy overheating.”

You might easily forget reading that that the way our system is set up the Reserve Bank moves last. If the economy overheated – and on everyone’s reckoning it did (both IMF and Reserve Bank positive output gap estimates were very large) – it is the MPC’s fault. It is their job to, as far as possible, lean against the economy overheating (or the opposite) and keep core inflation near the target midpoint. They failed, and that is on them not on the government of the day (which might have run bigger deficits than many were comfortable with, but those deficits weren’t kept secret – most especially from the MPC). Whether or not the LSAP made much difference to demand (Conway believes it did), the responsibility clearly rests with the overall package of monetary policy measures – OCR setting, LSAP, and the Funding for Lending programme (that went on offering cheap loans to banks until the end of 2022). There is no sign in his speech, press release, or interview that Conway – and presumably his bosses – ever really accept that responsibility/blame. Nor is there any real mention of what was actually at the root of the problem: an egregious forecasting failure. Like many/most other forecasters – but unlike them actually wielding power and responsible for outcomes – the MPC badly badly misread the state of demand and resource pressures through Covid, and the result was the inflationary mess that followed. It was hard to get right – few did – but when you take the role you need to take the responsibility. All too few central bankers have. Conway wasn’t there when the worst mistakes were being made, but he now speaks for the institution (and, currently, specifically for Hawkesby, who held the critical role of DCE responsible for monetary policy when it mattered).

But if the forecasting mistakes were pretty common and widespread (inside and outside central banks, here and abroad), the most evident costly failure is purely on the Reserve Bank itself. This is from Conway’s speech

In other words, even granting for the moment the Bank’s view that the LSAP did a lot of good to justify the large losses, really they would prefer not to have used it at all, because a modestly negative OCR would have achieved the same (claimed) benefits without the massive financial risk and actual $11 billion in losses to the taxpayer. Last week’s papers use quite a bit of the passive voice, suggesting that the inability to use negative rates had been something quite out of their control, perhaps something banks were to blame for. Someone, anyone, no one…but certainly not the Bank.

Actually, it was all on the Reserve Bank. An internal working party in 2012 had recommended (I chaired it) that the Bank ensure our own systems and those of banks were able to cope with negative rates should they ever be needed. The then Governor accepted those recommendations, but it seems that nothing happened until it was far too late (it wasn’t until Covid was almost upon them that the Bank realised nothing had been done and some banks – apparently it wasn’t even all – weren’t operationally capable). It is all the more extraordinary because in the second half of the decade the Bank had clearly been doing preparatory thinking for coping with the next severe downturn – there was a thoughtful Bullletin article on options in 2018, and of course that serious interview of Orr’s I’d linked to earlier. But no one seems to have done the basic engine-room sort of work, reviewing with banks their ability to cope with an instrument used in other countries for many years by then. There was turnover at the top – Orr came on board in March 2018, Hawkesby in March 2019 – but it isn’t as if in mid 2019 these should have been remote issues (the OCR had been cut to its then lowest ever level of 1 per cent, and it wasn’t going to take a particuarly savage shock to put zero in view). And yet nothing was done and – on the Bank’s own telling – the cost to the taxpayer was the full $11 billion or so (since they themselves now say they could have had the macro benefits they claim without the risks/losses if only they – Orr, Hawkesby, the 2019 MPC – had ensured basic operational readiness). That was on them, and only them. (Incidentally, the Bank reckone that by Q42020 those issues were sorted out, and yet they went on taking additional LSAP risk – and then incurring further losses – well into mid 2021.)

A learning organisation, the sort that acknowledges mistakes and learns from them, would be quite open about the cost of their own failure. The Hawkesby/Conway Bank, not so much.

All that was on the assumption the Bank was right and there were huge gains achieved through their monetary policy efforts, notably including the LSAP purchases/punt.

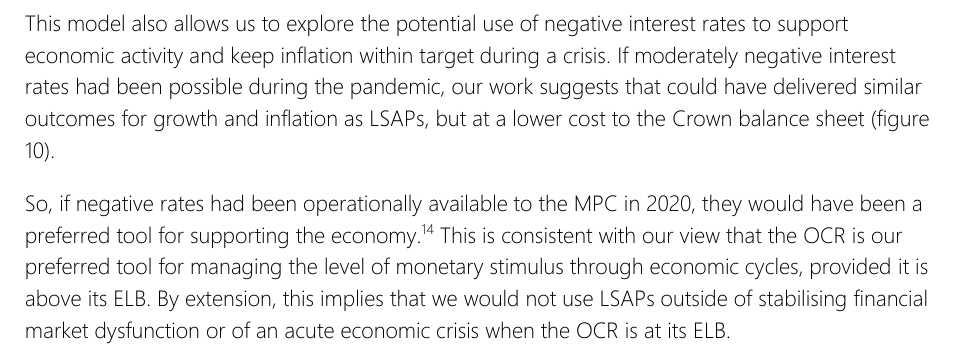

And that rests on two propositions. The first is that there were substantial boosts to GDP, and second that government tax revenue was permanently higher as a result.

Conway used this chart (from the Analytical Note modelling effort)

(No, they aren’t saying tax revenue got to 42 per cent of GDP; it is just an illustrative device).

In principle, if there had been a very deep hole in economic activity which monetary policy choices had closed much quickly than otherwise, there’d also be a windfall gain in tax revenue. (That was the scenario for the highly questionable little IMF exercise in 2023 linked to earlier.)

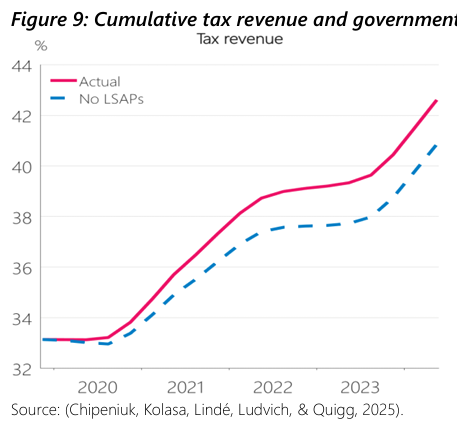

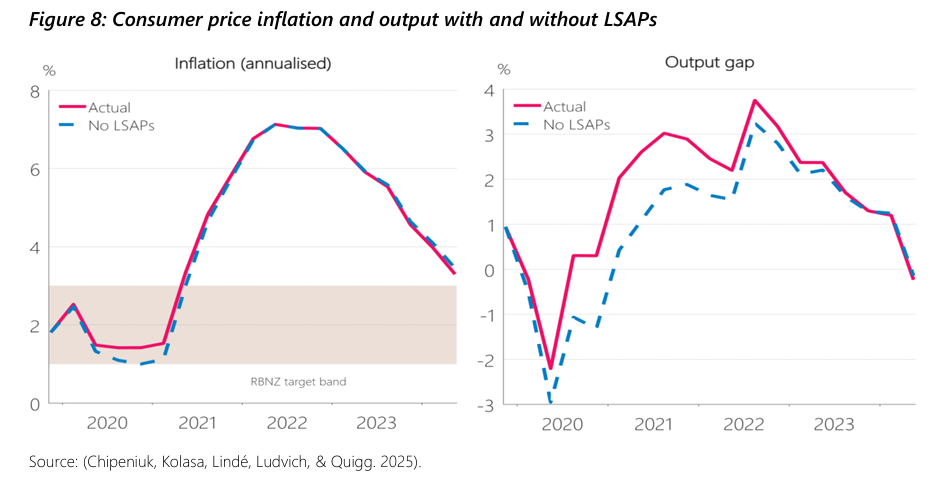

Unfortunately, while in 2020 the Bank thought there was such a hole (eg as late as the November 2020 MPS the Bank thought there was a negative output gap of about 2.5 per cent, which would persist around those levels for the whole of 2021), they are now quite clear in there view that there was no such hole. In their most recent projections, they estimate that even in the September quarter of 2020 (ie straight after the first and longest severe lockdown) the output gap was (barely) positive. And in the real world monetary policy actions (starting from late March) just don’t have such large and immediate real effects as to have made a big difference to activity as soon as mid-August (ie halfway through the September quarter). With hindsight – albeit only with hindsight – monetary policy choices, including the LSAP if it had real effects, were driving the economy further away from a balanced position (ie into a substantially positive output gap, now estimated to have peaked at almost 4 per cent of GDP, and the associated surge in core inflation).

And this is where the Bank’s package last week gets borderline dishonest. Conway uses this chart

which a casual reader might think was all gain. But the chart ends just around the point where the output gap crosses into negative territory, and thus completely – and deliberately (we must assert for a senior policymaker) – ignores the more recent period, in which the Bank estimates that we are now in a materially negative output gap, and will in time have had three years of a negative output gap (ie GDP tracking below potential, with government tax revenue consequences). Pretty much all observers ascribe that negative output gap to the necessary working off of the earlier, marked, RB-allowed/enabled overheating (ie dealing with the inflation). Any honest reckoning of the fiscal consequences needs to take into account the entire period. There probably were some fiscal gains from the Bank’s monetary policy choices – surprise inflation reduced the real debt burden, and resulting fiscal drag picked up some extra revenue – but I doubt the Bank really wants to claim credit for that inflation they weren’t supposed to be aiming for and did not forecast.

Most likely, over the full period, there were modest – but largely unsought and undesired – revenue gains (achievable, see above, with conventional instruments if only the Bank had done its preparatory job – and for central banks, like airport fire brigades, preparation for crises is a core part of the job), but large and easily identifiable losses from the risky punt made on the LSAP.

But all that assumes that the LSAPs made a material difference at all. That has long seemed quite unlikely to me. You can – as the Bank and IMF staff have done – construct a stylised model in which the LSAP makes a material difference, but that model doesn’t really seem to fit very well what was going on, here and abroad, and the LSAP simply isn’t necessary to explain almost everything that did go on.

To be clear, I think most economists will agree that if the LSAP worked it wasn’t as (in the Herald’s unfortunate term) “money-printing”. The volume of settlement cash created – all reimbursed at the OCR – was simply not a material channel. If the LSAP made a difference it did so by one of two (perhaps mutually reinforcing) mechanisms: altering market interest rates in ways that had macro consequences (this is the Reserve Bank’s own story going back to 2020), and/or reinforcing market convictions/views that the OCR will be kept extraordinarily low for a protracted period.

This is from the model Conway hung his hat on, in which he

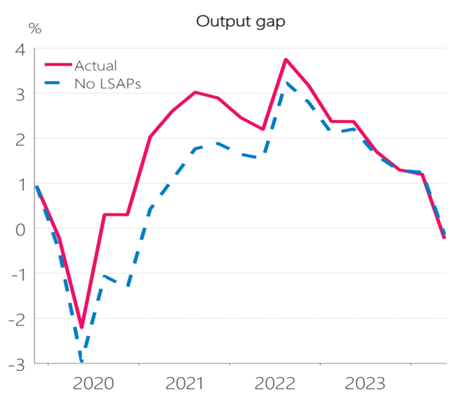

cites the modelling exercise – not an empirical estimation but a stylised representation – in which the choice not to use the LSAP (in New Zealand) makes at peak about 150 basis points of difference to long-term government bond rates (relative to the counterfactual in which only the actual OCR cut was done) and a 20 per cent difference to the exchange rate. In this modelling exercise we are told that most of the work is being done by the exchange rate adjustment (itself responding to changing interest rate differentials), noting that long-term interest rates themselves aren’t a material part of the New Zealand domestic transmission mechanism.

But we are also told that the LSAP was roughly equivalent in its economic impacts to a 100 basis points cut in the OCR. And we’ve had plenty of swings in the relative policy rate spreads of 100 basis points or more (including since 2021) and none of them has resulted in a 20 per cent change in our exchange rate (which has been astonishingly stable over the last 15 years or so).

Another chart from Conway’s speech is this

where you’ll see (red bars) that New Zealand’s use of government bond purchases was one of the largest among advanced countries (similar to the UK and Canada). But you will also see quite a group of countries to the left of the chart that seem to have done little or no QE over this period. Korea, for example, also cuts its policy rate by 75 basis points, but is there any sign of its real exchange rate rocketing upwards because they did no QE? Well, no. And one can run through the other countries and you will search in vain for such large effects (and yes each country has its own idiosyncrasies). Australia did no material QE until the end of 2020 (for much of the year they relied on policy rate cuts and an announced target for a three year rate) and there isn’t any sign of the AUD appreciating sharply against the NZD (where our central bank was actively pursuing QE).

And there are similar problems with the long-term bond yield story. Eyeballing that chart Conway cited, you’d have to think that advanced countries that did no little or QE in government bonds would have seen their long-term government bond yields rise sharply (and, to be clear, the New Zealand OCR was about middle of the pack for how much advanced country central banks cut in 2020). But again, evidence of such effects is sparse indeed. Take Korea again, their long-term bond yields didn’t fall as much as New Zealand’s did, but they certainly didn’t rise in 2020. Nor did Norway’s or Iceland’s – or, indeed, any advanced country. I don’t find it implausible that the scale of New Zealand’s LSAP might have made a bit of difference to longer-term bond rates, but eyeballing the cross-country experiences something like 20-40 basis points looks more plausible – eg our long-term bond rate did fall more than Australia’s in mid 2020.

And that is for a 10 year bond. What matters in the domestic economy is mostly 1 and 2 year rates (including through the mortgage lending and refinancing channel). And so the important question is likely to be whether the LSAP did anything much – directly or by signalling reinforcement effects – to affect those short-term rates. And there I think champions of the effect of the policy will find themselves on the backfoot. Those shorter-term bond and swap rates certainly fell very low (some were briefly slightly negative for a few weeks around September 2020, although by the end of 2020 all the short-term bond yields were at or above the 25 basis points that was then the OCR), but is there good reason to suppose those rates would have been much different absent the LSAP (or with an LSAP brought to an end in say December 2020)?

What else was going on? By late 2020 the Reserve Bank told us the operational issues around negative rates had been sorted out. In the Survey of Expectations (semi-expert respondents), the December quarter survey remarkably – looking back now – had the mean expectation for the OCR a year ahead at -0.16 per cent (with inflation two years out nonetheless still expected to well undershoot the midpoint). The MPC itself had pledged back in March 2020 (rashly) not to change the OCR for a year. And what of the Bank’s own forecasts? With all the stimulus already built in the Bank in the November 2020 MPS was projecting that inflation would stay at or marginally below the bottom of the target range through 2021 and 2022, and that the output gap would remain deeply negative at least through all of 2021. The Bank published “unconstrained OCR” numbers – where the OCR would go if deeply negative OCRs were possible, to get inflation back towards target – getting down to -1.5 per cent by the end of 2021. The fact that those forecasts and expectations were deeply wrong – as we know now – is irrelevant to the fact that that was the air people were breathing (and markets were trading) in late 2020. The prospect of any rise in the OCR any time soon seemed remote, and cuts couldn’t be ruled out (remember that only the MPC pledge to March 2021 had ever prevented the OCR being cut to at least zero).

Is it plausible that the LSAP had some effect on these rates? Well, perhaps. I wouldn’t quibble if someone was suggesting 20 or 30 basis points but…..short-term rates were always going to be much more heavily influenced by expectations of future OCR moves, and – independent of any LSAP announcements – the macro forecasts at the time were very very weak (as actually they were in Australia – check the RBA November 2020 inflation projections).

What of the stylised modelling results themselves? Well, I’d take them with a considerable pinch of salt. You might have hoped that someone in the Reserve Bank with an instinctive feel for NZ business cycles etc (surely there are still one or two of them) might have interjected and asked at some point how it was that this model posited near-instantaneous real economic effects from a change in the real exchange rate (the usual stylised view has been that those lags are particularly long, longer than those for interest rate effecs)

Or someone might have asked how it was – so very convenient – that the model produces only helpful effects on inflation from the LSAP (with no LSAP and a higher exchange rate perhaps direct price effects hold up inflation in 2020), and no unhelpful ones, despite the large positive impact on the output gap. And, as a reminder, it is the standard view that the real economic effects of monetary policy take more like 6-8 quarters to be substantially seen in inflation. If the LSAP made a real and material difference, it should have made one also to inflation – exacerbating the problems – in mid-late 2021, but this exercise somehow manages to tidy away any such effect.

Who can know quite what is driving the people at the top of the Reserve Bank. Perhaps they genuinely believe all this stuff, but I guess if you’d been a prominent part in the loss to taxpayers of getting on for $11 billion you’d have a fairly strong incentive to convince yourself it had all really been worthwhile. And I guess with the current more-moderate personalities at least we’ve moved on from those claims Orr used to make that the benefits had actually been multiples of the cost.

But whatever now drives them, these are lessons I think you should take away:

had the Bank done its basic crisis preparedness job in the years leading up to Covid, LSAP would probably never have been deployed at all (or used only on a much smaller and briefer scale – the Bank also likes to claim they helped settle markets in late March 2020 although the evidence suggests any effect was small and entirely incidental to the Fed addressing problems at source). Orr’s instincts on preferred policy instruments (effective and with much lower financial risk) were correct,

ultimately the major failure was a forecasting one. On the path of forecasts as they were in 2020, 2021 and early 2022, the Bank would still have wanted to be providing lots of monetary policy stimulus for a long time (that is what forecasts of very low inflation and large negative output gaps tell central banks to do – and contrary to Conway’s claim, this had nothing to do with the 2019-2023 specification of the Bank’s target; it would be the same today). Thus, the path of inflation would have been very much as we actually experienced it.

but at least if we were going to experience the consequences of a major macro forecasting failure, the taxpayer wouldn’t have been facing almost $11 billion of losses in addition (to the inflation and the dislocation, still being experienced, in getting rid of it).

responsibility for the substance rests with those in office over 2019-2021 (Orr, Hawkesby, Bascand primarily – and the rest of the then MPC)

responsibility for the spin now rests with Hawkesby, Conway, and (presumably) Silk. Who knows if the rest of the MPC even saw this stuff before it went out. It would be interesting to hear perspectives from some of them – not involved over 2019 to 2021.

Finally, in fairness one might note that central banks generally have not been great at acknowledging failure and mis-steps. But being in bad company really is no defence. Recall that the quid pro quo for central bank operating autonomy was supposed to be serious transparency and accountability, built on demonstrable expertise. All appear to have been lacking at 2 The Terrace.

A couple of weeks ago the editor of Central Banking magazine (something of an house journal for central bankers, and for whom I’ve done book reviews for some years) invited me to write a fairly full article for a non-NZ audience on the extraordinary events of recent months. The request/invitation was for a piece along the following lines:

“The aim would be to provide readers with an insight into how a highly respected institution (internationally, too) ended up in a position where both its top two officials were forced to resign and (perhaps) what steps could to be taken to redress the matter and restore the RBNZ’s reputation for sound governance?”

Having been so caught up in the unfolding detail, writing something like that proved to be a useful discipline, trying to stand back just a little and tell a story.

I wrote the article in the couple of days before we left on holiday, answered the follow up questions, and then Central Banking published the final version on their website yesterday morning (there is a paywall but registration should provide access)

[Link deleted as no longer relevant – see below]

There are only trivial differences between draft below and the final version, mostly the addition [UPDATE: by Central Banking] of various references/footnotes to the published version.

[UPDATE: Both I and Central Banking magazine have received demands to retract and apologise for the article under threat of legal proceedings by Adrian Orr, who appears to have objected to aspects of how his time in office, as a senior public figure and Governor of the Reserve Bank of New Zealand, was characterised. Central Banking has for now removed the article (link above) for further review. I posted the article here initially mainly to help readers who had had difficulty getting free access to the original via registration on the Central Banking website. As I’m currently travelling and cannot easily modify the text to make clear and extensively document a few points I have chosen to delete the article here as well.]

[FURTHER UPDATE 1 Oct: I have now been advised that there has been a “confidential settlement” between Orr and Central Banking magazine’s owner, under which they have agreed to remove the article permanently. The following statement now appears on the Central Banking website.]

UPDATE 21 October

I have decided that I will not republish the text of the article I wrote for Central Banking here, even with amendments. The piece had been written for an overseas audience, and through the sort of lens the magazine had requested. There is copious material on my blog on the events of the last two years, pre and post Orr’s exit, and more snippets have emerged in recent weeks. I hope at some stage to produce a NZ-focused summary account and analysis of those events.

UPDATE: 24 November

Among Orr’s claims has been that in my opinion piece I had alleged that he had “bullied his staff”. I was surprised by this claim. Several weeks ago I asked my lawyers to communicate with his to make clear that I had not made any such claim (and had not intended to do so and did not intend to do so now) and expressed my regrets if Mr Orr had read the text in the way suggested.

A couple of nights ago, shortly after the Minister and Treasury finally released the suite of texts between Willis and Rennie, ZB featured interviewer Heather du Plessis-Allan talking to Herald journalist Jenee Tibshraeny (who has been over the Orr/Quigley/Willis saga issue from day one). There wasn’t anything concrete that was new in the conversation but it was the ending that struck me.

Tibshraeny: In this instance I’m disappointed by the lot of them. I can’t even distinguish who is most culpable and feel like as a member of the public I’ve been misled and it is disappointing.

Du Plessis-Allan: It just looks like a giant cover-up doesn’t it?

Neither of them seem like zealots, let alone anti-government zealots with an agenda. So what a sad state of affairs we’ve come to in this country.

But the Minister has clearly found herself some supporters in The Post (their journalists have also been a bit sympathetic to Orr) with an article this morning where they claim – it must have been music to Willis’s ear – that “overall, Willis appears to have helped rather than hindered the fuller facts going on record while not at any point seeming to defend the Reserve Bank’s own miscommunications”. Which would be an extraordinary claim anyway, but it was belied by the fact that a few paragraphs earlier they had reminded readers that on 5 March, after the deeply problematic Quigley press conference, Willis told The Post journalists that she was satisfied with the explanation Quigley had given for the Governor’s departure. And, of course, none of the explanations given that day (and there were several, mostly designed to have us accept something like “inflation is in the target range, time to do something different, nothing to see here”) were at all convincing, and the Minister – who had urged Quigley to do the press conference – knew that the public had been actively misled then. And if perhaps she coulddn’t predict quite how badly Quigley was going to do when she got him to go out there, there is no sign – not the slightest – that she either expected or wanted him to tell the truth. And, of course, over the subsequent months she did occasionally wring her hands in public, regretting eventually that the Bank wasn’t being a bit more open. But…..she is the Minister of Finance, with knowledge and leverage, not “helpless mother from Karori” putting her thoughts in Letters to the Editor of The Post. She could have acted, she chose not to do so, and if it hadn’t been for the Ombudsman we might still have been dealing with official denial and avoidance, enabled by her. That she enabled the obstruction and coverup for months is nicely captured in this exchange with Heather du Plessis-Allan just six weeks or so ago.

Of course as I noted last Friday there are still material unanswered questions about how the choices – big picture and detailed – of communication of the Governor’s departure (and supportive messaging etc) came together. Statements of that sort don’t emerge in half an hour, and there were material choices to be made. It is hard to believe that no one in the Minister’s office had any involvement, or that they and the Minister were not actively thinking through the issues and risks and options pretty much from the time the Minister got that text from Rennie on the evening of 27 Feb suggesting things would now come to a head fairly quickly. I’ve lodged one more OIA on those matters this morning.

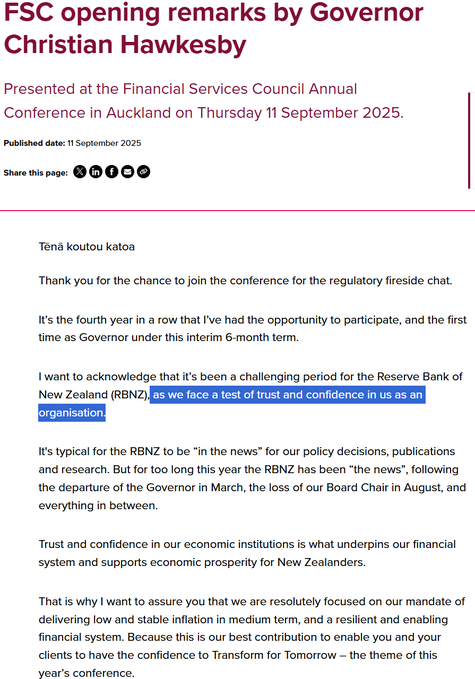

And then of course there is the Reserve Bank itself. The temporary Governor turned up yesterday to speak at the Financial Services Council and began this way

I suppose we should give him a little credit for even mentioning the “test of trust and confidence in us as an organisation”, except that….having giving it a passing mention he went on to talk about inflation.

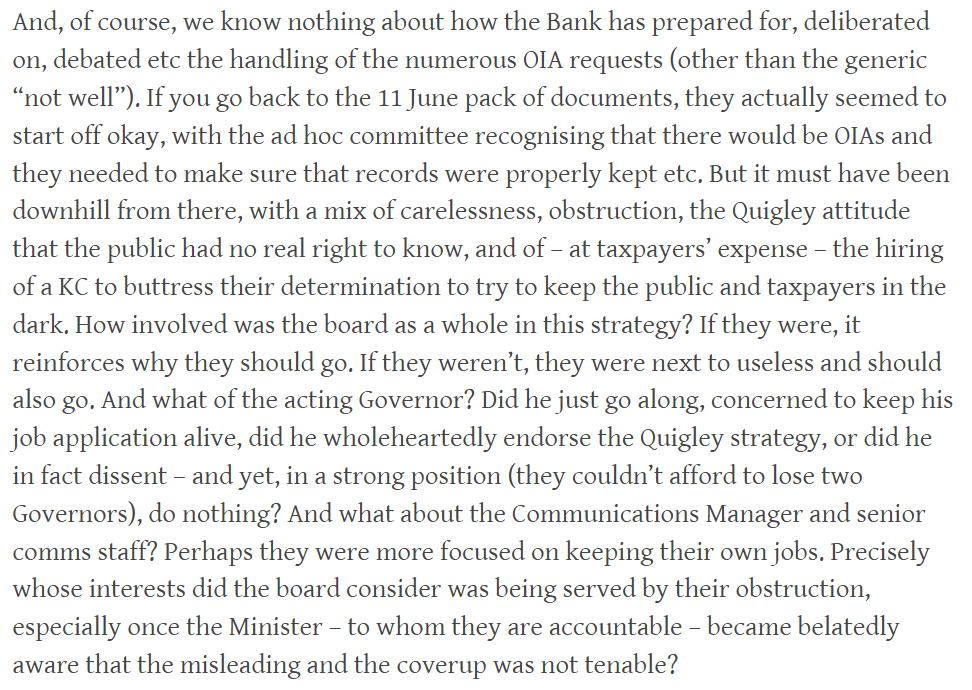

There are still serious questions for all those involved at the top level of the Bank (temporary Governor, board members, key communications staff etc). Rather than write it all again here is a paragraph from last Friday

I’ve also lodged an OIA on those issues those issues this morning. But the wider questions for the Board become even more pointed now that we know they were so intent on getting Orr out that they were likely to recommend the Minister to dismiss him just a few days after their formal process had begun (predetermination and all that?). And yet they still apparently thought it just fine to deceive the public – approving Quigley’s actions presumably – and to go on doing so for months. People of integrity would resign at this point.

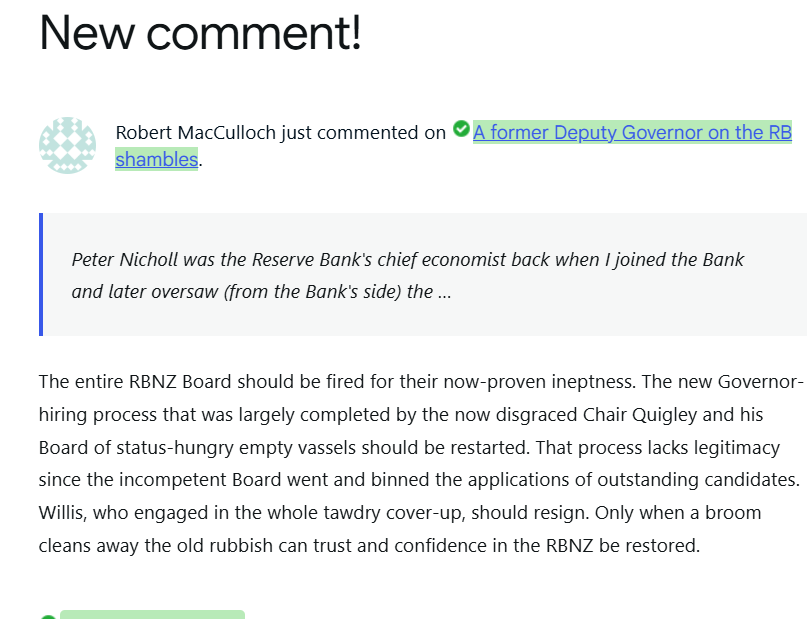

Late yesterday after my short post with former Deputy Governor Peter Nicholl’s article on the Reserve Bank shambles (and specifically the governance failures), Auckland university professor of economics Robert MacCulloch left this comment

Taking his point about the questionable legitimacy of the Quigley-led (and rest of Board) process for selecting a nominee, I’m not sure I’d go quite as far as he does. Time is moving on, and there is a pressing need to have permanent new management in place. On the other hand, quality really matters. So my stance is probably that the Minister (and the wider Cabinet) need to ask themselves very seriously whether any nominee they have settled on really reaches the standard needed now: a first rate independent highly credible person of gravitas, management capability, and some intellectual stature. If they have, well and good. If not, then there would be a case to reopen the process (preferably after sorting out the board members themselves). Rumour hath it (well, a journalist told me) that the nomination has already gone out to the other political parties for consultation. Here the role of Barbara Edmonds becomes really quite important. If she can really be persuaded that a nominee is not just “any warm body, because the job needs filling” but a serious credible and respected figure, then that could be quite persuasive (and recall that the legislative provision Labour introduced requiring consultation with other parties was presumably done in the spirit of the notion that a person appointed as Governor really should command at least grudging respect across the spectrum). But if Edmonds isn’t convinced – and the situation has deteriorated further in the last couple of weeks – she and her leader need to be willing to take Willis aside and say so.

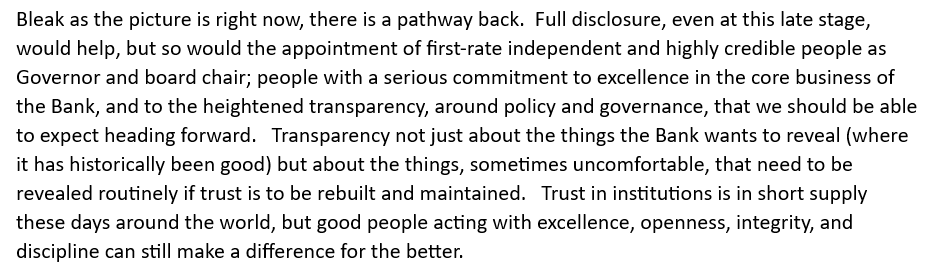

And finally for now on this issue, this is the closing paragraph of a piece I wrote earlier this week on the whole grim saga.

And is that for a while. My wife are heading off on a month’s holiday tonight so it will be at least a month before there is anything more from me here. By then, one hopes, there might have been announcements of strong credible independent people to take up the two key roles, Governor and board chair (and, actually, a new MPC member too). Perhaps some new commitments to greater monetary policy transparency too, along the lines Kelly Eckhold at Westpac suggested last week. But we’ll see.

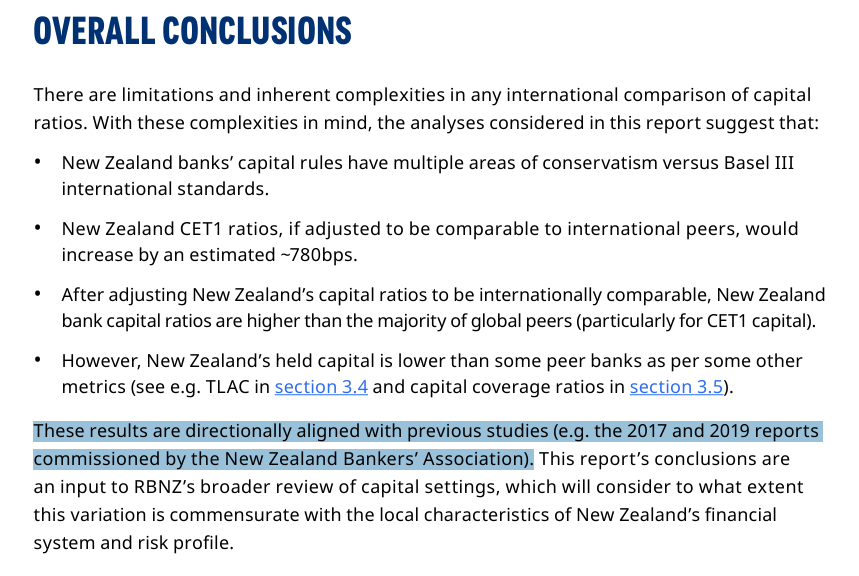

And that means that among the various other things I just never got to in recent weeks was making a submission and a substantive post on the Reserve Bank’s consultation on the capital requirements review that the Minister prompted them to initiate once Orr had gone. As it happens, I don’t have much problem with what they are proposing, and I really strongly welcome the fact that the interim guard (Hawkesby/Quigley) did go to the effort of commissioning a decent external consultant to review bank capital levels in New Zealand and those in a bunch of other somewhat comparable advanced economies (a measurement exercise rather than a policy one). Orr refused to commission anything of the sort when he was still unilaterally in charge in 2019. This was the conclusion of that new report.

My own issue with the entire framework – 2019 (eg here and here) and now – is that it is built on assumptions about the (GDP) cost of banking crises (themselves, the bits able to be ameliorated by capital buffers) that bare no relationship to reality in advanced economies, no matter many decades one looks back. The Bank now justifies sticking with this assumption – which is crucial to any serious cost-benefit analysis – on the grounds that it is “internationally conventional” in such work. No doubt “Internationally conventional” provides a safe harbour for bureaucrats, but it is no substitute for serious thought and critical review.

It is arguable that this unsafe assumption may not matter unduly at present, if market demands (shareholders, bondholders) mean that banks would choose to hold quite high capital ratios even if regulatory requirements were set lower. And of course – another thing not mentioned in the consultation – is that for our largest banks it would be APRA rules that would still be binding even if the Reserve Bank were to adopt an even less demanding model. But we really should be able to expect a higher standard of analysis – including such basics as the ability to distinguish the costs of misallocating credit and real investment in the preceding boom from those narrowly from actual bank failures or near-failures themselves – from our financial stability and bank regulatory agency.