A couple of nights ago, shortly after the Minister and Treasury finally released the suite of texts between Willis and Rennie, ZB featured interviewer Heather du Plessis-Allan talking to Herald journalist Jenee Tibshraeny (who has been over the Orr/Quigley/Willis saga issue from day one). There wasn’t anything concrete that was new in the conversation but it was the ending that struck me.

Tibshraeny: In this instance I’m disappointed by the lot of them. I can’t even distinguish who is most culpable and feel like as a member of the public I’ve been misled and it is disappointing.

Du Plessis-Allan: It just looks like a giant cover-up doesn’t it?

Neither of them seem like zealots, let alone anti-government zealots with an agenda. So what a sad state of affairs we’ve come to in this country.

But the Minister has clearly found herself some supporters in The Post (their journalists have also been a bit sympathetic to Orr) with an article this morning where they claim – it must have been music to Willis’s ear – that “overall, Willis appears to have helped rather than hindered the fuller facts going on record while not at any point seeming to defend the Reserve Bank’s own miscommunications”. Which would be an extraordinary claim anyway, but it was belied by the fact that a few paragraphs earlier they had reminded readers that on 5 March, after the deeply problematic Quigley press conference, Willis told The Post journalists that she was satisfied with the explanation Quigley had given for the Governor’s departure. And, of course, none of the explanations given that day (and there were several, mostly designed to have us accept something like “inflation is in the target range, time to do something different, nothing to see here”) were at all convincing, and the Minister – who had urged Quigley to do the press conference – knew that the public had been actively misled then. And if perhaps she coulddn’t predict quite how badly Quigley was going to do when she got him to go out there, there is no sign – not the slightest – that she either expected or wanted him to tell the truth. And, of course, over the subsequent months she did occasionally wring her hands in public, regretting eventually that the Bank wasn’t being a bit more open. But…..she is the Minister of Finance, with knowledge and leverage, not “helpless mother from Karori” putting her thoughts in Letters to the Editor of The Post. She could have acted, she chose not to do so, and if it hadn’t been for the Ombudsman we might still have been dealing with official denial and avoidance, enabled by her. That she enabled the obstruction and coverup for months is nicely captured in this exchange with Heather du Plessis-Allan just six weeks or so ago.

Of course as I noted last Friday there are still material unanswered questions about how the choices – big picture and detailed – of communication of the Governor’s departure (and supportive messaging etc) came together. Statements of that sort don’t emerge in half an hour, and there were material choices to be made. It is hard to believe that no one in the Minister’s office had any involvement, or that they and the Minister were not actively thinking through the issues and risks and options pretty much from the time the Minister got that text from Rennie on the evening of 27 Feb suggesting things would now come to a head fairly quickly. I’ve lodged one more OIA on those matters this morning.

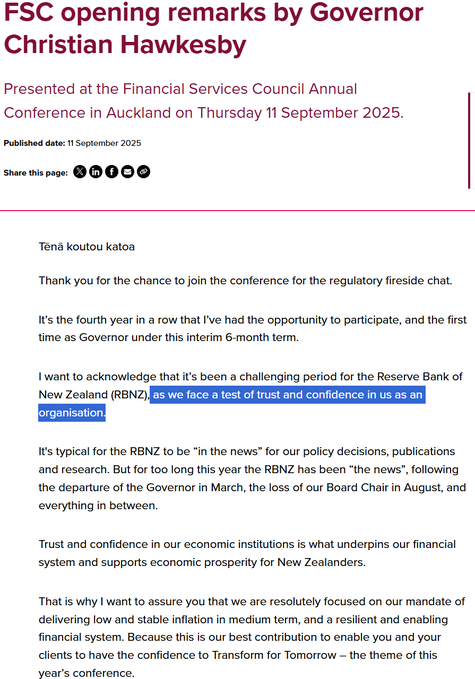

And then of course there is the Reserve Bank itself. The temporary Governor turned up yesterday to speak at the Financial Services Council and began this way

I suppose we should give him a little credit for even mentioning the “test of trust and confidence in us as an organisation”, except that….having giving it a passing mention he went on to talk about inflation.

There are still serious questions for all those involved at the top level of the Bank (temporary Governor, board members, key communications staff etc). Rather than write it all again here is a paragraph from last Friday

I’ve also lodged an OIA on those issues those issues this morning. But the wider questions for the Board become even more pointed now that we know they were so intent on getting Orr out that they were likely to recommend the Minister to dismiss him just a few days after their formal process had begun (predetermination and all that?). And yet they still apparently thought it just fine to deceive the public – approving Quigley’s actions presumably – and to go on doing so for months. People of integrity would resign at this point.

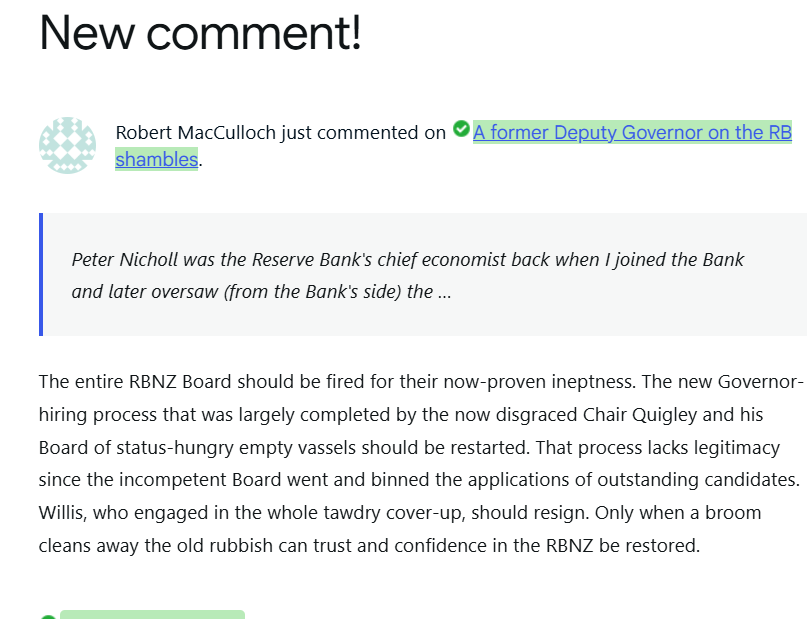

Late yesterday after my short post with former Deputy Governor Peter Nicholl’s article on the Reserve Bank shambles (and specifically the governance failures), Auckland university professor of economics Robert MacCulloch left this comment

Taking his point about the questionable legitimacy of the Quigley-led (and rest of Board) process for selecting a nominee, I’m not sure I’d go quite as far as he does. Time is moving on, and there is a pressing need to have permanent new management in place. On the other hand, quality really matters. So my stance is probably that the Minister (and the wider Cabinet) need to ask themselves very seriously whether any nominee they have settled on really reaches the standard needed now: a first rate independent highly credible person of gravitas, management capability, and some intellectual stature. If they have, well and good. If not, then there would be a case to reopen the process (preferably after sorting out the board members themselves). Rumour hath it (well, a journalist told me) that the nomination has already gone out to the other political parties for consultation. Here the role of Barbara Edmonds becomes really quite important. If she can really be persuaded that a nominee is not just “any warm body, because the job needs filling” but a serious credible and respected figure, then that could be quite persuasive (and recall that the legislative provision Labour introduced requiring consultation with other parties was presumably done in the spirit of the notion that a person appointed as Governor really should command at least grudging respect across the spectrum). But if Edmonds isn’t convinced – and the situation has deteriorated further in the last couple of weeks – she and her leader need to be willing to take Willis aside and say so.

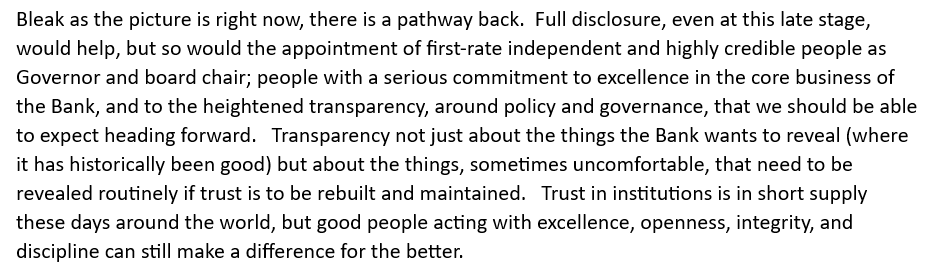

And finally for now on this issue, this is the closing paragraph of a piece I wrote earlier this week on the whole grim saga.

And is that for a while. My wife are heading off on a month’s holiday tonight so it will be at least a month before there is anything more from me here. By then, one hopes, there might have been announcements of strong credible independent people to take up the two key roles, Governor and board chair (and, actually, a new MPC member too). Perhaps some new commitments to greater monetary policy transparency too, along the lines Kelly Eckhold at Westpac suggested last week. But we’ll see.

And that means that among the various other things I just never got to in recent weeks was making a submission and a substantive post on the Reserve Bank’s consultation on the capital requirements review that the Minister prompted them to initiate once Orr had gone. As it happens, I don’t have much problem with what they are proposing, and I really strongly welcome the fact that the interim guard (Hawkesby/Quigley) did go to the effort of commissioning a decent external consultant to review bank capital levels in New Zealand and those in a bunch of other somewhat comparable advanced economies (a measurement exercise rather than a policy one). Orr refused to commission anything of the sort when he was still unilaterally in charge in 2019. This was the conclusion of that new report.

My own issue with the entire framework – 2019 (eg here and here) and now – is that it is built on assumptions about the (GDP) cost of banking crises (themselves, the bits able to be ameliorated by capital buffers) that bare no relationship to reality in advanced economies, no matter many decades one looks back. The Bank now justifies sticking with this assumption – which is crucial to any serious cost-benefit analysis – on the grounds that it is “internationally conventional” in such work. No doubt “Internationally conventional” provides a safe harbour for bureaucrats, but it is no substitute for serious thought and critical review.

It is arguable that this unsafe assumption may not matter unduly at present, if market demands (shareholders, bondholders) mean that banks would choose to hold quite high capital ratios even if regulatory requirements were set lower. And of course – another thing not mentioned in the consultation – is that for our largest banks it would be APRA rules that would still be binding even if the Reserve Bank were to adopt an even less demanding model. But we really should be able to expect a higher standard of analysis – including such basics as the ability to distinguish the costs of misallocating credit and real investment in the preceding boom from those narrowly from actual bank failures or near-failures themselves – from our financial stability and bank regulatory agency.

Yes, Orr/Quigley/Willis again. For everyone’s sake now – well, perhaps except her own – one can only wish that the Minister of Finance would finally decide, more than six months on, to make a full and complete disclosure of what actually went on around the exit of Orr and the aftermath.

Instead, the snippet by painful snippet process continues. Since my post yesterday we’ve learned some more things:

First, questioned by Barbara Edmonds in the House yesterday, the Minister finally gave the gist of texts between her and Iain Rennie on 27 Feb re the commencement by the Bank’s Board of an “employment process”. She and Treasury have withheld these texts for many months, long after she herself was the first to formally disclose (to FEC on 18 June) that there had indeed been an “employment process” prior to Orr’s departure. That in turn lead her to realise – what she’d have known if only she were an assiduous reader of this blog! – that in fact on 18 June she had also told FEC, three times with Rennie sitting next to her, that she’d first heard from him about the “employment process” on 24 February. Last night just before the House rose she made a personal statement correcting this point. No doubt it was an honest, if careless, mistake in June, although it doesn’t reflect very well that there was no earlier correction (when Rennie must have known, or suspected and should have quickly checked afterward, that his minister has mis-spoken).

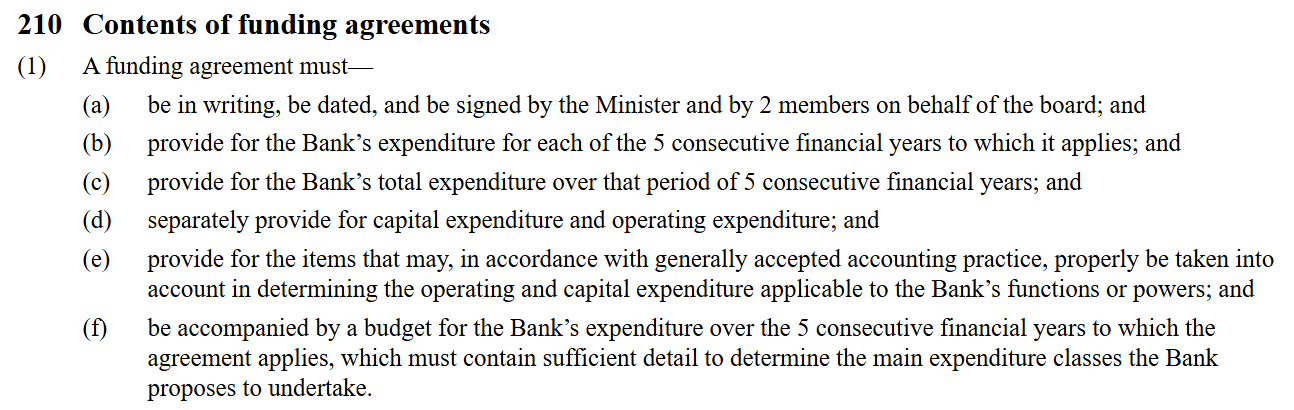

Second, and much more importantly, just prior to 2 this afternoon Treasury finally released the set of texts in full. There are a couple about the funding agreement stance from 14 Feb, which are useful but don’t materially add to the information we already have (although do make clear that Rennie had only spoken to Quigley about the funding agreement bid on the morning of the special 14 Feb board meeting). There is a mysterious one from Willis to Rennie on 17 Feb “Are you coming to the 230”, which has no obvious significance but Treasury must think it is somehow in scope. And then there are the crucial 27 Feb texts.

The first of those adds nothing new, but the second does (going beyond what Willis told the House yesterday). Note that fourth sentence: “Neil’s current thinking is that you could receive recommendation later next week unless decision is taken to go down voluntary exit route”. In context – and given the range of the Minister’s power – this could only be a possible recommendation to dismiss. So not only did the Board envisage their process culminating in a dismissal recommendation (NB an interesting pre-judgement before hearing Orr’s response), but the Minister was fully informed of that (and actually tossed in the observation that the board would need good legal advice, apparently approving of the lawyer Rennie advised her the board was using. (Incidentally, she would also have needed good legal advice had it come to a recommendation to dismiss, given that any decision could have been challenged in the courts). This completely undercuts the line Willis herself has run for months about how it was all nothing to do with her because it was an “employment process” when, as I’ve stressed and the Board, she, and the Treasury clearly knew, she was the one with the (hiring and) firing powers, and only her.

The third development was a question to Willis from Edmonds in the House this afternoon. She asked whether the Minister considered that Quigley’s characterisation of the exit from 5 March (and beyond) as “a personal decision” was misleading. The Minister said that she had relied on Quigley’s judgement that that was all that he could say. Edmonds could have strengthened the question, because Quigley also said on the day that “the Governor had got inflation into the target range and felt it was time to go” and denied that there were any conduct, policy, or performance disputes at the heart of the exit. The Minister is just making up stuff if she believes that any of those lines were really satisfactory, unless “satisfactory” involved keeping the substantive truth from the public. We still do not know – and MoF claims not to either – what NDA provisions there actually were, and nor do we know why the Minister (operating in the public interest supposedly) did not insist on (a) finding out in advance, and b) tightly constraining them so that the public was not misled.

Edmonds moved on to ask why the Minister also didn’t correct the record on/after 11 June (the Bank’s deeply misleading selective release and statement, which tried actively to avoid suggesting there had been any employment issues – even though it was implicit in the existence of an exit agreement). The Minister responded that she had not been aware of the Board’s specific concerns, or of Orr’s responses, or of the terms of the exit, she did not want to expose taxpayers to legal risk, and (supposedly highmindedly) did not “want to politicise a sensitive employment process”). None of this really stacks up. As it is, on 18 June, at FEC (but barely if at all reported at the time – I hadn’t noticed it) she noted, what Quigley had sought to obscure, that there had in fact been an “employment process”, and of all the answers she didn’t have she could – and probably should – have insisted on them. She was aware the Board was driving the Governor out but had no idea what the concerns were? Yeah right. And, of course, decisions around funding, and decisions to fire the Governor were – by Parliament’s design – ones made by politicians. Willis concluded that she had relied on Quigley and he should have done better. Well, of course, but he was her man, and she covered for his approach for months, deceiving the public in the process.

On the final question, Edmonds asked if (rhetorically no doubt) if Willis really believed New Zealanders could trust her when she had withheld information, had known she might receive a recommendation to dismiss etc and (with a final flourish) when it fact it was Willis who had driven Orr out. Willis attempted (rather laughably) the high road, suggesting that Edmonds was free to be the great defender if Orr if she wished, but as for her (Willis) she wouldn’t deign to “politicise” Orr’s exit.

And those were the new developments.

But there are so many questions still outstanding. For the Board, at what point did they engage external counsel to advise on a process that (it is finally clear) they envisaged leading to an unprecedented recommendation to dismiss the central bank Governor? And was this prompted mainly by Orr’s behaviour at the 20th and 24th meetings or had it been brewing even before that? Also for the Board, given that clear direction, how can any of them with any integrity remain in office having been collectively responsible for the 11 June release, which was now even more clearly deliberately deceptive (under a guise of pseudo-transparency).

As for the Minister (and Treasury) it remains inconceivable that we have had the whole story. You, as senior minister, don’t just get a text out of the blue suggesting the part-time (mostly Labour appointed) board might recommend firing the Governor without wanting to know more, unless of course you already knew more. It is beyond belief that there were no discussions after Orr’s walkout from the 24 Feb meeting, and not very likely that – given that Rennie was being used as the comms intermediary (why?) – that no one at Treasury was looking into legal processes, grounds etc.

And, of course, why did she take no steps to ensure that a reasonably honest (not necessarily full or complete) statement was given to New Zealanders on a) 5 March, b) 11 June or c) at any other time up to and including the Ombudsman determination a couple of weeks ago? Whose interests was she serving then? Was her stance more about distancing herself from a process than legitimate legal/privacy issues for Orr?

Someone who doesn’t follow these things much commented to me recently “how can anyone now trust anything the Reserve Bank says?” A good question, but as information continues to seep out from Willis, much the same might, unfortunately, be asked about her. I remain convinced the ousting Orr was well-warranted and welcome, to her credit given the opening Orr’s behaviour created. But not the cover-up, the active misleading, and the obstruction. Or the lack of full disclosure to this day.

It isn’t impossible that you, readers, are getting tired of the still-unfolding Orr/Quigley/Willis saga. You wouldn’t be alone in that. I have many more intrinsically interesting things to do (spent yesterday writing a review of new academic history of US banking supervision from 1798 to 1980, and am reading a history of little-known sovereign borrowing scandal from the early 19th century) but…..we are still short on answers and on accountability, notably from the Minister of Finance, who may have authorised but certainly enabled the systematic efforts led by Neil Quigley to mislead New Zealanders for months as to what went on. At any point, from and including 5 March (the day Orr’s resignation was announced) she could have a) insisted and b) personally ensured that the truth came out. She didn’t and still hasn’t given us a complete and straight story, or expressed any contrition for anything she was party to in the last six months. Deliberate efforts by, and enabled by, a senior minister to mislead New Zealanders would once, and once brought to light, have been treated as a very serious offence (but then, as I noted here repeatedly, MPs never seemed very bothered when Orr made a mockery of their place in the system and actively misled – or worse – them repeatedly). The rot runs quite deep.

Yesterday saw another OIA response from the Reserve Bank dribble in, and with it one more snippet of information. It exposed, once again, my tendency to look for the least-worst explanation, which has been quite unhelpful in making sense of the mess of recent months.

A couple of weeks ago, the Reserve Bank released to me a Letter of Expectations that the Minister of Finance had sent to the chair of the Bank’s board (Quigley) last year, outlining how the Minister expected that the Board would approach bidding for and negotiations on the next (2025-30) Funding Agreement. The Reserve Bank has a website page where it publishes ministerial letters of expectations. They simply never published this particular letter of expectation on that page, or on the website page gathering together material on the 2025-30 Funding Agreement. Par for the course you might reasonably think, given how obstructive and then slow and partial the Bank has been.

As I noted in that post a couple of weeks ago, the Funding Agreement letter of expectation had made it clear that the Minister was looking for cuts. This was the relevant snippet.

But the version of the letter the Bank was released was undated. The Bank had been quite open about the general 2024 Letter of Expectation, which was dated 3 April 2024. It was fine, but fairly general, noting that further detail relating to the next funding agreement would be coming “in due course”.

I guess I had in mind that perhaps that letter hadn’t been written until much later. After all, the existing Funding Agreement didn’t expire until 30 June 2025 (and when Treasury actually got the Bank’s bid in September 2024, the papers suggest they did nothing with it for months anyway, considering it mainly in the context of this year’s wider government budget)

But what the Bank disclosed to me yesterday was that the funding agreement letter of expectation had also been received by the board chair on 3 April 2024.

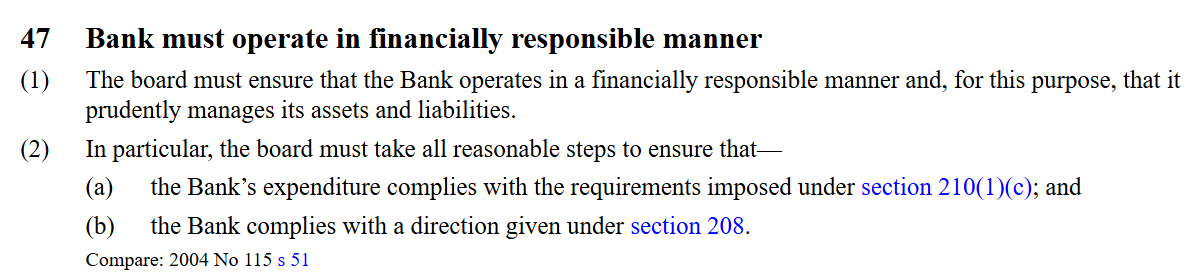

And that matters because it was well before the Reserve Bank board made final decisions about the Bank’s 2024/25 budget. Quite possibly, the Governor was already encouraging the Board to agree to a grand spend-up in 2024/25 anyway – on the dubiously legal, but morally outrageous, basis that their total spending over the five years of the 2020-25 Funding Agreement would still be under the total allowed spending in that term (even though a) the agreement and Act specifically referred to individual year limits, b) the limits for each of the last two years had been reset by Grant Robertson just before the 2023 election, and c) there was a wider climate of spending restraint being driven by the Minister of Finance). Perhaps he already planned that such a spend-up would lock in a level of spending/staffing that might make it hard for the Minister to cut much when the new Funding Agreement was finally determined.

But, on 3 April 2024, he had the Minister’s own words for an interpretation that a Funding Agreement bid would be okay if it involved a 7.5 per cent cut relative to the Bank’s budget for 24/25. Wherever that budget happened to be set, apparently. Talk about dangerous incentives….in a system where the Bank sets its own budget, not directly constrained by (eg) parliamentary appropriations…..and the board signed up to this and went along, setting a budget for 24/25 about 23 per cent above what the Robertson Funding Agreement variation had allowed for that year, and then pitching a new Funding Agreement bid just 7.5 per cent below that level (and far above what even Grant Robertson had approved for 24/25). It was a try-on that really amounted to spitting in the face of the Minister, operating in total disregard to the times (let alone to the wellbeing of the staff, if the double or quits gamble went wrong, as eventually it did).

It is breathtaking all round. The Governor and Board attempted to drive a cart and horses through dangerously loose wording. Neither the Treasury nor the Minister of Finance seem to have had the measure of the people they were dealing with, and both were so asleep at the wheel that (a) when the Bank came back with a draft Statement of Performance Expectations in late April 2024 that deliberately left the budget numbers blank, neither followed this up and insisted on straight answers, and b) when the inflated Funding Agreement bid came in a few months later they sat on it for months and did nothing. No one was dismissed, no one was even severely wrapped over the knuckles. A senior political journalist told me last week that in an interview on 30 October the Minister had, unprompted, indicated that she was going to cut Reserve Bank spending……but she’d done absolutely nothing as the board had run rampant for months, including staff numbers still growing markedly. It wouldn’t be until mid-February that things would finally come to a head. As any parent knows the time to deal with bad behaviour is firmly and early, not leaving the offender with the implicit message that Mum and Dad don’t care too much, only to make a fuss belatedly.

Realising that this Funding Agreement letter of expectation had been received as early as 3 April prompted me to dig out the published minutes of Board meetings from the March and June quarter of last year (from which we are told nothing has been withheld) and the Board chair’s response to the (general) 2024 Letter of Expectations (for some mysterious reason known as the Strategic Issues Letter).

Rereading those documents in the light of what we now know, it is interesting how early both the Bank and Treasury had started work on the next Funding Agreement issues (the February 2024 minutes record that a very senior Treasury official – deputy secretary Leilani Frew, now departed – had been named as relationship manager for the funding agrement process, and the board had approved a memo to Treasury “to establish and agree foundational interpretations relating to the funding agreement and the principles underlying our approach to setting our baseline expenditure forecast”). The May Board minutes record Frew and the macro deputy secretary visiting the board and noted that ‘the work towards the next funding agreement, noting that there has been constructive engagement between RBNZ and Treasury an that baseline savings are in the process of being identified” (but presumably neither Frew nor Board, nor their staff, asked the questions that would have revealed the spending spree the Bank was just about to go on with the draft 24/25 budget – the immediately previous item on the Board’s agenda).

You might have supposed that having (a) had two letters of expectation from the (new) Minister of Finance on 3 April, and b) having a deadline to submit to the (new) Minister of Finance, just about to bring down her first government budget in straitened fiscal times, for consultation/comment a draft Statement of Performance Expectations (including budget numbers) by the end of April, that these sets of documents would be the subject of serious discussion by the Board at its April meeting.

But the Board didn’t meet in April 2024 at all. Now, the March minutes record that there was an (unminuted) “workshop” on 23 April “to discuss the next iteration” of the Statement of Performance Expectations and Statement of Intent Refresh, but those minutes also just delegated to the Governor and chair the authority to sign out to MoF for consultation the draft SPE at the end of April. As it happens, the document was signed out by neither, but by one of Orr’s many deputies. Was the Board aware they weren’t planning to tell the Minister about the planned size of the 24/25 Budget? We don’t know, and the (published records) conveniently don’t show. Did they engage with the two letters of expectation then? We don’t know.

But it seems unlikely, because even if it came up at the 23 April workshop, Quigley had already sent his Strategic Issues Letter back to the Minister on 19 April, purporting to respond to both letters.

Note that he avoided the specifics from the Minister’s letter on the next Funding Agreement and gave only the vaguest indication of a more general approach (“we will consider and respond to”). Surely Treasury (Frew) and the Minister and her advisers should have been put on notice when they got such a vague response? But apparently not, given that they raised no questions/concerns when the budget numbers weren’t included when the draft Statement of Performance Expectations was sent in 10 days later?

There is no suggestion in any of the June quarter minutes from 2024 that the Board ever discussed the Letters of Expectations or thought hard about the implications, or the environment against which they were written. The May minutes do mention the Strategic Issues Letter but only “The Board noted the Strategic Issues Letter”. They seem to have been out on another planet, perhaps led by the nose by Orr, but with no one – Board, Treasury, Minister – providing the sustained vigilance (protecting the public interest and public purse) that was needed. The only Board questions noted in the minutes were looking for assurance that the 24/25 budget was going to be legal – and perhaps Orr’s tame in-house provided some such dubious assurance, as lawyers (in-house and external) are so ready to do for clients – but with not even a hint of a question as to whether such a Funding Agreement blowing budget was right or responsible or was likely to prove sustainable, no stress testing (for example) of what the implications (for people and for the organisation) might be if they did later hit a wall.

It really astonishing (or perhaps not; this is modern NZ) how little serious accountability there is in New Zealand public life. Of course, Orr has gone, but not because of anything he was doing mid-late last year, and Quigley eventually went too – again not because of what he led and did last year but because eventually the post-Orr coverup got a bit embarrassing. I guess too that the relevant Treasury Deputy Secretary has moved on, although there is no hint of that having anything to with being asleep at the (leadership) wheel when the egregious foundations were being laid for the Feb/Mar blowup this year. No board member has been dismissed, or as we understand it even reprimanded, and one was even reappointed this year. The board deputy chair – fully party to last year’s decisions – is holding the fort post-Quigley.

And then there is the Minister of Finance. By far her worst offence was enabling the deliberate deception of New Zealanders for months, when she could have cleared things up at any time she choice (Quigley may have become a nuisance to her, but he was her man, she empowered and enabled him). She still hasn’t been fully straight with New Zealanders. But her role last year – both directly, and in insisting on a more active engaged performance from Treasury – looks pretty culpable. Perhaps if she’d taken a stronger stance from when she first took office, Orr and Quigley would have been reined in much earlier, and the chaos and dishonesty of this year – and damage to her own standing (and the disruption of staff lives) – might have been avoided (many of us were probably glad to see Orr gone in the abstract, but…..no one wanted this).

Remarkably, one other snippet in the May 2024 board minutes is a brief note “the Board discussed the chair’s first meeting with the Minister of Finance”. The government had been sworn in on 27 November 2023, the Minister had been on record with her concerns about Orr personally, and Bank bloat, she’d even promised an independent review of monetary policy. She knew the Funding Agreement had a year to run, but was insisting on immediate cuts elsewhere. It was hardly a quiet and easy corner of her domains and yet she seems not to have bothered meeting with the board chair – her agent, and board wielded the power on prudential policy, where she also had concerns – for months after taking office. You can only shake your head and wonder what she was thinking, and why she made so little effort for so long to use the tools – formal and informal – at her disposal.

It was six months ago this afternoon that the resignation of the Governor of the Reserve Bank was announced, and with it the tangled and ongoing web of deception and obstruction.

I wasn’t planning to write anything today, but information continues to seep out – occasionally proactively, sometimes involuntarily, and sometimes (apparently) through journalists’ sources. In just the last day or two, we’ve learned a whole lot more about the largely unknown – eg the Minister of Finance says she wasn’t aware of it at all – special Board-members-only Reserve Bank Board meeting on 14 Feb, when the Board finally has to stare in the face the reality that their fanciful bid for resources for the next five years was utterly unacceptable to Treasury and the Minister. It also turns out that Treasury’s first advice on the bid that had been lodged back in September, and which is still described as only a “preliminary assessment”, had only gone to the Minister the previous day (that paper was finally released by the Minister yesterday afternoon, Treasury having previously withheld it). None of this had made any of the Reserve Bank’s previous statements (11 June or 29 August).

This morning The Spinoff has a piece with material new details, apparently from an inside source. They don’t change the overall characterisation of the story but they flesh out the picture a bit more. The new snippets I spotted included

Days after that crucial special board meeting (I’ve now requested both papers from the RB)

and on 26 Feb (and note that ongoing obstructiveness, about events that are now months old and will hopefully never recur)

Quigley may have gone but the obstructive approach from Hawkesby and the remainder of the board seems to continue.

I have updated my own more detailed timeline to take account of Spinoff’s information. As and when anything more emerges I will attempt to update it but there is a standing link here.

It is worth being reminded of others things the Bank still refuses absolutely to disclose. I had a request in a couple of months ago for just the elements of the exit agreement governing a) the process for agreeing a statement [ie for the 5 March announcement] and b) the non-disclosure terms. The Bank has refused to release that information – so the public has no idea what secrecy they committed themselves (or Orr) to, as regards the departure of one of the most powerful and controversial officials in New Zealand. The Ombudsman lived down to form and confirmed to me yesterday that their office is backing the Reserve Bank on this one, despite what would seem to be a clear public interest now (and long since) in transparency (whether through release of specific documents or summaries of them – the latter done in last week’s partial timeline).

There are two other things where nothing material has been revealed yet. The first relates to the 5 March announcement itself, and the second to the subsequent RB obstructionism.

Nothing in the selective pack of documents released on 11 June, or in any OIAs since, has revealed anything about the bringing together of the Reserve Bank statement announcing the resignation on 5 March. The Bank seems to have known for several days, probably since the previous Friday (28th) that Orr was likely to be going, and agreement on exit agreement terms appears to have been reached by Monday 3 March (although not signed until 5 March). You don’t bring together a document like that press release on such a sensitive issue in half an hour, or without multiple drafts or sets of edits. There must have been discussions about the approach that should be taken – “just how untruthful and misleading can and should we really be?” sort of thing. We know from disclosed documents that Orr and his lawyers had to clear out and they presumably had both wording requests, objections to other proposed phrasings, and probably received pushback on their own proposed lines. There is also nothing about how Quigley’s mid-afternoon two sentence addition statement (which explicitly introduced the “personal decision” bait, reinforcing the line that it was about “inflation job done, time to go, nothing to see here”) came about. Did anyone – other board members, acting Governor, senior comms managers, legal staff – raise any objections? Did they even see what Quigley was planning to say before it went out? Was there any prepping of the board chair for his press conference that afternoon? (it would seem inconceivable in general not to have – someone inexperienced in a press conference on a highly sensitive issue – but after six months of this few things would surprise any longer). Oh, and of course, what input – or visibility – did the Minister or her office have as the comms strategy and press release were formulated (loss of a major economic official etc)?

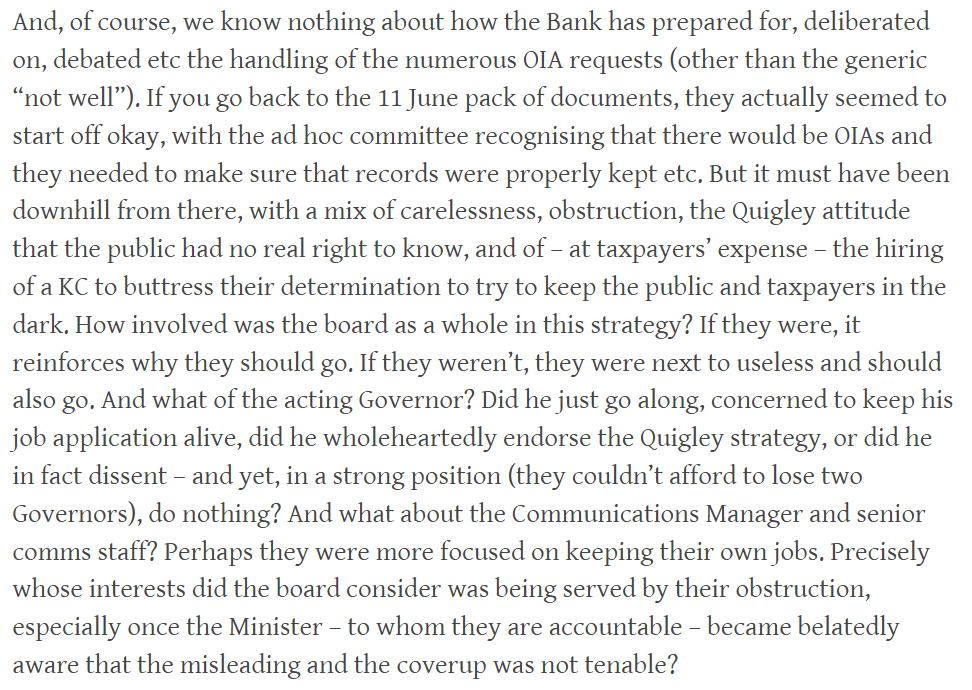

And, of course, we know nothing about how the Bank has prepared for, deliberated on, debated etc the handling of the numerous OIA requests (other than the generic “not well”). If you go back to the 11 June pack of documents, they actually seemed to start off okay, with the ad hoc committee recognising that there would be OIAs and they needed to make sure that records were properly kept etc. But it must have been downhill from there, with a mix of carelessness, obstruction, the Quigley attitude that the public had no real right to know, and of – at taxpayers’ expense – the hiring of a KC to buttress their determination to try to keep the public and taxpayers in the dark. How involved was the board as a whole in this strategy? If they were, it reinforces why they should go. If they weren’t, they were next to useless and should also go. And what of the acting Governor? Did he just go along, concerned to keep his job application alive, did he wholeheartedly endorse the Quigley strategy, or did he in fact dissent – and yet, in a strong position (they couldn’t afford to lose two Governors), do nothing? And what about the Communications Manager and senior comms staff? Perhaps they were more focused on keeping their own jobs. Precisely whose interests did the board consider was being served by their obstruction, especially once the Minister – to whom they are accountable – became belatedly aware that the misleading and the coverup was not tenable?

Questions – more questions – and perhaps the basis for further OIAs if anyone chooses to ask.

Meanwhile, six months on we still don’t have a permanent Governor. Reports suggest the process is fairly far advanced, but how much confidence can we have in someone this board – chaired by Quigley until Friday afternoon – will have come up with. There is a crying need for a first rate candidate, and not one tarred by the Orr years or the months of obstruction. We must hope the government insists on one, but given the Willis/Luxon record to date – slow and weak in dealing with RB matters, not showing that much sign of caring much – it is difficult to be optimistic. And if the government goes along with a mediocre nominee, we must hope the Opposition parties insist on excellence, and don’t just nod through someone on “any warm body” grounds. A first-rate board chair also seems vital – including to both support, counsel, and challenge the new Governor – and it seems unlikely that that person can be found among the compromised existing board.

I think my post yesterday made a pretty conclusive case that the Minister of Finance had been fully part of the choice to deliberately mislead New Zealanders about what went on with the resignation of Adrian Orr. It might, initially, have been a fairly passive involvement re the proposed comms lines – when she, as responsible minister, should have been taking the lead in the run-up to 5 March, not leaving things to Quigley and the post-Orr Bank management (who, to put it mildly, do not have a strong track record on openness and accountability, or much sense of the likely public and political interest and risks). But she and her office quickly became fully part of it – prevailing on Quigley to do a press conference, knowing that it was exceptionally unlikely he was going to tell the truth, never challenging his statements before they went out, and signalling to the media afterwards that she was comfortable that a sufficient explanation had been offered. And then for months, even as it appears she gradually realised the coverup wasn’t going to prove tenable and offered occasional rebukes of Quigley, she continued to defer to the Bank/Quigley and used none of the knowledge or leverage that she had to force a more truthful set of disclosures. When finally Quigley was tossed overboard on Friday, it was only in the wake of fresh public furore about stuff she’d known of all along, and even then her press release just (so she says) recycled Quigley’s excuses for going – “the good job, well done, time to move on” stuff, Quigley had for a long time tried to deceive us with about Orr. Yes, she got more honest in her radio interview shortly after, which was better than nothing but not a great deal.

All in all, it should be quite unacceptable behaviour from a very senior minister. And even at this late stage there is no contrition, no sense that she might ever have done anything better or different. In face of the pretty clear set of facts it is both unconvincing, and leaves her looking weak (prisoner of Quigley gone rogue, sort of thing).

When I wrote that post yesterday I hadn’t heard the interview/exchange on Radio New Zealand earlier that morning (audio here, article here). Willis was no more convincing than in any of her other defences (eg as reported by the Herald, in an article linked to in yesterday’s post). She knew, she actively deferred to the Board chair for months, and at any time she could have insisted on more truthful explanations (even if the RB persisted in its own obstructive OIA responses). But I wanted to touch just briefly on a line she used in that interview yesterday, where she claimed that the independence of the central bank needed to be respected, and it would have been quite inappropriate for her to be involved in anything around Orr’s exit.

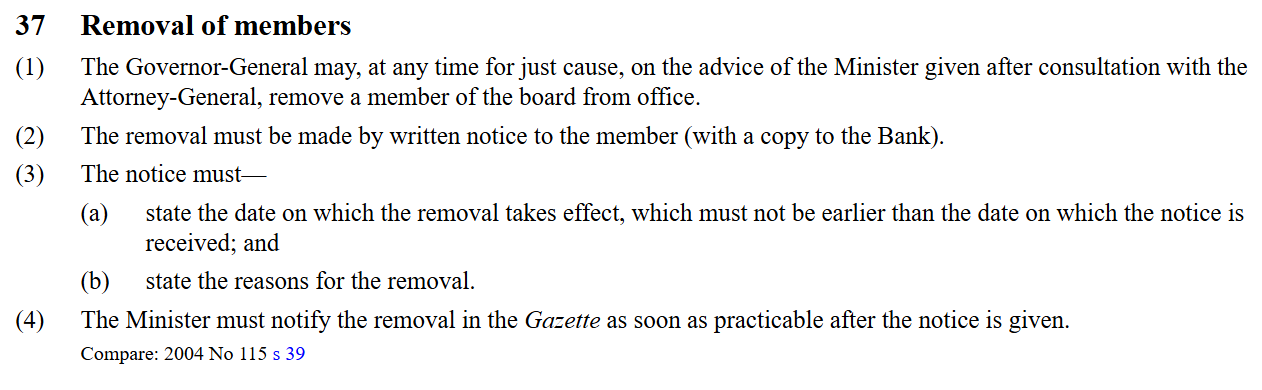

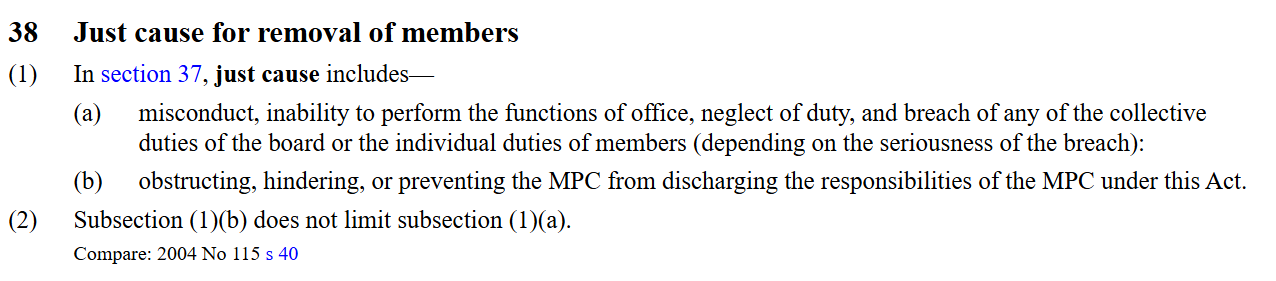

The Minister knows very well that the Reserve Bank legislation is carefully designed to distinguish matters over which the Bank has policy-setting responsibilities (eg many areas of prudential policy, such as bank capital requirements), where the Minister sets the goal but the Bank has operational autonomy (around monetary policy: the Minister sets the inflation target, the MPC adjusts the OCR to (aim to) deliver inflation near target), and where the Minister has primary responsibility. The old mantra was that Act was designed to balance operational autonomy with accountability, and to delineate carefully where it was that ministerial powers and responsibilities should be, and needed to be, exercised. One can debate the structure of the Act – I do, in a number of respects – but it is the law, and the Minister voted for the current legislation when it went through the House in 2021.

No one, but no one, seriously suggests that the issues that prompted Orr’s departure (announced on 5 March) had anything at all to do with the conduct of monetary policy (where it is important for the Minister and Prime Minister to keep their distance, not offering OCR advice in private meetings). As far as we know – and the Minister says she hasn’t seen the letter of complaint – the issues the Board sought responses on related to Orr’s personal conduct, and issues around trust in the context of a breakdown over Funding Agreement negotiations. There has never been a hint that monetary policy decisions were in the mix.

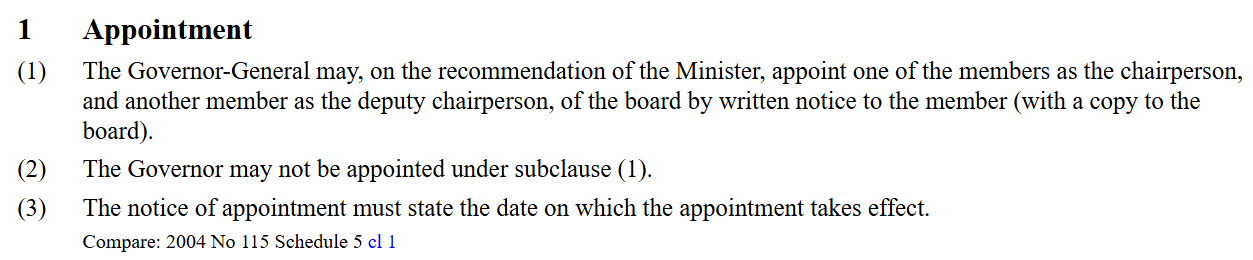

And the Act is quite clear that hiring and firing a Governor is finally a matter for the Minister (and Cabinet). The Board has roles in some of that – the Minister can only appoint as Governor a person the Board nominates (she is not bound though to accept any specific nominee), and the board can offer thoughts on whether the Governor’s performance or conduct rises to dismissal level, but even there the Minister (and only the Minister) can act to remove the Governor without a recommendation from the Board. Orr’s resignation was, as the law requires, submitted to the Minister, just cc’ed to the Board. So the repeated claim from the Minister that it was really important that she had nothing to do with any of it (was just a passive bystander, updated only when necessary) does not stand a moment’s scrutiny. Not only did the law give her a perfectly valid role, but so – frankly – did commonsense. In Opposition she’d objected to some of board appointees Robertson had made, who were mostly still there in February 2025. She knew that Quigley’s public handling of some past Bank issues had been questionable (to put it charitably). Wouldn’t any sensible senior minister, informed (say) on Friday 28 February that it was now all but certain that the Governor was going, after “employment discussions” initiated by the Board, have been all over the proposed communications lines? She might not have wanted her hands, or those of her office, to be too visible, but to sit idly by while the Bank (and Orr) dreamed up comms line – which would inevitably face robust external scrutiny – was to (voluntarily) make herself a hostage to fortune. That would be both risky and inept.

But the real point of this post wasn’t to repeat ground from yesterday. Instead, I want to put the Minister’s highly questionable part in the events of the last few months in the context of her overall handling of Reserve Bank issues since her days in Opposition.

Anyone who watched FEC hearings prior to the election could detect the frosty (at best) relationship between Orr and Willis. At times she did ask searching questions, and Orr did not like that, and tended to treat her – as so many of those who challenged or criticised him – dismissively. But there was never much follow through from Willis.

National opposed Orr’s reappointment, when (as the new law required) the other parties in Parliament were consulted. It was good that she did, but her central argument was half-baked (at best) and thus undercut the thrust of what could have made it hard for Robertson to proceed.

The point in the first sentence of that clip from her letter was quite right – and one hopes she bears that approach in mind with the appointment to be made shortly – but she’d already undercut the case with the half-baked “it’s election year argument”. People like me, who agreed with the bottom line (it really was dreadful that Orr was reappointing, leading us to this year’s mess), had to distance themselves from such an ineptly made case.

In Opposition she made much of the need for a strong independent inquiry into monetary policy during the Covid period (pushing back against the adequacy of the Bank’s own rather self-congratulatory and premature review of the MPC). One could debate how useful it might be, but it was a strong commitment, but nothing happened. (Curiously, in the March 2025 Board minutes there is this

and yet still nothing has been seen or heard.)

They made quite a bit about the staff bloat and loss of focus in Opposition, but then what?

Even in Opposition, there was no follow-up when Quigley was caught out actively misleading the Treasury, which in turn prompted them and Robertson to mislead the public in (about the infamous ban on experts serving on the first MPC).

It was pretty clear when National was in Opposition that they’d have preferred to be rid of Orr if they could. I pointed out back then (in a post prompted by a conversation with an interested party) that he couldn’t just be removed, but that there were quite a few things that could be done to put pressure on, to encourage early change, to improve how the MPC worked, and perhaps even to prompt Orr to think it really wasn’t an environment he wanted to stay on in). Almost none of it was done.

Quigley’s term as chair expired on 30 June last year. He’d covered for Orr for years, he’d led the board that recommended the reappointment, he’d been responsible for the blackball (and the lies), and he’d been chair since 2016. It was no-brainer to replace him, and would have been entirely uncontroversial, but she didn’t. She didn’t even keep the board fully manned (she was stuck with the Labour appointees until their terms ended, but you have to use the leverage and opportunities you have).

She did nothing to overhaul the charter for the Monetary Policy Committee, to encourage greater openness and accountability, or an expectation that members would be available for speeches/interviews. She seems to have done nothing more generally to encourage scrutiny and openness – it is now almost 11 months since the Governor or any second tier Bank person gave an on-the-record speech (extraordinary by modern central banking standards).

And if she did appoint two new MPC external members when the terms of the two 2019 originals finally ended, and the new ones appear to have been an improvement…..but we can’t really tell because we hear nothing of or from them. And then, again for reasons that escape understanding, she extended for one last six month period the last and elderly external MPC member from 2019 who’d been there through all the policy mistakes and communications lurches of recent years (that position now needs to be filled in the next few weeks).

We might also give her some credit for this year appointing a bit more economic expertise to the Board, although both appointees seem stronger on macroeconomics, which the Board isn’t directly responsible for, than on the regulatory side of things which the Board has direct responsibility for.

And what about the organisational/management side of things? Given the Minister’s evident unease about Orr, and her (quite appropriate) Opposition concerns about use of resources, you’d have thought that on coming into office she’d all over this (herself, and on her behalf her office and The Treasury) making life much less comfortable for the Bank from day one, even if (as was the case) they had a generous Funding Agreement running through to 30 June 2025.

Instead what we got was little and feeble for far too long.

Take last year’s Letter of Expectation to the Board (dated 3 April) These documents can’t compel agencies to do anything in particular, but wise boards are sensitive to the emerging expectations and priorities of ministers. There is six pages of the letter but nowhere does the Minister hone in on the very rapid increase in spending and staff numbers and signal a need for cutbacks. There is just woolly generic stuff

This was written in the run-up to last year’s government budget. Most departments were facing cuts immediately, and one other independent agency – ACC – while not directly controlled by ministers decided that, reading the times, they’d make savings anyway. It wasn’t even suggested to the Bank. And although there was a reference to the future

which should have been enough for a Board attuned to the times, it was pretty thin gruel and there is no sign the Minister ever sought to use the moral authority of her office, her bully pulpit.

The Bank doesn’t include the specific Letter of Expectation they got a bit later on the next Funding Agreement with the other documents on that deal, but it is here. I pointed out last week that, reasonable as it seemed, it contained a rookie error

talking in terms of savings relative to the Bank’s 24/25 budget, rather than savings relative to the Funding Agreement limits for 24/25. And even then, you might have hoped that in an agreement reached only every five years, in an institution that the Minister knew had lost focus and discipline, you might want a zero-based case for spending rather than just trimming the last level your predecessor happened to approve.

But, of course, it was all worse than that. The Bank actually set a budget that was about 23 per cent in excess of the Funding Agreement limits for 24/25 – fully and unanimously endorsed by the board – and when they had to consult the Minister on the Statement of Performance Expectations for 24/25 they simply left out the numbers. They didn’t tell the Minister what they were planning to spend. And neither she nor Treasury insisted on finding out. It isn’t clear when they finally realised, but it looks like not until very late last year at the earliest. And even when they did there is no sign of any consequences for anyone. There is no robust letter from the Minister rebuking the Bank for such egregious excess (and even if the Bank has a KC who claims – as lawyers do for their clients – that it wasn’t strictly illegal, it was entirely out of step with the thrust of government policy, and the times), the board chair wasn’t sacked, and no board members were removed (another of them was actually reappointed this year).

And then of course there was the egregious Funding Agreement bid approved by the board (unanimously) in late August and lodged with Treasury in September 2024. In a sane and serious world, Treasury would have opened the document, realised the gamesmanship that was afoot (at taxpayers’ expense) – this was trying to set a base for the next five years using the bloated 24/25 budget as base, not the previous Funding Agreement limits – and a) sent it back immediately, with clear expectations of something much lower, and b) immediately informed the Minister of what was going on, and advised her to call in, or write to (or both), the chair and the Governor to make clear that not only was the budget itself a fundamental breach of trust, but that the new bid was egregious and utterly unacceptable.

[UPDATE: This afternoon (4/9) MOF proactively released various documents relating to the Funding Agreement. Among them is Treasury’s preliminary assessment to the Minister of the Bank’s Funding Agreement bid, which is dated as late as 13 February.]

But there is no sign that the Minister did any of that, or that her expectations of Treasury monitoring of the Bank were sufficiently clear that Treasury did anything either. It seems not to have been until very early this year that the Bank finally began to get a sense that the bid was not going to fly.

In the end, she sort of got there. The final Funding Agreement limit was a lot lower than the Bank had wanted – and involved big dislocation for the Bank and staff because of the unauthorised spree the Bank had continued on with last year, when the Minister could have acted to bring it to a halt much earlier. Even then of course, the cuts relative to the Robertson levels were modest, and the current restructuring seems to be taking staff numbers back to about 2023 levels, probably still 50 per cent above what is necessary. And the Governor and board chair are now both gone. But what a messy and inadequate way to have got there.

It isn’t as if everything she has done as regards the Bank has been bad or wrong, but most of it has been late and/or weak, when she knew from Opposition days that it was a problem institution with a highly problematic chief executive. Who knows why. I wonder if some of it was that she just didn’t care much (it was a below the radar issue with no votes in it) and perhaps she was rather out of her depth (eg the limp arguments recently about independence, showing she has no deep feel for the legislative model, or an ability to articulate it). She seems to have been poorly advised, and ill-served by his own advisers and by The Treasury (which has since cleaned out and replaced almost all its senior managers).

But all in all it is a deeply underwhelming performance from such a senior minister. And if that stuff is just regrettable, avoidable and expensive, the coverup and deliberate sustained intention to mislead New Zealanders around Orr’s departure is inexcusable: weak, inept, and dishonest.

UPDATE: While I was typing this post I had an email from a senior political journalist who passed on this snippet (with permission to use it)

“On October 30 I interviewed Willis about her role as State Service Minister. So it was not an economic interview, per se. At the end of the formal part of the interview we chatted about a few things but we did not discuss the Reserve Bank until she brought it up and said she was determined to cut back its funding.”

Which is interesting, and perhaps consistent with my story. Her instincts were sound – the funding needed to be cut back – but it isn’t clear that she did anything at the time, and it isn’t even clear that she’d yet had any advice on the bid or was aware of the egregious 24/25 budget the Bank’s board had set for itself. The “strong signals” – see this morning’s post – don’t seem to have come until February, months later.

I had an OIA response yesterday from the Reserve Bank. There is more obstructionism, so a letter will be going off to the Ombudsman this morning, but there was also some interesting information released.

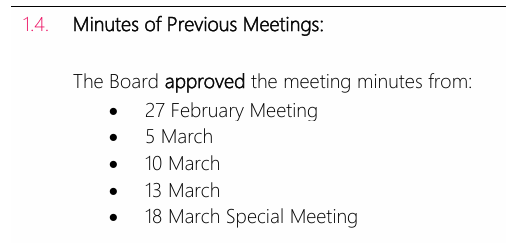

A while ago the Bank’s Board started publishing proactively minutes (carefully crafted ones) of its meetings. It seemed like (and was) a welcome (if limited) initiative, including because it minimised the number of OIA requests they’d need to deal with. But they leave out a lot, and it also only slowly became clear (to me anyway) that they were only releasing minutes of what they described as the regularly scheduled meetings (more or less monthly). The minutes of the February and March Board meetings included these

Of those this year, only the 27 February meeting was a regularly scheduled one (you can read the minutes of that meeting on their website, although almost all the interesting stuff isn’t included (there is nothing about the Funding Agreement or about the Governor – to be clear, not redacted or withheld on OIA grounds, simply not included in the minutes, despite the Public Records Act). Similarly at the full meeting in late March there is no discussion or debrief on the resignation of Orr, or of communications around it, or on approaches to the various OIAs they had already received. Yeah right.

Anyway I asked for the minutes of the other meetings, and received them (in full) yesterday. There are no redactions. The 5/6 March, 10 March and 13 March ones were done by email circular confirming a) Orr’s exit agreement and b) aspects of the revised Funding Agreement proposal. The meeting of the 18th dealt with the appointment of a temporary Governor, where there appears to have been substantive discussion including on expectations of such a person, but a decision that the only person they would seek an expression of interest from would be Hawkesby.

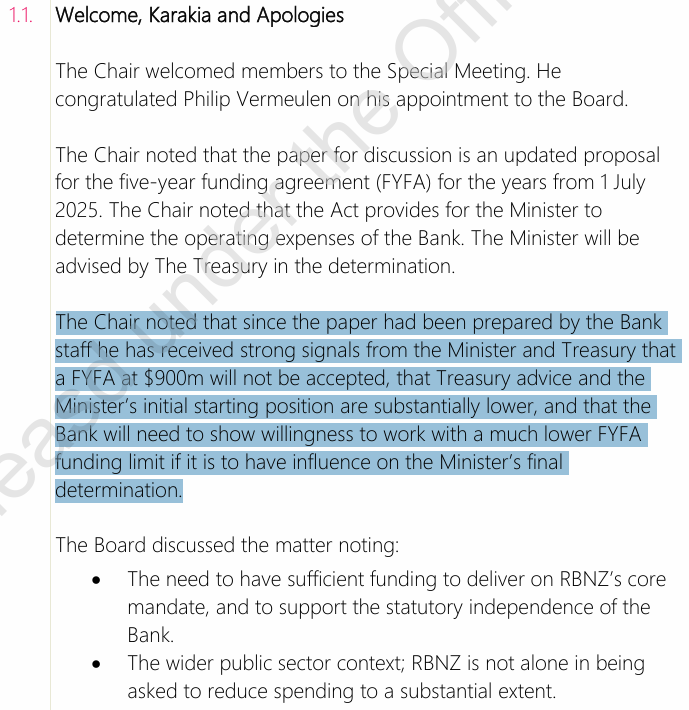

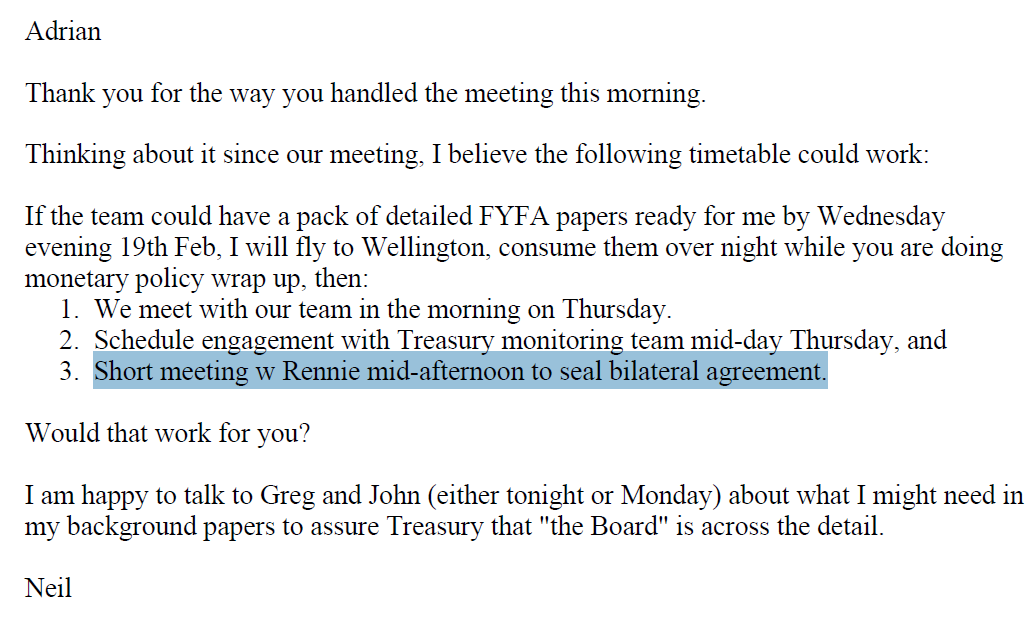

The one that caught my eye though, and the reason for this post, was the minutes of the 14 February special Board meeting. It was a virtual meeting attended by all board members, but with no other senior management present, just a staff notetaker. Here is the substance of the minutes (not forgetting the opening prayers)

Which seems like a rather important, and deliberate, omission from the carefully chosen set of documents the Bank released on 11 June, when they were still trying to divert us from what actually happened.

What they had released included the following.

From an Orr email of 5 Feb (to senior management, cc’ed to Quigley and Finlay). (I hadn’t previously noticed the rather surprising final bracketed observation – a Governor whose MPC was charged with keeping inflation near 2 per cent worries that inflation could average 3-5 per cent per annum over five years)

And from a long email from Orr to the Board on the morning of the special Board meeting (but before it)

And then an email exchange between Orr and Quigley after the board meeting. This is from Quigley

To which Orr responds with a “Yep all good”.

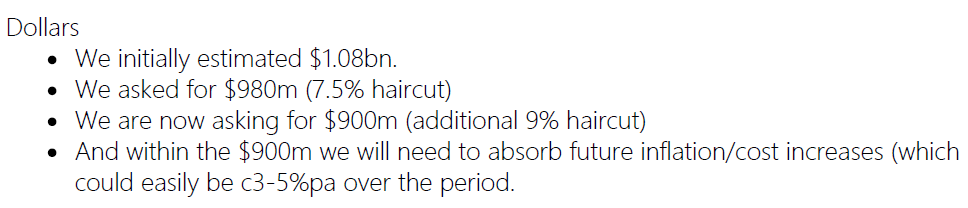

But what they didn’t release was the bit in the middle, which makes the timeline a bit clearer. The Bank had submitted its original Funding Agreement bid back in September, unanimously approved by the Board. This was the egregious one (seeking $981 million over five years), presented as offering savings of 7.5 per cent, but in fact involving materially higher future spending than the Funding Agreement covering the period to 30 June 2025 (variations approved by Grant Robertson had allowed). There is no sign in the minutes of December quarter Board meetings that they’d had any serious blowback (or feedback at all) and the only mention of the Funding Agreement is a discussion of the ‘nature and structure” of the next Funding Agreement when a couple of senior Treasury officials came for a regular visit.

The (still) missing bit is what initially prompted the Bank to propose to revise down its bid. That plan was the paper in front of the Board at the 14 February meeting, in which it appears to have been proposed to lower the bid from $981 million to $900 million. Perhaps there was some initial Treasury pushback, but it cannot have been too strong or clear, because note the chairman’s introductory comments (emphasis added).

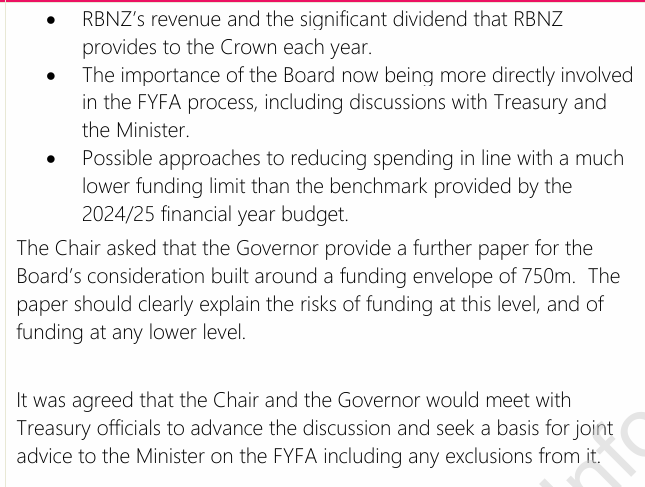

The Chair noted that since the paper had been prepared by the Bank staff he has received strong signals from the Minister and Treasury that a FYFA at $900m will not be accepted, that Treasury advice and the Minister’s initial starting position are substantially lower, and that the Bank will need to show willingness to work with a much lower FYFA funding limit if it is to have influence on the Minister’s final determination.

“Strong signals” and from both the Minister herself and from Treasury, that what was probably intended as a compromise offer would come nowhere near meeting the mark. (Which is to the credit of the Minister and Treasury, but why weren’t those messages being sent back almost as soon as the initial dropped into the Secretary to the Treasury’s inbox five months earlier? And why has none of this previously been disclosed?)

The Board’s response seems, belatedly, quite realistic (noting “RBNZ is not alone in being asked to reduce spending to a substantial extent”) but then you have to wonder how Quigley ever envisaged later that day that they would be able to “seal bilateral agreement” with Rennie at a meeting the following week. Did Orr not disclose to either Quigley or the rest of the board at the meeting on the 14th just how strongly opposed he was to having spending limits pulled back to around the levels in the expiring Funding Agreement? Did it only become clear when Orr lost his cool – and refused to apologise – at that meeting he and Quigley had with mid-level Treasury staffers on the 20th? In the end it wasn’t his call – the Funding Agreement is between the Board and the Minister, and the chief executive is responsible for working within it – but if he hadn’t put his cards on the table, in a calm and rational manner, at a special board meeting on the issue, it is hardly to his credit. And if the goal of the 20 February meeting had really been “joint advice” to the Minister, it is even more reason for Quigley to have regarded Orr’s behaviour as so unacceptable (and utterly counterproductive).

Does any of this greatly matter at this point? Probably not, but it does fill in a few more blanks (and prompt another OIA or two).

UPDATE 5/9 . There must have been quite serious and perhaps robust debate and exploration of issues/options, since the meeting ran for 105 minutes with no staff. Unsurprisingly the minutes don’t record the tenor of the debate but note that that same evening Quigley thanked Orr for the way he’d handled the meeting, so this one can’t have been explosive.

That was the Minister of Finance’s chief press secretary responding on behalf of the Minister to an inquiry from Stuff journalists shortly after Neil Quigley’s ill-starred press conference late on the afternoon of 5 March, the day Adrian Orr’s resignation was announced. But I’ll come back to that.

The main problem for the Minister of Finance, in finally encouraging Neil Quigley to resign late last Friday afternoon, is that throwing him to the wolves (well overdue) left her exposed to the long-running questions about what she knew and when, and what part she had played – actively or passively – in the choice to deliberately mislead New Zealanders about what had gone on around the out-of-the-blue no-notice resignation of one of the most powerful unelected officials in New Zealand, one who had generated enormous controversy in his time and whose frosty relationship with Willis, dating back to Opposition days, was obvious to all.

I’ve been writing on this, and on Monday the Herald’s Jenee Tibshraeny had a powerful piece calling out the Minister and noting that – unlike the public – the Minister got no, or next to no, new information from the Ombudsman-led Reserve Bank release on Thursday. The title of her piece said it all really

but noting, importantly (and emphasis added), that “Both the Reserve Bank board and Willis have engaged in what looks like a cover-up of the circumstances surrounding Adrian Orr’s resignation as Governor in March”. offering chapter and verse. This wasn’t just Quigley’s doing (or that of his board and temporary Governor) but Willis’s too.

The Minister apparently claims to regard these criticisms as unfair to her. She was, we were supposed to believe, a helpless Karori mother, pleading in vain for Quigley to be upfront with the public about the loss of one of her key officials, holder of an office where she – as Minister – is personally responsible for any hiring and firing, the one to whom (as the law requires) Orr’s resignation was addressed. Tibshraeny had another piece yesterday afternoon reporting the Minister’s side of the story. This seems to be the essence of her case for the defence

Setting aside for now the question of how much money the Bank has spent trying to stop the public knowing, all this tells us is what we already knew: that the Minister realised rather sooner than the Bank – and Quigley specifically – that the coverup and active misleading was untenable and could not go on indefinitely, but (a) the resignation was in March, and her earliest such comments were in June, and b) she did nothing meaningful about it (until last Friday) when she could have insisted on transparency from day one, or any time onwards. She had (considerable) leverage. But it is pretty clear that she and her office were fully party to the strategy of deceiving New Zealanders, probably hoping interest would quickly die away.

At this point, it is probably helpful to step back and step through the timeline in February and early March. (My overall, and updated, timeline is here.)

In preparing yesterday for this post I went back and read quite a lot of the initial coverage (5/6 March) and some of the OIAs. It was in a BusinessDesk column, dated 5 March, by their highly-experienced and regarded Pattrick Smellie, that I noticed this

I don’t recall noticing it at the time, and it has had no apparent follow-up. Perhaps it seemed (like a number of other things) unimportant that day, when it appeared that Orr had simply tossed his toys and walked off, and if it was apparent that we weren’t getting the full story, there was no reason to think we were being outrightly lied to. I have no idea whether Smellie’s “it is understood” had substance – but he doesn’t seem like someone who just interviews his typewriter – and put no further reliance on it, but if there is anything to it (or to the suspicion of it), it is probably relevant context. Once again, on RNZ this morning, the Minister was claiming it was important that she had nothing to do with the hiring/firing (or facilitated resignation) of Reserve Bank Governors, even though her role is quite central and explicit in the carefully designed Reserve Bank Act (current version, and all its predecessors since 1989).

The story seems to have unfolded through February. On 5 February Orr, having become frustrated with Treasury, advises his board and senior management that he had told staff to “cease and desist” negotiating funding agreement issues with the Treasury, suggesting that it should now be a matter for the Board and Minister directly. That stance seems not to have lasted because 10 days later (14 Feb) Orr and Quigley were exchanging notes about agreeing a deal with Treasury the following week.

But in the meantime, the Minister had been trying to get meetings that month with Orr on both funding agreement and bank capital issues. One of the Herald’s various OIAs revealed that Orr had been stonewalling, using as an excuse the “sacrosanct” nature of MPC deliberations during mid-February, and suggesting that he couldn’t meet with the Minister then, even on quite separate matters (this of course didn’t stop him having his usual pre-MPS meeting with the Prime Minister and Minister of Finance the day before the MPS itself was released). The meeting between Orr, Quigley (and, for part of it, Hawkesby), the Secretary to the Treasury, and the Minister on the afternoon of Monday 24 February was the earliest date Orr appears to have agreed to. In the interim, Orr had once again lied to the Finance and Expenditure Committee and, that same day (20 Feb) he and Quigley held a Funding Agreement meeting with mid-level Treasury officials where, not only was there no meeting of minds or settlement, but Orr so completely lost his cool, and must have refused later to apologise, that Quigley chose to put in writing an apology to the official concerned. Just an extraordinary situation – a board chair helpless in the face of his chief executive’s misbehaviour, unable even to secure an apology from the chief executive himself.

We do not know whether the Minister was aware of this episode before the meeting on 24 February. There is no paper trail shedding light on that (one way or the other), but it would be surprising if she was not made aware of how combustible Orr had become over these issues (and would the mid-level official handling Funding Agreement negotiations not have told his own boss or Rennie himself what happened, would no one in Treasury have alerted the Treasury secondees in MoF’s office, or indeed her – ex Treasury – political adviser? Would Rennie not have mentioned it to Willis?) Phone calls and oral advice don’t easily get captured in OIA responses, unless it suits responders to do so.

And so we come to the 24 February meeting. The Treasury file note of that meeting – which so enraged Quigley when he learned about it as the OIAs rolled in – is here. I had previously defended Treasury, noting that the record – of a high level meeting on important outstanding issues – seemed both reasonable and moderately expressed. But, as it happens, Tibshraeny revealed that yesterday she had a OIA response from Willis (beyond the original deadline) making it clear that the Minister herself had been very keen to have the meeting properly documented, having staffers followup with Treasury to ensure that it was being done.

This was the meeting where the Governor distanced himself from the Board, bagged Treasury, and then (so it seems reasonable to deduce) stormed out.

One thing I hadn’t previously noticed about this file note is that it records comments from the Minister on the earlier agenda items (bank capital reviews she was seeking, and banking competition issues) but there is no comment from the Minister recorded on the Funding Agreement issues (either before or after Orr walked out). It also records no comments from Treasury. Is that really credible (was it really only Orr and then Quigley who made any comments of substance?) or did it suit the Minister not to have had anything she said on those issues documented (given that we now know she had an active interest in the file note)? I don’t know, but it seems a reasonable question.

Things must have escalated quite quickly from there. It just isn’t conceivable that after that performance by Orr, coming on top of the 20 February episode at Treasury, that there was no contact to reflect on what had gone on between Quigley and either the Minister herself or senior people in her office (the latter perhaps for plausible deniability?) Quigley had pro-actively apologised for Orr’s conduct to a mid level Treasury official, so how much more assiduous was he likely to have been around the Governor’s performance in front of the Minister (especially when so much – future Bank funding – depended on the Minister)? Perhaps it was a one on one after the meeting, perhaps a phone call or two, but surely something?

At very least we know (from the RB’s June release) that within 24 hours or so – and before the board itself had met – various top RB officials independently became aware that exit was possible and established an ad hoc to manage the situation if it escalated. I happened to be listening yesterday to the recording of the Minister’s estimates hearing in June and there she states (three times) that it was on 24 February itself that she was told by the Secretary to the Treasury that “employment discussions” were underway between the Board and the Governor. (Other material suggests she may have had that date wrong and that the advice was on the 27th, but she did repeat the 24th a couple of times, in a hearing for which she will have been extensively prepared.)

And if, and the Minister now claims, she had next to no involvement in what came next, that must have been wholly and solely a tactical choice by her. She was, after all, one of the government’s senior ministers, the person concerned was one of her most senior officials (and by far the most prominent) and, by contrast, the Bank’s board then was almost entirely made of underwhelming Grant Robertson appointees, and Quigley had an established track record of not being a safe pair of hands in front of journalists etc under scrutiny. The Minister may have wanted to establish a “look, no hands [of mine] in this” but not only can she not credibly disclaim responsibility, but if there were concerns the board had – about things not visible to her – surely (as the hirer and firer) she had an obligation (to Orr, if no one else) to check them out. It might just have been an aggrieved, out of their depth, board. But, of course, Willis was aware throughout that that 24 February meeting – in her office – had been the final catalyst for the ouster. (And to be clear, I am not in the slightest critical of the ousting itself – Orr should never have been reappointed, and he appears to have acted recently in ways that handed those with power his own head on a platter.)

The Board and Orr met, and then exchange emails, including notably the Board’s statement of concerns for which they sought a response from Orr. (The Bank’s release last week only explicitly mentions recent issues, although my – generally reliable – inside source told me that it included concerns dating back several years.)

Through these days the Minister chose to up the ante, by providing quite specific comments to the Herald’s Thomas Coughlan for this article on Reserve Bank funding he published on 27 February. At the time, I thought nothing particularly of it, except of course to welcome comments suggesting cuts were likely to be required, because I/we then knew nothing of the backdrop. But the Minister did, and it is probable that she chose to respond to Herald inquiries, and to be as specific as she was, after the 24 February meeting, and knowing that a showdown with Orr was underway, knowing indeed that the Board would be meeting – and Funding Agreements issues would be on the table – on the 27th.

It was on the 27th that the statement of concerns was sent to Orr, and also when he got board approval for him stepping aside, remaining out of the office until the situation was resolved, with Christian Hawkesby to act as Governor. The Minister has since said she was aware that Orr had stepped aside earlier (before 5 March), and we must presume she was advised of it that day (there are – content redacted – texts involving Rennie and MoF that day). Are we really supposed to be believe that a highly political senior minister didn’t ask what was going on, or gave no guidance? If so, it can only have been because she did not want to be fixed with knowledge, but that does not change the fact that the evolving situation was her responsibility (she hires and fires, she is accountable to Parliament, the Board is accountable to her). At any point, she could have intervened and taken control (and probably should have, most especially around exit agreement issues).

By this point it appears that both sides (Orr and the Quigley, the latter for the board) had resorted to “senior counsel” to negotiate terms. By Monday afternoon (3 March) the ad hoc management committee had heard that agreement had been reached – although presumably formally documenting it means it wasn’t signed until 5 March. The plan at this point was for an announcement on either the Friday (7th) or the following Monday (10th), although at the last minute this is brought forward to 1:30pm on 5 March after Orr alerted people to concerns about leaks.

The Minister says, and I guess we must believe her, that she did not see, and has not since seen, either the letter of concerns or the exit agreement. But, again, this does not absolve her of responsibility. They were her board, Orr was her responsibility, and she was the one who was going to have to face parliamentary scrutiny. Did she not seek any assurances about lump sum termination payments, or things that resembled them? Did she not raise any issues about what would be said, by whom, when, let alone what sort of NDAs Quigley and the Board might be signing up to? The paper trail does not tell us, but it seems utterly inconceivable that there was no communication about what the story was going to be or how it would be told. And, again, if the Minister just sat back and let Quigley get on with it, she made herself part of such a strategy, if only by acts by omission. She was not a helpless victim (of Quigley here) but a powerful player making deliberate choices.

The paper trail suggests that the Minister had the planned Reserve Bank press release by late morning on 5 March (sent across by Quigley). This statement, which had been lawyered by both sides, represented the first attempt to spin the story. Recall that the Minister was not an innocent bystander here – it was her to whom Orr was actually resigning. The press release was full of “good job, well done, time to step aside” fluff, and there is no sign that either the Minister or anyone in her office raised any objections (to the text, or to the Bank-attached note which indicated that there was no plans to say anything further “if” there were questions). Willis knew that the statement was intentionally misleading – she has since told us she knew about the “employment discussions”, she’d been in the 24 Feb meeting, she knew Orr had been gone for a week, and yet she raised no objections. She doesn’t even seem to have asked what commitments had been made, by either side, under an NDA. But those were her choices; she went along.