A few weeks ago, just before I went away for 10 days holiday, the latest in the saga of the Reserve Bank MPC, and the blackball on external experts when the first MPC appointments were made, appeared in the Herald.

You’ll recall that it was widely understood that there had been such a blackball, put in place by the Bank’s Board and agreed by the Minister of Finance. It was widely understood by pretty much everyone – the Minister, Treasury and Reserve Bank staff, former senior Reserve Bank figures, (quite probably even MPC members themselves), a former senior adviser to the Minister, and Bank spokespeople – and was widely reported, and not denied, once the news got out formally with an OIA release from the Minister to me back in 2019, which had included a procedural papers from Treasury’s appointments and governance manager, handling the formal side of the appointment process, which described the blackball. Lines in that paper – that they were being particularly cautious but that a more relaxed approach might be adopted in future appointments – had been echoed in later comments by people speaking for the Bank. All this had come on top of the person, with macro-specific expertise, who back in 2018 had enquired about the MPC roles and been told by the Board’s recruitment firm that there was a blackball on research expertise, and who had then gone to the Board chair (Neil Quigley) himself to check, and had been told face to face that indeed there was such a ban. I wrote about it all here.

The reason I (and others) were still writing about it was that a few months ago, when forthcoming MPC vacancies were first advertised, it became apparent that the blackball had been lifted, and in this round people with research expertise and possible future research activity in areas of macroeconomics and monetary policy would not be barred from consideration by the Bank’s Board. That was, and is, good news (cynics might suggest that the Board is simply likely to fall back on adopting a slightly different test, barring anyone who might prove awkward for the Governor, but leave that issue for later). But then Treasury, backed by the Minister, issued a statement to the Herald claiming there had never been a blackball, it had all been a sad misunderstanding, and tossed one of their own former mid-level staffers under a bus by suggesting that when she’d written that memo to the Minister, she’d simply got the wrong end of the stick. And, so OIAs revealed, they made this comment – without any serious scrutiny or testing (including asking the person concerned) – because Neil Quigley had, on two occasions, this year told them so. The Treasury official had simply got things wrong, and all that had happened is that some academic who was interviewed for the role had refused to commit to not commenting publicly if appointed, and so that person had not been taken any further. Or so Quigley said.

In that post last month I outlined why this simply wasn’t a credible story, and that either Quigley was simply and deliberately misrepresenting things, or – years on – was suffering from a faulty memory, and had conflated two quite different things. Either way, his claim now that there had never been a blackball simply did not stack up, and Treasury should not have been uncritically making statements based on it, perhaps particularly when it involved throwing one of their own former managers (and managers at Treasury aren’t junior people) under a bus. Treasury should now be rather annoyed at Quigley, for putting them in a situation where taking him at his word – a senior government appointee – had left them with egg on their face (I have an OIA in on how, if at all, they have dealt with this subsequently).

Anyway, that is all prelude to the Herald’s story on 12 September. In my posts I had noted that among the many reasons for scepticism about the Quigley story was former Board member Chris Eichbaum. I knew he used to read my stuff (he told me so one day when I ran into him) and had not been backward in coming forward, commenting in replies on Twitter when he thought I’d got it wrong or been unfair about the Board and its role/performance. Not once had he objected to my characterisations of the existence of a blackball (this back before he left Twitter).

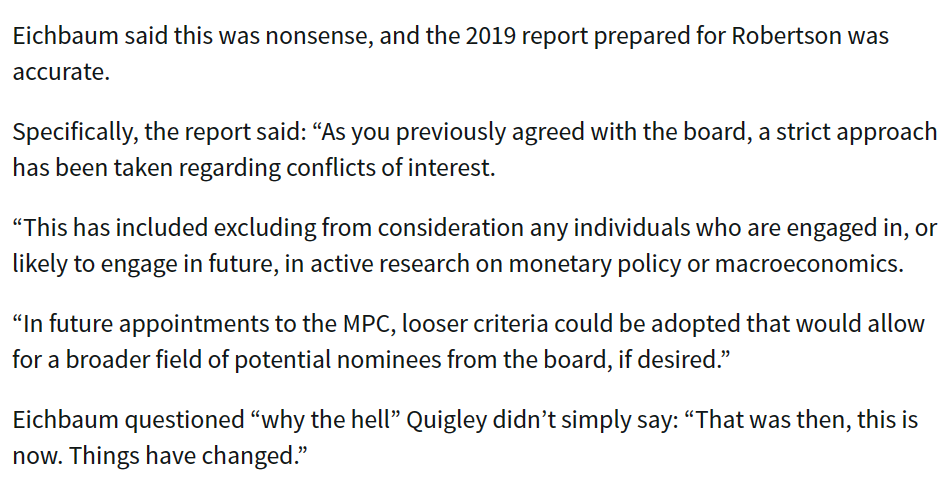

The Herald’s Jenee Tibshraeny got in touch with Eichbaum to see if he had anything to say now. He did. In fact, her story opens with an Eichbaum expletive.

Asked specifically about the 2023 Treasury denial, which had channelled Quigley, this was Eichbaum’s response

Well indeed.

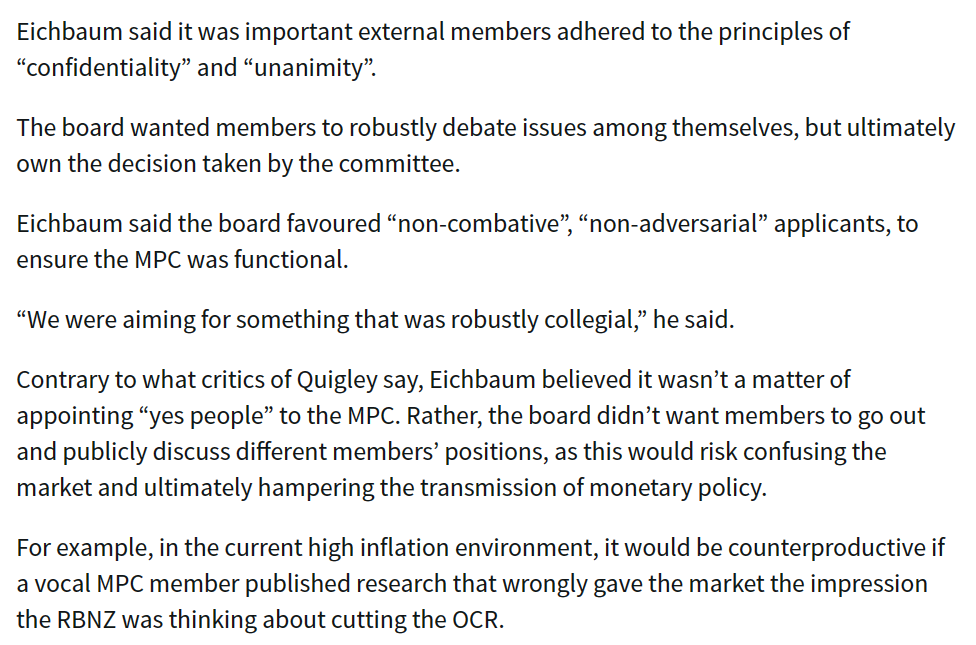

He’d added

noting that today’s Board might not be as “risk-averse” as the old Board was.

Here it is worth noting that Eichbaum was not just any Board member, but was one of the small interview panel (him, Orr, and Quigley) for these MPC roles back then.

I also understand that Eichbaum regards the Herald article as having fairly and accurately represented his views/comments.

That might have seemed fairly open and shut. There are suggestions there is no love lost between Eichbaum and Quigley (one of the left, one of the right, and Quigley had been a former senior manager at Victoria University where Eichbaum taught – and comments on Quigley from people at Vic then often seem to have quite an edge to them), but it all seemed pretty clear. There was an expertise blackball, as everyone else had believed until Quigley belatedly sought to deny it.

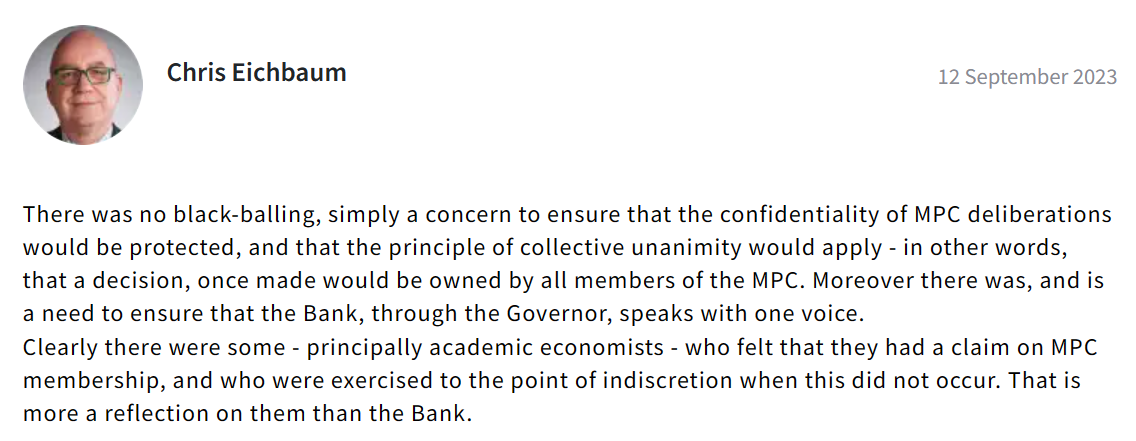

But there were some more Eichbaum comments in the post, on a slightly different strand of what seems to have gone in 2018/19.

Which seems to give support to what outsiders have supposed all along (anyone awkward for management, especially the Governor, wasn’t going to be welcome), but is also consistent with that “consensus collegial” model of MPC decisionmaking which the Minister went along with (but which is not practiced in the best practice MPCs globally). The Bank had actually wanted to ban external MPC members from giving speeches or interviews at all, but the Minister didn’t go along with that…..and the practical solution seems to have been to appoint people who had neither the interest, inclination or ability to give speeches or serious interviews (despite being responsible, supposedly actually accountable, statutory appointees and decisionmakers).

But it also points to what Quigley may have been remembering when he falsely claimed there had never been a general blackball. There clearly was – as Eichbaum says – but it looks as though they may have also turned down one person who got as far as an interview because he/she wanted to be freer to speak. That wasn’t a wider general ban, but specific to an individual and the limitations of the model the Bank wanted around MPC. There was still a wider ban on people with actual/future macro research expertise etc.

But focus on that final para of Eichbaum. In open and transparent central banks – Bank of England, Fed, Riksbank – individual MPC members often give speeches or interviews, sometimes based on their own research, often drawing on their own analysis, outlining their thinking on issues, risks, and outlooks, including policy outlooks. It is quite normal, not at all problematic, and quite consistent with the inevitable huge uncertainty around any view on the outlook and likely required future stance of monetary policy. But we don’t want any of that sort of openness in the Robertson/Orr/Quigley Reserve Bank……and they’ve delivered. We’ve heard nothing of substance – research or not – from any of them.

And that might have been that, but on the same morning the Herald article Newsroom published a column on the MPC blackball issue by Eric Crampton, who has had many of the same views as me on the issue.

And one Chris Eichbaum left a comment.

This is the same person quoted in the Herald saying Treasury’s description of the blackball had been quite right, and it was only a shame Quigley hadn’t just said so and said they’d now moved on.

But this comment, if it is to be interpreted consistently with this comments to the Herald, must also be about that desire to ensure that no external MPC members were speaking in public at all, at least never articulating any views of their own. That is a different issues than the macro research expertise blackball – not much more defensible in substance, but at least with some precedents (notably in the RBA model that the Bank wanted to model its committee on – more ornamental than substantive).

What of that second paragraph? I am not aware of anyone who thought they had a “claim on MPC membership” – and Eichbaum seems to have no evidence for his claim – but a really large number of people, economists and not, many of whom would not have wanted to touch an Orr RB MPC with a barge pole, were nonetheless seriously disconcerted that our MPC was to be the only one in the world where formal expertise in the subject was a disqualifying factor. As it clearly was, as Eichbaum acknowledged to the Herald. And recall that the story did not break in the first place because some aggrieved academic went to the press but because a citizen used the OIA and the Minister of Finance complied with the law and released the relevant material.

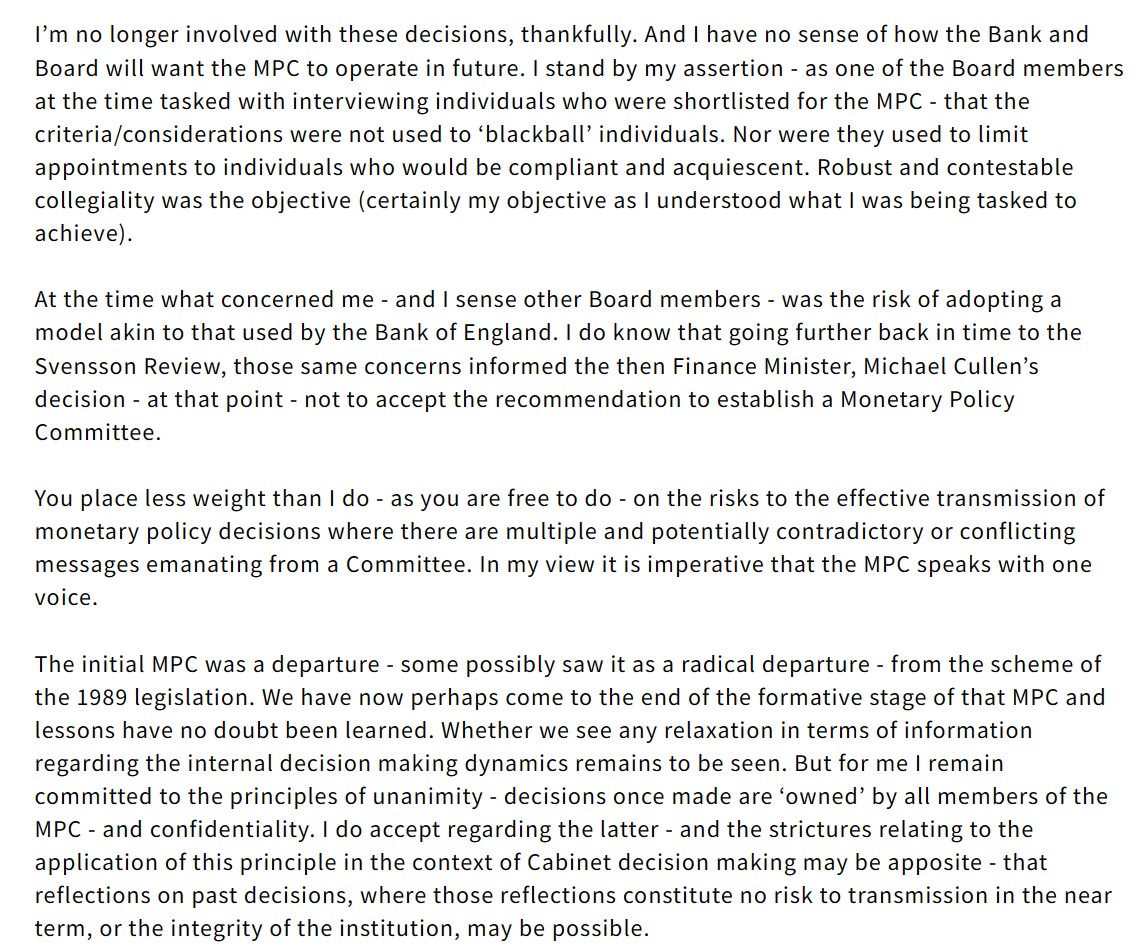

In the Newsroom comments column Eric Crampton responded to Eichbaum. Here were some relevant bits of Eichbaum’s reply.

It is interesting in its way, but what it seems to confirm is the conflation of two quite separate events by Quigley. The block put on an individual at the interview stage seems to have been specific to one person’s desire to be free to communicate publically while in office.

But that is very different from the message conveyed by the Board’s recruitment firm – confirmed face to face by Quigley – that no one with active or future research interests in and around monetary policy would be considered (would even be longlisted), let alone interviewed or appointed.

There is no real doubt that happened. The person who recounted their experience to me is someone whose integrity and honesty I have never had any reason to doubt. The fact of that blackball also squares with what the record of a Board meeting discussion in 2018 suggested (copy in earlier posts).

But I realised that when the Bank had responded to my OIA request in 2019 re MPC appointments it had left out a lot of material that as clearly covered by the wording of my request. So I lodged a few weeks ago a further request – noting the prior omission – asking for all dealings with the recruitment firm around that first round of appointments. The Bank is slowwalking that request too – citing the need for “consultations”, about events 4-5 years ago – but before long we should have those answers too.

(Interestingly, I had another OIA back from the Minister of Finance last week re any discussions/advice this year re the blackball and its removal. It appears he was not involved at all (which I have no particular problem with, although one might perhaps have hoped for a more proactive approach).

Some of you will be wondering why any of this matters. To me it is a matter of two things. First, a really bad decision was made in 2018/19, which got the MPC off to a very poor start. But at least as importantly, because honesty and integity matters, or should do, in public life, and particularly in and around powerful independent agencies. We’ve simply not seen that from Neil Quigley (and here I am clear that his responsibility is personal: the Governor and management have not weighed in to support his, clearly wrong, story).

But it does bring us to today. In the papers I got from the Bank a month or so back there was a lot of material about the process that is underway to fill the two MPC external vacancies next year. It is a quite unsatisfactory situation. The Board – appointed entirely by the current Minister of Finance, few of whom have any relevat expertise – have not only advertised to fill the MPC vacancies, have had their recruitment firm tell at least one qualified person that they simply won’t be considered, but were on schedule to have conducted final interviews last month, positioned to deliver recommendations to the Minister of Finance once a new government is formed.

Perhaps that would be no great problem if a Labour-led government were to be returned – his friends and appointees on the Board will be delivering names consistent with the last few years’ model of the Reserve Bank. But it is highly unsatisfactory if there is a new government, especially in light of the concerns both National and ACT have expressed about the Governor and the Bank’s stewardship. If Nicola Willis is appointed Minister of Finance, she should start the process from scratch, making clear to the Board the sort of people, and sort of model (hopefully both more expert and more open) that she wants, opening the process to people who might be more interested in serving under such a model, even if Orr is still in place. The first vacancy is not until 1 April next year. It is very difficult to get rid of the Governor himself – and thus Willis has made a virtue of necessity in ruling it out – but if a new government is at all serious about change it has to start with a keen focus on all vacancies, MPC and Board, as they arise. Whether they are really serious – I’m sceptical – I guess only time will tell.

While there’s no one size fit all for the design of monetary policy committees in operationally independent central banks: whether its composition is internal only or a mixture of internal/ & external members; or whether the decision is reached by a voting or a consensus process ( and there are variants to all 4 of those features in both Advanced and Developing economies), the central issue is about whether the design leads to: (a) better decision making, (b) transparency and (c) accountability. Ideally (b) & (c) improves (a), but that is probably open to much debate. Whether there is any impact on the efficacy of monetary policy transmission by adopting one design over the other again is a topic that is debatable. Personally, I doubt whether the ‘voting’ style created any headwinds to monetary policy transmission whether that be the BoE, the Fed, or to a lesser extent the Riksbank, Bank of Iceland or the Bank of Thailand.

LikeLike

I doubt the precise governance model makes any predictable or systematic difference to mon pol outcomes,so my focus is more on transparency and accountability as important in their own right.

LikeLike

Well, when you bring in externals on the rationale of avoiding organisational ‘Group Think’ it’s reasonable to expect transparency around decisions (and the thinking behind those), especially when there is crossover into the fiscal arena, as QE has done – hence I think the BoE is a better operating model from a governance perspective, even if the outcomes haven’t been ideal.

LikeLike

Oh, indeed.

LikeLike

[…] that one of the other Board members from 2018/19, actively involved in the selection proceess, went on record to the Herald to (a) disagree with Quigley, b) wonder why Quigley didn’t just act to clarify things, and also, […]

LikeLike