I didn’t have too much problem with either the Reserve Bank Governor’s speech a couple of weeks ago on a framework for how monetary policy might deal with the oil shock, or with this week’s OCR review release from the Monetary Policy Committee. It was really all very orthodox stuff, much as any of the previous Reserve Bank Governors over the inflation targeting era might have said. Almost always, you will let the first round (direct and indirect) price increases through – as major relative price changes, and as happening too soon for monetary policy to do anything much about anyway – and then keep a very close eye on what happens beyond that to the generalised medium-term inflation outlook (where the pressures can be conflicting – weaker economy on the one hand, and potentially higher “true” inflation expectations on the other). And, of course, when the oil shock hits, no one really knows how long the disruption and associated price effects will last, and that matters.

A comment that was passed to me yesterday had expressed concern that the MPC might be going soft on inflation risks, they having mentioned the potential near-term growth implications of the shock (which could yet be savage, given how low the price elasticity of demand for diesel is). That prompted me to go and dig out the Monetary Policy Statement the Bank issued in the wake of the first oil shock of the inflation targeting era, that prompted by Iraq’s invasion and occupation of Kuwait on 2 August 1990.

That invasion caught most of the world flat-footed. It complicated life for us too. We’d just issued a small tightening statement on 1 August, which hadn’t made us at all popular with a government that was facing a crushing defeat in an election now only a couple of months away. We tightened again – different system then from today’s OCR – on 3 August, and when mortgage rates rose that day the (normally sensible) Minister of Finance was reduced to calling the banks “mean” and claiming they were out to get the government. We were also just a couple of weeks out from the scheduled release of our second Monetary Policy Statement (editorial and production processes were a lot more protracted then than now, and the documents weren’t forecast focused), for which the team I managed was responsible. We pretty quickly realised that we needed to postpone the MPS by a couple of weeks and I spent a harried few days rushing out a substantial redraft, centred now on the oil shock policy issues.

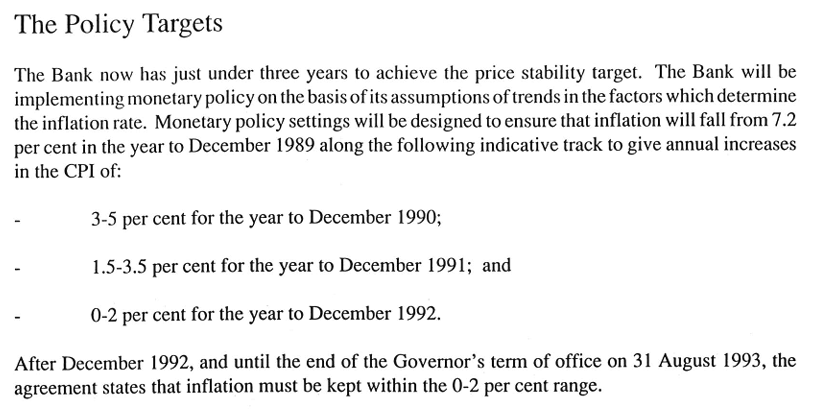

Oil price shocks, of course, had not exactly been unknown to this point. In fact, the two dramatic ones to that point (1973 and 1979) were only about as far back in history then as 2007/08 and 2022 shocks are now. And in devising the inflation targeting framework, and the formal Policy Targets Agreements between the Governor and Minister, we’d been careful to think hard about how to handle supply shocks of that sort. And we had discussed specifically an oil shock scenario in our first Monetary Policy Statement in April 1990.

Folklore sometimes has it that the Brash Reserve Bank was full of utter zealots and nothing, but nothing, would ever allow us to deviate from a narrow path to price stability, and certainly not any considerations of output or employment. It simply was not so, whether in conception, or in practice. There were numerous examples during the early years, but this is a particularly clean one.

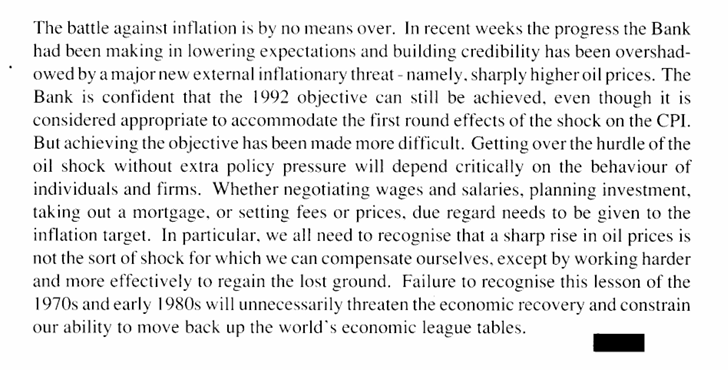

Here is what we had to say in the Monetary Policy Statement finally released at the start of September.

Whereupon the extract (above) from April was repeated, before the discussion continued

Reading that final sentence, there is a certain similarity to much current commentary…..

And we ended the entire document this way

Our monetary policy approach then was right, and flexible, and not at all reluctant (my diary, for example, records a senior-level meeting on 7 August where we agreed, without apparently any significant dissent, that even the 1991 indicative target range for inflation on the path to price stability (announced here in the April MPS) should probably be increased (there was later a formal adjustment, in agreement with the Minister)).

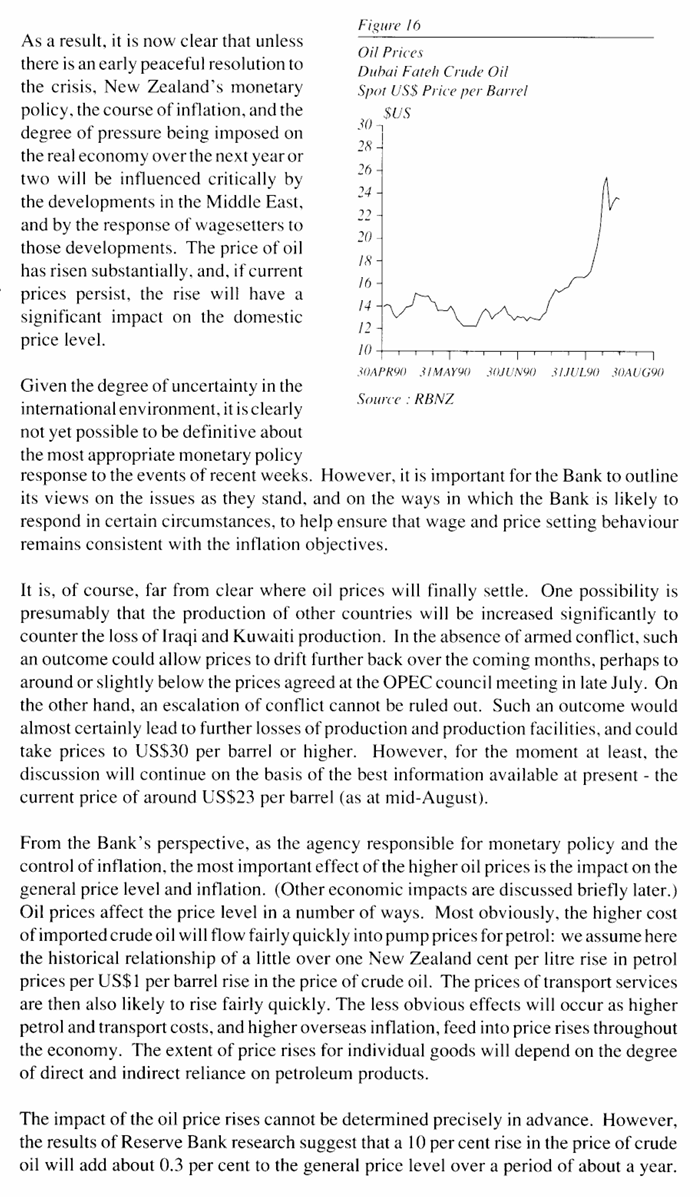

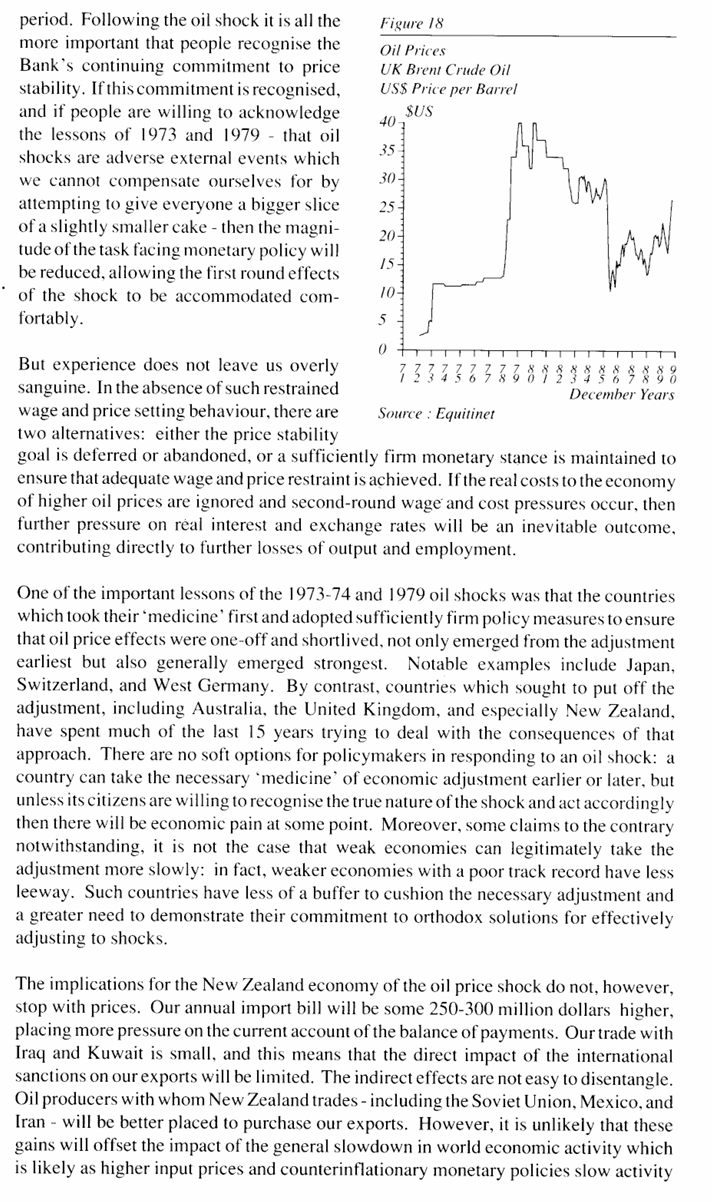

Rereading that 36 year old text, one thing I was struck by was that our experience then had been with oil price shocks that proved semi-permanent (see Figure 18 above for both the 1973 and 1979 shocks). Faced with permanent oil shocks it really was critical to get across messages like the one above, that if the national cake was now smaller we couldn’t try to fix that by all trying to cut ourselves a larger slice. As it happened, permanent shocks haven’t been a feature since then; whether in 1990/91, in 2008 (more a demand-driven surge, but still extreme for countries like us), or in 2022. The current view is that the Iran-related disruption, severe as it is (and likely to worsen, as it affects end users at least) will also be temporary, and that presumption is a reasonable one on which central banks are likely to operate for the time being.

(Acute readers may have noticed the final sentence of that September 1990 document – the bit about threatening “our ability to move back up the world’s economic league tables”. We were then optimistic. Unfortunately, in the decades since, we’ve managed nothing better than slowing our rate of relative decline. It is difficult to think of any country we were poorer than in 1990 that we are richer than now. But whatever the – contested – reasons for the failure, it wasn’t anything much to do with the Reserve Bank or its handling of monetary policy over the decades, whether faced with demand shocks or more supply shocks like today’s oil one.)

UPDATE: Prompted by my son, I had a look at the claim in the previous paragraph. Using the IMF per capita GDP data, expressed in PPP terms, it seems we have overtaken two countries since 1990 (Oman and Japan). Since per capita numbers are influenced by changing demographics, I also had a look at the OECD real GDP per hour worked data, also expressed in PPP terms. We have also overtaken Japan on that metric (Oman is not part of the OECD). Note that relative to Japan, they have gone from being well ahead of us in 1990, to just slightly behind now (essentially, given measurement issues, much the same). Overall, using the real GDP per capita data from the IMF, New Zealand has dropped about 10 places down the international league table since 1990.

There have been numerous OIA requests around events leading up to and surrounding the (pretty clearly) coerced exit of Adrian Orr on 5 March. The Reserve Bank in particular continues to keep on with a fair amount of delaying and stonewalling, clearly resistant to the idea that the public has any real right to know what happened, in a case involving one of the most powerful officials in New Zealand, with a track record of poor personal behaviour and very costly policy choices. Judging from a couple of their recent responses to me and one I noticed to someone else via fyi.org they seem to be working towards a date around 18 September (at least three requests are extended to that date), perhaps around the expected timing of any final Ombudsman determination on the various appeals already in train. By then it will be well over six months since Orr resigned, and that it is with the Ombudsman apparently taking this matter seriously. It is pretty bad, in both appearances and substance, and had the Bank and the Minister of Finance been at all serious about transparency and accountability we could have had a full reckoning within a couple of weeks of Orr’s departure, and then moved on towards rebuilding the institution and with it its credibility and authority (eg that “social licence” Orr used to like to bang on about).

And yet, various responses do come in. While I was away last week there were responses – each with some information – from the Reserve Bank itself, from The Treasury, and from the Minister of Finance. In their different ways, whether by acts of commission or omission, they do not show any of those three parties in a good light.

You’ll recall that it was the Reserve Bank’s egregious Funding Agreement bid, and the resistance to it by the Minister of Finance and Treasury, that finally sent Orr over the top, resulting in behavioural breakdowns (described in the Herald the other day, with apparent extreme understatement, as “including at least one indecorous outburst”) that led to his coerced resignation.

I’ve been trying for months to get to the bottom of this; both how they ever made such an egregious bid in the first place, and how Treasury and the Minister did so little for so long, such that this only came to a head in late February (the bid having been submitted in September).

We know:

that in her letter of expectation to the Bank’s Board in April 2024 the Minister set out her expectations about future spending. Against the backdrop of what was happening to other agencies most people would read this as suggesting that the Bank could expect less authorised spending under the new Funding Agreement than under the old one.

The Reserve Bank nonetheless went ahead and set its own 24/25 budget (which it could, in law, do) 23 per cent above the amount of operating spending authorised for that year by Grant Robertson in a variation to the previous Funding Agreement made just prior to the 2023 election.

The Reserve Bank did not tell the Minister of Finance this, by the simple device that when – as the law requires – they gave her the opportunity to comment on their 24/25 draft Statement of Performance Expectations, they simply left out the planned budget amount. (It was filled in in the final published version but…..who reads such things).

The Treasury seems not to have raised any concern about this egregious 24/25 budget – it isn’t even clear they asked about it or were aware of it at any time during 2024 – and certainly did not alert the Minister to what had happened.

The Reserve Bank (and note that this was the Board, unanimously, and not just the Governor) in September 2024 lodged a bid for the 2025-30 Funding Agreement that was quite explicitly set on the basis of involving a level of future operating spending 7.5 per cent below their own (grossly inflated) 24/25 budget.

Numbers consistent with this bid found their way into the HYEFU expense tables in December last year (Treasury telling me that they simply took the numbers the Bank gave them).

Treasury appears not to have engaged seriously with the Funding Agreement bid until February this year.

It was pretty much beyond comprehension all round. How could the Reserve Bank Board have the gall to have a) set such an initial budget inconsistent with the recently updated funding agreement and b) then used that as the base for a bid for such a higher level of resources (incidentally going on to commit to large and expensive new office space in Auckland without any certainty as to their future approved spending)? How could the Minister of Finance, who had very evidently been no fan of Orr, have let all this happen (where was her suspicion/curiosity, where was that of her advisers)? And how could The Treasury, supposedly the guardians of the public purse and specifically charged with monitoring the Bank (and Board minutes show Treasury DCEs turning up for chats at Board meetings), have been so oblivious to what was going on (would this have been an acceptable standard in any other government department monitoring its Crown entities)?

The Bank has been quite obstructive in releasing the relevant material (Treasury, more cooperative, reveals that it really had none) and are still refusing to release the final Funding Agreement bid that went to the Bank’s Board (I really only want it to check whether the Board exercised any discipline on management excess but the minutes suggest not). However, in consultation with Treasury, they have now released a letter of expectation sent by the Minister of Finance to the Board chair headed “Expectations for the 2025-30 Funding Agreement proposal and review process”.

The version they released has no date on it (I asked yesterday, but perhaps they’ll take another 20 working days to reply), but it must have been after the April 2024 general letter of expectation (see above), although perhaps not much after it.

[UPDATE 8/9: The Bank has confirmed to me today that the Board chair received the funding agreement letter of expectation from the Minister of Finance on 3 April 2024.]

If you were dealing with honourable people, it would be a perfectly reasonable letter.

The Minister outlines the general fiscal context:

In pretty much any core government agency the budget for 24/25 would have been the appropriations made by Parliament for that department for that year. The Reserve Bank was different, because it had a five year Funding Agreement, in which approved operational spending for each individual year was specified. The Minister (and Treasury, as drafters of the letter) should still have been safe because you’d surely be able to count on the Bank having set a 24/25 operating expenses budget very much in line with the limits in that previous Funding Agreement for 24/25?

With decent people, but not it appears with the Reserve Bank Board (Quigley, Orr, and the rest). They simply set themselves a budget for 24/25 that bore no relationship at all to what they’d previously been allowed to spend for that year, and then took the Minister at her (literal) word and put in a bid 7.5% lower than that grossly inflated budget. And thus, per the covering Board paper dated 12 August 2024, Bank management (in this case, two of the – very many – deputy chief executives, Greg Smith and Simone Robbers) offer this assurance to the Board

And on the letter of the Minister’s request, it was indeed so. But it was fundamentally dishonest and any half-alert board members (including, but not limited to, Quigley and Orr) must have known that. It is almost inexcusable that any of the Board members involved – both in setting the 24/25 budget itself, and playing fast and loose with the clear intent of the Minister’s letter, in turn leading to the massive dislocation to the organisation and its staff this year – are still in office (driving the determination of the nominee to be the next Governor).

These are the guilty men and women who are still in office, drawing (incidentally) the highest board fees for any non-commercial government agency in New Zealand:

Nei Quigley (who, for reasons apparent to no one else, the Minister continues to express confidence in)

Rodger Finlay, the deputy chair

Jeremy Banks

Susan Paterson

Byron Pepper

Meanwhile, Treasury seems to have been asleep at the wheel, and doing a particularly poor job in pro-active advice to the Minister, in drafting things in a way that ethically challenged people could not drive a cart and horses through, and in undertaking constant and reasonable challenge and scrutiny of the Bank. And the Minister and her team hardly emerge looking good, when they been clear all along that they’d had doubts about Orr.

Where, you might also wonder, were the Opposition and FEC? But the primary responsibility rested with the Board, the Treasury, and the Minister. And if we can’t count on more honest and straightforward behaviour from those charged with monetary stability and the regulation of our financial system, or more effective scrutiny from those responsible for safeguarding the public purse, things are even further gone than this pessimist had come to fear. Mistakes will happen, but then the question is whether those in a position actually take them seriously and do something. There is no sign Nicola Willis has done that (after all, all those board members are still in office, and although their bid was cut back there were no consequences for them for the havoc they wreaked or the ethically-challenged try-on).

The second part of this post skips forward some months. But before we get to that take note of what the Bank and Quigley had done in the earlier section, hardly (one would have thought) conducive to good and trustworthy relationships going forward between the Bank and Treasury, if Treasury now realises they have to dot every i and cross every t, and check every single document that the Bank is not attempting to pull a fast one).

You might remember that a month or so ago I reported what an apparently well-informed insider had told me about what really happened around the Orr departure. Pretty much all of that story has checked out as things unfolded. One element of the story was that Neil Quigley had gone ballistic when he learned that Treasury had kept a fairly full file note of a critical meeting held on 24 February between the Minister of Finance, the Reserve Bank, and the Treasury. So I lodged an OIA request with The Treasury, and this was the response

Personally, having taken many file notes of meetings with Ministers of Finance and Treasury earlier in my career, neither the fact of the file note nor its contents seemed particularly surprising or inappropriate. Major issues (not just the funding agreement but bank regulatory ones) were being discussed, the language is not inflammatory – although the Orr walkout (itself described in muted terms) certainly was.

The fault here seems (and not surprisingly) all with Quigley. As ever with him, there is never a sense of why the Official Information Act exists, or whose interests it is supposed to serve. Instead, we get implied threats of (a) “this will require the full force of RBNZ legal advice to be brought to bear on it”, and b) the suggestion that release would “immediately destroy the goodwill between Treasury and the Bank that I have tried to create over the past few years”. You might wonder how Quigley is feeling now that the full file note has been released, but even set that to one side……goodwill????? This was the same Board chair whose chief executive had behaved so egregiously in a meeting with Treasury that Quigley had felt compelled to provide a written apology, and whose Governor (in that 24 Feb meeting) had (in muted Treasury language) “expressed frustration at the relationship between the RBNZ and the Treasury”. And this was the Board chair who had pulled the wool over Treasury’s eyes by agreeing to a budget for 24/25 quite out of step either (and more importantly) with his own Funding Agreement, or with the spirit of government fiscal policy last year, and then used that abuse as the base for a bid for a big increase in authorised spending for the coming years.

Quigley then puts one of the Bank’s attack dogs, their General Counsel, onto the issue and we have his crucial email as well

So, the Bank’s General Counsel tries to threaten Treasury that the Bank would not in future be willing to hold meetings with Treasury and the Minister of Finance on its future funding? Yeah right, but it is an attempt to intimidate Treasury.

And then, of course, there is that second paragraph. Which goes to the whole point, that the Reserve Bank’s Board appears to have engaged in attempts to make end runs around any serious public scrutiny, including via the OIA, by doing sweet-heart deals with Orr, the terms of which they also refuse to disclose. Fortunately, sweetheart deals done by Quigley et al don’t bind The Treasury, without whom it seems we would have no idea what went on at that critical meeting, when things were so bad that within 24 hours the exit process was getting underway.

Quigley repeatedly displays no regard for the public interest, and any relationship to the truth or straightforwardness on Reserve Bank matters seems entirely incidental (ie whether or not it serves his ends of the moment – see the repeated active misleading of the public, both on 5 March and since).

And, just briefly, one final OIA, this time from Willis herself.

My informant had told me that on the afternoon of 5 March there had been heavy pressure from the Minister’s office for the board chair (Quigley) to do a press conference on the resignation. One of the Bank’s earlier OIAs had also mentioned such approaches. The Minister’s response confirms that there were two conversations that afternoon involving her Senior Press Secretary and the Bank’s communications head to that end, and it also releases the draft press release and Bank comms plan that Neil Quigley had provided to the Minister’s office late on the morning of 5 March which included this: “Recommended media response plan for if [ “if”???? Really?] we get questions: No further comment”. The ill-fated press conference, at which Quigley did so poorly and actively misled the public, was clearly Willis’s initiative.

But that was not my main interest. I also asked for copies of “any material relating to exit conditions for Orr (process or substance)”. The Minister’s response was “No information about the Reserve Bank Governor’s exit conditions is held”. Which really is inexcusable. As a reminder, the Minister (and Cabinet) appoints the Governor, the Minister (and Cabinet) are the only ones who can dismiss the Governor, and the Governor’s resignation has to submitted to her specifically. The Minister is also responsible for the Board, and appoints – and can dismiss at will – the Board chair, and is the only person in the entire mix with any degree of direct public accountability. And yet we are expected to believe she is so incurious as not to enquire at all as to what sort of cover-up arrangements Quigley (and the “senior counsel” both sides engaged) was cooking up with Orr, as the basis for his departure, or even at what cost. And when a key precipitating event was a meeting she was part of?

I’m not sure I really believe it – not “holding material” is likely to be different from no phone calls were made, directly or indirectly, (and there is set of texts involving Iain Rennie on this topic that are still being withheld in full by Willis) – but if it is true it reflects very poorly on her as a steward of the public interest.

(And that is even granting that the wider public interest was almost certainly served by Orr’s departure, a couple of years after he would already have gone had the previous government not, inexplicably, reappointed him.)

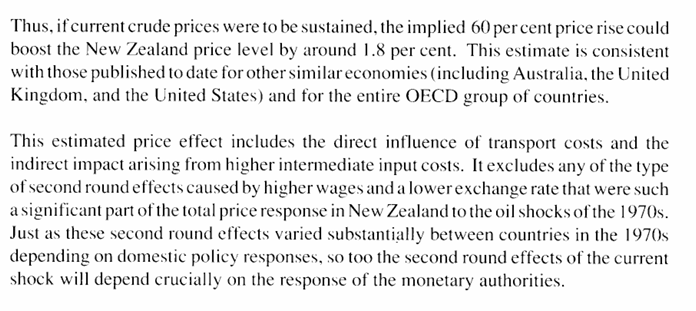

That is the headline in a story in The Post this morning. After inquiries from Post journalists a Reserve Bank spokesperson said that final decisions on organisational change, advised to staff last week, would mean a net loss of 142 jobs (35 of which were currently vacant; presumably the Bank has had some sort of hiring freeze in place for some months now).

The last public number we had for Reserve Bank staff numbers was in the Minister’s Funding Agreement Cabinet committee paper: 660 FTEs as at 31 January. Presumably a) there were some vacancies even then, and b) the number of jobs was greater than the number of FTEs, but even if there were 700 filled or unfilled jobs in January the recent decisions would still be a cut in excess of 20 per cent. That is brutal in any organisation, especially when its statutory roles and functions haven’t changed a jot. It is hard to imagine morale is particularly high in the Bank at present, and we might even sympathise with the more junior of the staff losing their jobs, especially those hired in the last year or two, really on what amounts to false pretences. Even those (probably a minority) doing useless jobs far beyond the scope of the Bank’s actual statutory functions.

You don’t really expect junior hires to a core government agency to have to do due diligence on whether that agency was running spending levels – and hiring plans – far in excess of what had been approved for them by the Minister of Finance. But that is what had happened: Board approved spending last year was 23 per cent higher than what the previous Minister of Finance had approved for 24/25 when he increased the Funding Agreement amounts just before the last election. Treasury didn’t seem to have noticed, or done anything to call it out, so one can only sympathise with new hires now being thrown back onto the job market.

And you can see how last year’s excess created today’s problems. The number of FTEs increased from 601 to 660 between 30 June last year and 31 January this year. Had they not gone on that last hiring binge, adjustment now would be much less painful all round. This table, showing FTE numbers, is from the 2023/24 Annual Report published last September.

It is a reminder of how rapidly Orr and Quigley had been ramping up staff numbers, with no substantial change in functions. Cut FTEs by 20 per cent from that 31 January level (660) and it would take the Bank down to 528 FTEs, at which point it would still be larger than it had been on 30 June 2023, the final balance date under the previous Labour government (under whose term almost all agencies had seen rapid growth in staff numbers). It makes the point that the cuts the current Minister of Finance approved have not been deep at all relative to what was going on (spending allowances, staffing) on Labour’s watch. (I reckon the Bank’s core functions could probably be done professionally with 350 staff, but save that debate for another day.)

One way of seeing this is to look at the Bank’s total operating expenses. In the final budget approved during Labour’s term, the Bank budgeted to spend $212 million in total operating expenses in 2023/24. For 2025/26. the recently published budget for total operating expenses is $204 million, 3.8% lower than in 2023/24. Add in, say, 5 per cent inflation over the two years and you are still looking at a real cut of under 10 per cent. Not easy to adjust to perhaps, but not very different from what a lot of other government agencies have experienced. The wild card of course was the budget for 24/25: $231 million. This year’s budget is about 14 per cent lower than that in real terms. But that 2024/25 budget never had any ministerial authorisation at all.

Another, but murkier, way of looking at it is to look at approvals under the Funding Agreement (which cover a – changing – subset of total operating expenses, but which are where the Minister of Finance is supposed to have control).

In the August 2023 update to the last Funding Agreement, Grant Robertson approved the Bank spending $149.44 million on in-scope operating expenses. In addition, they were explicitly allowed to spend on these items about $5 million of the amount that had been allowed for currency issuance expenses but which wasn’t needed for that purpose. So, say, $154,5m on in-scope operating expenses.

In the new Funding Agreement approved by the Minister in April this year, total in-scope operating expenses allowed for this year is $155 million (dropping away to $145 million next year, for reasons not made clear in the documents published so far, but maybe reflecting upfront restructuring costs – redundancy payments now for all those losing their jobs, already some weeks into 25/26?).

But you can’t just compare and contrast $155 million with $154.5 million because in the new Funding Agreement more spending items have been moved out of scope, not required to be covered within that $155 million limit. There are some smallish items (eg costs associated with the Bank’s legacy superannuation scheme, totalling probably less than half a million this year). But there is also this

Remember, these are business case costs, not some full cost of a project but you’d think they might easily total another million or two (consultants don’t come cheap).

And there is this explicit carveout, with some numbers

ie $5 million a year

Add those three items back in and the appropriate comparison to last year’s Funding Agreement level (the $154.5 million) is perhaps more like $161.5 million ($155 + 5 + 1.25 + 0.25). It drops away next year, but taking $10 million off that total still doesn’t leave them much less than the $154.5 million they were allowed for 24/25. The big problem – for them – is that they simply ignored that 24/25 limit and went for broke, hoping they could trick the Minister into setting them a permanently higher new baseline level of spending. It didn’t work fortunately. In a decent world they’d all (Orr, Quigley, the rest of last year’s board) apologise to the Minister, to the public, and to their own staff. In our world, staff lose their jobs and Quigley and the board keep theirs.

It is still interesting that they are needing to make such deep staff cuts to meet the budget and stay within the new Funding Agreement limits. Perhaps one partial reason might be the big new commitment they made to office space in Auckland – in what is apparently one of the fanciest new buildings in Auckland, with a five star green rating as well – on a scale which to have been anything like justified would have required even more growth in staff numbers. They signed up to that 4800 square metres last November, with no idea where the Funding Agreement would land and knowing they’d already well-overreached the previous Funding Agreement limits. According to last year’s Annual Report they spent $1 million on Rental and Lease Expenses (presumably mostly/wholly on their existing office space in a 40 year old building in Queen St). Not exactly a source I’d rely on for much but Google’s AI overview suggested that annual lease costs on the space in the new building could be $3.5 million (and their lease there runs from 1 August, while the existing lease doesn’t expire until 31 December).

In concluding I want to come back very briefly to the Post article. It is right to say that the Bank got much less than it had had the gall to ask for (unlike Oliver Twist, in asking for more they were already bloated), but what they are allowed to spend this year and next isn’t much different in real terms than what Grant Robertson had allowed them when he’d set the spending limit for 24/25. It is just a shame – actually, it should be scandalous – that they chose to ignore that limit so egregiously. Taxpayers and their own staff now pay the price.

Today, 5 August, is five months since the shock resignation – or, as now seems much the most likely, engineered exit – of the then Governor of the Reserve Bank, who disappeared from office that very day, getting generously paid for several more weeks but not working until the official date his resignation became legally effective, 31 March. Since then we’ve heard not a word of explanation from him and (more importantly, since they are still public officials) have been deliberately, actively, repeatedly, and still to this day obstructed and mislead by the Reserve Bank Board, notably the chair Neil Quigley, enabled by the Minister of Finance, and implemented (in respect of OIAs) by the temporary Governor, Christian Hawkesby.

Applications for the position of Governor closed a couple of months ago, so I guess we must assume that the selection and recommendation process is now fairly well advanced. The Board established a Governor Search Committee

Being chaired by Rodger Finlay – who has no background in macroeconomics or regulatory policy, and who had a questionable start to his time with the Bank (still chairing the board of the company that owned the country’s fifth largest bank) – doesn’t inspire much confidence. And if Finlay appears like a decent general corporate governance type of person, recall that he has been deputy chair through a) the reappointment of Orr, b) the Board approving the Bank running spending levels last year far beyond what the Funding Agreement had envisaged or allowed, and c) (and so we learned yesterday) was part of the Board that allowed management to sign a new lease on Auckland offices last November, massively larger than the current office, with space for many more staff than they currently had, when i) the Bank was already spending more than their Funding Agreement had allowed, and ii) they (presumably) still had no real steer from the Minister of Finance as to what approved spending for 25/26 and beyond was going to be. [Oh, and he’s been party to the cover-up of the last five months.]

Quite a team he and Quigley must make. Not exactly a team to inspire any confidence in the wisdom of whoever they end up putting forward as a first nominee to the Minister of Finance, or a team that might assure a good potential Governor that he or she was going into a well-led governance structure. Responsibility for that is shared by those Board members and by the Minister of Finance who has continued to express confidence in Quigley (for reasons not comprehensible to anyone outside her bubble) and refused to proactively ensure vacancies were quickly filled by new able people.

We had a Governor resign once before. Don Brash announced his resignation and left office on 26 April 2002. Just under four months later, Alan Bollard was announced as the new Governor.

Defenders of the Board and Minister might point out that things are a little more complicated this time. By law, the Minister now has to consult with the other political parties in Parliament (in practice the Opposition parties, since the coalition parties will already have been involved through the Cabinet appointments process).

The law does not require the Minister to change her mind if the other parties (some or all) disagree (perhaps strongly) with a nomination, although the statutory provision would be empty if she did not pay at least some heed to concerns expressed. (There is no sign Grant Robertson did – and it was his new provision – when he went ahead and reappointed Orr, over objections from both ACT and National in late 2022, but if the provision is to have any meaning at all, you’d hope there would be some serious reflection on any objections, especially when an incumbent is not involved.)

However, if the paper work is a bit more time-consuming now than it was in 2002, bear in mind that the appointment of Bollard was accomplished in less than four months even though Michael Cullen had rejected the Board’s initial nomination.

By law (see above) the Minister and government can only appoint someone the Board recommends. But that does not mean that the Minister has to accept any particular recommendation. That isn’t the empty provision people sometimes suggest. There have only been three new Governor appointments since the legislative model came into effect (in 1990) and Michael Cullen recorded in his autobiography that he rejected the then Board’s nomination of Rod Carr (deputy and at the time acting Governor).

As was his perfect right to do. (The Board must have at least half-expected their nomination to be rejected as it was understood among senior management at the time that Helen Clark had made clear that she wasn’t going have any “Brash-clones” appointed.) I’ve long championed the much more conventional model in which the Minister gets to appoint their own preferred person as Governor directly (perhaps accompanied by scrutiny hearings by FEC before the person actually takes up the office).

But it was all done in less than four months, and it is now five months and counting since Orr left (and the Bank in 2002 was in nothing like the mess, or urgent need of new strong capable respected leadership that it is now). I hope the Minister is drumming her fingers and urging the Board to get on with it.

Quite who they might come up with remains a mystery, or whether the couple of new Board members this year might persuade their colleagues that whatever the Board has once seen in Orr he should be almost a benchmark antithesis of the sort of person who should be chosen.

I wrote a post a couple of months ago, shortly before applications closed, prompted by the advert for the job and what it suggested the Board might be after. As I have noted throughout, I don’t believe there is any obvious ideal candidate, and so inevitably compromises will have to be made (and in recruiting a person, the Board and Minister need then to have regard to the willingness and ability of the person to clean house and build a new and more capable second tier – we cannot for long be in a position where the deputy chief executive responsible for macroeconomics and monetary policy has (a) no background in the subject, and b) can’t intelligently comment on anything of substance other than from a script she has been given).

That said, straws in the wind aren’t terribly encouraging.

I’ve heard that a couple of very able applicants didn’t even get an interview (there is such an abundance of talent? Really?). And then there was media report (that I’d heard via markets people earlier) that a Bank of Canada Deputy Governor (they have many) was a strong possibility, perhaps even a frontrunner.

This would seem an ill-advised choice if it was really a direction the Board was considering taking. Gravelle seems to have no particular connections to New Zealand (other than a couple of conferences, one by Zoom), and comes from an organisation that – unlike the Reserve Bank of New Zealand – does not do banking (and non-banking) financial regulation and supervision, these days a big part of the Bank’s job. For all its undoubted analytical strengths, the Bank of Canada also has a quite different sort of monetary policy governance model (entirely internal) than New Zealand’s. And then there is the adverse selection issue: a person who was good enough to be a serious contender for Governor in his/her own country (G7 country and all that) would not be very likely to put themselves forward to be Governor of a much smaller, poorer, remote country’s central bank, a country with which they’ve had no particular ties. As a couple of people have put it to me, it is a bit reminiscent of the old imperial days – someone not quite up to being appointed Governor-General of Canada or Australia might still be handed down to New Zealand. And it is not as if parachuting in foreign appointees to top economic roles here has been a particular success story (see last two Treasury secretaries), nor in many ways was bringing back an expat after 15 years away to the Reserve Bank (even if Orr’s record makes Wheeler look less bad). Can we really have fallen so far that we can’t find a credible respected appointee at home?

Always possible I guess. Compelling choices certainly aren’t thick on the ground.

What of the temporary Governor, Christian Hawkesby? These were my comments a couple of months ago

Much of which I would repeat today. But unfortunately since early June we’ve seen not just that Hawkesby has been a part of the obstruction effort re Orr’s departure (and if he is working to Board direction the fact that he has not been willing/able to insist on a more open approach is a poor reflection on any claim he has to be thought a worthy occupant of the permanent role. And then of course there was that last sentence. We now know that not only did he repeatedly sit alongside Orr while he (Orr) mislead Parliament, but that Hawkesby himself misled them just three months ago. He proved unable to even pass that low bar I mentioned in June.

I ended that earlier post speculating on some possible sorts of names I hadn’t seen mentioned in any of the media articles (bearing in mind that the advert had talked of the importance of both financial markets knowledge and CEO experience)

Since Stobo is (a) an economist by training, b) has CEO experience, c) has financial markets expertise, and has been appointed to his current public sector role (chair of the FMA) by this government, and is a thoughtful and reflective person .you could see why he might be a strong contender if he wanted it (and was willing to give up his portfolio of directorships etc and media commentary). If one can’t have much confidence in the FMA, there’d definitely be worse people for the job.

But it is time to get on with it and get a new Governor in place. And then get on and refresh the Board, with a new chair to work with and oversee the Governor.

When our kids were little one of the books we often read them was “Bears in the Night” in which the young bears, hearing a noise outside, sneak out of the house at night, climb Spook Hill and then, terrified by the sudden appearance of an owl – not the most threatening of birds – whose call they’d heard, rush back to the comfort and security of home and bed.

It came to mind when reading some of the arguments being advanced by government officials and banks over the Credit Contracts and Consumer Finance Amendment Bill currently making its way through the Finance and Expenditure Select Committee.

The key controversial bit of the bill is the proposal to legislate retrospectively to close down class action suits currently before the courts against ANZ and ASB in respect of flaws in loan variation procedures etc that occurred between 2015 and 2019. The Credit Contracts and Consumer Finance Act had been amended in 2015 in ways that provided (MBIE’s words here) “that the borrower is not liable to pay interest or fees over any period of non-compliant disclosure made before loans are entered into or varied”. In late 2019 the Act was further amended so that for future breaches courts would have “explicit discretion to extinguish or reduce the effect of this provision in order to reach a just and equitable outcome”. That amendment was deliberately and consciously not made retrospective, but the current government now proposes to further amend the Act to apply the post-2019 regime to breaches that arose between 2015 and 2019.

Retrospective legislation is, almost without exception, an odious concept. Perhaps one might make an exception where, say, there was a clear typo in the legislation, giving a quite different meaning to the words of the legislation than Parliament had clearly intended. That wasn’t the case here. Rather, right or wrongly, Parliament changed its mind in 2019 about what the law should be going forward. Now the government – egged on by the banks – wants to make it as if a consciously and deliberately chosen law never was.

(Perhaps one might also make an exception to the general principle against retrospectivity if it was belatedly realised that the words Parliament had enacted enabled the strong to egregiously exploit the weak. I don’t know that that exception is in the typical lawyers’ list, but as a citizen/voter I could see the possibility (perhaps a parallel to exercise in criminal cases of a royal prerogative of mercy).)

What is puzzling is why the government would propose to amend the law retrospectively to help out large and highly profitable foreign banks. And in so doing to bypass what is apparently usually the practice when (as happens on rare occasions) retrospective legislation is passed, when cases already before the courts are (apparently) protected.

I hadn’t paid an awful lot of attention to the whole issue until two or three weeks ago when big scary numbers generated by the Reserve Bank were reported (eg here) and thus entered the public debate under headlines (not, to be clear, sourced to the Reserve Bank) about threats to the financial system unless this retrospective law was passed. $12.9 billion (the maximum estimate reported) sounded like a lot of money (but just glancing at articles I didn’t have a basis for knowing what a right number might actually be), even if stories about threats to the soundness of the financial system never rang true even for a minute.

And I still didn’t pay a lot of attention until the media reporting this week of the appearances before the select committee of the Bankers’ Association (strongly in support of the proposed amendment), the lawyers for the plaintiffs in the class action suits, and representatives of the litigation funders, LPF. The video of those appearances, and associated questions and answers, is currently here.

Yesterday, one of LPF’s representatives rang me, apparently given my name by several people as someone who might write a critical piece for them, especially on the Reserve Bank numbers, and the uses and abuses being made of them. I don’t really do submissions for hire, and am not taking any money from them, but my interest was piqued, and I benefited from a couple of useful conversations with them. More importantly, they sent me the document that contains the material from the Reserve Bank, a paper from MBIE to the then Minister of Commerce and Consumer Affairs (Andrew Bayly) from October last year which includes “Annex Two: Summary of RBNZ modelling and advice”. That annex appears to have been written by the Bank. The full document is here

In other words, we know nothing about the model, the scenarios, assumptions etc although it appears – from the OIA exclusion ground cited – that they must have obtained some data from one or other of the banks to somehow inform their numbers.

Note, though, that even the “big scary number” scenario, isn’t exactly a grave financial stability risk: “low to medium impact on capital ratios” is the Reserve Bank’s own line. Big numbers but if the underlying business models are profitable (as New Zealand banking typically is) then even in a hypothetical like this recapitalisation wouldn’t be expected to be an issue (whether from direct shareholder injections or retained earnings). Aside from anything else, and as they note, litigation will roll on for years. Losing on the scale of this “big scary number scenario” would be painful, but from the outside you could conceptualise it as a bit like a backward-looking windfall tax which, justified or not, wouldn’t normally really affect future behaviour. And when bureaucrats and the like come up with three scenarios, or three policy options, they typically expect people will be drawn to the middle one as perhaps best expressing their view or preference (and to be clear in this Annex the Reserve Bank is not taking a position on the merits of the proposed retrospective amendment).

It really isn’t clear how the Reserve Bank came up with the big scary number. Over the period in question – 2015 to 2019 – total housing and consumer loans averaged about $275 billion. If the average interest rate over this period was about 5 per cent, the average disclosure failing occurred half way through the period, and a third of all retail loans in the economy (by value) were subject to disclosure failings, the total interest involved would have been be about $10 billion, which is (I guess) in the same order of magnitude as the Reserve Bank’s $12.9 billion number (especially if one allows for interest on such an amount through to today).

But we know, for multiple reasons, that this cannot be a number to take seriously.

For a start, if the Bankers’ Association and its members thought it was even roughly accurate as an estimate of the sector’s exposure, they’d have hired a consultant economist to churn out quickly a well-explained and documented version of their own (rather than just waving around the worst Reserve Bank numbers, where any details as to how it was done are – perhaps conveniently for them – blacked out). It wouldn’t take long, and the Bankers’ Association clearly isn’t short of money to deal with this issue: at their FEC appearance they brought along three [UPDATE: two apparently] KCs to help testify and answer questions on legal dimensions. One of those KCs – James Every-Palmer – actually told FEC (at about 24 minutes in) that the sums being sought in the cases against the ANZ and ASB were “as I understand it, hundreds of millions of dollars” (before then handwaving to tie this to a system-wide $12.9 billion dollars). ANZ and ASB together make up the best part of half the banking system, so if the Bankers’ Association understands the claims against them to be “hundreds of millions” then even if that represented $1 billion in total, it is all but impossible to see how the rest of the system could be exposed to $12 billion of claims.

There are several reasons for that statement: no other claims have been lodged, the litigation funders told the committee they had heard of no other claims (and any such claims could really only go forward with litigation funding given the cost of civil justice), and the existing legislation is written in such a way that any further claims, not already lodged, would almost certainly be out of time (more than five years on from when breaches were disclosed). I’ll leave those points to the lawyers to argue about, but there is also some hard data on the numbers of customers involved.

The Commerce Commission reached settlements with the four big banks (and Kiwibank) some years ago, and those settlements (which involve compensation for actual loss, and did not preclude civil action by customers) are all sitting on the Commerce Commission website to consult.

102000 customers were affected. That appears to have been around 30 per cent of ANZ’s mortgage customers in 2015, and at 31 December 2015 ANZ had about $63 billion of retail credit outstanding.

Under the existing provisions of the CCCFA, customers were not liable for interest in the period between an erroneous notification and either when it was corrected and they were notified, or when they next made a (validly informed) change to their loan. Someone who changed the fixed term of their mortgage in December 2015 (getting incorrect disclosure) is likely to have changed it again before the end of 2019 – say, on average, December 2017 – and received correct information then.

However, as I understand it, the (potential) ability to claim back all interest also only applies to those loans which had been taken out from 2015 onwards, so it is likely to be only a minority who are covered by the current class action suits, given that the poor disclosures only occurred for one year.

It isn’t impossible – depending on the specific assumptions – to get up to a total towards $1 billion of exposure, BUT we already know that is a) more than Bankers’ Association lawyer suggested the claims were, b) more than implied by the plaintiffs’ settlement offer this week (around $300m, suggesting that was around two-thirds of the total exposure).

The ASB situation is a little murkier. For ANZ, the bank knew exactly who’d been affected (and so past actual reimbursements were for actual errors). At the time of its Commerce Commission settlement, ASB did not know how many or who had got the wrong disclosure, only that in total 73000 customers were potentially affected.

The breach went on for longer so a larger proportion of those customers are likely to be able to potentially claim back the interest and fees paid over those years (the median such customer in principle having a claim for about two years of interest). But we have no idea how many customers actually got the correct disclosure – ASB seems not to have had the systems to know, but presumably if this case proceeds will go to lengths (costly lengths) to ensure that the actual victims of procedure “not consistently followed” are identified and only for them might there be an exposure (in the Commerce Commission settlement all 73000 were paid a fixed and modest lump sum, presumably cheaper then than trying then to go through every customer file).

If 20 per cent of the affected (post 2015) customers got the incorrect disclosures, I could produce an estimate as high as $700-800 million. But again, as with ANZ, these numbers seem higher than material in the public domain from those better placed to know already suggests. And even taken together with a high-end estimate for ANZ, nowhere near half of the $12.9 billion for the Reserve Bank’s high-end scary number scenario.

And those are the two banks against whom a case is actually being taken.

Of the other two big banks, BNZ accepted a warning from the Commerce Commission. The number of customers involved was much smaller (11956 in total) of whom 2300 had been directly compensated by BNZ. Meanwhile, the Westpac settlement involved new credit card customers only (so, on average, far smaller loan balances) and only 19000 of them. Kiwibank – while smaller in total – has a substantial retail customer base and seems to have had a similar issue to ASB. It had 35000 new borrowers with a variation potentially affected. But it is hard, even adding all three up, to get to more than another $1 billion maximum exposure. And, to repeat, no class action civil case has been taken against those banks, or indeed any of the smaller lenders, about whom MBIE purported to be so worried. Even if things were not out of time, smaller lenders who’d breached might in any case have been unlikely to have sufficient customers to attract a potential litigation funder).

Only someone with access to really detailed information at an individual bank level could come up with a reasonably robust system-wide estimate of potential exposure in the now, almost impossible event, that cases were to have been taken against any other institutions. But it still looks as though even the Reserve Bank’s second scenario – which they describe as “low impact” on capital ratios – would err on the high side. Based on what the Bankers’ Association lawyers have said, based on what the plaintiff’s lawyers have said, and taking account of the absence of other claims and the likely out-of-time nature of any further claims, it is difficult to see how a worst case involving actual claims before the courts exceeds $1 billion in total.

You can understand why the ANZ and ASB and their shareholders would prefer not to pay such a sum, and would (a) fight it in court, and b), if they could, lobby for a retrospective law change. But it simply isn’t a financial stability issue. It is worth remembering that 15 years ago a big tax case went against the banks, costing them $2.2 billion in an economy then about half the size (nominal GDP) of today’s (and in the midst of a severe recession). Banks affected emerged just fine. When MBIE advised the Minister last October to act to “immediately alleviate distress in the market”, there was (and is) no sign of distress in the market – as it affected ability or willingness to lend, of large players, players being sued, or other lenders – just some “distress” in the local board rooms of ANZ and ASB.

(And note that MBIE’s own advice a month later – page 31 here – was that the proposed amendment was “not clearly necessary to address concerns about the financial position of either ANZ or ASB” and “we acknowledge that applying this amendment to the active class action has “upside” potential for the banks only”.)

Without someone launching an OIA – which the Bank might well stall for several months – we have no way of knowing what the Reserve Bank makes of the use being made by the Bankers’ Association of the $12.9 billion number, or even whether they would still stand by it as a plausible scenario now, 9 months on. But it is pretty clear that – with material then in the public domain – a number on that scale never made any plausible sense, and that the only cases that are actually before the courts – the only cases now likely ever to be – probably involve total stakes less than 10 per cent of that “big scary number”. The banks affected will know that too, but in expected value terms it is no doubt better them to just repeat over and over the “big scary number” and hope to scare the government into passing this retrospective law than to come straight out and acknowledge the plausible maximum scale of any exposure if they lose in courts (and several rounds of appeals) and if the courts made awards fully consistent with the plaintiffs’ claims.

I took from the select committee appearances the other day that while the plaintiffs and their funders oppose the use of retrospectivity on principle, they would (unsurprisingly perhaps) be content with a carveout that meant that the proposed amendment did not apply to cases already before the courts. You can understand why ANZ and ASB would not like that, but why shouldn’t the government and Parliament, particularly once they realise that the big scary number is just a fairy tale, although being used rather more maliciously than a typical parent readings Bears in the Night to their young ones? And yet lawyers for ANZ have the gall to suggest that the plaintiff’s settlement offer this week is “a cynical attempt to influence the law reform process currently before Parliament”. One might well understand why the plaintiffs might make a settlement offer when ANZ and ASB seem to have the government lined up in their corner, but there is no mistaking that brandishing the poor old Reserve Bank’s big scary number is much more evidently an attempt to keep the select committee in line and make public opinion a little less unsympathetic to a law change designed specifically (and only) to help two big (foreign) banks.

For anyone interested, there is a column by Jenny Ruth ($) on related issues this morning.

Finally, regular readers will know that I am not exactly a “bank basher” and have often here derided the rather desperate anti-Australianism implicit in a lot of the NZ political attacks on banks. I think we have a pretty good banking system generally. I’m not necessarily a big fan of the CCCFA in any of its forms (and thought the actual plaintiff who was wheeled up to the select committee the other day was singularly unpersuasive – unlike his lawyer). But I don’t like people playing fast and loose with “big scary numbers”, when they know (or could reasonably be expected to know) that they, and claims made for them, bear little or no relationship to reality. And I don’t like retrospective legislation one little bit.

In both The Post and the Herald this morning there are reports of interviews with executive members of the Reserve Bank’s Monetary Policy Committee: the Bank’s chief economist Paul Conway in The Post and his boss, and the deputy chief executive responsible for monetary policy and macroeconomics, Karen Silk in the Herald. In a high-performing central bank the holders of these two positions should be the people we look to for the most depth and authoritative background comment on monetary policy and economic developments. But in New Zealand we are dealing with the legacy of the Orr/Quigley years where we struggle to get straightforwardness, let alone depth and insight.

Now, to bend over backwards to be fair, interview responses will depend, at least in part, on what the journalist concerned chooses to ask. But then standard media training advice is to answer the question you wish they’d ask, not (necessarily or only just) the one they did. An interview with a powerful decisionmaker is a platform for the decisionmaker.

The Conway interview appears somewhat meandering and not very focused. I wanted to touch on three sets of comments in it.

First, asked about the transition after Adrian Orr’s sudden (and unexplained) departure, he says it is business as usual and it has been “a very smooth transition”.

“I think this institution is bigger than even Adrian Orr [it was certainly bigger – much bigger – as a result of Adrian Orr]……There’s a real sense of the ‘show must go on’ and it really has. We miss Adrian. It is a bit less fun around the place, less jokes going on – probably more appropriate jokes”, he smiles again.

So in addition to Orr being a bully, an empire builder, and someone well known for freezing out challenge and dissent, he also created an uncomfortable and inappropriate working environment? Or at least that is what Conway appears to be saying about the man who recruited him.

But you also wonder about just how straight Conway is being (and why the journalist didn’t ask more). After all, the Bank itself tells us there are big changes afoot (presumably consequent on the new Funding Agreement, prospect and actual). In the just over two months since Orr resigned, the top tier of management has been brutally slimmed down (credit to Hawkesby). At the start of March there was the Governor and an Executive Leadership Team of seven Assistant/Deputy Governors and one “Strategic Adviser”. Since then, Kate Kolich, Greg Smith, Sarah Owen, Simone Robbers and Nigel Prince have all either left already or we’ve been advised they will soon be doing so (none with an announced job to go to). Governor plus eight has been reduced to Governor plus four. And

That first group is Conway’s own level (though presumably the Bank will continue to need a chief economist). And then on down to the staff (and much of this is because Orr/Quigley massively blew the budget limit Grant Robertson had set for them and went on one last hiring spree last year). You somehow suspect that all is not exactly sweetness, light, and engagement at the Reserve Bank.

And then there was this

Conway is on record as a bigger-government sort of guy (we had his extra-curricular stuff last year, as an example) but what possessed him, interviewed as an MPC member and senior central banker, to suggest that more state interventions and bigger government might be “worth thinking about”? It simply isn’t in his bailiwick, and he shouldn’t have allowed himself to be dragged into responding to a hypothetical, especially about one outside the Bank’s responsibilities.

And finally, we got the meandering thought that “it’s possible that we get to a point where people just adjust their behaviours and ‘uncertainty’ becomes the new normal and we just get on with it. I’ve got no ’empirics’ to base that on – it’s just, I think, a very interesting thought-stream.”

Really? A “very interesting thought-stream” that people do in fact adapt to the world as it is? Startling and insightful (not).

Then, of course, there is his boss, Silk. Most serious observers regard her as fundamentally unqualified for her job, and not the sort of person who would be likely to be on an MPC anywhere else in the world, let alone as the deputy primarily responsible for monetary policy. She can be counted on to safely deliver speeches on operational topics that others have written for her, and to answer purely factual questions at MPS press conferences and FEC about what has happened to swap yields and mortgage rates. And that is about all.

She also seems to have a mindset in which rates being paid on existing mortgages are what matter rather than the rates facing marginal borrowers and purchasers. Perhaps it is what comes from a non-economics background in a bank? Thus, in the Herald interview we are told that she claimed that “the effects of the 225 basis points of OCR cuts the committee had delivered in less than a year were yet to be widely felt”. The journalist added some RB data on average actual mortgage rates which might appear to back that up. Of course, expected cash flows matter as well as actual ones – if your fixed rate mortgage is going to roll over in a couple of months onto a much lower rate that will almost certainly be affecting your comfort, confidence, and willingness to spend now. But more to the point, marginal rates for people looking at buying a property or otherwise taking on new debt have come down a long way, and were already down a long way months ago. This chart is from the Bank’s own website, showing short-term fixed mortgage rates.

As at yesterday, rates were a few basis points lower again than the end-April rates shown here. 200 basis points plus down from the peak, and that not just yesterday. And falling wholesale rates, which underpin these falls in retail rates, also affect the exchange rate, another important part of the transmission mechanism. (And, of course, with all Silk’s focus on the cash flows of existing borrowers, she never ever mentions the offsetting changes in the cash flows for existing depositors – I’m of an age to know!)

So far, so predictable (at least from Silk). But then there was this (charitably I’ll assume the word “fulsome” was not hers)

Reasonable people might differ over the inflation outlook and the required future path for the OCR, except that we were told in the MPS that there was unanimous agreement from the MPC to the forecast path for interest rates. And that is a path that is lower from here than the path published (again unanimously) in the February MPS (the deviation begins after the May MPS, not at it). In other words, not only did the February path show some further easing from (where they expected to be, and were, by) May onwards, but the May path shows even more easing from here forward.

And yet Silk talks of a “much stronger easing signal” sent in February.

Frankly, they seem all over the place. If the Committee (as it did) unanimously agrees to publish a (somewhat) steeper downward track than the one you had before then either you have an easing bias – always contingent on the data of course – or you made a mistake in adopting the track you did. And if you are comfortable with the track, it feels like a mis-step for the temporary fill-in Governor to announce that there was no bias. I guess Silk might have got stuck having to cover for her fill-in boss, but it is a pretty poor look all round. Surely (surely?) they must have rehearsed lines about biases before the press conference? Surely, if so, someone pointed out the disconnect between the proposed words and the chart above?

And finally from Silk we learn that “price stability is one of the conditions you need for growth”. It simply isn’t – and the economists on the committee are usually much more careful, with the standard central banker line being that price stability, or low and stable inflation, is the best contribution monetary policy can make (many muttering under their breath that that contribution isn’t necessarily very large). Not to labour the point but the economy was still growing, reaching its most overheated point in late 2022, when core inflation was around its worst.

All in all, not a great effort at communications from the MPC this week. As I noted in my post on Thursday, there was none of the prickly frostiness of Orr, and no sign of deliberately or conscious setting out to mislead Parliament, but it simply wasn’t a very good performance. And while Hawkesby is new to the role, chairing MPC and acting as its prime spokesperson on the day, Conway and Silk have no such excuse. Someone flippantly suggested that perhaps there is something about May and the MPC – last May was when the MPC went a bit wild talking of raising rates further (the OCR was still going to be above 5 per cent by now), and then Conway tried to blame his tools, rather than the judgements of him and his colleagues, for the associated forecasts.

If the government is at all serious about a much better, world class, Reserve Bank, they need to work with the Board to find a Governor who will lift the game and the Governor/refreshed Board will need to work with the Minister to produce a stronger MPC. It would seem unlikely that in such an improved Bank/MPC there would be a natural place for either Conway or Silk, pleasant enough people as they may be.

Things seem to be at a pretty low ebb in and around the Reserve Bank. There was, in particular, the mysterious, sudden, and as-yet unexplained resignation of the Governor (we’ve had four Governors since the Bank was given its operational autonomy 35 years ago, and only two have completed their terms and left in a normal way, which must be some sort of unwanted advanced country record). Having slimmed down the bloated number of Orr’s deputies by one last year, another of them quietly resigned and left last month on (apparently) short notice and no specific job to go to. Of those who remain, two are (at best) ethically challenged and one is simply unqualified for the job she holds.

And then there is the mystery as to why a temporary Governor (specifically provided for in the Act) has not yet been appointed, even though it is now four weeks since Orr tossed his toys and walked out (formally finishing on 31 March, but no longer present). I wrote about this briefly on Monday morning when it emerged (in The Post) that despite what the Minister and Bank had led us to believe on the day Orr resigned (effective 31 March), there would not be a temporary Governor in place from 1 April. The Bank’s spokesperson, quoted in the Post article on Monday so badly misread the relevant provisions of the Act that the Bank seemed to feel it necessary to issue a release yesterday, which added nothing but at least didn’t muddy the water further. The Bank’s Board has to (finally) make a recommendation of a person to serve as temporary Governor by 28 April, but even once she gets such a nomination the Minister of Finance can take as long (or short) as she likes to make an appointment (or, presumably, knock back a recommendation and send the Board away to make another).

Reasonable people would have assumed that within a few days of Orr announcing his resignation (and storming off), the Board would have met and made a recommendation. With more than three weeks notice (at least on paper) having been given there was really no excuse for not even having a recommendation on the Minister’s desk by the end of March. We are left to wonder why. Perhaps Hawkesby didn’t want the job? Perhaps the Board doesn’t have confidence in him to do even the fill-in role? Perhaps the Minister had indicated that she didn’t want him? We don’t know, and neither do international markets who (like the rest of us) were taken off-guard by Orr’s resignation. It really isn’t a good look. And if for some reason Hawkesby isn’t an option (and there are very slim pickings among the other 2nd tier managers), perhaps they could twist the arm of former Deputy Governor Grant Spencer and bring him back for a second stint filling in between Governors (only it would be legal this time)?

The unsatisfactory picture was compounded just a little later on Monday morning when Hawkesby and the Board chair Neil Quigley fronted up to the Finance and Expenditure Committee to announce that they were after all going to have a review of bank capital requirements (their opening statements are here). This had all been arranged with the Minister of Finance, who put out a simultaneous statement welcoming the review, and confirmed by the Bank’s Board at a meeting last week (which the outgoing – but still in office, and thus still a Board member – Governor did not attend).

[UPDATE: Meant to mention that Hawkesby did himself no favours – if he aspires to be seen as anything other than Orr’s man – when he opened his FEC statement this way (emphasis added)

“I’d like to begin by acknowledging our Governor, Adrian Orr, who over 7 years would have attended FEC hearings more than 50 times and always been engaging. We are looking forward to continuing that relationship.”

Orr actively misled FEC repeatedly, and the frostiness of his encounters with any questioning FEC members has been repeatedly commented on. ]

Recall that, rightly or wrongly (I think wrongly), Parliament has given policymaking powers on such matters to the Bank (and specifically to the underqualified Board). Recall too that just a few weeks ago the Minister of Finance had indicated that she was seeking advice on ways to compel the Bank to change policy. Presumably the Board – and perhaps management – reading which way the political winds were blowing simply caved and arranged Monday’s FEC appearance and announcement, rather than risk losing their powers. They were, after all, in a weak position: as far as we know the Bank’s Funding Agreement for the next five years has not yet been approved (the Minister has talked of coming cuts), there wasn’t a permanent Governor in place, and even the appointment of a temporary Governor seemed to be hanging in some sort of limbo.

It is always possible that the Bank itself (especially now minus Orr – who last year was vociferously defending current policy and, as so often, attacking any critics) thought that a review was (substantively) timely and appropriate, but it looks a lot like bowing to political pressure, at a point of particular weakness. In an independent agency. And, frankly, since I believe that big policy calls should be made by elected politicians, I’d rather the government had actually legislated to shift big-picture prudential policymaking powers back to the Minister of Finance, while retaining a vital role for a better-performing Reserve Bank to advise and to implement (essentially the model in most other areas of government policymaking).

There are also lots of questions about where to from here with the review. The suggestion from Quigley is that the review will be completed by the end of the year, but while decisions are finally a matter for the Bank’s Board, it does invite the question of what role (if any) the new permanent Governor is to have (at least if it is anyone other than Hawkesby). By law, the temporary Governor can (eventually) be appointed for six months, extendable for another three. Even if the Board gets on and advertises for a permanent Governor this month, at best it will be several months before a new Governor is on board (eg there was roughly six months between Don Brash resigning and Alan Bollard starting work). With a non-expert Board wouldn’t one normally expect the Governor to be taking the lead in formulating the advice on which the Board would finally make decisions? Or is the new person to be presented with a fait accompli?

And then of course, there are questions about the nature of the review itself. Is it purely appearance theatre (“we need to look like we are doing something”) or is it genuinely a case of an open-minded reassessment? There is talk of consulting banks before any changes are made, but what about the wider group of interested experts and commentators (many of whom submitted on the 2019 policy proposals/decisions)? And for all the talk of commissioning “international experts”, surely only the most naive would take that at face value. You choose your expert according to your interests (eg a different group if one wanted people likely mostly to reaffirm your priors than if you were genuinely opening things up). I reread yesterday my post about the “international experts” Orr had commissioned in 2019, and the rather limited (and conveniently-supportive, having been chosen for a purpose) contribution they made. Those earlier experts were barred from talking to anyone in New Zealand other than the handful the Bank approved. Will it be any different this time?

And although back in 2019 the law was such that the decisions were still those of Orr alone (the Board then had a different role), Quigley was also the Board chair then and has had Orr’s back right throughout his time in office – apparently serving the Governor’s interests more than the public’s interest. His own questionable relationship with the facts on a number of occasions has also been documented here on various occasions. Apparently Quigley presented quite well at FEC on Monday, but so what? When he isn’t under pressure – and FEC was more attuned to welcome the review than ask very searching questions – he is a smooth operator (when he is under pressure, well…..see his press conference on the afternoon Orr resigned).

My own view, back in 2019, was that even the final Orr position – which pulled back from the initial proposals – went further than was really warranted. But one of the things I’d be looking for as part of the Bank’s review this year – and as a test of seriousness and openmindedness – is a rigorous and transparent comparison of the New Zealand capital requirements (for large and for small banks) with those of other countries. The Reserve Bank made no atttempt whatever to provide those sorts of comparisons in 2018/19.

One might think of countries like Norway, Sweden, Denmark, Australia and Canada, but perhaps also advanced countries where the bulk of the banking system is made up of subsidiaries of much-larger foreign banks (for example, the Baltics). To do this properly isn’t a superficial exercise of comparing headline capital ratios. One needs to look at things like the composition of balance sheets (in a quite granular way), risk weights on individual types of exposures (standardised and IRB) and so on. One might, in principle, take the business structure of one or more New Zealand banks and actually apply the rules in other countries to see how much capital they would be required to have on those rules, relative to the rules here.

If the current Reserve Bank policy, and scheduled further increases in minimum required capital, ended up pretty much in the pack, relative to the situation in other advanced countries, it might be considered the end of the matter. There might not be anything very optimal about what those other countries have chosen to do, but the case for any revision to the New Zealand rules would be that much harder to sustain than if (for example) the full New Zealand requirements imposed much higher capital requirements on much the same sort of portfolios. There is no compelling reason to believe that the exposure to really serious adverse shocks is any greater in New Zealand than in other advanced economies, so absent a compelling argument that the rest of the world is just “too lax”, being somewhere around the median of other countries might be a reasonable benchmark for New Zealand authorities (in a world of inevitable great uncertainty). (Incidentally, there would be no point in having requirements lower than those applied by APRA, since their requirements would set a floor for the Australian banking groups as a whole – there has been too little mention of the APRA group requirements in the recent New Zealand debate).

Reviewing some old posts yesterday I also stumbled on this chart, taken from a 2019 working paper of the Basle Committee on Banking Supervision (which I wrote about here)

I don’t want to fixate on the individual numbers, but simply to reiterate the point that any wider economic gains from higher required minimum capital ratios abate quite quickly as those requirements are increased. Actual numbers that might emerge will depend heavily on things like assumed discount rates (the ones used in these studies are far below the standard discount rates for us in New Zealand public policy evaluation), and the ability (or otherwise) of high capital ratios to save us from financial crises with severe economic consequences (a point quite in contention in 2019, when I observed that the numbers used by the Bank and their supporters were grossly implausibly large).