It is the time of the cycle when plenty of groups are keen to have their policy ideas and prescriptions be heard. After all, parties may still be finalising policies and there seems to be a reasonable chance of a new government and different set of ministers before long.

Many are just self-interested (no doubt the authors mostly believe there might be wider benefits, but the fact remains that they are championing policies to help their firm/industry/sector). As an example I found a link in my email this morning to one called a “Blueprint for Growth”. It was this from the covering press release that made me rashly open the handful of slides:

“Today’s announcement is just the beginning, as we know that good, evidence-based, bipartisan policy leads to better outcomes for all New Zealanders. This is part of the key to unlocking the future prosperity and productivity in New Zealand.

Instead it was a bunch of suggestions from the Financial Services Council, some probably worthy, others purely self-interested, that were primarily going to be good for member firms of the Financial Services Council and which, whatever their merits, were going to do nothing at all for productivity,

Yesterday the New Zealand Initiative released a rather more substantive effort, an 86 page collection of proposals and recommendations across a wide range of areas of government policy (nothing on foreign policy for example, and no references to China at all, except perhaps by allusion when discussing the proposed foreign investment regulatory regime, and no mention at all of company tax). (I wrote about their Manifesto 2017 here.)

In some parts of the left, the New Zealand Initiative is looked on as some sort of lobby group for big business, and anything they say is, accordingly, to be dismissed without further examination. The Initiative would sometimes have you believe that it was the opposite: simply public-spirited disinterested people, focused only the well-being of all New Zealanders, who put up their money (in some cases, although mostly their shareholders’ money) only to produce research and analysis without fear, favour, or predisposition. The truth is probably in the middle, but it really shouldn’t matter because the Initiative is transparent about (a) who their members are, (b) their staff and the views of those staff, and (c) their analysis and research. Their stuff should be taken on its merits, and critically scrutinised in the same way as any other contributions to debates. Topics chosen will presumably reflect, to some extent, members’ interests (in both senses of that word) but that is a different matter than what is said on those topics.

I probably agreed with half the proposals in the latest Prescription. I often find myself agreeing with them on second order issues, while profoundly disagreeing with them on the diagnosis and prescription for New Zealand’s long-running productivity failure. But it is a fairly serious collection of ideas and I was a bit surprised not to have seen any media coverage.

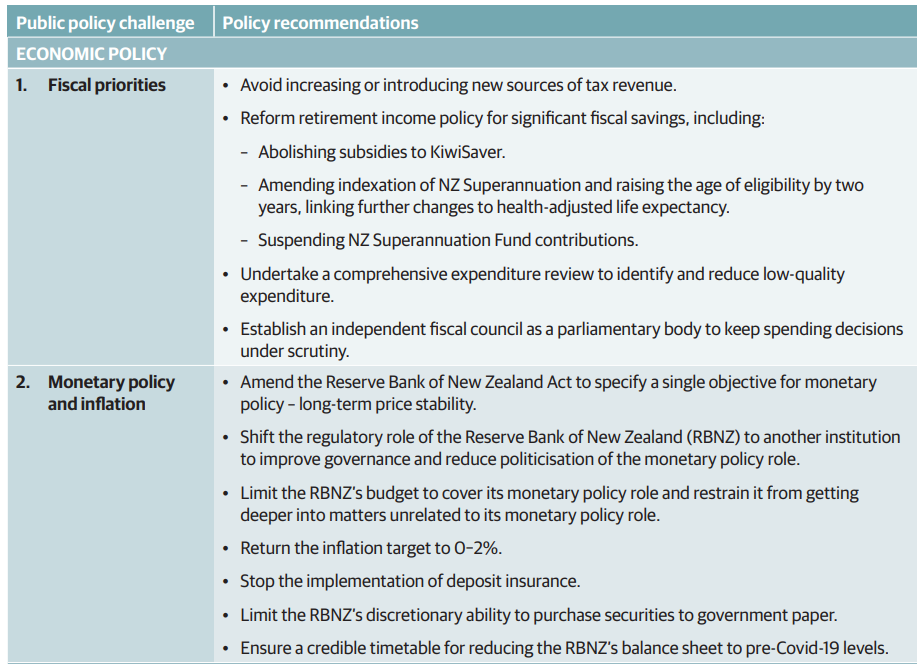

In this post I wanted to comment only on their fiscal and monetary policy recommendations, summarised here (and discussed in a bit more depth on page 20-22 of the PDF.

Take fiscal first.

While I generally agree with the first recommendation (no new or higher taxes) – since there is plenty of room to close the (large) deficit by cutting out low-value spending over several years – some of the arguments adduced in support don’t stand much scrutiny. Take, for example, this paragraph

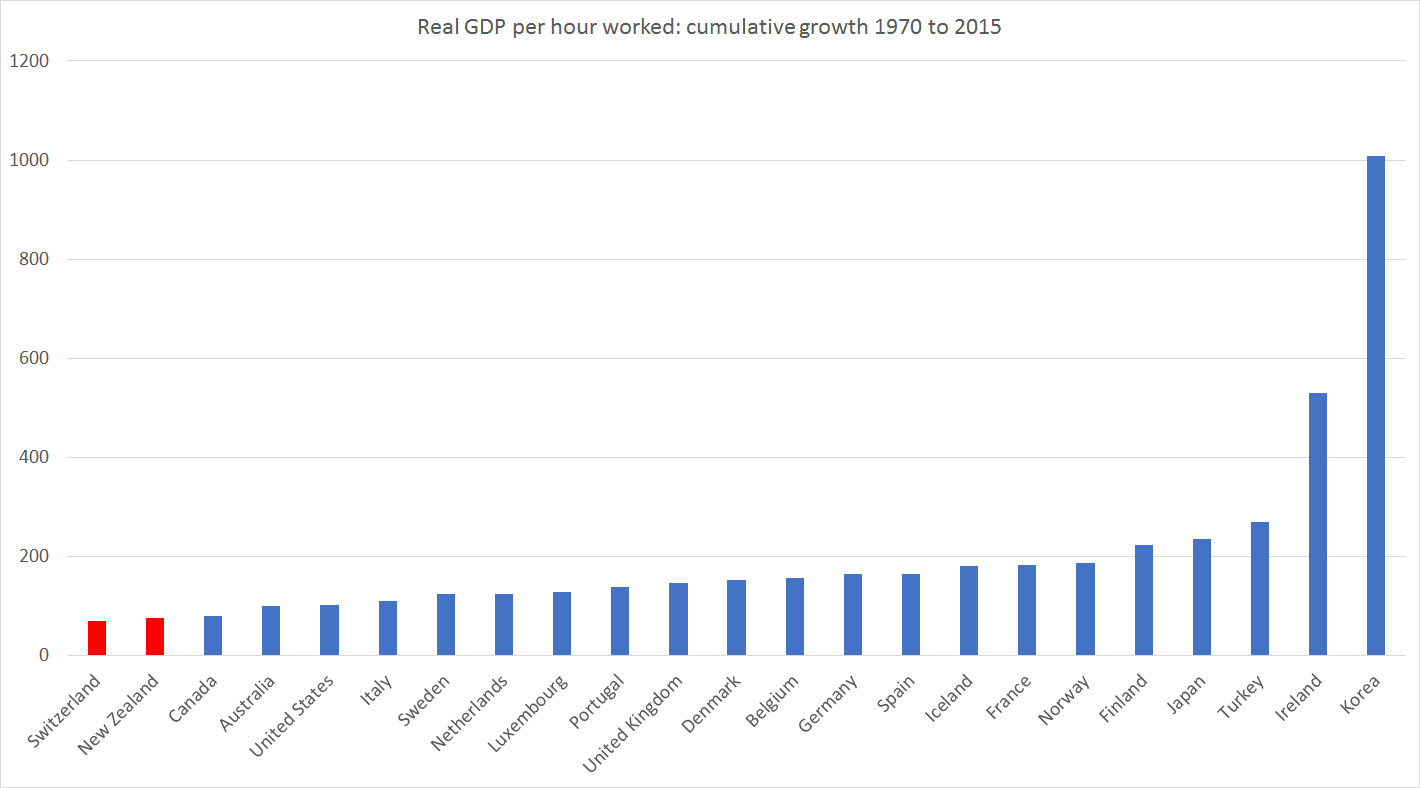

It is certainly true that Singapore and Taiwan have markedly lower rates of tax to GDP than New Zealand (or other advanced countries). On the other hand, OECD data for taxes and social security contributions as a share of GDP show that these days both Japan and Korea have about the same or higher tax shares than New Zealand does. Switzerland, Australia and the US are certainly lower than New Zealand, but then Canada is higher. And “Europe aside” does tend to rather overlook the fact that most of the world’s advanced economies are in Europe. (The Ireland line was fairly disreputable, it being well-understood that Ireland’s GDP numbers are seriously distorted by international tax factors. Using as a denominator the one the Irish authorities recommend (modified GNI), Ireland’s tax share is much the same as New Zealand’s).

I largely agree with their proposals around retirement income, and was surprised to realise that Kiwisaver subsidies now cost about $1 billion per annum. The text suggests that they envisage a pretty slow increase in the age of NZS eligibility, which does fit with what National is promising but should not be necessary in a first-best set of recommendations. Lift the age of eligibility by one quarter a year and it would be at 67 in eight years’ time.

There is quite a difference between suspending contributions to the New Zealand Superannuation Fund (the headline recommendation) and the alternative they moot in the fuller text of simply winding up the Fund. Do the former and Labour is likely to simply resume contributions again. There is no natural place for the government taking your money and mine (or, worse, borrowing it) to punt in international markets at our risk. The NZSF was initially designed for two things: to keep Michael Cullen’s colleagues’ spending sticky fingers off his early large surpluses, and to help buttress an NZS age of 65. We’ve not now had regular surpluses for a long time, and there is no good reason – with improvements in life expectancy – why the eligibility age for the universal state pension should be the same now as it was set at, for the then means-tested age pension, in 1898. NZSF should be wound up and the government’s gross debt substantially reduced.

The third bullet – comprehensive expenditure review – is fine, even admirable. But specifics, and willingness to actually cut, will matter. I like the idea of getting rid of interest-free student loans (my kids look at me reproachfully) but…..what hope?

I have long favoured a (small) Fiscal Council, or perhaps a slightly wider Macroeconomic Policy Council. This is a quite different thing than the policy costings office National, Labour and the Greens are all keen on (as a public subsidy to political parties). That said, if one were serious about austerity in the next term of government – and for my money the NZI doesn’t give sufficient weight to the scale of the fiscal challenge – I’m not sure I’d be treating new nice-to-have agencies (even very small ones) as any sort of priority. I’d rather focus on replacing the Secretary to the Treasury (whose term is up next year) and revitalising the analytical and advisory capabilities of The Treasury.

What of the monetary policy and Reserve Bank proposals. In several places, they overlap with ideas I’ve pushed here over the years.

I was in favour of something like the change to the statutory monetary policy mandate to the Reserve Bank, and am actually on record (in my submission to FEC in 2018) as having favoured going further. The change to the way the mandate was expressed was never envisaged as materially altering how monetary policy was run (from Robertson’s perspective it mostly seemed to be political product differentiation), and I don’t think there is any evidence it has actually done so. The Reserve Bank has made big mistakes in recent years but they have been analytical and forecasting mistakes, not things that can be sheeted home to the change in the way the mandate was expressed (here I imagine the Governor and I would be at one, although of course he’d be reluctant to get anywhere near the world “mistake”). All that said, since making the change made no substantive difference and was mostly about product differentiation, so would undoing it. We need real change at the Bank (and in how it is held to account) so I won’t argue strongly about symbolic change, a least if it markets/headlines real underlying change.

On the other hand, I have long favoured splitting up the Bank, and leaving a monetary policy and broader macro stability focused central bank, and then a New Zealand Prudential Regulatory Agency (probably comprising the regulatory functions of the Bank and much of the FMA’s responsibilities). That such a model would parallel the Australian system is not a conclusive argument on its own, but it is a real benefit when the biggest banking and insurance players in New Zealand are Australian-based. The Initiative argues that

Separating the functions into two organisations would improve governance and reduce the risk of political interference in the RBNZ’s core mission of price stability.

I agree (strongly) with the former. The current (reformed) Reserve Bank has a dogs’-breakfast of a governance model. I’m (much) less persuaded by the latter argument. I have seen no sign – in my time at the Bank or in recent years – of political interference in the operation of monetary policy. The mistakes have been Orr’s, and if there are valid criticisms of Robertson they are that he has showed little interest in doing anything about holding the Bank (and its key personnel) to account. Monetary policy and financial institution regulation are just two quite different functions, and need different skill-sets in CEOs. It isn’t impossible to make the current combined model work – though it would need big changes, including some legislative overhaul – but it simply isn’t the best model for New Zealand. (Such a reform would, done the right way, also render the Governor’s position redundant, with two new chief executive positions to fill.)

Should the Bank’s budget be cut? Yes, of course (and that comprehensive spending review shouldn’t overlook opportunities there), and since the NZI document was finalised we’ve seen an egregious increase in approved Bank spending without even the courtesy (or statutory obligation) to provide any documentation in support. But the budget is only one lever. As important will be finding expert people to lead the institution and monetary policy function who are really only interested, in their day job, in thinking about macroeconomics and doing and communicating monetary policy excellently, without fear, favour, or suspicion of either partisan allegiance or using a public role for private ideological purposes.

I have written here previously that I favour returning the inflation target to 0 to 2 per cent. That said, I don’t find the Initiative’s reasoning very persuasive

A lower target range would encourage the RBNZ to pursue more prudent monetary policies,

minimising the risk of excessive inflation and promoting sustainable economic growth.

But there is no evidence for these claims. Adrian Orr and his minions would have made more or less exactly the same forecasting mistakes in recent years with a target centred on 1 per cent as with the actual target centred on 2 per cent.

Perhaps more importantly, I don’t think the New Zealand Initiative team has ever taken sufficiently seriously the current (regulatorily-induced) effective lower bound on nominal interest rates. That constraint can and should be fixed but unless it is fixed it would be irresponsible to recommend lowering the inflation target.

On deposit insurance, I have long favoured deposit insurance, as a second-best way of reducing the scale and risk of government bailouts of banks (if no one is protected a failing big bank will almost certainly be bailed out, whereas with (retail) deposit insurance it is more credible to think that wholesale funders might be allowed to lose their money in a failure. That said, my argument was primarily about the big banks, and the deposit insurance regime will not cover only them. I do worry about heightened moral hazard risks around the small institutions. One could, I suppose, argue that capital ratios are now high enough there is very little risk of a large bank failing, to a point where it is credible that depositors could face material losses, but that argument cuts both ways in that with high capital ratios moral hazard risks are much smaller even in the present of deposit insurance.

The second to last item on the monetary policy list is a curious one. The Reserve Bank has run up losses of about $11 billion dollars through an LSAP conducted almost entirely in government bonds. So while I agree with limiting what NZ assets the Bank can buy, I don’t think it gets near the heart of the issue. New Zealand legislation is generally for too lax in allowing huge risks to be assumed with no parliamentary approval (whether the Minister of Finance issuing guarantees, for which there is no limit, or the Reserve Bank – which cannot default on its debts – buying risky assets. While there is a need for some crisis flexibility, the scale of the intervention undertaken (over more than a year) should not again be possible without parliamentary approval. That, incidentally, does not impair monetary policy operational autonomy both because the LSAP is a very weak (just risky) instrument and because (see above) the effective lower bound on the nominal OCR itself can and should be fixed.

I have no particular problem with something like the final item on the list, but as regards the LSAP expansion it would seem to be already there. The Bank’s holdings of government bonds are being slowly but steadily sold back to The Treasury (and others are maturing in RB hands). One can argue that the mix of sales might have been different or that the pace should have been (much) faster, but the domestic monetary policy bit of the balance sheet will shrink a lot. There are debates to be had about how much of an “abundant reserves” approach is taken in future – I’d probably favour not – and there are issues that should have had more scrutiny around increases in foreign reserves that the Minister has approved this year, but they are probably second order in nature.

With only 86 pages and lots of policy areas to get through, the NZI document was never going to cover all the significant issues in any subject area. I have quite a list of others, both as regards fiscal policy and around monetary and financial regulatory policy, but this post was about engaging the debate on the ideas NZI has proposed, not tackling all the ones they didn’t or didn’t have space for. Overall, I’m mostly sympathetic to the direction they suggest, but any incoming government actually interested in change should subject the specifics to some serious critical scrutiny.