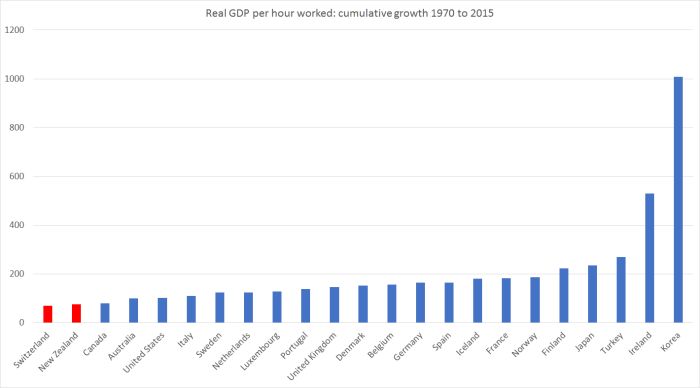

This coming Sunday, voters in Switzerland get to vote on the future monetary system. I don’t share the New Zealand Initiative’s enthusiasm for Switzerland – the only OECD country since 1970 to have had slower productivity growth even than New Zealand – but I do like the element of direct democracy in their system: binding referenda on matters initiated by citizens. No doubt it produces some silly results at times, but that’s part of democracy – not ideal, just better than the alternatives. And it isn’t as if our own system is immune to silly policies, unaccountable institutions etc.

I’d forgotten that the Vollgeld referendum was coming up until I saw yesterday that the eminent Financial Times economics columnist Martin Wolf was expressing the hope that the Swiss vote for change this Sunday. It isn’t clear that he really favours the general adoption of the specific system called for in the Swiss referendum but, in his words,

Finance needs change. For that, it needs experiments.

Dread word that: experiments. I remember the efforts we went to one year to get all uses of the word out of the OECD’s review of the New Zealand, in the midst of the reforms of the late 1980s and early 1990s. For better or worse, one can’t do randomised control trials in macroeconomics and monetary policy: “experiments”, if tried at all, have to be done on entire nations.

What are the Swiss being asked to vote on next week? The Vollgeld (“full money”) initiative is described by its proponents here, and described/analysed by a couple of independent Swiss economists here.

The key element of the proposal is this

The 100% reserves requirement means that all sight deposits in Swiss Francs (CHF) in Switzerland would have to be entirely kept as reserves in the Swiss National Bank. This implies that commercial banks would not be able anymore to use a fraction of these deposits to finance their lending activities, as they currently do. Swiss money would then entirely become “sovereign money”, controlled by the Swiss National Bank.

Proponents of the Vollgeld approach put a great deal of emphasis on something they label as “money”. As they note, the issuance of notes and coins is controlled by the state – even if in practice, supply simply respond to demand – and argue that the same should apply to other transactions balances (eg a traditional cheque account). Some seem to argue from a principled position that money creation is a natural business of the state, and thus direct control over the quantity of transactions balances created is simply a logical corollary. Of course, in New Zealand it was almost 80 years after the establishment of responsible government before the state here issued any payments media (coincidentally, but not inconsistently, we were the highest income country in the world through much of that period). Personally, I’d continue to mount an argument for removing the current state monopoly on the issue of bank notes.

Others focus on more pragmatic arguments around monetary and financial stability. If all demand deposits are fully backed by deposits at the central bank – or, at the limit, if all demand deposits were directly claims on the central bank – and were held on a separate balance sheet, there would be no more bank runs on demand deposits.

Ideas of this sort aren’t new. Proponents often hark back to the so-called Chicago Plan proposed by some prominent US economists in the 1930s, and at one stage in his career as orthodox a figure as Milton Friedman favoured 100 per cent reserve requirements for demand deposits.

But if the broad ideas aren’t new then, as the independent Swiss economists observe, runs on demand deposits also aren’t the main issue in real-world financial fragility. They put that down to the existence of deposit insurance – although Vollgeld advocates argue that under their system deposit insurance could be got rid of – but whatever the explanation

…the main source of fragility of modern banks is …..rather the wholesale short term debt issued by banks and held by professional investors, including other banks. These investors, who are not insured, may suddenly stop lending to a bank (this is called a wholesale run) if they suspect that the bank may have solvency problems. This wholesale short term debt is an important source of funding for the banks in the current system, but it is also a source of fragility, as the Global Financial Crisis of 2007-2009 has shown. The 100% reserves requirement would not apply to short term debt.

Wholesale funding markets seizing up was an issue even for Australasian banks in 2008/09.

Vollgeld advocates (at least those looking at the issue in detail) are aware of these other sort of “runs”, or market refusals to rollover funding at maturity, but don’t have a detailed response.

To tackle it, paragraph 2 of article 99a of the VGI mentions that the SNB would have the power to set a minimum duration for the debt issued by commercial banks. The VGI does not give much detail on this question, but it is clear that a new liquidity regulation would have to be introduced as a complement to the 100% reserve requirement. Indeed, financial stability can only be guaranteed in the Vollgeld system if the banks are strictly limited in their ability to issue wholesale short term debt as they do today.

I’ve long argued that the issue goes beyond even that. One could have all – or almost all – lending done by closed-end mutual funds (ie no early redemption at all, you just sell your claim on the open market) – something like the model favoured by prominent US economist Larry Kotlikoff – and there would still be financial crises, they would just take a different form. The nature of a market economy is that people get optimistic, and then over-optimistic, about particular industries, or the economy more generally. And then opinion changes – actual outcomes don’t quite meet expectations or whatever – and the flow of new investment, the flow of finance dries up. The dot-com boom, and subsequent bust, were good examples of that. So, in their way, were the Australasian post-deregulation booms and subsequent busts in the 1980s (they involved some bank failures late in the post-bust adjustment, but those failures were incidental).

And nothing in the Vollgeld proposals (or in similar Sovereign Money proposals in other countries, including New Zealand) deals with that. Nor does it really deal with the fact that many countries – including New Zealand and Australia and Canada – have gone for a very long time without bank failures (except in that brief post-deregulation transition period), and yet not been immune to recessions, periods of ill-judged investments, or prolonged booms or prolonged periods of underperformance.

Some advocates of reform put a great deal of emphasis on the alleged problem that lending simultaneously creates deposits, at a systemwide level. This is a feature not a bug. Lending transfers claims on resources from one person to another, and both sides of that need to be recorded – if I borrow to buy a house, the counterpart to that is that the seller of the house collects the proceeds of the sale. These people tend to confuse the position of an individual bank – for whom secure access to funding is absolutely critical – from the macroeconomics of the system as a whole. No (later troubled) New Zealand finance company – none of whom banked with the Reserve Bank – conjured its deposits out of nowhere: they first persuaded depositors and debenture holders to back their business model, and finance all manner of (often quite bad) projects. The finance companies didn’t fail because they had on-demand deposits (mostly they didn’t) but because they made really bad loans, and were part of the associated misallocation of real resources. Nothing in the Vollgeld initiative (or similar Sovereign Money proposals) seems to address that.

So why does someone as eminent as Martin Wolf encourage Swiss voters to vote for the Vollgeld initiative on Sunday? Mostly, it seems from reading his article, because he grossly exaggerates the real economic cost of financial crises, conflating the headline events (runs on banks, wholesale or otherwise, bailouts etc) with the correction for the misallocation of real resources that occurrred during the boom years and (in the case of 2008/09) treating all the slowdown in productivity growth as a consequence of “the financial crisis” when signs of it were already apparent before the crises. (I dealt with some of these issues in this post some time ago. ) Changing the rules around transactions balances just wouldn’t make that much difference. And although Martin Wolf and the Vollgeld advocates talk bravely of how such reforms might allow governments to more readily walk away from failing banks (ie the bits not offering transactions balances) at best that is aspirational. AIG and the federal agencies weren’t offering transactions balances – and were bailed – and even in New Zealand one of the key motivations for the OBR model isn’t about transactions balances, but about maintaining the credit process (all the information on firms that enables banks to continue to provide working capital finance with confidence).

Over the years, I’ve spent lots of time looking at various monetary reform proposals. When I was a young economist, Social Credit was still represented in the New Zealand Parliament, and their acolytes regularly wrote to the Governor and the Minister of Finance. Their ideas genuinely were wrongheaded and dangerous. In my experience, though, most such proposed reforms aren’t, and they often capture important elements of truth. But the proponents typically oversell the likely gains from what they are proposing. I don’t think the Vollgeld initiative model would be particularly damaging or costly – although there are a lot of details not spelled out, and the transition could be very unsettling (especially in a world of zero or negative interest rates) – but it just wouldn’t offer the gains the proponents claim. Monetary matters are rarely quite that important and in a market economy, human nature will have its head, and sometimes things will turn out badly. More often, of course, real financial crises reflect wrongheaded policy interventions that skewed choices and incentives and made the bad outcomes more likely (I’d include both the US crisis of 2008/09, and the Irish crisis in that category – and probably the Australasian and Nordic crises of the late 80s and early 90s).

In truth, calls for reform (from people like Wolf) and public support for ideas like the Vollgeld one (apparently perhaps 35 per cent of people may vote for it), probably stem more from some ill-defined sense that something is wrong (with economic and political outcomes). Banks and monetary systems are a convenient target – just like the idea here that somehow fixing monetary policy might make a material difference to our economic underperformance – but probably the wrong one.

Readers sometimes suggest that the Reserve Bank is reluctant to ever fully engage with alternative models. I’m not sure what they’ve been doing more recently, but when I was at the Bank I spent quite a bit of time over the years unpicking various proposals and trying to understand their strengths and weaknesses. It wasn’t always very systematic, and often depended on the interests of individuals, but I’d be surprised if the Bank is that much different now. We even used to send people along to debate some of those proposing alternative models. A speech I did along those lines is here. I’m not sure I’d stand by absolutely everything in it today, but we were an institution willing to engage.