It isn’t impossible that you, readers, are getting tired of the still-unfolding Orr/Quigley/Willis saga. You wouldn’t be alone in that. I have many more intrinsically interesting things to do (spent yesterday writing a review of new academic history of US banking supervision from 1798 to 1980, and am reading a history of little-known sovereign borrowing scandal from the early 19th century) but…..we are still short on answers and on accountability, notably from the Minister of Finance, who may have authorised but certainly enabled the systematic efforts led by Neil Quigley to mislead New Zealanders for months as to what went on. At any point, from and including 5 March (the day Orr’s resignation was announced) she could have a) insisted and b) personally ensured that the truth came out. She didn’t and still hasn’t given us a complete and straight story, or expressed any contrition for anything she was party to in the last six months. Deliberate efforts by, and enabled by, a senior minister to mislead New Zealanders would once, and once brought to light, have been treated as a very serious offence (but then, as I noted here repeatedly, MPs never seemed very bothered when Orr made a mockery of their place in the system and actively misled – or worse – them repeatedly). The rot runs quite deep.

Yesterday saw another OIA response from the Reserve Bank dribble in, and with it one more snippet of information. It exposed, once again, my tendency to look for the least-worst explanation, which has been quite unhelpful in making sense of the mess of recent months.

A couple of weeks ago, the Reserve Bank released to me a Letter of Expectations that the Minister of Finance had sent to the chair of the Bank’s board (Quigley) last year, outlining how the Minister expected that the Board would approach bidding for and negotiations on the next (2025-30) Funding Agreement. The Reserve Bank has a website page where it publishes ministerial letters of expectations. They simply never published this particular letter of expectation on that page, or on the website page gathering together material on the 2025-30 Funding Agreement. Par for the course you might reasonably think, given how obstructive and then slow and partial the Bank has been.

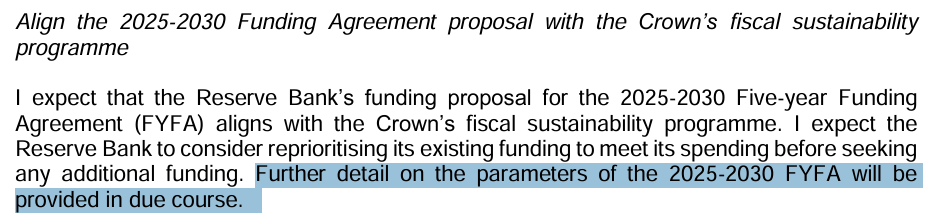

As I noted in that post a couple of weeks ago, the Funding Agreement letter of expectation had made it clear that the Minister was looking for cuts. This was the relevant snippet.

But the version of the letter the Bank was released was undated. The Bank had been quite open about the general 2024 Letter of Expectation, which was dated 3 April 2024. It was fine, but fairly general, noting that further detail relating to the next funding agreement would be coming “in due course”.

I guess I had in mind that perhaps that letter hadn’t been written until much later. After all, the existing Funding Agreement didn’t expire until 30 June 2025 (and when Treasury actually got the Bank’s bid in September 2024, the papers suggest they did nothing with it for months anyway, considering it mainly in the context of this year’s wider government budget)

But what the Bank disclosed to me yesterday was that the funding agreement letter of expectation had also been received by the board chair on 3 April 2024.

And that matters because it was well before the Reserve Bank board made final decisions about the Bank’s 2024/25 budget. Quite possibly, the Governor was already encouraging the Board to agree to a grand spend-up in 2024/25 anyway – on the dubiously legal, but morally outrageous, basis that their total spending over the five years of the 2020-25 Funding Agreement would still be under the total allowed spending in that term (even though a) the agreement and Act specifically referred to individual year limits, b) the limits for each of the last two years had been reset by Grant Robertson just before the 2023 election, and c) there was a wider climate of spending restraint being driven by the Minister of Finance). Perhaps he already planned that such a spend-up would lock in a level of spending/staffing that might make it hard for the Minister to cut much when the new Funding Agreement was finally determined.

But, on 3 April 2024, he had the Minister’s own words for an interpretation that a Funding Agreement bid would be okay if it involved a 7.5 per cent cut relative to the Bank’s budget for 24/25. Wherever that budget happened to be set, apparently. Talk about dangerous incentives….in a system where the Bank sets its own budget, not directly constrained by (eg) parliamentary appropriations…..and the board signed up to this and went along, setting a budget for 24/25 about 23 per cent above what the Robertson Funding Agreement variation had allowed for that year, and then pitching a new Funding Agreement bid just 7.5 per cent below that level (and far above what even Grant Robertson had approved for 24/25). It was a try-on that really amounted to spitting in the face of the Minister, operating in total disregard to the times (let alone to the wellbeing of the staff, if the double or quits gamble went wrong, as eventually it did).

It is breathtaking all round. The Governor and Board attempted to drive a cart and horses through dangerously loose wording. Neither the Treasury nor the Minister of Finance seem to have had the measure of the people they were dealing with, and both were so asleep at the wheel that (a) when the Bank came back with a draft Statement of Performance Expectations in late April 2024 that deliberately left the budget numbers blank, neither followed this up and insisted on straight answers, and b) when the inflated Funding Agreement bid came in a few months later they sat on it for months and did nothing. No one was dismissed, no one was even severely wrapped over the knuckles. A senior political journalist told me last week that in an interview on 30 October the Minister had, unprompted, indicated that she was going to cut Reserve Bank spending……but she’d done absolutely nothing as the board had run rampant for months, including staff numbers still growing markedly. It wouldn’t be until mid-February that things would finally come to a head. As any parent knows the time to deal with bad behaviour is firmly and early, not leaving the offender with the implicit message that Mum and Dad don’t care too much, only to make a fuss belatedly.

Realising that this Funding Agreement letter of expectation had been received as early as 3 April prompted me to dig out the published minutes of Board meetings from the March and June quarter of last year (from which we are told nothing has been withheld) and the Board chair’s response to the (general) 2024 Letter of Expectations (for some mysterious reason known as the Strategic Issues Letter).

Rereading those documents in the light of what we now know, it is interesting how early both the Bank and Treasury had started work on the next Funding Agreement issues (the February 2024 minutes record that a very senior Treasury official – deputy secretary Leilani Frew, now departed – had been named as relationship manager for the funding agrement process, and the board had approved a memo to Treasury “to establish and agree foundational interpretations relating to the funding agreement and the principles underlying our approach to setting our baseline expenditure forecast”). The May Board minutes record Frew and the macro deputy secretary visiting the board and noted that ‘the work towards the next funding agreement, noting that there has been constructive engagement between RBNZ and Treasury an that baseline savings are in the process of being identified” (but presumably neither Frew nor Board, nor their staff, asked the questions that would have revealed the spending spree the Bank was just about to go on with the draft 24/25 budget – the immediately previous item on the Board’s agenda).

You might have supposed that having (a) had two letters of expectation from the (new) Minister of Finance on 3 April, and b) having a deadline to submit to the (new) Minister of Finance, just about to bring down her first government budget in straitened fiscal times, for consultation/comment a draft Statement of Performance Expectations (including budget numbers) by the end of April, that these sets of documents would be the subject of serious discussion by the Board at its April meeting.

But the Board didn’t meet in April 2024 at all. Now, the March minutes record that there was an (unminuted) “workshop” on 23 April “to discuss the next iteration” of the Statement of Performance Expectations and Statement of Intent Refresh, but those minutes also just delegated to the Governor and chair the authority to sign out to MoF for consultation the draft SPE at the end of April. As it happens, the document was signed out by neither, but by one of Orr’s many deputies. Was the Board aware they weren’t planning to tell the Minister about the planned size of the 24/25 Budget? We don’t know, and the (published records) conveniently don’t show. Did they engage with the two letters of expectation then? We don’t know.

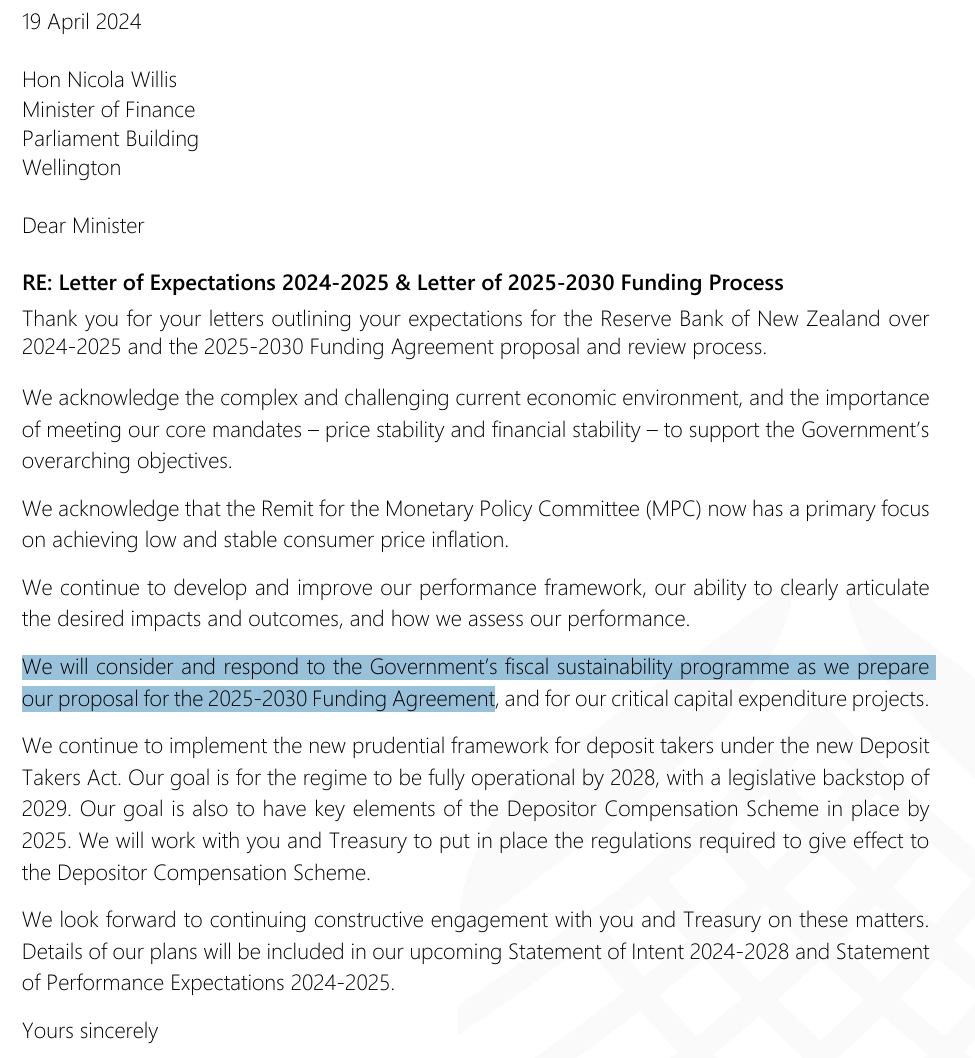

But it seems unlikely, because even if it came up at the 23 April workshop, Quigley had already sent his Strategic Issues Letter back to the Minister on 19 April, purporting to respond to both letters.

Note that he avoided the specifics from the Minister’s letter on the next Funding Agreement and gave only the vaguest indication of a more general approach (“we will consider and respond to”). Surely Treasury (Frew) and the Minister and her advisers should have been put on notice when they got such a vague response? But apparently not, given that they raised no questions/concerns when the budget numbers weren’t included when the draft Statement of Performance Expectations was sent in 10 days later?

There is no suggestion in any of the June quarter minutes from 2024 that the Board ever discussed the Letters of Expectations or thought hard about the implications, or the environment against which they were written. The May minutes do mention the Strategic Issues Letter but only “The Board noted the Strategic Issues Letter”. They seem to have been out on another planet, perhaps led by the nose by Orr, but with no one – Board, Treasury, Minister – providing the sustained vigilance (protecting the public interest and public purse) that was needed. The only Board questions noted in the minutes were looking for assurance that the 24/25 budget was going to be legal – and perhaps Orr’s tame in-house provided some such dubious assurance, as lawyers (in-house and external) are so ready to do for clients – but with not even a hint of a question as to whether such a Funding Agreement blowing budget was right or responsible or was likely to prove sustainable, no stress testing (for example) of what the implications (for people and for the organisation) might be if they did later hit a wall.

It really astonishing (or perhaps not; this is modern NZ) how little serious accountability there is in New Zealand public life. Of course, Orr has gone, but not because of anything he was doing mid-late last year, and Quigley eventually went too – again not because of what he led and did last year but because eventually the post-Orr coverup got a bit embarrassing. I guess too that the relevant Treasury Deputy Secretary has moved on, although there is no hint of that having anything to with being asleep at the (leadership) wheel when the egregious foundations were being laid for the Feb/Mar blowup this year. No board member has been dismissed, or as we understand it even reprimanded, and one was even reappointed this year. The board deputy chair – fully party to last year’s decisions – is holding the fort post-Quigley.

And then there is the Minister of Finance. By far her worst offence was enabling the deliberate deception of New Zealanders for months, when she could have cleared things up at any time she choice (Quigley may have become a nuisance to her, but he was her man, she empowered and enabled him). She still hasn’t been fully straight with New Zealanders. But her role last year – both directly, and in insisting on a more active engaged performance from Treasury – looks pretty culpable. Perhaps if she’d taken a stronger stance from when she first took office, Orr and Quigley would have been reined in much earlier, and the chaos and dishonesty of this year – and damage to her own standing (and the disruption of staff lives) – might have been avoided (many of us were probably glad to see Orr gone in the abstract, but…..no one wanted this).

Remarkably, one other snippet in the May 2024 board minutes is a brief note “the Board discussed the chair’s first meeting with the Minister of Finance”. The government had been sworn in on 27 November 2023, the Minister had been on record with her concerns about Orr personally, and Bank bloat, she’d even promised an independent review of monetary policy. She knew the Funding Agreement had a year to run, but was insisting on immediate cuts elsewhere. It was hardly a quiet and easy corner of her domains and yet she seems not to have bothered meeting with the board chair – her agent, and board wielded the power on prudential policy, where she also had concerns – for months after taking office. You can only shake your head and wonder what she was thinking, and why she made so little effort for so long to use the tools – formal and informal – at her disposal.

You are correct , I am over this topic.

It has removed Ms Willis from my very short list of persons suitable to replace Luxton.

I am surprised at your surprise at finding our politicians capable of such behaviour.

Keith

LikeLike

Naive optimism has long tended to be a weakness!

LikeLike

It can only be assumed, as you intimate, that there were conversations about how to circumvent the intent of what the Minister and Government were seeking. The ramp-up in spending and deceitful positioning of a “cut” had to have been both discussed and signed off by the Board. They are not stupid people and cannot have been misled by Orr. They are explicitly complicit.

LikeLike

Don’t be discouraged Michael. I am sure you had no idea how this saga would drag on, and as it did, you deserve out gratitude for not simply giving up and sighing that…”This seems to be the NZ way.”

One might say that it is a common human foible to avoid anything unpleasant. I am sure if almost any major financial ‘process’ was to be investigated in detail,…eg the Fletcher boardroom,…the Cook Strait Ferry saga,…one would find that those involved avoided confrontation, accountability, etc., and simply moved on with perhaps an unspoken vow to never deal with certain individuals ever again.

But your investigation, no witch hunt, simply looking at the reality, will hopefully bring some change. Perhaps Parliamentary reviews might become more muscular. Perhaps Ministers might become more specific, and follow up, regarding their expectations of the Civil Service.

Yes pigs might fly, but nevertheless thanks for staying the distance.

LikeLiked by 1 person

Thanks. As it happens, and looking through old emails the other day, I didn’t even lodge a first OIA until about 6 weeks after the announcement resignation. I guess I just assumed he’d got tired and frustrated and had gone. It was only as some media OIAs started to be reported that it became apparent that there was prob more to the story.

LikeLike

Appreciate your efforts…. Gaining a full scenario now

LikeLike

This latest revelation adds another frustrating layer to the saga. What stands out most is the lack of timely accountability, both from the Board and the Minister.

LikeLike