It is almost never an (unconditionally) good thing if an official policy interest rate (in our case the OCR) is being adjusted in large bites, whether that is (for example) 175 basis points of cuts in the last six months or 375 basis points of increases in just twelve months a couple of years back. One can think of rather hypothetical exceptions: a civil war ends and the reckless central bankers who financed it are suddenly sent on their way (so actual and neutral rates fall a lot), or a bold reforming government takes office with an immediate policy programme likely to dramatically lift potential growth, and involving lots of new investment (pressure on resources) in the transition (so actual and neutral rates rise a lot). But that isn’t the story of New Zealand in the last few years (or any of our advanced country peers). Really big changes in official interest rates are usually a reflection of bad stuff having happened: that might be a really nasty external shock (as in late 2008) or past mistakes by the central bankers responsible.

But of course you get no hint of this from the Governor speaking for the MPC. The general gist I’ve seen in headlines reporting his comments in the last 24 hours is to talk things up. Rather than watch the Governor’s FEC appearance I went for a walk this morning, but as I was walking I happened to note this

It might be necessary at this point (almost certainly was) but it isn’t an unconditionally good thing, and it would be good if he (and the political cheerleaders trying to muscle in and claim credit – Luxon, Willis, Seymour) showed even some sign of recognising it. But I guess contrition is a bygone word. (Opposition political parties tend to use the point – big cuts generally mean something bad happened – only to switch rhetoric when they in turn hold office.)

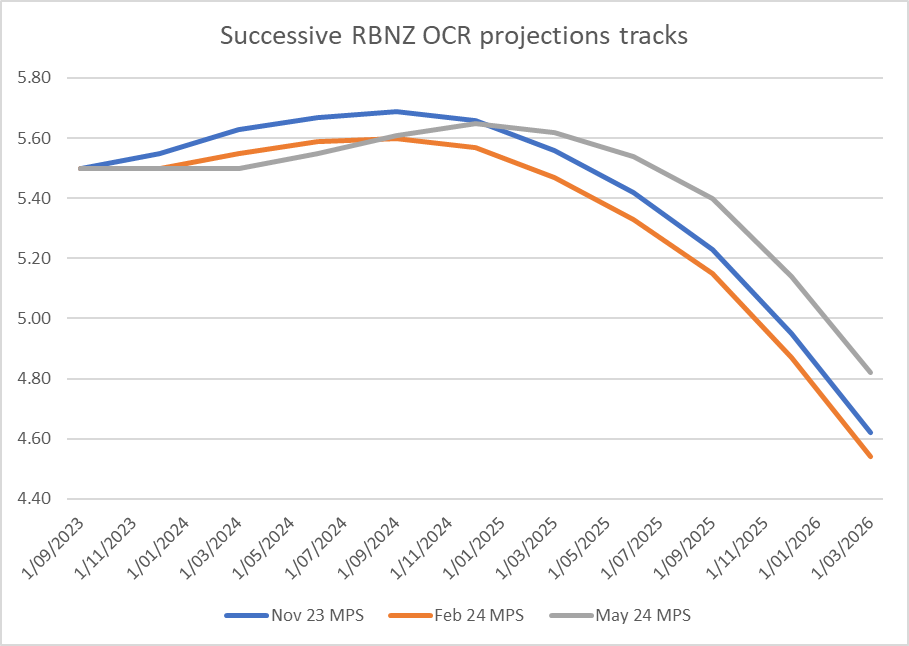

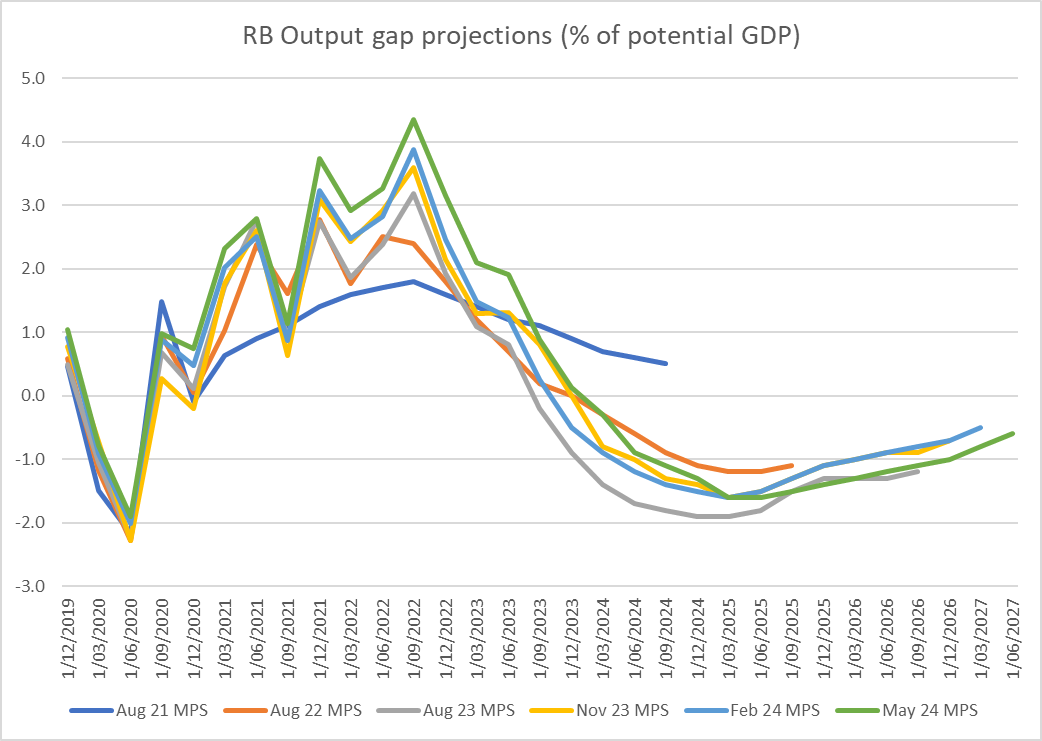

In truth, the Reserve Bank and its MPC really does not know what it is doing. Their own successive forecasts show it. In this chart I’ve taken their projections for the OCR in the June quarter of 2025 for each of the last five MPSs. Only 9 months ago they thought the OCR in the June quarter would average more than 200 basis points higher than they now think.

That might be pardonable if some really big external shock had hit the New Zealand economy. But there hasn’t been any such shock. Commodity prices haven’t plummeted, fiscal policy hasn’t suddenly tightened, no financial crisis has broken upon us

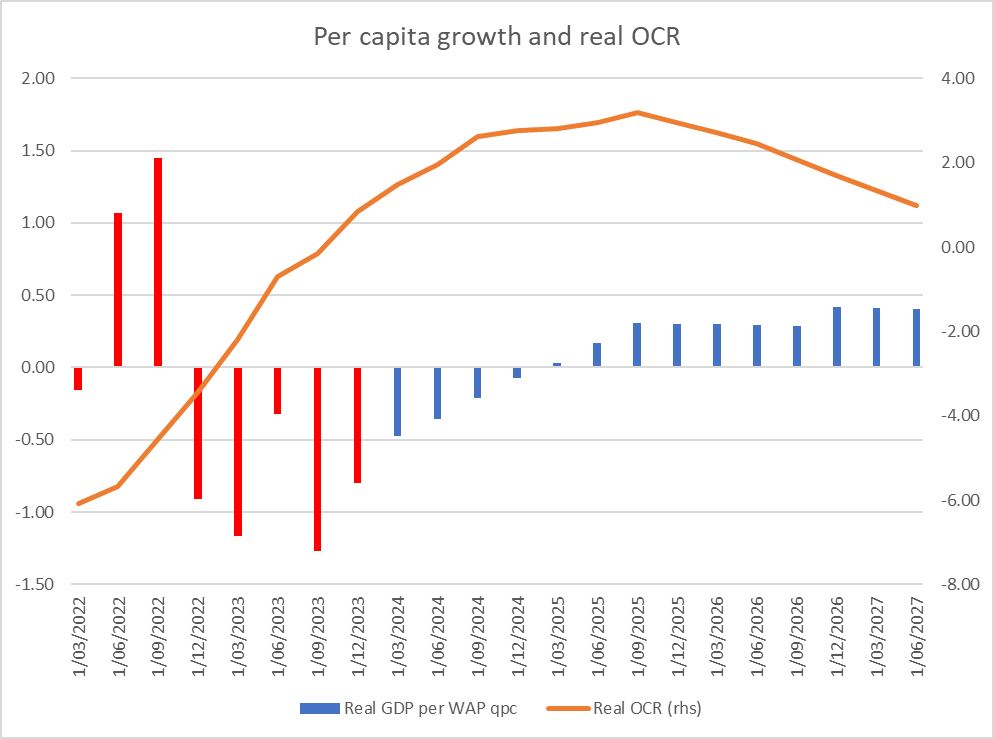

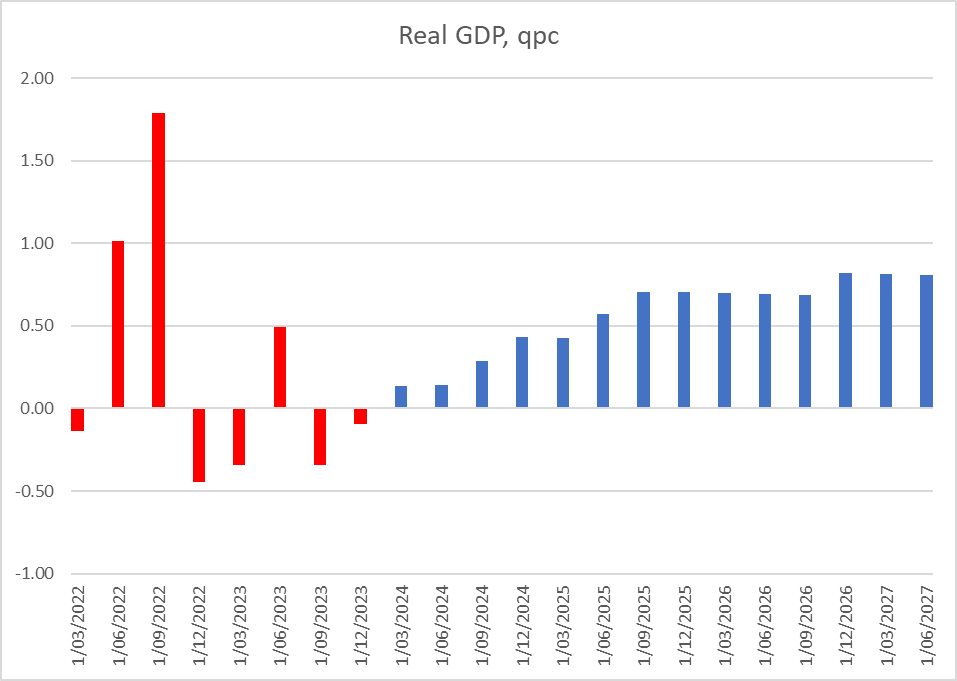

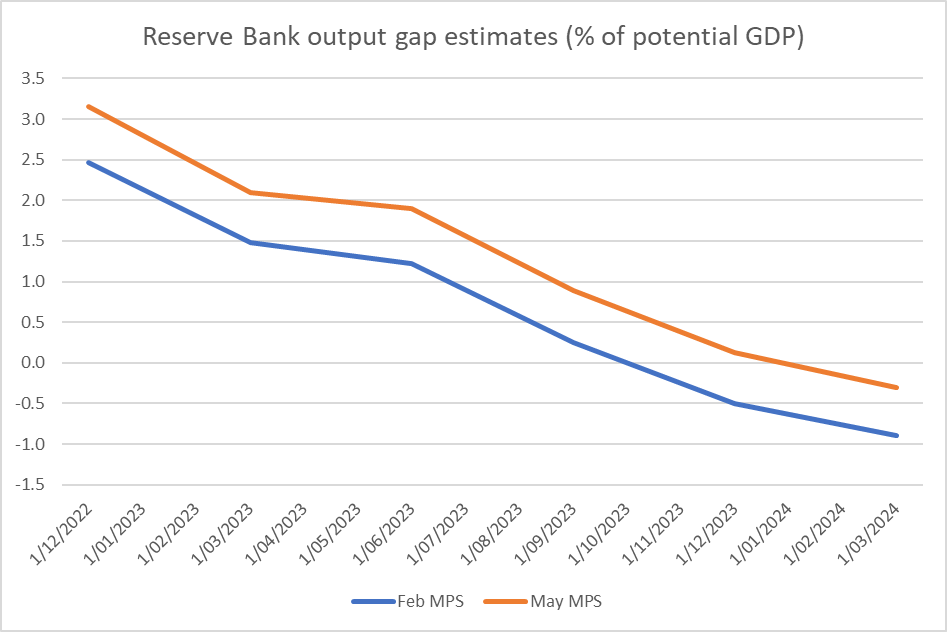

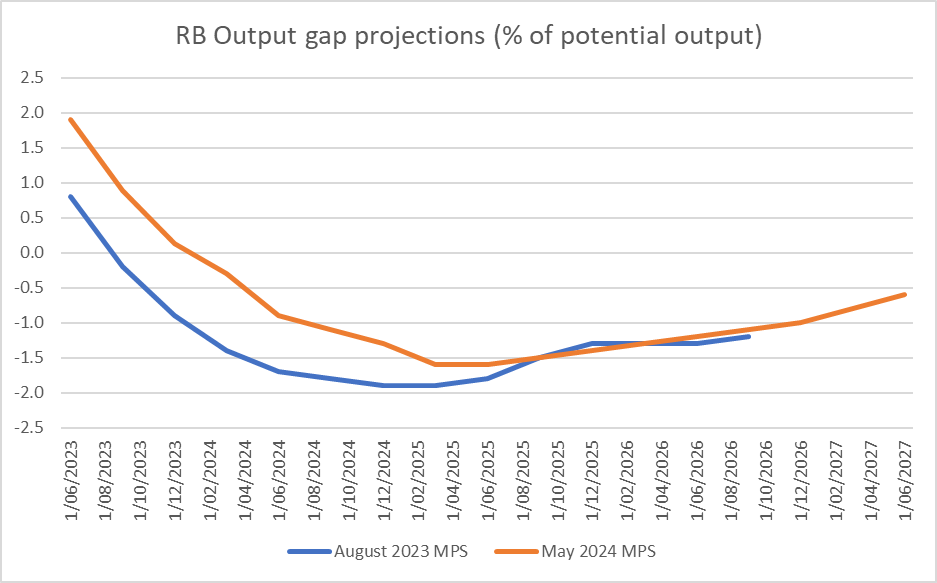

The MPC’s output gap estimates for around now have bobbled around a little, but haven’t really changed a lot (and recall that monetary policy works with a lag, so for example the December data – the GDP input for which we finally get next month – won’t have been materially affected by OCR cuts late last year).

The MPC might respond – if they ever engaged – that perhaps they haven’t usually been much worse than the typical market forecaster. But we – citizens – don’t employ those forecasters, while we delegate a great deal of power and prestige to this supposedly expert committee.

They might also argue that they are doing their best. No doubt, but their best isn’t very good. And what that means is that we are still in a phase – as we have been for the last five years – where neither we nor they can have any confidence whatever in their numbers or statements about what comes next or where the OCR might be at, say, the end of the year. After all, that is 10 months away, and 10 months ago they thought the OCR now would be 5.6 per cent. They simply do not have a good understanding of the inflation process – a big part of the job they are charged with doing. Perhaps we’ll still be at 3.75 per cent, or perhaps we’ll be at 2 per cent: neither seems that implausible, given how inadequate the understanding of the inflation process has been, even without really big external shocks.

Which brings me to some more mundane observations and puzzles around the numbers they did produce in yesterday’s statement.

The big one relates to the fact that, on the Bank’s own telling, the OCR is above its best estimate of neutral now and never drops below neutral (the Bank’s current estimate is 2.9 per cent, while the OCR doesn’t drop below 3.1 per cent). And the current (negative) output gap is estimated (by the Bank) to be about 1.5 per cent of GDP (and the unemployment rate, picked to peak about now at 5.2 per cent, is also well above the Bank’s estimate of a NAIRU). And yet, as if by magic – because there is no visible explanation – quarterly GDP growth is expected to bounce back almost immediately to well above potential, and the unemployment and output gaps close over the next couple of years. But how (on the Bank’s numbers)? When one gets into an economic slump (material negative output gaps), it is normal for policy rates to undershoot neutral for a while to provide the impetus to get the economy back on course (and avoid inflation undershooting). The current slump (negative output gap) isn’t as deep as in, say, 2009, but it isn’t nothing either.

But then there is the other puzzle. Why isn’t inflation falling further (on the Bank’s numbers)? The Bank doesn’t help people trying to make sense of their inflation projections because (a) they don’t publish projections for core inflation (quite a major gap now), and b) they don’t publish their inflation projections in seasonally adjusted terms. But when the output gap is forecast to be negative for the next couple of years (and materially so this year), surely we should be expecting to see inflation fall further. But it doesn’t seem to.

Non-tradables is not core inflation, but it is the best they provide (bearing in mind that non-tradables historically averages well above headline, and so isn’t expected to settle anywhere near 2 per cent per annum). Their non-tradables forecasts for 2025 are already as low as they are ever thought likely to get.

I can do same sort of chart for their LCI wage inflation forecasts. The trough is already reached in the June quarter this year (just a few weeks away) with the unemployment rate still above 5 per cent.

It doesn’t seem to hang together very well as a story.

There aren’t many interesting charts in the MPS itself, but this one caught my eye.

It is based on a working paper that hasn’t yet been published (less than ideal) but seems to show that the bits of non-tradables inflation that are most responsive to monetary policy pressure have already fallen too or below the rates of inflation experience during the pre-Covid decade, where core inflation quite materially undershot the midpoint of the target range, that the MPC is required to focus on. It isn’t an ideal chart, including because it doesn’t show the earlier period when core inflation got beyond the top of the target range, but – given that the latest (Dec) outcomes will have been driven by the OCR at 5.5 per cent, and that (as above) the OCR never gets below neutral, you’d have to think it likely to more disinflation was already in the works, including with the OCR now at 3.75 per cent.

Perhaps there are good answers, but if so (a) they aren’t in the MPS, and b) the MPC members never give speeches or serious searching interviews.

I have noticed that the Bank has consistently been forecasting a large rise in the terms of trade – for reasons that elude me – and perhaps that is some part of a story, but surely any effects of even that puzzling projected rise are already included in those (disinflationary) output gap, unemployment gap, and OCR gap numbers?

Two final thoughts.

When the MPC was established six years ago, the hope – and perhaps promise – was that we would have better quality decision-making and more transparency and accountability. Sadly, any such suggestions have quickly turned to dust, whether under Grant Robertson as Minister of Finance or, more recently, Nicola Willis. The quality of the external members has improved a little over the last year, with two new appointments by this government, although one elderly retired academic who served on the committee from the start (through all the costly mistakes of 2020 to 2022) has recently been extended again by the Minister of Finance. But we hear nothing from any of these people, whether in speeches, interviews, testimony to Parliament’s FEC. Or the minutes of the MPC meetings (the Summary Record of Meeting, which takes up the first three pages of the MPS). These documents have become utterly pedestrian and largely repetitive of material elsewhere in the document. And perhaps more to the point, there is rarely if ever any sense of divergences of view or serious explorations of alternatives, this around subject matter where (see above) the consensus view has so often been so wrong in recent years. Here is the final page of yesterday’s Summary Record of Meeting, where there is just nothing suggested any sort of range of views.

One hears on the grapevine suggestions that the MPC does in fact sometimes have robust debates. Perhaps, but they give no hint of this – in a field that everyone knows is characterised by huge uncertainty, and where challenge and contest of ideas and evidence is vital – and there is no serious accountability. One can only hope that one day, perhaps looking to the end of the Governor’s final term (in March 2028) the Minister of Finance might seek some advice from The Treasury on how to finish the work that Grant Robertson began, but let run off the rails. Some of these people might be uncomfortable about having to front up with their views and analysis, or having to account for their judgements, but – academic or otherwise – if that is so they simply aren’t the right people for such powerful policymaking positions.

And finally, someone reminded me yesterday that the Reserve Bank is holding a closed-door conference in a couple of weeks to mark 35 years since the Reserve Bank Act of 1989 came into effect, and inflation targeting in New Zealand – pioneering as it was – took formal legal effect. They look to have a couple of good keynote speakers (Ben Bernanke, and Bank of England MPC member Catherine Mann – whose BOE speeches are always worth reading, even if her contribution (in a former role) to debate on New Zealand productivity and immigration a few years ago was spectacularly bad). I’m sure the select invitees will enjoy a good time and some expensive hospitality.

The Reserve Bank says that the aim is as follows

One hopes then this will include serious and self-critical reflections on how the last few years came to happen. The promise of inflation targeting was that serious outbreaks of core inflation – and aassociated real unexpected redistributions of wealth, and nasty adjustments to get things back under control – simply would not happen again. And yet they have. Much of the promise in the New Zealand context was that in exchange for delegating huge power to the Reserve Bank, we’d see serious accountability when mistakes were made – and yet, as far as I can see, no central banker anywhere has paid a price for the mistakes of recent years. Or perhaps they may reflect on the not-so-small matter of the massive financial losses central bankers here and abroad ran up on the taxpayers’ bill over the last few years. But – based on the approach of our own Governor, MPC and ministers in recent years – probably not. I’m certainly still in the camp that sees inflation targeting as better than the alternatives – at the 25th anniversary conference I offered some thoughts on why nominal GDP targeting didn’t seem a better choice for New Zealand, in 1989 or more recently – but I’m much less convinced than I was decades ago that delegating the power to central bank Governors or MPCs makes sense. We need expert advisers, but accountability for central bankers has proved so elusive we might be better off putting the decisionmaking back with the people we can toss out, the politicians.

PS: I also saw this comment, presumably from the Governor’s FEC appearance. If this means an end to the long summer holidays and a return to eight meetings a year then it would be most welcome.