Over the last couple of years I’ve commented at various times on (a) the loss of experienced research staff (b) the rapid turnover of senior managers, and (c) the bloated number of (very highly paid) new senior managers at the Reserve Bank.

I haven’t paid overly much attention to the overall staff turnover data. And it turns out that was probably just as well.

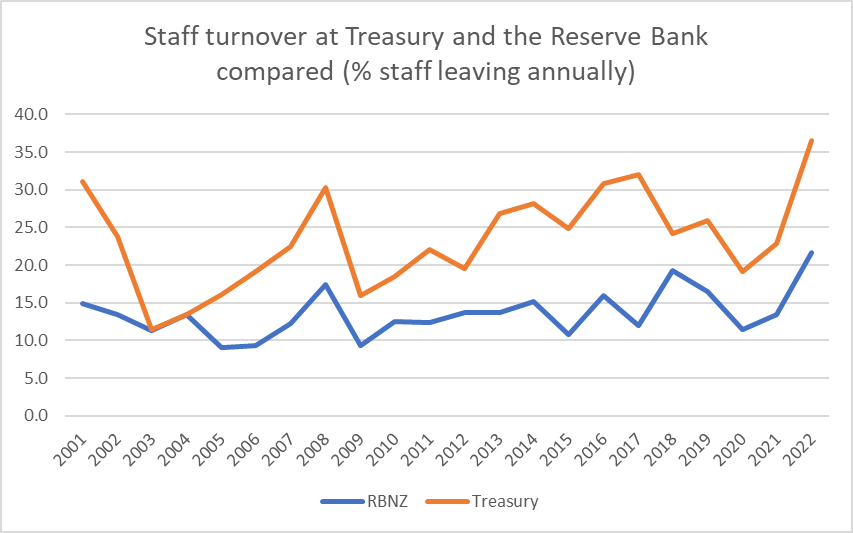

Here is a chart of annual staff turnover rates for the Bank this century. There has been a sharp increase in the last year (to June 2022).

But Simon Chapple, at Victoria University’s Institute for Governance and Policy Studies, went to the effort of digging out the same data for the Bank and a bunch of other public sector agencies, and kindly sent me a copy of his spreadsheet.

Of all the other public sector agencies, perhaps the best comparator is The Treasury. They are very different agencies but have often been bracketed together.

There is a lot more variability in the Treasury series, but (a) it has been higher or no lower than the Bank every year this century, and (b) over the last year has had an absolutely staggering 36.5 per cent turnover rate. It was bringing to mind the stories from 35 years ago when at one point (and if I recall correctly) the median length of service at The Treasury was under two years.

Here is the data for three other agencies: the (public service) Department of Prime Minister and Cabinet, the Public Service Commission (previously SSC), and Statistics New Zealand.

I suspect the DPMC figures can be discounted, as DPMC built up a huge temporary operation to co-ordinate the Covid response (including lots of comms staff for all those adverts), but in the most recent year even SNZ had slightly higher staff turnover than the Reserve Bank. (For the public service as a whole – not shown – the staff turnover rate was exactly the same as at the Reserve Bank.)

Over the last year or so, presumably two – mutually reinforcing – influences have been at work. First, the economy has been materially overheated reflected, among other places, in an extremely tight labour market. When the opportunities are good and finding new jobs is easy a given person is more likely to move in any particular year. And the second is the rather arbitrary block on wage increases for many public servants. All else equal, not only has that made moving to the private sector relatively more attractive – private sector wage increases have run well ahead of public sector ones – but has also created the readily-visible bizarre incentive that the only way many public servants can get a pay rise is to change jobs (whether to other positions in the private sector or elsewhere in the public sector), perhaps with some grade inflation thrown in (people who aren’t really senior or principal analyst material getting given those titles and salaries). Moving simply because it is the only way to get a pay rise – in a generally overheated labour market – makes sense for the individual, but almost certainly does not for the public sector as a whole.

(And here I am not entering into questions of whether public sector salaries are generally too high (or not) or the size of the public sector: issues for other people on another day.)

Zero staff turnover would generally not be desirable. When I used to pay more attention to these things at the Bank we used to be told that for established well-run professional organisations a 10-15 per cent annual turnover rate was fairly normal (perhaps coincidentally that was the rate the Bank tended to have). I find it harder to believe that 25-30 per cent annual turnover rates – as at The Treasury – is entirely healthy, no matter how much you might encourage rotation, fresh opportunities etc. But one would have to hope that the 2022 turnover rates for all these public sector agencies prove to be peaks, and that by the 2023 and (especially) 2024 annual reports, staff turnover has settled back to much more normal levels for organisations of this sort. Whatever your view of the appropriate size of government, what agencies we do need need capable and experienced staff.

Good post Michael.

The significance of turnover is the impact it has on productivity and the increase to overheads (principally for training).

In professional organisations (and more so if they have a high technical content in the work) up to 10% of their working capacity may be lost to annual training to maintain competence in the profession.

As a rule of thumb, productivity of new recruits in any professional organisation is low in the first year as they are “learning the ropes” and it’s only in the second year that they become fully productive. As turnover rates increase, proportionately more of the productive capacity of the organisation is lost to the training overhead. At 50% turnover the organisation is operating at less than half its potential performance capability. What this means in the public service is a higher cost to the taxpayer from unnecessarily high turnover.

As capacity declines there is also greater tendency to push work out to consultants or contractors, and correspondingly greater incentives for staff to work in those organisations, further increasing the costs to the taxpayer. That also comes with the need to recruit or contract more communications staff – telling and selling stories to substitute belief and hope for the realities of substandard performance.

Interesting to note in the SSC numbers the rise post GFC coinciding with the rise of the “woke” and “progressive” movements and their influence.

The ideal of a dedicated and loyal career public servant whose duty of service is to principles of public and institutional interests rather than the fancies and stories of the government of the day appears sadly to be consigned to that of a quaint historical notion. We are paying for the change.

LikeLike

The Treasury turnover isn’t surprising given their performance. Tsy was one of the worst scoring agencies in the NZIER review of policy advice quality. A correlation perhaps?

LikeLike

Did this reflect a new boss at all?

LikeLike

Possibly, but more likely a result of Maklouf running the place into the ground

LikeLike

As with a lot of organizations, there were those that refused (rightly as it turned out), to be vaxed and therefore were essentially constructively dismissed.

The shame was that some of the useless at the top never went. Didn’t have the courage to defend their own life.

LikeLike

Aren’t typos a pain? I am sure you meant “wrongly” rather than “rightly”.

https://www.cidrap.umn.edu/covid-19-vaccines-saved-estimated-20-million-lives-1-year

In any case, with a research focused organisation like the RBNZ, it is not unusual for recent graduates to come for a short time, get experience and build resumes before heading off for the private sector, or further graduate education. Not to mention fixed term staff secondments from other countries.

So the staff churn may all be at the entry level and there may well be reasonable longevity/experience at senior levels even with a highish staff turnover rate.

LikeLike

The high turnover likely due to implementation of a QE strategy that no one at the RBNZ actually understood. Looks to me more like a sacking or forced resignation for a bumbling attempt at QE that left Grant Robertson out of pocket by the 2nd round of lockdowns. NZ QE started at $100billion, stopped at $59billion and accidently repaid reducing actual QE to only $27billion.

That bumbling QE attempt actually turned out to be accidently the correct future strategy. It has certainly given the RBNZ much more flexibility with interest rate rises than the RBA that is now having to deal with a $800billion Australian QE on the books. I hope we all do realise by now that the Cash Settlement Account is a liability account ie RBNZ still owes the banks $27 billion for buying $59 Billion of NZ banks NZ treasury bond holdings. It also looks like the Govt bought out Kiwibank shareholders Kiwisaver and NZ Super by utilising the RBNZ cash settlement account. Anyone worked out how the transaction occurred? It sure looks like the RBNZ Balance Sheet has been used for that purpose?

LikeLike