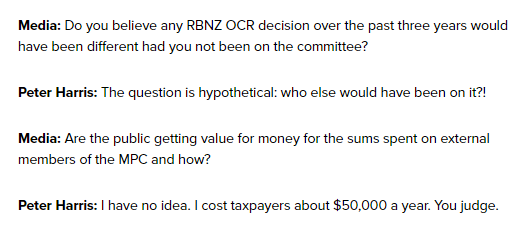

A consistent theme of this blog over the 3.5 years since the Monetary Policy Committee was established has been the severe inadequacies in the way the MPC was designed, and in the way it has been staffed. Last Tuesday, Stuff journalist Tom Pullar-Strecker had an article that reported on a variety of similar concerns, informed by extensive comments from former Reserve Bank chief economist John McDermott. A particular focus was on the role of the non-executive members (“the externals”).

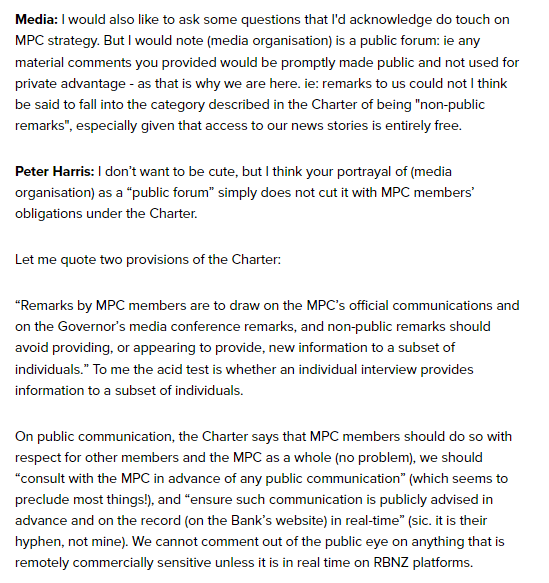

At the press conference for the Monetary Policy Statement Pullar-Strecker asked the Governor about the externals, and if he didn’t get far (the awkward questions at that press conference were mostly left completely unaddressed), he did get from Orr an observation that externals were free to talk, subject to (Orr’s interpretation of) the MPC Charter provisions (in turn agreed by Orr and the Minister) under which for the first 24 hours after an MPS the Governor was the sole spokesperson for the Committee. It rather invited questions once that 24 hour window had passed.

And it seems that Pullar-Strecker did. Just before 5pm yesterday a document headed “Monetary Policy Committe (MPC) external committee member Peter Harris responds to media questions” dropped into the inboxes of anyone signed up for Reserve Bank announcements. Given the context, it was pretty obvious that the questions were from Pullar-Strecker (later confirmed by him and his story), but the Reserve Bank was at pains to keep anonymous the media outlet, even deleting a reference to Stuff in one of the reporter’s questions.

Kudos to Pullar-Strecker for pursuing the issue. In 3.5 years of the MPC’s life, it is only the second interview ever granted by an external MPC member (there was some comments by Harris to Bloomberg a couple of years back), despite the huge power that (on paper anyway) MPC members wield, not to speak of the mayhem (inflation, looming recession) now following in their wake.

Unfortunately, if the Bank can now push back and say “see, Harris did (another) interview”, the substance of the interview mostly just serves to confirm doubts about the institution and the individuals. From their perspective it is hard to see what, if anything, is gained by choosing to make him available in this way (and I don’t think we need to doubt that doing the interview will have had the sign-off of the Governor, and was perhaps encouraged by him). At times, Harris displays all the grace and constructive open and engagement we might expect in a rebellious 15 year old told they have to make conversation with Grandma at the family Christmas celebrations. If the answers aren’t quite monosyllabic grunts. most of them might as well be.

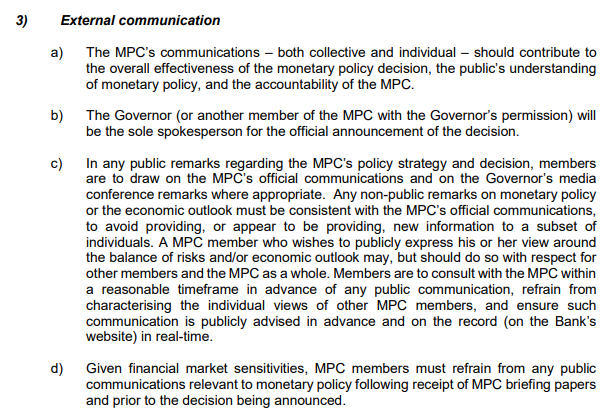

Since it is important background to the interview, here is the relevant section of the MPC Charter.

I don’t suppose anyone has any particular problem with a), b) and d). In fact, from a) one might positively welcome the explicit mention of the notion that communications should contribute to the accountability of the MPC. The focus is on c). If one interprets the first two sentences as being about the most recent decisions, there isn’t too much problematic there, at least in principle, given the model that favours consensus decisionmaking. After all, good minutes of the MPC meetings (unlike the ones we have) would give considerable weight to outlining the conflicting arguments, perspectives, considerations, and some members might reasonably emphasise some of those rather than others (a consensus decision that everyone can “live with” – the Governor’s own word – does not necessarily mean everyone came to that decision for the same reasons.

Note that the Charter does not prevent – in fact explicitly allows for – members from expressing “his or her view around the balance of risks and/or economic outlook”. As the Governor put it last week, there are some courtesies to be observed (let your colleagues know in advance, don’t attack other individual members’ views in public). And there is the requirement that “such communication is advised in advance and on the record (on the Bank’s website) in real-time”. There is certainly no obstacle to recent MPC members reflecting on what has passed, or on the structure, processes etc of the MPC. Note too that the Charter applies to all MPC members, not just the externals

That final provision in c) looks to have been designed to cater for MPC member speeches. It is easy to announce in advance that an address will be being given and to commit to release the text on the Bank’s website when the address is being given. Whether speakers stick to their written text – Orr apparently rarely does – is perhaps harder to police.

Note, however, that there was no advance notice of the Harris interview, so the Bank – which issued the statement on Harris’s behalf – appears to have been complicit in breach of the Charter. More generally, although the text of this interview is available on the Bank’s website, no other interviews by MPC members are (in the last few days for example, Conway with Bernard Hickey, Hawkesby with Stuff, Silk with Reuters – as it happens, each of those MPC members talking about more market-sensitive stuff than Harris ended up doing). It isn’t uncommon for (internal) MPC members to give interviews to media outlets and (a) never provide transcripts, and (b) which are behind paywalls. The Charter looks like it could do with an amendment to require that the text of any media interview with an MPC member in their MPC capacity should be published on the Bank’s website simultaneously with the story published by the interviewing outlet. That is the sort of approach an organisation seriously committed to transparency would take.

On this occasion, the Bank’s approach – emailing out the text – looks to have been some sort of revenge play, undermining the capacity of the journalist to break a story from the interview, in return for the offence of challenging the Bank/MPC. The rules and practices depend on how compliant the journalist is. Pullar-Strecker noted on Twitter that the Bank had not even told him this was the approach they were going to take.

What of the substance of Peter Harris’s interview.

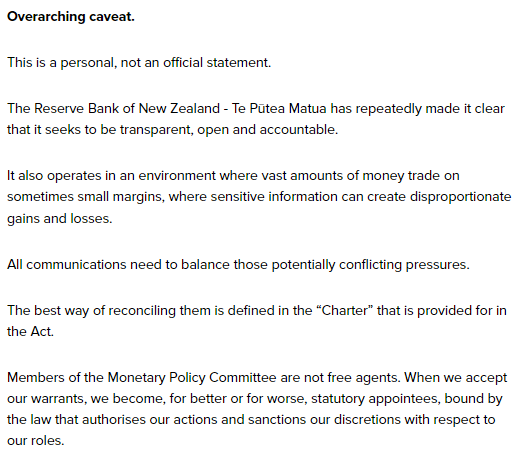

It begins with this rather defensive ‘overarching caveat”

Except that Conway, Silk, and Hawkesby had each given fairly extensive interviews in recent days. The Charter just is not that constraining, unless you want to avoid scrutiny/comment (or, more generally, Orr seems to favour internal members, who of course directly answer to him). Now, it is fair to note that none of those internal member interviewees were actively advancing alternative perspectives on the inflation and monetary policy outlook, but they weren’t all simply reciting already-published lines either (from Silk we learned that apparently we will have only a “technical recession”, from Hawkesby – rather better qualified to comment – that actually these things are often quite a bit sharper than forecast).

Before proceeding further I should say that I didn’t think all the questions to Harris were particularly well-framed. But it is pretty standard media advice that you answer the question you want to answer. If the question is ill-phrased or not really to the point, answer another one. And if you and your organisation are really committed to being “transparent, open, and accountable” do it in an open, constructive and positive way, not grudgingly or petulantly.

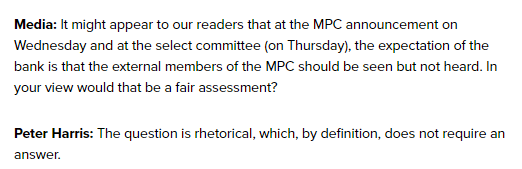

Surely he could have come up with a more constructive response than that? It was, after all, a reasonable question when Orr highlights that all the MPC members were present, but only he and his direct reports were able to say anything. No one forced them to be there, so what did they themselves see the point as having been?

This was interesting, suggesting that Harris had the questions in writing so had had the opportunity to think – and take advice – about how to respond.

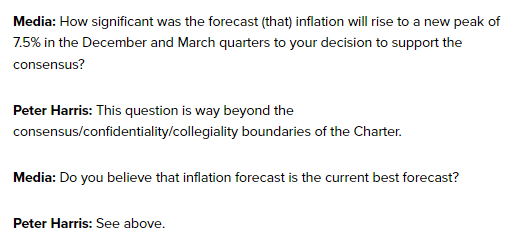

As far as I can see none of the questions on monetary policy itself went beyond the sort of thing the internal MPC members were answering in their recent interviews. The journalist pushes back

Which surely leaves everyone confused. The transcript of this interview was published in full on the Bank’s website. If MPC members really aren’t allowed to interviews, why is he doing one?

Even if you don’t want to say much of substance, there are ways of answering these questions that don’t come across as deliberately obstructive, and indeed might offer some insight on the value (or otherwise) a particular MPC member is adding. To take the second question as an example, it was an easy invitation to say something like “yes, but of course any medium-term forecast is inevitably not that much better than a shot in the dark – that is the nature of economics and economies – and mostly likely a lot will turn out different. It is our – my – best view for now, but our processes emphasise holding any view lightly, and regularly updating our forecasts and policy”.

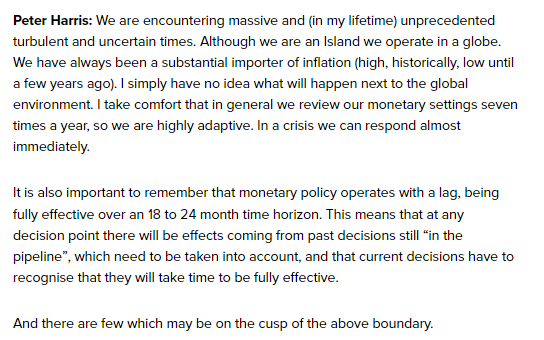

The interview continues

I have no idea what the final sentence is supposed to mean. Of the rest, when a family member read the interview they commented of the first sentence “is he 35?”. In fact, Harris is a lot closer to 70. If he really believes the first sentence – against the backdrop of the 1970s and 80s New Zealand – at very least the claim needs more elaboration. As it is, it simply seems designed as cover for the Bank’s failure (in company with many other central banks).

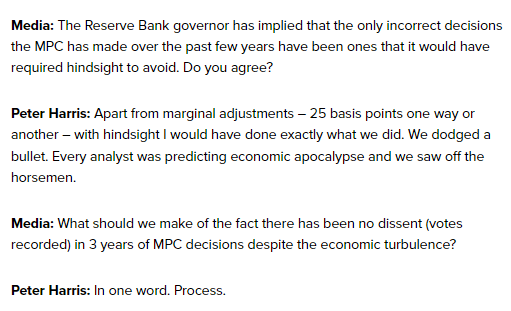

The interview continues

What an extraordinary claim: worst inflation outbreak in decades, MPC now aiming for a recession to reverse it,, not to speak of crisis lending programmes running on years after the crisis (something even management suggests they might have done better) and $9bn+ losses on the LSAP programme, and even “with hindsight I would have done exactly what we did”. It might be one thing to argue that “only with hindsight would I have done things much differently”, but “with hindsight I’d have done exactly what we did” is….well, almost beyond words. And all that apocalyptic rhetoric……I mean, with hindsight it is clear that “every analyst” (and more importantly in this context, every MPC) was wrong. With hindsight, they were mirages not the Four Horsemen.

He does go on after the one word (“Process”) to describe that process. The internal process doesn’t sound to have changed much since the decades I spent on the internal advisory MPC/OCRAG, but perhaps it is worth noting that in those days unanimity among the Governor’s advisers (it was then finally solely his call) wasn’t that common – in fact, successive Governors had us each put our recommendations in writing, initially without seeing what others were recommending, precisely to limit the risk of groupthink or peer pressure towards the end of the process. It is a very poor reflection on all involved that through the period of great uncertainty and the worst monetary policy stuff-up since the 1989 Reserve Bank Act gave the power to the Bank, not one MPC member, not even once, felt and reasoned sufficiently strongly as to dissent, on anything. Even now, no external MPC member has given us their own accounting for the handling of the last three years (beyond Harris’s “with hindsight we did it right”). Note that the recent Reserve Bank self-review is a management document, and I have an OIA request in at present to try to learn what the externals contributed and whether or not they agreed.

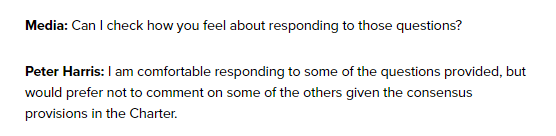

The interviews ends with two answers that sum up the grudging approach

Surely the first of those questions could have been treated as an open invitation to talk expansively about how “I can’t be certain about that, but let me tell you about what I think I as an external member have been able to bring to the table [as someone with decades of experience in New Zealand economic policy, strong connections to the labour market, as someone standing outside the day to day pressure staff and management face, as someone willing to ask awkward questions as part of a confidential deliberative process] – or whatever value he thinks he has offered.

And the final question? What would have been wrong with a more gracious “look others will have to be the judge of that, but I wouldn’t have accepted appointment and reappointment if I hadn’t thought I was adding value. If I can’t be totally detached in assessing my own contribution, when I look at my colleagues – Bob Buckle and Caroline Saunders – I can see the impact they’ve had around the table, the questions they’ve posed, the research they’ve helped spark.” and so on?

It was, of course, a shame that the interviewer didn’t also ask Harris to justify the exclusion of people with current expertise in matters monetary and macroeconomic from serving as external members of the Committee. It wasn’t his choice – Orr, Quigley and Robertson did that – but he now has the benefit of 3.5 years serving on a New Zealand MPC as an external member, and it would be quite reasonable to seek his perspective (and not at all in breach of the charter for him to have given a substantive answer).

We need a better model, and we need better people (internal and external) on the MPC. While perhaps it is better than nothing to have had this Haris interview, the substance (or lack) of it only tends to confirm how poorly we are being served.

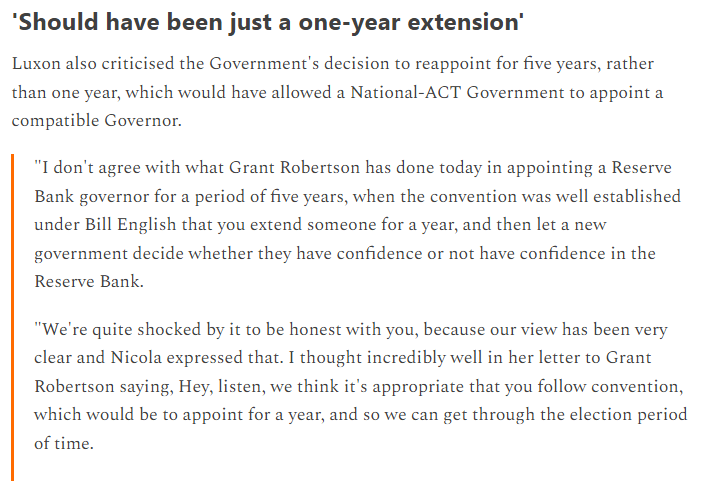

I watched the Q&A interview yesterday with the Leader of the Opposition Chris Luxon. Monetary policy and the position of the Reserve Bank Governor came up.

It is really quite disappointing that the Minister of Finance, presumably with the acquiescence of the Prime Minister, has so politicised the situation that a Leader of the Opposition can reasonably be asked what he would expect (eg possible resignation) of the Reserve Bank Governor after the election if National wins. If he is at all serious about his answer – appoint an independent reviewer as soon as they take office and only decide after that – it is a recipe for considerable, unwelcome, market uncertainty, and further reputational risk for New Zealand and its system of economic governance.

We really should have appointees to such positions that both sides of politics can respect and trust. That has always been implicit in the model under which the central bank is given operational autonomy over monetary policy (and the massive cyclical influence that involves), the Governor (and MPC members) are appointed for terms not coinciding with, and longer than, parliamentary terms, and (in NZ since 1990) where the Minister of Finance cannot simply appoint his or her own person as Governor. That expectation was further reinforced when the current Prime Minister and Minister of Finance in 2018 amended the Reserve Bank Act to explicitly require consultation with other parties in Parliament before a person is (re)appointed as Governor.

When Adrian Orr was first appointed at the end of 2017 that “general acceptance” threshold was probably met. There was plenty of Orr sceptics about. although often rather quietly (since they or their employers had to deal with either NZSF or the Reserve Bank, and Orr was never known for embracing criticism), but there was no great controversy about the appointment (as it happened the search and selection process had been well underway before the election and change of government, and the Bank’s Board – which put forward Orr’s nomination – had been entirely appointed by the previous National government).

It isn’t the case now. The two main Opposition parties had both made clear to the government, when the legally-required consultation occurred, that they had concerns about the proposed reappointment. But there has been no hint or sign that the Minister of Finance made any effort to engage to allay those concerns, instead – his own legislation notwithstanding – he simply pushed ahead and reappointed Orr, having had the nomination made by the new Reserve Bank Board, possessed of almost no subject expertise, he himself had appointed just a couple of months earlier. Perhaps a bit like the entrenchment outrage in the headlines today, it was lawful (much is in New Zealand) but it was far from proper.

(As I’ve pointed out before the actual argument National made in their letter re Orr was weak and their historical parallel was flawed, but then they were caught in a difficult position – unless Robertson heeded their concerns and looked elsewhere for a new Governor, they could be stuck with Orr as Governor, almost certainly unable to dismiss him (unless he did something particularly new and egregious in his new term) – and may have felt reluctant to outline a range of specific concerns about Orr and his stewardship in writing.)

TVNZ’s interviewer, who usually does a fairly good job, seemed to come to yesterday’s interview holding a brief for Orr. Among the lines he put to Luxon was the suggestion that he shouldn’t be too critical or Orr and the Bank because they had been the first developed country to raise their policy interest rate. This is the sort of spin the Bank itself likes to hear, and it uses a more-muted version of it at times. I don’t know how many times it has to be said but it is simply a false claim. It isn’t a matter of interpretation or nuance, it is simply false.

There are probably two main sets of groupings that are used to capture a list of developed countries or advanced economies. The first is membership of the OECD, and the second is the IMF’s “advanced economies” groupings. Neither is ideal. The OECD includes several Latin American countries (Costa Rica, Colombia, Chile, and Mexico) that are mostly much poorer and less productive than other members (I’ve often suggested they are “diversity hires”),and excludes Singapore and Taiwan. The IMF list on the other hand does not include any of the Latin American countries, but in central and eastern Europe seems to include countries if they are in the euro but not if not, even if the latter are equally productive. Since so many advanced countries are in the euro, there are really only 20 or so countries with monetary autonomy, setting their own interest rate.

On several occasions in the past on Twitter I’ve used the BIS’s monthly data on policy interest rates. Of the countries there that are on either the OECD or IMF lists, these were the first countries to raise policy interest rates in 2021.

Discount Mexico and Chile if you like and you are still left with five advanced country central banks having moved before our Reserve Bank did, all of them for countries that are either materially richer/more productive than New Zealand or (Korea, Hungary, Czech Republic) about the same. You could make further allowance for the Reserve Bank and accept that if their MPC meeting in August 2021 had been a day earlier, the OCR would first have been raised then, but they still wouldn’t have been the first to move.

There is no question but that our Reserve Bank moved earlier than the other Anglo central banks (or even the ECB) but what of it?

More generally, when individual central banks moved (early or late in calendar time) is really neither here nor there anyway. Each central bank faced different domestic situations in terms of capacity pressures, emergent inflation, and the core inflation outlook.

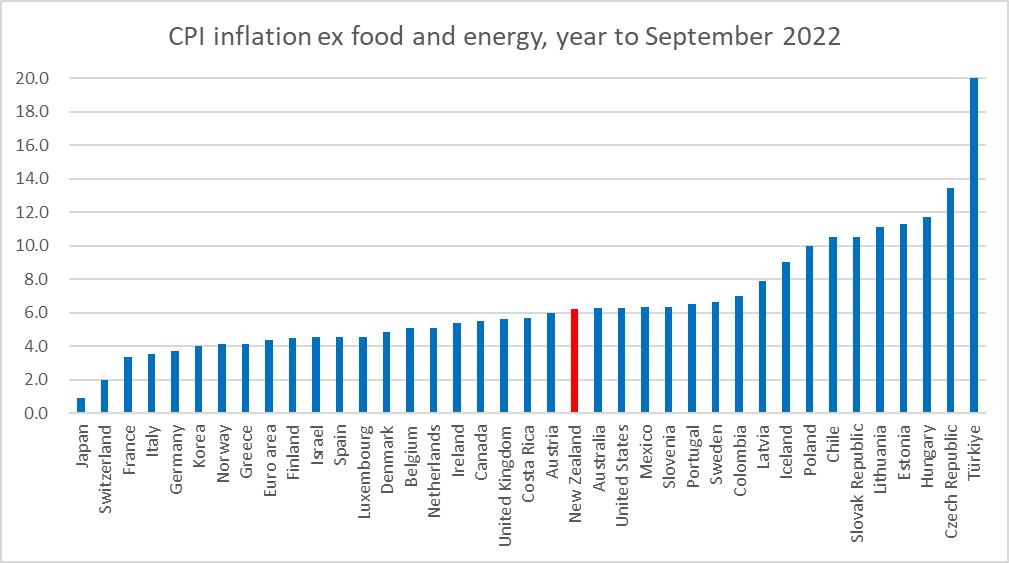

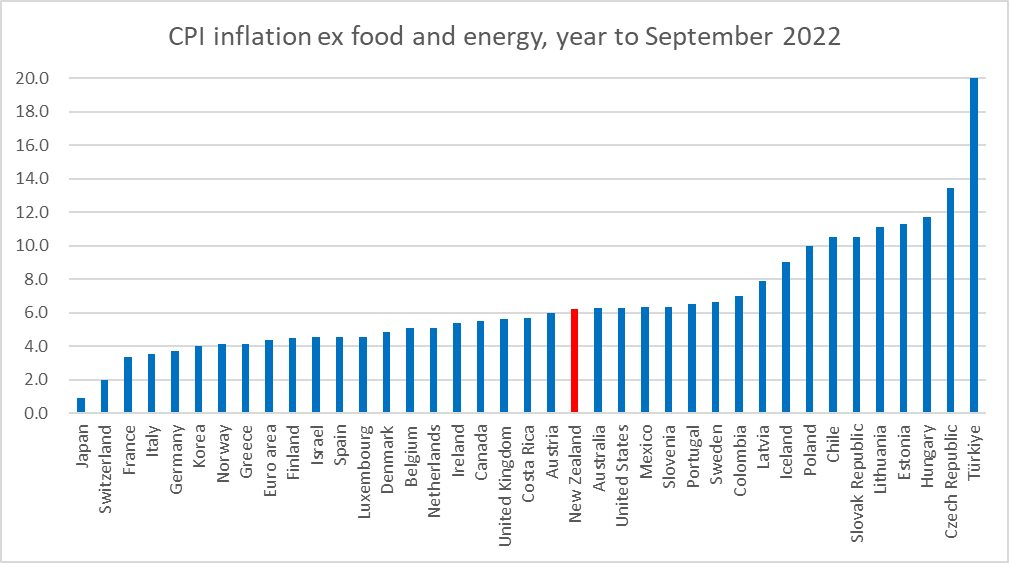

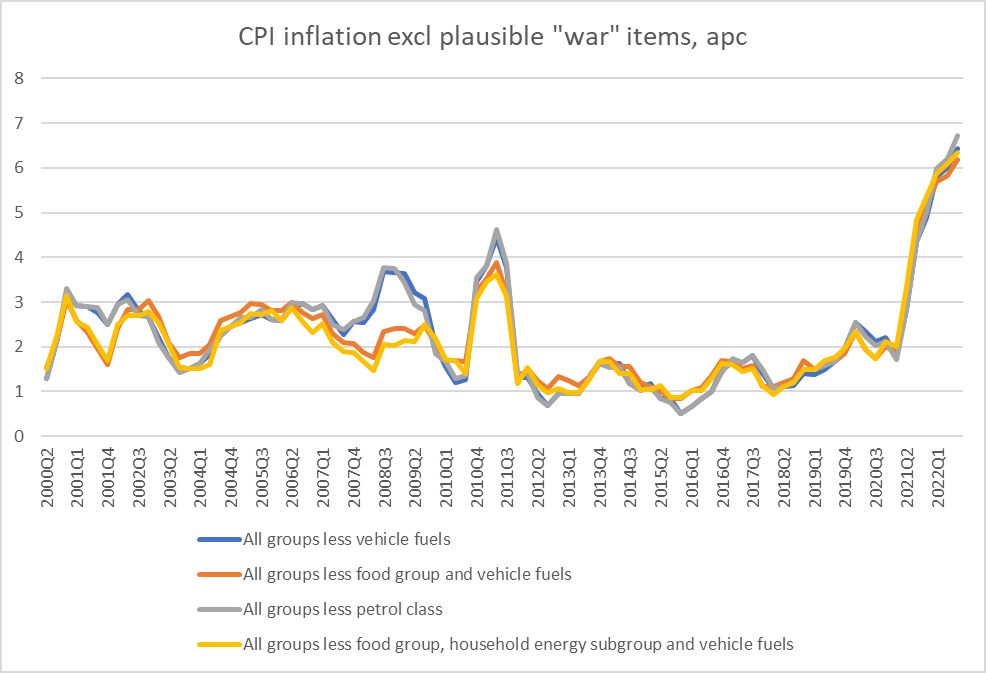

I’m not going to attempt to analyse the story each central bank faced last year, but I’ve shown this chart in a previous post.

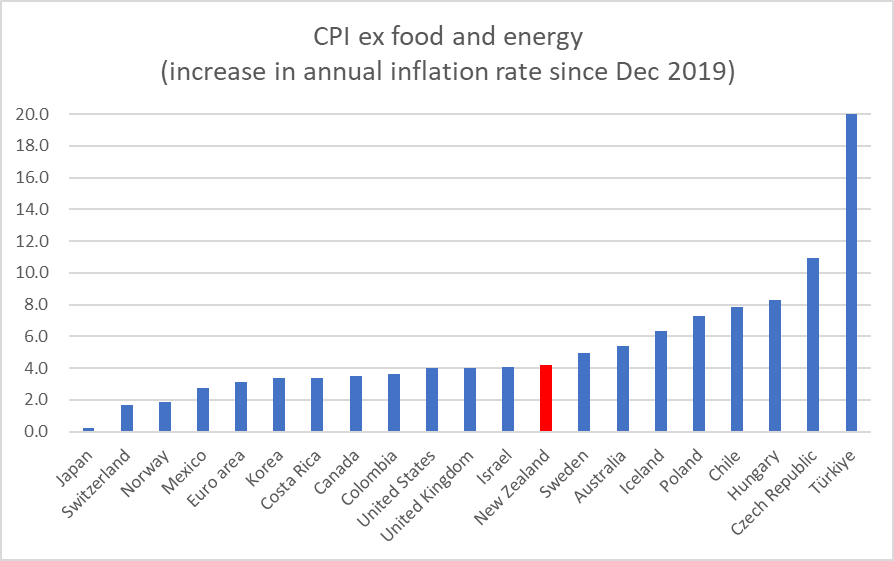

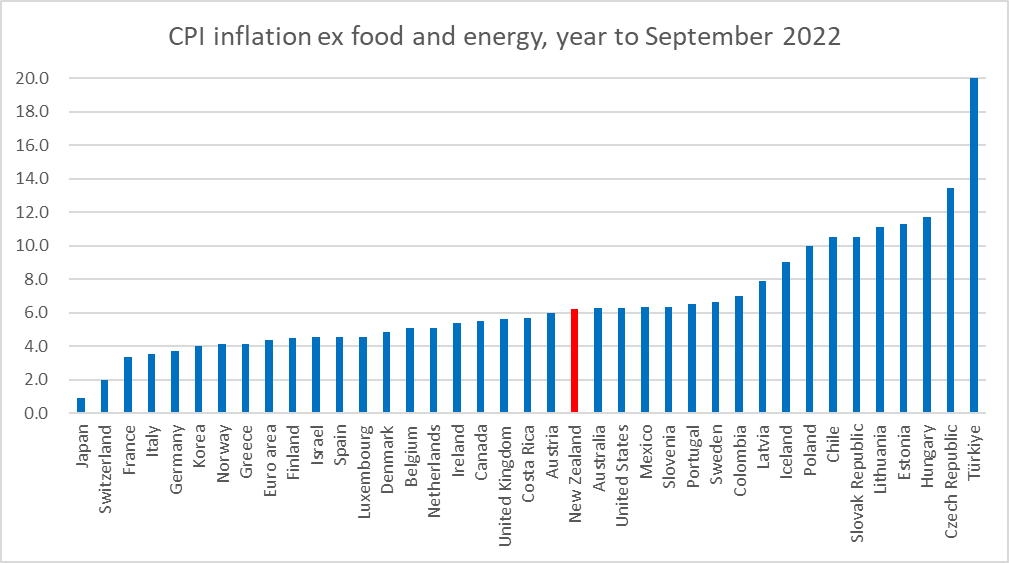

On the most recent data, for the only internationally comparable measure of core inflation we readily have, New Zealand’s core inflation rate now – a year on from the first OCR increase – is nothing special, being just above that of the median OECD country. If we focus only on OECD countries with their own monetary policies (and the euro area as a single observation) we get this chart showing the increase in the core inflation rate since just prior to Covid (actual Turkey increase is far larger than the scale allows).

It isn’t one of the worst, but again it is slightly worse than the median country (and, as it happens, worse than in three of the four Anglo countries, and worse than the euro area).

This isn’t another post trying to evaluate in any detail the Bank’s absolute or relative performance, but as a general observation almost all central banks have done poorly in the last couple of years, and little about the Reserve Bank’s policies or policy outcomes stands out from the pack. Media defenders of the Governor should take note, and/or get better basic researchers.

What the post is mainly about is central bank appointments. We’ve had some dreadful ones this year – the deputy chief executive responsible for matters macroeconomic who has no background or evident expertise in the subject, and who yet is a full voting MPC member, and (see above) the reappointment of the Governor. Then there was the decision (apparently joint between the Governor, Minister and (old) Board) to keep in place the blackball prohibiting anyone with current in-depth expertise in matters macroeconomic or monetary from serving on the MPC, all as prelude to the reappointment without much scrutiny of two external MPC members whose terms were expiring.

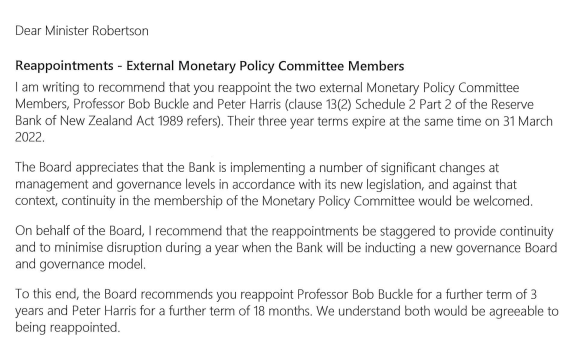

On which note, I had another OIA request back the other day, which included the letter from the Reserve Bank Board chair to the Minister of Finance recommending those reappointments. It was perhaps even more lame than I had expected. There was no attempt to evaluate or describe the contributions Buckle and Harris had made, nothing at all about the rapidly rising (core) inflation backdrop for which they shared responsibility, no suggestion of having considered any alternative candidates (neither Buckle nor Harris are young). In fact, the strongest (only) argument for reappointment seems to have been that “the Bank is implementing a number of significant changes in governance in accordance with its new legislation”, even though almost none of the 2021 Act had anything to do with monetary policy or the MPC

That letter did, however, partly answer one question I’d had. Peter Harris – former politically-appointed adviser in Michael Cullen’s office – was reappointed for a term of only 18 months to expire on 1 October 2023, right in the middle of the likely election campaign. Why, I wondered, would Robertson have done that – ministers after all being well aware of the convention that new appointments should not be made to positions starting close to likely election dates? But it turns out it was the Board’s doing, and there is no sign they gave any thought to the fact that the end of Harris’s term was going to land in the midst of the election period. Which seems quite unnecessarily careless of them. One hopes there is no question of any new appointment being made until after the election. If National were to win, the vacancy would give them an opportunity to begin to exert some influence; one would hope they would remove the bar on expertise, and at the same time amend the MPC’s charter to make it clearer that individual members were expected to bring expertise to bear and to be individually accountable.

But the current government is quite free to make the next MPC appointment. The worst of the first batch of external MPC members was Caroline Saunders. Her term expires on 31 March 2023. The papers released at the time of those 2019 appointments make it pretty clear that she was a diversity hire. Professor Saunders may be very capable in her own field but she has no background at all in macroeconomics or monetary policy. Consistent with that, we have heard not a word from here in her (almost) four years on the MPC. She has taken the taxpayers’ dime and there is no evidence she has made any contribution at all, and has done or said nothing – no speech, no interview, no parliamentary committee appearance – to provide any basis for holding her to account, even as she shares formal responsibility for the biggest monetary policy stuff-up in decades

It would be quite unfortunate if Saunders is reappointed (but most probably it is already a fait accompli, given that no vacancies have been advertised). If there was ever a case for a token female appointment (which there wasn’t; token appointees are never desirable), the ultimate in token appointees now holds a senior executive role on the committee. More generally, in any body – public or private – fresh blood should be introduced from time to time, and yet none of the externals has been changed, and (by the rules they themselves signed up to) those members are not allowed to foster any independent subject expertise themselves in their time on the MPC (and the Bank has been doing very little serious research, so there won’t be much expertise being fostered/extended inside). From a narrowly political perspective, one might have thought it might have been in the government’s interest to have found a strong new appointee who might have a good chance of doing two future terms.

Which bring us back to Luxon. It isn’t clear that National cares very much about any of this,or will fllow through if and when it takes office (why rock the boat when you now have an office to hold and savour?). I’m not at all optimistic, but if they are more serious than they seem, here was a post outlining some of things they could look at.

If you’d been given a great deal of delegated power and had messed up badly – not through any particular ill-intent, but perhaps you’d misjudged some important things or belatedly realised you didn’t have the knowledge to cope with an unexpected circumstance that you thought you had – and if you are anything like a normal decent person you would be extremely apologetic and quite contrite. Heck, borrow a friend’s car for the afternoon and come back with a dent in it – not even necessarily your fault – and most of us would be incredibly embarrassed and very apologetic. Bump into someone (literally) in the supermarket aisle and most of us will be quite apologetic – often enough proferring a “sorry” just in case, even if it is pretty clear it is the other person who knocked into us.

But the apparently sociopathic world of central banking seems to be different. The Reserve Bank (Governor and MPC) are delegated a great deal of power and influence. Back before the days of the MPC I used to describe the Governor as by far the most powerful unelected person in New Zealand (and more powerful individually than almost all elected people too). The powers – exercised for good or for ill – haven’t changed, they’ve just been (at least on paper) slightly diffused among a group of (mostly silent) people whose views we never quite know, and whose appointment is largely (effectively) controlled by the Govenor. (There was a nice piece in Stuff yesterday on the problems of the MPC, echoing many points made here over the years.)

It is not as if the Bank took on these powers reluctantly, or that the Governor had to have his arm twisted to do the job. The Bank championed the delegation (and reasonably enough) and every single member of the MPC took on the role – amply remunerated – entirely voluntarily. But they seem to have long since forgotten that counterpart to autonomy and operational independence that used to feature so prominently in all their literature, that great delegated power needs to be accompanied by serious accountability. Among decent people that would include evident contrition when things go wrong, no matter how good your intentions might have been, even if you thought you’d done just the best you personally could have.

The Auditor-General was reported yesterday raising concerns about the serious decline in standards of accountability in New Zealand public life. Whatever the situation elsewhere – and I have no reason to question the Auditor-General’s view – nowhere is it more evident than around the Reserve Bank, which exercises so much power with so few formal constraints. Much too little attention has been given to the fact that, having delegated them huge amounts of discretionary power to keep (core) inflation near 2 per cent, the Reserve Bank has messed up very badly over the last couple of years.

The issue here is not about intent or lack of goodwill, but about outcomes. When central banks were given operational autonomy it was on the implied promise that they’d deliver those sort of inflation outcomes, pretty much year in year out. The public wouldn’t need to worry about inflation because control of it – under a target set by elected politicians who would hold them to account – had been delegated to a specialist, notionally expert, agency, which would know what it was doing. 20 years ago the expectation on the Bank was fleshed out a little more: that they should do their job while avoiding unnecessary variability in interest rates, exchange rates, and output.

And what do we now have? Roughly 6 per cent core inflation, three years of annual headline inflation above the top of the target range, public doubts about just whether the Bank will deliver 2 per cent in future. Oh, and now the necessity (very belatedly acknowledged by the Bank yesterday) of a recession and a significant rise in unemployment to levels well beyond any sort of NAIRU to get inflation back in check. Add in the arbitrary wealth distributions – that no Parliament voted on – with the heavily indebted (including the government) benefiting from the unexpected surge of inflation the Reserve Bank has overseen, at the expense of those with financial savings. And the huge disruptions to lives and businesses from both the extremely overheated economy we’ve had for the last 12-18 months and the coming nasty shakeout. Oh, and that is not to mention more than in passing the $9.2 billion of LSAP losses the Reserve Bank up entirely unnecessarily (foreseeably).

It has not, to put it mildly, been the finest hour of the Reserve Bank. But there has been no a word of contrition – from the Governor or any of the rest of the Committee – and no real accountability at all (among other things, Orr and two of the MPC have been reappointed this year, with no sign of any searching scrutiny of their records or contributions).

Instead we just get lots of spin, and lightweight analysis. One of Orr’s favourite lines (repeated as I type at FEC this morning) is that the Reserve Bank was one of the very first central banks to tighten “by some considerable margin”, when in fact there were half a dozen OECD central banks that moved before our central bank did. We had claims from Orr a while ago that the macro benefits of the LSAP programme were “multiples” of those mark to market losses to taxpayers – a claim that quietly disappeared when they actually published their review of monetary policy. A few weeks ago Orr was telling Parliament that if it weren’t for the Ukraine war inflation would have been in the target range – notwithstanding the hard data showing core inflation was already very high well before the war – and then nothing more is heard of that claim when the MPS itself was published.

Yesterday we heard lots of bluster about workers, firms and households being enjoined to change their behaviour – even trying to damp down Christmas – as if inflation was the responsibility of the private sector, not the outcome of a succession of Bank choices and mistakes. But not a word from the Bank or Governor accepting any responsibility themselves.

To repeat, I don’t doubt that the Bank was well-intentioned throughout the last few years. Plenty of other people made similar mistakes in interpreting events. But it is the Reserve Bank and its MPC who are charged with – and paid for – the job of keeping the inflation rate and check. They’ve failed. Given that stuff-up they may now fix things up, but it is no consolation or offset to the initial huge series of mistakes. And not a word of contrition, barely even much acceptance of responsibility.

Which is a bit of a rant, but about a serious issue: with great power must go great responsibility, accountability….and a considerably degree of humility. Little or none has been evident here.

But what of the substance of the Monetary Policy Statement? Here I really had only three points.

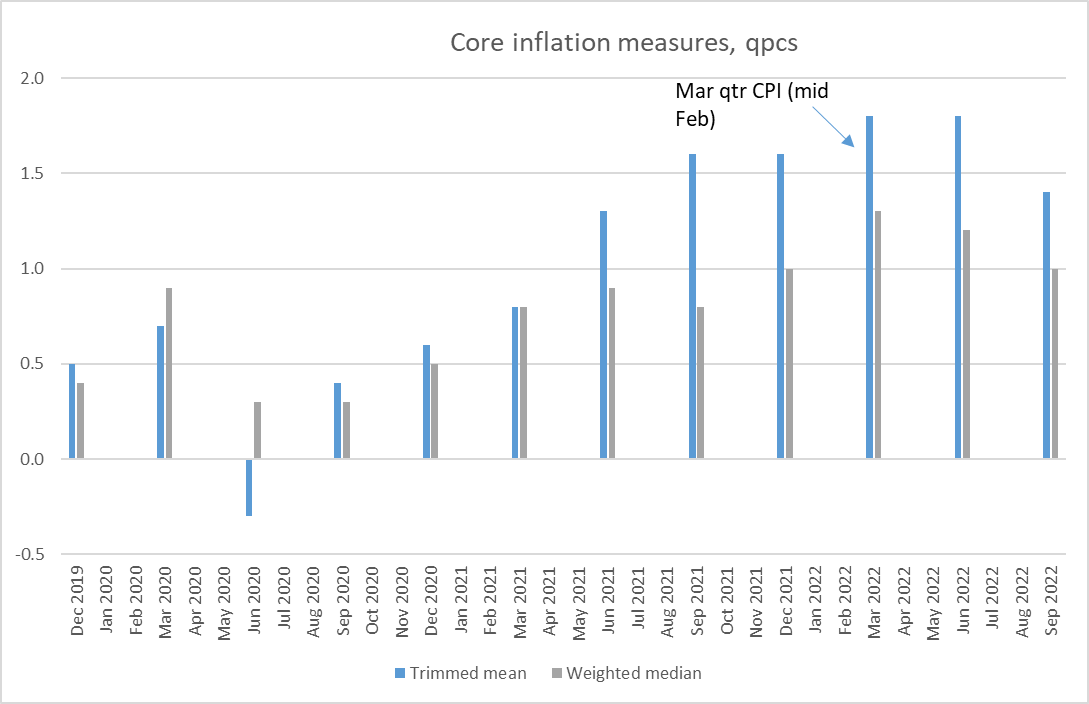

The first is the glaring absence of any serious in-depth analysis of what has actually been going on with inflation, at a time of some of the biggest forecast errors – and revisions in the OCR outlook – we’ve seen for many years. For example, every chart seems to feature annual inflation, which is fine for headlines but tells you nothing about what has been happening within that one year period. What signs are there, for example, that quarterly core inflation might have peaked (or not) – eg some of the charts I included here? There seemed to be no disaggregated analysis at all, for example of the sort one economic analyst pointed to in comments here the other day. This from the organisation that is responsible for inflation, and which has by far the biggest team of macroeconomists in the country. We – and those paid to hold the Bank to account – really should expect better.

And almost equally absent was any persuasive supporting analysis for the really big lift in the forecast path of the OCR, now projected to peak at 5.5 per cent. My main point is not that I think they are wrong but that there is little or no recognition that having misread badly the last 2-3 years (in good company to be sure), there is little reason for them or us to have any particular confidence in their forecast view now. Models and sets of understandings that didn’t do well in preventing us getting into this mess probably haven’t suddenly become reliable for the getting out phase. But even granting that, the scale of the revision up seems disproportionate to the surprises in the new data of the last few months. It has the distinct feel of just another stab in the dark (but then I’ve been a long-term sceptic of the value of central bank OCR forecasts), with little engagement with either weakening forward indicators or the lags in the system (in the last 6 weeks the Bank has now increased the OCR by as much as it did in the first six months of the tightening cycle. With a recession already now finally in the forecasts based on what the MPC has already done (they don’t meet again until late February and the deepest forecast fall in GDP is in the quarter starting just 5 weeks later – the lags aren’t that short) they can’t really be very confident of how much more (if any) OCR action might be needed.

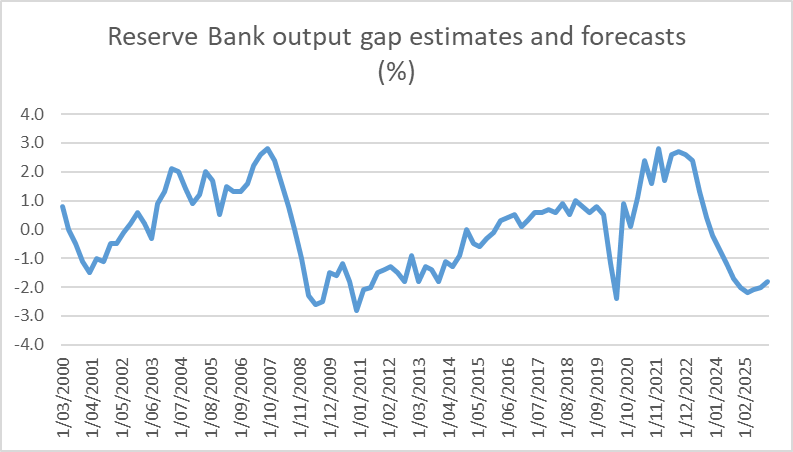

Finally, it is constantly worth bearing in mind the scale of the task. Core inflation has been running around 6 per cent and should be close to 2 per cent. That scale of reduction in core inflation hasn’t been needed/sought since around 1990. In 2007/08 inflation had got away on us to some extent, but a 1.5 percentage point reduction would have done the job of getting back to around 2 per cent. As Westpac pointed out in their commentary, the scale of the economic adjustment envisaged in these forecasts (change in estimated output gap) is very similar to what (the Bank now estimates) we experienced over 2008 to 2010.

The open question then is perhaps whether this sort of change in the output gap is likely to be sufficient: 13 years ago it delivered a 2 percentage point reduction in core inflation, but at present it looks as though we need a 4 percentage point reduction now. It isn’t obvious that other surrounding circumstances now will prove more propitious than then (eg for supply chains normalising now read the deep fall in world oil prices then).

Perhaps it will, perhaps it won’t, but you might have expected a rigorously analytical central bank and MPC to have attempted to shed some light on the issue. But once again they didn’t.

(My own money is probably on a deeper recession next year, here and abroad but……and it applies to me as much as to anyone else … if you got the last 2-3 years so wrong you have to be very modest in your claims to have the current and year-ahead story right.)

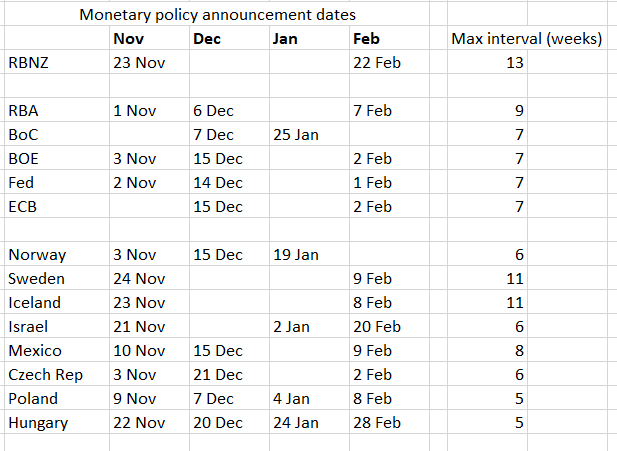

The Reserve Bank’sMonetary Policy Committee has its final meeting for the year on Wednesday, and then they shut up shop. For a long time. The next scheduled announcement is not until 22 February, a full 13 weeks (3 months) away. Nice job if you can get it, and although I’m sure management and staff will still be working for much of the intervening period, the same is unlikely to be said for the three non-executive members, who are generously remunerated by the taxpayer, utterly invisible, and only need to show up when meetings are scheduled.

This strange schedule has been in place for quite a few years now, having been adopted at a time when the OCR wasn’t being moved much at all (and when the Bank was raising the OCR, it often proved to have been a mistake). But having been in place for a while does not make it any more defensible or sensible. In fact, last year’s three month summer break almost certainly was one factor in how slow the MPC was to get on with raising the OCR once they’d finally made a start. On no reading of the data (contemporary data that is) did it make sense for us to have ended 2021 with the OCR still lower, in nominal terms, than it had been just prior to Covid. And having experienced the issue last summer (when perhaps it caught them by surprise) there was no excuse for not resetting the schedule for this summer.

One can always mount defences (for almost anything I suppose). Monetary policy works with a lag, the OCR adjustments can be just as large as they have to be, perhaps there is a bit of a tradeoff between time doing analysis and time spent preparing for meetings. But none of it is very convincing in this context. And it is out of step with their peers.

Here is a table of the monetary policy announcements dates over November to February for a fairly wide range of OECD country central banks. None, not even Sweden and tiny Iceland, are taking as long a break as our MPC (and although I didn’t tot up all the northern hemisphere summer meeting dates, it didn’t look as though any took as long a break then as our MPC takes now). The median country has a longest gap of seven weeks between meetings over this period.

[UPDATE: In addition, the South Korean central bank meets on 24 Nov, 13 Jan, and 23 Feb]

There are substantive macroeconomic arguments for (and against) a 75 basis point OCR adjustment this week, but one of arguments some have advanced is that they really need to go 75 basis points this week because they don’t have another opportunity until late February. But whose fault is that? It is entirely an MPC choice. They have a very flexible instrument and just choose to tie their hands behind their backs to give themselves a very long summer break.

The whole situation is compounded by the inadequacies of New Zealand’s key bits of macroeconomic data. We now have the CPI and the unemployment rate for mid-August (the midpoint of the September quarter). Most OECD central banks already have October CPI data, almost all have September unemployment rate data (and several have October unemployment rate data), and three-quarters of OECD countries already have September quarter GDP data (a few even have monthly GDP estimates).

The combination of slow and inadequate data and widely-spaced summer meetings really isn’t good enough, especially at a time when there is so much (perhaps inevitable) uncertainty about the inflation situation and outlook. The inadequacies of our national macroeconomic statistics cannot be fixed in short order (not that the government shows any interest in doing so anyway). But how often, and when, the MPC meets is entirely at the Committee’s discretion, and easily altered with little or no disruption other than to the holiday plans of some appointed and (supposedly) accountable policymakers (people who not incidentially – and pardonably or otherwise – have done such a demonstrably poor job of their main responsibility, keeping core inflation in the target range, in recent times.

The MPC should be announcing on Wednesday (a) an extra OCR review for a few days after the CPI release in January, and (b) a commitment to revisit the meeting schedule for future years to bring the length of the long summer break back to (say) no longer than the one the RBA takes. If they don’t journalists at the press conference and MPs at FEC should be asking why not.

(Writing this post brought to mind memories of Orr 20+ years ago when the OCR was first introduced championing having only four reviews a year. The OCR then was new, inflation was low and stable. One hopes that sort of thinking no longer lurks in the back of the Governor’s mind.)

Way back in 1990 Parliament formally handed over the general responsibility for implementing monetary policy to the Reserve Bank. The government has always had the lead in setting the objectives the Bank is required to work to, and has the power to hire and fire if the Bank doesn’t do its job adequately, but a great deal of discretion has rested with the Bank. With power is supposed to come responsibility, transparency, and accountability.

And every so often in the intervening period there have been reviews. The Bank has itself done several over the years, looking (roughly speaking) at each past business cycle and, distinctly, what role monetary policy has played. These have generally been published as articles in the Bank’s Bulletin. When I looked back, I even found Adrian Orr’s name on one of the policy review articles and mine on another. It was a good initiative by the Bank, intended as some mix of contribution to debate, offering insights that were useful to the Bank itself, and defensive cover (there has rarely been a time over those decades when some controversy or other has not swirled around the Bank and monetary policy).

There have also been a couple of (broader-ranging) independent reviews. Both had some partisan intent, but one was a more serious effort than the other. When the Labour-led government took office in 1999 they had promised an independent review, partly in reaction to their sense that we had messed up over the previous few years. A leading Swedish academic economist Lars Svensson, who had written quite a bit about inflation targeting, was commissioned to do the review (you can read the report here). And towards the end of that government’s term – monetary policy (and the exchange rate) again being in the spotlight – Parliament’s Finance and Expenditure Committee did a review.

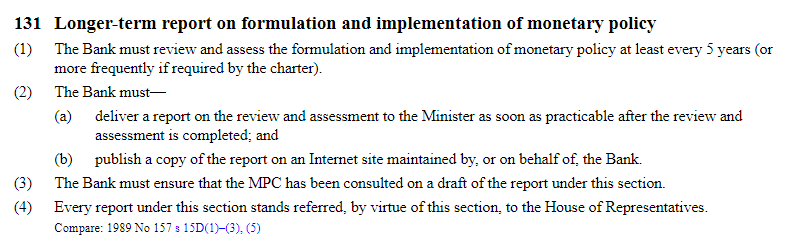

When the monetary policy provisions of the Reserve Bank Act were overhauled a few years ago this requirement was added

It made sense to separate out this provision explicitly from that for Monetary Policy Statements (in fact, I recall arguing for such an amendment years ago) but the clause has an odd feature: MPSs (and the conduct of monetary policy itself) are the responsibility of the MPC, but these five-yearly longer-term reviews are the responsibility of “the Bank”. In the Act, the Bank’s Board is responsible for evaluating the performance of both management and the MPC, but the emphasis here does not seem to be on the Board. It seems pretty clear that this is management’s document, and of course management (mainly the Governor) dominates the MPC. Since the Board has no expertise whatever in monetary policy, it is pretty clear that the first of these reports, released last week, really was, in effect, the Governor reporting on himself.

And although plenty of people have made scathing comments about that, there isn’t anything necessarily wrong about a report of that sort. After all, it isn’t uncommon (although I always thought it odious and unfair given the evident power imbalance) for managers to ask staff to write about notes on their own performance, as part of an annual performance appraisal, before the manager adds his/her perspective. The insights an employee can offer about his or her own performance can often be quite revealing. And it isn’t as if the Bank’s own take on its performance is ever going to be the only relevant perspective (although, of course, the Governor has far more resources and information at his disposal than anyone else is going to have). The only real question is how good a job the Bank has done of its self-review and what we learn from the documents.

On which note, I remain rather sceptical about the case (National in particular is making) for an independent review specifically on the recent conduct of monetary policy. Some of those advocating such an inquiry come across as if what they have in mind is something more akin to a final court verdict on the Bank’s handling of affairs – one decisive report that resolve all the points of contention. That sort of finality is hardly ever on offer – scholars are still debating aspects of the handling of the Great Depression – and if there was ever a time when choice of reviewer would largely determine the broad thrust of the review’s conclusions this would be among them. Anyone (or group) with the expertise to do a serious review will already have put their views on record – not necessarily about the RBNZ specifically (if they were an overseas hire) but about the handling of the last few years by central banks generally. There is precedent: the Svensson review (mentioned above) was a serious effort, but the key decision was made right at the start when Michael Cullen agreed to appoint someone who was generally sympathetic to the RB rather than some other people, some of equal eminence if different backgrounds, who were less so. It would be no different this time around (with the best will in the world all round). A review might throw up a few useful points and suggestions, and would probably do no harm, but at this point the idea is mostly a substantive distraction. Conclusions about the Reserve Bank and about its stewardship are now more a matter for New Zealand expert observers and the New Zealand political process (ideally the two might engage). Ideally, we might see some New Zealand economics academics weighing in, although in matters macroeconomics most are notable mainly by their absence from the public square.

That is a somewhat longwinded introduction to some thoughts about the report the Bank came out with last week (120 pages of it, plus some comments from their overseas reviewers, and a couple of other background staff papers).

I didn’t think the report presented the Bank in a very good light at all. And that isn’t because they concluded that monetary policy could/should (they alternate between the two) have been tightened earlier. That took no insight whatever, when your primary target is keeping inflation near the middle of the target range and actual core inflation ends up miles outside the range. Blind Freddy could recognise that monetary policy should have been tightened earlier. When humans make decisions, mistakes will happen.

The rest of the conclusions of the report were mostly almost equally obvious and/or banal (eg several along the lines of “we should understand the economy better” Really?). And, of course, we had the Minister of Finance – not exactly a disinterested party – spinning the report as follows: “It is really important to note that the report does indicate that they got the big decisions right”. It should take no more than two seconds thought to realise that that is simply not true: were it so we would not now have core inflation so far outside the target range and (as the report itself does note) pretty widespread public doubts about how quickly inflation will be got down again. It would be much closer to the truth to say that the Reserve Bank – and, no doubt, many of their peers abroad – got most of the big decisions wrong. It has, after all, been the worst miss in the 32 years our Reserve Bank has been independent, and across many countries probably the worst miss in the modern era of operationally independent central banks (in most countries, after all, monetary policy in the great inflation of the 1970s was presided over by Ministers of Finance not central banks).

But there is no sense in the report at all of the scale of the mistake, no sense of contrition, and – perhaps most importantly in my view – no insight as to why those mistakes were made, and not even any sign of any curiosity about the issue. The focus is almost entirely defensive, and shows no sense of any self-critical reflection. There are no fresh analytical insights and (again) not even any effort to frame the questions that might in time lead to those insights. And no doubt that is just the way the Governor (who has repeatedly told us he had ‘no regrets’) would have liked it. And here we are reminded that this is very much the Orr Reserve Bank: the two senior managers most responsible for the review (the chief economist and his boss, the deputy chief executive responsible for monetary policy and macroeconomics) only joined the Bank this year, and so had no personal responsibility for the analysis, preparation and policy of 2020 and 2021 but still produced a report offering so little insight and so much spin. Silk, in particular, probably had no capacity to do more, but the occasional hope still lingered that perhaps Paul Conway, the new chief economist, might do better. But these were Orr’s hires, and it is widely recognised that Orr brooks no dissent, no challenge, and in his almost five years as Governor has never offered any material insight himself on monetary policy or cyclical economic developments. Even if they had no better analysis to offer – and perhaps they didn’t, so degraded does the Bank’s capabilities now seem – contrition could have taken them some way. But nothing in the report suggests they feel in their bones the shame of having delivered New Zealanders 6 per cent core inflation, with all the arbitrary unexpected wealth redistributions that go with that, let alone the inevitable economic disruption now involved in bringing inflation a long way back down again. It comes across as more like a game to them: how can we put ourselves in the least bad light possible with a mid-market not-very-demanding audience (all made more unserious as we realised that the Minister of Finance had made the decision a couple of months ago to reappoint Orr, not even waiting for the 120 pages of spin).

At this juncture, a good report would be most unlikely to have had all the answers. After all, similar questions exist in a whole bunch of other countries/central banks, and if the Reserve Bank has the biggest team of macroeconomists in New Zealand, there are many more globally (in central banks, academe, and beyond) but it doesn’t take having all the answers to recognise the questions, or the scale of the mistakes. In fact, answers usually require an openness to questions, even about your own performance, first. And there is none of that in the Bank’s report.

Thus, we get lame lines – of the sort Conway ran several times at Thursday’s press conference – that if the Bank had tightened a bit more a bit earlier it would have made only a marginal difference to annual inflation by now. And quite possibly that is so, but where is the questioning about what it would have taken – in terms of understanding the economy and the inflation process – to have kept core inflation inside the target range? What is it that they missed? (And when I say “they” of course I recognise that most everyone else, me included, also missed it and misunderstood it, but……central banks are charged by Parliaments with the job of keeping inflation at/near target, exercise huge discretion, carry all the prestige, and have big budgets for analytical purposes, so when central banks report on their performance, we should expect something much better than “well, we acted on the forecasts we had at the time and, with hindsight, those forecasts were (wildly) wrong”.) The question is why, what did they miss, and what have they learned that reduces the chances of future mistakes (including over the next year or two – if your model for how we got into this mess was so astray, why should the public have any confidence that you have the right model – understanding of the economy and inflation – for getting out of the mess? At the press conference the other day the Governor and the Board chair prattled on about being a “learning organisation” but you aren’t likely to have learned much if you never recognised the scale of the failure or shown any sign of digging deep in your thought, analysis, and willingness to engage in self-criticism. We – citizens – should have much more confidence in an organisation and chief executive will to do that sort of hard, uncomfortable, work than in one of the sort evident in last week’s report.

With hindsight one can make a pretty good case that no material monetary policy action was required at all in 2020. One might be more generous and say that by September/October 2020 with hindsight it was clear that what had been done was no longer needed. But that wasn’t the judgement the Reserve Bank came to at the time – and it is the Bank that has been tasked with getting these things right. Why? (And, of course, the same questions can be asked of other central banks and private forecasters, but the Reserve Bank is responsible for monetary policy and for inflation outcomes in this country.)

I may come back in subsequent posts to look at more detail at a number of specific aspects of the report (including a couple of genuinely interesting revelations) but at the big picture level the report does not even approach providing the sort of analysis and reflection the times and circumstances called for (in some easier times a report of this sort might have not been too bad, although you would always look for some serious research backing even then).

And if you think that I’m the only sceptic, I’d commend to you the comments from the former Deputy Governor of the Bank of Canada. On page after page – amid the politeness (and going along with distractions like the alleged role of the Russian invasion) – he highlights just how relatively weak the analysis in the report is, how many questions there still are, and a number of areas in which he thinks the Bank’s defensive spin is less than entirely convincing.

New Zealanders deserved better. That we did not get it in this report just highlights again that Orr is not really fit for the office he holds. In times like those of the last few years – with all the uncertainties – an openness to alternative perspectives, willingness to engage, willingness to self-critically reflect, and modelling a demand for analytical excellence are more important than ever.

Last week I reread Victoria University historian Jim McAloon’s history of New Zealand economic policymaking from 1945 to 1984, Judgements of all Kinds, first published a decade or so ago. Good works of economic history, let alone of the history of economic policymaking, aren’t thick on the ground in New Zealand, and as McAloon himself notes in a journal article published a year or two later:

“Economic history has a relatively low profile in New Zealand. Few economics programmes offer much in the way of economic history, and none of them offer courses in New Zealand economic history. Very few academics in New Zealand economics programmes publish in economic history. Victoria University, once boasting the only New Zealand chair in economic history, has largely abandoned the field.”

(Actually, when I was at Victoria in the early 80s – and not wise enough myself to have done much economic history – there were two professors of economic history)

Against this background of rather slim pickings, McAloon’s work is a useful contribution, including because he has gone back to at least some of the relevant archives. If you are at all interested in this period of New Zealand history – the backdrop in time to the post-1984 reforms and upheaval – I’d recommend the book, not because it is great or comprehensive but because it is (ie exists). In truth, although the title advertises coverage starting from 1945, there is quite a bit of material on economic policymaking in the 1930s and during the war too.

There is lots of interesting material, including about episodes few people now are particularly aware of (notably around the sterling area after the war). McAloon has his bugbears – not having much time for the British generally, or New Zealand farmers more specifically. And the phrase “the settler economy” keeps popping up, even when referring to events and developments decades after such a label had any more than rhetorical weight. I think he envisages the book as serving a somewhat revisionist purpose, in redeeming the tarnished reputation of the policymakers and advisers of the pre-1984 decades. I’m partial to a little of that sort of thing myself – for all his faults, for example, Muldoon clearly faced some of the most very adverse times to be a Minister of Finance almost throughout the 17 years that his terms spanned – but my sense is that McAloon sets himself rather too easy a target, in pushing back against some of the more florid rhetoric one still sometimes hears (from older politicians, economists, and business people) about the post-war New Zealand economy, and in the process acquits the policymakers, and most of their advisers, rather too readily. There is no doubt that the New Zealand economy in 1984 was a very different thing than it had been in 1945, and there had been plenty of sensible changes of policy made over the intervening decades. But the overall story remains one of deep relative decline, with no evident prospect of reversing that deterioration. And it wasn’t as if policymakers and advisers were innocents, unaware of the decline: by the very early 1960s serious independent reports from respected New Zealand economists were explicitly highlighting the extent of the relative productivity decline.

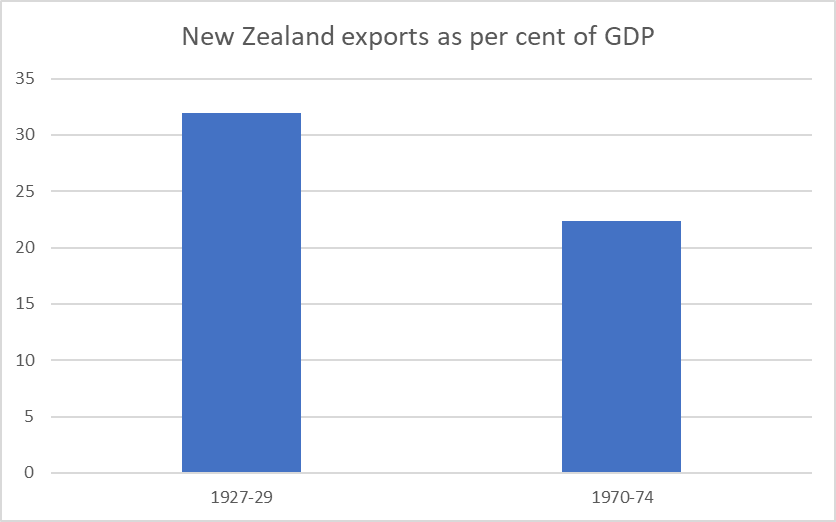

I’ve show numerous graphs here over the years highlighting New Zealand’s relative decline. But perhaps this simple one captures a significant aspect of what was going wrong. Read any book writing about inter-war New Zealand economic developments and it will make the point that per capita exports from New Zealand then were thought to be the highest of any country. That reflected a high level of GDP per capita and a high export share of GDP.

Consistent data over many decades is a challenge, but here are exports as a share of GDP as they were on the brink of the Great Depression (using as the GDP denominator the average of the three historical estimates on Infoshare) and by the early 1970s (using data from the OECD database).

By the early 1970s, not only had exports shrunk markedly as a share of New Zealand’s GDP, but that share was only around the median of the OECD countries (for which the OECD has data back that far), and that despite small countries typically trading more than large ones and New Zealand being in the smaller population grouping of OECD countries. One can debate the various possible causes of this steep relative decline, but New Zealand government policies did not, to say the least, help.

Anyway, the prompt to reading McAloon’s book again was that my son had been enrolled in McAloon’s second year New Zealand history course. If there are no specialist economic history courses at Victoria – which almost beggars belief given the way the university (and especially its commerce etc faculty) used to try to tout itself as preparing young people for careers in the public sector – at least there is some exposure to economic history topics in some of the history courses. Among the many essay topics students could choose from was one about New Zealand economic management from 1929 to 1975, and when my son chose to do that topic I suggested that reading the lecturer’s book might be worthwhile.

And here I divert into proud parent mode. I’ve included below the essay that Jonathan wrote on economic management over that period. I don’t agree with all of it (and had not read it until after the lecturer’s (high) marks came back) but – like the lecturer – I thought it was a pretty strong effort for a second-year student, and some of my readers may find the subject matter of interest. (And if anyone wants to hire a budding macroeconomist, he’ll probably be on the market in a couple of years.)

Controlling into Decline: Assessing government management of the New Zealand economy, 1929-1975.

by Jonathan Reddell

The period from 1929 to 1975 was an age of evolution in the New Zealand (NZ) economy. The upheavals of the Great Depression created a new consensus, while the economy continued to undergo the transition from a colonial to an independent economy. It cannot be said, however, that the period was an age of success. New Zealand’s relative decline during the period should not be understated. In 1939, New Zealand’s GDP per capita was $10,297, ahead of the Netherlands’ $7,079 and Canada’s $7,600. By 1975, both had surged ahead of New Zealand, as had others including Sweden.[1] New Zealand’s per capita growth rate lagged about 1% behind that of other developed market economies throughout the post-war period.[2] From 1929-1975, the performance of governments has been mixed, but that the economy was more often ill-managed than not. There are success stories, such as the diversification from Britain, and New Zealand remained one of the most prosperous countries on the planet, but on balance it was a drift into (relative) decline.

The role of the Great Depression in reshaping consensus economic thought in advanced capitalist economies is well known. The dislocations caused by the worst recession in modern history created the post-war consensus on full employment and the role of the state. This consensus would endure until the 1970s, when it was overturned by another crisis. New Zealand was no exception to this.[3] The following paragraphs will discuss government management of the Depression, and the new economic thought that was put into practice by the First Labour Government. The essay will then discuss the post-war consensus policies and assess how well governments managed the economy to achieve them.

The Depression’s impact on New Zealand was severe. A primary exporter, New Zealand was hard-hit by a shock whose hardest blow fell on commodities. Exports fell between 55-60% between 1928-29 and 32-33.[4] Rankin has estimated that joblessness peaked at over 35% of the workforce in 1932.[5] To compound matters, the New Zealand economy had been weakened by Britain’s anaemic economic performance in the 1920s due to the overvaluation of sterling from 1925.[6] Meanwhile the government’s ability to respond was constrained by the immense burden of public debt. In the 1931 Budget, public debt charges were by far the largest component of state expenditure, amounting to £10.9 million out of £24.7 million.[7] The debt burden and global loss of confidence severely constrained the government’s ability to borrow in London, while the inelastic debt payments meant that other sources of expenditure had to be cut, as a balanced budget was considered key to stability.[8]

While New Zealand did devalue against other currencies when Britain went off gold in September 1931, it did not devalue against sterling until 1933, prolonging the pain for exporters. From 1933, recovery was relatively rapid, as reforms including devaluation and the creation of a new monetary system under the Reserve Bank which allowed the Indemnity Act to lapse and monetary expansion while agricultural exports improved; by 1935 GDP per capita had recovered to the 1929 level.[9] Overall, the Coalition government’s management of the Depression was mixed. Belief in the desirability of a balanced budget constrained policy, as did the debt burden. On the other hand, the recovery was eventually strong, and as Hawke notes, actions were generally “sensible and sometimes imaginative.”[10] While it can be argued that the government could have taken more steps after Britain went off gold, overall, it is hard to argue with his judgement that, given the circumstances, the government did about as well as anyone else would have.[11]

By the time Labour came to power in 1935, the economy had generally recovered. Members of the new government had been greatly affected by the Depression and came to believe in the importance of boosting demand and that unemployment should never be allowed to reach such levels again.[12] Policy would be aimed at stabilisation, at security, at protecting the populace from the swings of the global economy. This would be achieved through polices such as expanded welfare and guaranteed prices for exporters. Nash wrote that the government, “intended to protect the producer…from the uncertainties of price.”[13] For dairy, this was done through the 1936 Primary Products Marketing Act. Labour perceived that the Depression illustrated New Zealand’s excessive vulnerability to the world economy, and aimed to counteract it, to ensure long term full employment. The state would lead industrial development to achieve both full employment and a less dependent economy. Labour’s policies marked a profound departure from the pre-Depression economy and created the basis of the post-war consensus which would last until 1975.[14] Stabilisation policy was locked in through the experiences of World War II (WW2), when the state took strong direct action and was generally successful.[15]

The post-war economic consensus consisted of several elements. National accepted the focus on full employment, and the welfare state, with Holland professing a belief that everyone had the right to employment and necessities.[16] A 1956 Royal Commission laid out the objectives of economic policy as: full employment, price stability, development, and promoting economic, social, and financial welfare of New Zealanders.[17] Governments from 1935 looked to manage the economy in pursuit of these goals, particularly full employment. The following paragraphs will assess their success regarding the economy.

The 1938-39 crisis was important in setting in the controls that would characterise the economy to 1984. From 1935 recovery continued apace, with GDP per capita one of the highest in the world in 1939. This would lead to crisis. The 1938-39 balance of payments crisis was a problem of the government’s own making, and a sign of things to come. Labour’s demand policies had resulted in a red-hot domestic economy, while a slowdown in the world economy resulted in a significant fall in export receipts. The trade balance fell from £10.5 million in 1937 to £2.9 million a year later.[18] Labour, unwilling to take actions that might harm workers like devaluation or fiscal retrenchment, opted for capital and import controls, which in some form would last until 1984. According to Hawke, the controls symbolised Labour’s move to an ‘insulationist’ economy.[19] The story of an overheated, full employment economy leading to a balance of payments crisis would be repeated periodically throughout the consensus period, including the crises of 1957-58 and 1966-67. The controls gave rise to a distorted economy and would have significant future negative impacts. Labour’s stabilisation policies undoubtedly had some value, but the obsession with full employment resulted in mismanagement in the 1930s, as it would again.

Post-depression governments would manage the economy with full employment front of mind. For Labour, it was, according to McAloon, “not negotiable.”[20] Speaking on the Employment Bill in 1945, Fraser said that “there is no greater tragedy than…being denied the opportunity,” to work, and being prevented from “contributing…to the production of goods and services.”[21] This undoubtedly succeeded, at least until the 1970s. From the late 1930s, the number of registered unemployed was incredibly low, bottoming out at 38 in 1950 and 1951.[22] While this number understates the true unemployment rate, estimates of that are as low as 1%.[23] This was a very low number by international standards.

While other countries also looked to achieve full employment, New Zealand’s unemployment was extremely low. For example, the United States, through the 1946 Employment Act declared a goal of “maximum employment.” However, even when the 1960s governments sought to make it a reality, unemployment never fell below 2.5%.[24] Therefore successive governments succeeded at managing the economy to achieve a level of full employment that was very low compared to other countries. A low unemployment rate has obvious benefits, but it also has costs. As was discussed, running a full employment economy with unemployment below the natural rate required import controls, to prevent domestic demand resulting in balance of payments crises. If unemployment had been allowed to rise to its natural level, which, as Gould notes, was likely quite low[25], the economy would have been less prone to fluctuations, whether in fiscal policy or the terms of trade, as demand for imports would have been generally weaker and there would have been less need for controls. Another negative of New Zealand’s extremely low unemployment rate was that fears of unemployment levels like other countries, particularly on the left, delayed NZ’s entry into the International Monetary Fund (IMF). Kirk exemplified those sentiments when he declared during the debate that NZ had “built up a social order that is unique,”[26] which IMF membership would imperil. In fact, non-membership of the IMF raised the cost of dealing with crises, while it did not prevent or cause higher unemployment.

Related to the full employment goal were import controls. As has been noted, successive governments looked to defend full employment while staving off balance of payments crises with import and capital controls, which would minimise the ability for New Zealand’s foreign reserves to drain. While National attempted to liberalise after 1949, controls were reimposed in 1951-52. These stop-go policies would repeat themselves, as the perceived foreign exchange constraint remained strong.[27] Import controls had major negative impacts. One was that import controls gave rise to import-substituting industries like textiles. These were often inefficient and misallocated resources away from potential export sectors. The high capital-output ratio of the economy through the 1950s and 1960s suggests inefficient usage, as it indicates a high level of capital was being used for low levels of output.[28] A 1968 World Bank report argued that “import restrictions are a hidden form of protectionism, which tend to result in a misallocation of resources,” and that they have failed to result in net exchange savings.[29] This seems believable as other sources have identified the high level of effective protection on NZ manufacturing, perhaps as high as 70% by the mid-1960s, and as a result, a functional tax on productive farmers, which weakened the NZ economy.[30]

While some level of control was understandable, particularly after WW2 given dollar shortages, New Zealand’s controls outlasted those of other OECD countries. Australia abolished import licencing in 1961.[31] A significant issue with New Zealand’s approach was the unwillingness to regard interest rates as a meaningful stabilisation tool. While many central banks abandoned interest rate control after WW2, New Zealand did not use interest rates even into the 1970s, while Australia had done so since the 1950s, due to factors including social credit influences and the sensitivity of farmers.[32] This had significant drawbacks because it meant more heavy-handed, distortionary controls were necessary to manage the economy. If interest rates, rather than direct controls, had been utilised as a policy tool, it seems likely that New Zealand’s relative decline would have been less marked. Easton argues that other OECD economies suffered from high protection of their agriculture sectors.[33] However, this mainly held up a dying industry and didn’t constrain the growth of industries like technology, while in New Zealand, controls raised the cost of inputs, effectively taxed agriculture, a growth sector, and allocated industrial capacity away from exports to import substitution.

The management of price stability is a mixed picture. An overheated economy continuously exerted inflation pressure. However, these pressures were mostly well constrained from the late 1940s. Condliffe observed that the New Zealand economy came out of WW2 “taut with supressed inflation.”[34] As wartime controls eased, inflation picked up to about 10% in 1947-48.[35] The government enacted several sensible measures to ease demand pressures and bring inflation down. These included a continued emphasis on national saving rather than overseas borrowing, which took money out of circulation, and the revaluation of 1948, which lowered the prices of exports and imports.[36] The New Zealand experience continued to be shaped by global conditions, as the Korean boom drove inflation to new heights in the early 1950s. While inflation fell and was generally relatively low between 1955 and 1970 it continued to be perceived as a threat. Hawke has observed that “prices rose by 2-3% in most years…worrying to many contemporaries.”[37] This perception is illustrated by a farmer, writing to the Press in 1961 that, “for the genuine farmer inflation is the worst thing that can happen.”[38] Thus, to the extent that governments are responsible for assuaging the fears of their citizens, NZ governments failed in that regard.

However, from a macroeconomic perspective, inflation was well managed until the late 1960s. The breakdown of the consensus between government, employers, and unions, particularly with the Nil Wage Order of 1968 was significant.[39] It combined with the overheated economy to produce significant levels of inflation that was managed inadequately through blunt instruments like freezes, due to ongoing full employment commitments. On balance, controlled inflation with overfull employment endured for a surprisingly long time. It is not clear, however, how much credit can be given to governments. New Zealand’s experience continued to be shaped by the global environment, and the inflation experience was similar to other countries, albeit at a lower level of unemployment.[40] A stronger factor seems to be the enduring legacy of Depression leading to a moderation of union militancy, which constrained wage, and thus price, inflation. However, governments do deserve at least some credit for keeping inflation as low as it was.

The third objective of economic policy was industrial development, which, from the mid-1950s linked with the need to diversify export markets as bulk purchase agreements ended in 1954 and Britain desired to join the European Economic Community. McAloon notes that “industrial development, trade development…were closely related over the decade after 1957.”[41] Industrial development was viewed as desirable from the late 1930s, as part of the quest to make New Zealand more insulated from price swings. This received greater focus under the Second Labour Government from 1957, particularly under the influence of Bill Sutch. Sutch wrote that “rapid and radical action is needed to readjust our economic structure,” towards manufacturing.[42] Sutch’s ideas reflected the flawed but orthodox view that there was a long-term decline in the terms of trade of commodity producers relative to industrial producers, known as the Prebisch-Singer thesis.[43] Its orthodoxy is illustrated by the World Bank’s report which argued that New Zealand’s fundamental problem was being “still too narrowly dependent on a few export commodities.”[44] Successive governments believed that industrial development was a priority, both for reducing balance of payments difficulties and maintaining prosperity.

The success of industrial development is a mixed picture. There were successful developments, such as the Kawerau pulp and paper mill and the wider forestry industry, and the domestic economy diversified throughout the 1960s. However, as was already noted, import controls resulted in misallocation towards import substitution, and experiments such as a cotton mill in Nelson were highly problematic.[45] The belief that too much agriculture was making New Zealand poorer seems particularly strange given that it remained the most productive industry.[46] The dominance of sheep and cow products did decline, from 90% of receipts in the 1930s to 53% in 1977/78, as new industries picked up: manufactured and forest products made up 23.4% of exports.[47] However, these exporters were often heavily subsidised, illustrated by the large incentives put on machinery in 1972.[48] These subsidies created their own inefficiencies. Again, governments were deploying distortionary solutions to questionably real problems. On the other hand, management of the diversification from Britain was successful. Trade agreements were signed with Japan in 1958, and significantly, with Australia in 1965.[49] Britain’s share of New Zealand exports fell from 51% in 1965 to 34% in 1971.[50] While there is much to criticise governments for how they handled the economy, they managed this landmark transition well, even if Britain’s relative economic marginalisation made trade readjustment inevitable.

In conclusion, the Depression shook the New Zealand economy, establishing a new order which sought full employment, price stability, and industrial development. While these were, for a time, achieved, it came at the cost of extensive controls which were a leading contributor to New Zealand’s relative decline. While successes like trade diversification cannot be overlooked, overall government management of the economy cannot be said to have been successful. The fundamental duty of government is to deliver prosperity and while New Zealand remained prosperous, it could have been much more so.

World Bank. The World Bank Report on the New Zealand Economy 1968. (1968).

Secondary Sources

Bernanke, Ben S. 21st Century Monetary Policy. New York: W.W. Norton & Company, 2022.

Bertram, Geoff. “The New Zealand Economy 1900-2000.” In The New Oxford History of New Zealand, edited by Giselle Byrnes, pp. 537-572. Melbourne: Oxford University Press, 2009.

Bloomfield, G.T. New Zealand: A Handbook of Historical Statistics. Boston: G.K Hall & Co., 1984.

Condliffe, J.B. The Welfare State in New Zealand. London: Allen and Unwin, 1959.

Easton, Brian. In Stormy Seas: The Post-War New Zealand Economy. Dunedin: University of Otago Press, 1997.

Gould, John. The Rake’s Progress? The New Zealand Economy Since 1945. Auckland: Hodder and Stoughton, 1982.

Greasley, David, and Les Oxley. “Regime Shift and Fast Recovery on the Periphery: New Zealand in the 1930s.” The Economic History Review 55, no. 4 (2002): pp. 697-720. https://doi.org/10.1111/1468-0289.00237

Gustafson, Barry. From the Cradle to the Grave. Auckland: Reed Methuen, 1986.

Hawke, G.R. The Making of New Zealand: An Economic History. Cambridge: Cambridge University Press, 1985.

Holland, Sidney. Passwords to Progress. Christchurch: Whitcombe and Tombs, 1943.