Way back in 1990 Parliament formally handed over the general responsibility for implementing monetary policy to the Reserve Bank. The government has always had the lead in setting the objectives the Bank is required to work to, and has the power to hire and fire if the Bank doesn’t do its job adequately, but a great deal of discretion has rested with the Bank. With power is supposed to come responsibility, transparency, and accountability.

And every so often in the intervening period there have been reviews. The Bank has itself done several over the years, looking (roughly speaking) at each past business cycle and, distinctly, what role monetary policy has played. These have generally been published as articles in the Bank’s Bulletin. When I looked back, I even found Adrian Orr’s name on one of the policy review articles and mine on another. It was a good initiative by the Bank, intended as some mix of contribution to debate, offering insights that were useful to the Bank itself, and defensive cover (there has rarely been a time over those decades when some controversy or other has not swirled around the Bank and monetary policy).

There have also been a couple of (broader-ranging) independent reviews. Both had some partisan intent, but one was a more serious effort than the other. When the Labour-led government took office in 1999 they had promised an independent review, partly in reaction to their sense that we had messed up over the previous few years. A leading Swedish academic economist Lars Svensson, who had written quite a bit about inflation targeting, was commissioned to do the review (you can read the report here). And towards the end of that government’s term – monetary policy (and the exchange rate) again being in the spotlight – Parliament’s Finance and Expenditure Committee did a review.

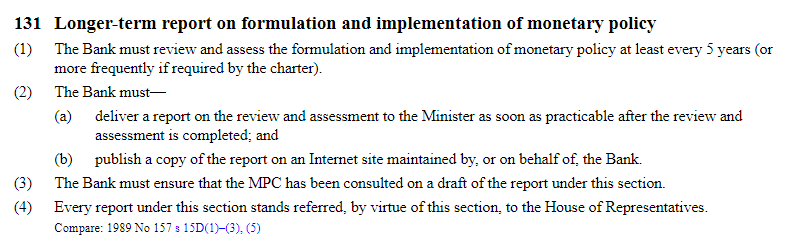

When the monetary policy provisions of the Reserve Bank Act were overhauled a few years ago this requirement was added

It made sense to separate out this provision explicitly from that for Monetary Policy Statements (in fact, I recall arguing for such an amendment years ago) but the clause has an odd feature: MPSs (and the conduct of monetary policy itself) are the responsibility of the MPC, but these five-yearly longer-term reviews are the responsibility of “the Bank”. In the Act, the Bank’s Board is responsible for evaluating the performance of both management and the MPC, but the emphasis here does not seem to be on the Board. It seems pretty clear that this is management’s document, and of course management (mainly the Governor) dominates the MPC. Since the Board has no expertise whatever in monetary policy, it is pretty clear that the first of these reports, released last week, really was, in effect, the Governor reporting on himself.

And although plenty of people have made scathing comments about that, there isn’t anything necessarily wrong about a report of that sort. After all, it isn’t uncommon (although I always thought it odious and unfair given the evident power imbalance) for managers to ask staff to write about notes on their own performance, as part of an annual performance appraisal, before the manager adds his/her perspective. The insights an employee can offer about his or her own performance can often be quite revealing. And it isn’t as if the Bank’s own take on its performance is ever going to be the only relevant perspective (although, of course, the Governor has far more resources and information at his disposal than anyone else is going to have). The only real question is how good a job the Bank has done of its self-review and what we learn from the documents.

On which note, I remain rather sceptical about the case (National in particular is making) for an independent review specifically on the recent conduct of monetary policy. Some of those advocating such an inquiry come across as if what they have in mind is something more akin to a final court verdict on the Bank’s handling of affairs – one decisive report that resolve all the points of contention. That sort of finality is hardly ever on offer – scholars are still debating aspects of the handling of the Great Depression – and if there was ever a time when choice of reviewer would largely determine the broad thrust of the review’s conclusions this would be among them. Anyone (or group) with the expertise to do a serious review will already have put their views on record – not necessarily about the RBNZ specifically (if they were an overseas hire) but about the handling of the last few years by central banks generally. There is precedent: the Svensson review (mentioned above) was a serious effort, but the key decision was made right at the start when Michael Cullen agreed to appoint someone who was generally sympathetic to the RB rather than some other people, some of equal eminence if different backgrounds, who were less so. It would be no different this time around (with the best will in the world all round). A review might throw up a few useful points and suggestions, and would probably do no harm, but at this point the idea is mostly a substantive distraction. Conclusions about the Reserve Bank and about its stewardship are now more a matter for New Zealand expert observers and the New Zealand political process (ideally the two might engage). Ideally, we might see some New Zealand economics academics weighing in, although in matters macroeconomics most are notable mainly by their absence from the public square.

That is a somewhat longwinded introduction to some thoughts about the report the Bank came out with last week (120 pages of it, plus some comments from their overseas reviewers, and a couple of other background staff papers).

I didn’t think the report presented the Bank in a very good light at all. And that isn’t because they concluded that monetary policy could/should (they alternate between the two) have been tightened earlier. That took no insight whatever, when your primary target is keeping inflation near the middle of the target range and actual core inflation ends up miles outside the range. Blind Freddy could recognise that monetary policy should have been tightened earlier. When humans make decisions, mistakes will happen.

The rest of the conclusions of the report were mostly almost equally obvious and/or banal (eg several along the lines of “we should understand the economy better” Really?). And, of course, we had the Minister of Finance – not exactly a disinterested party – spinning the report as follows: “It is really important to note that the report does indicate that they got the big decisions right”. It should take no more than two seconds thought to realise that that is simply not true: were it so we would not now have core inflation so far outside the target range and (as the report itself does note) pretty widespread public doubts about how quickly inflation will be got down again. It would be much closer to the truth to say that the Reserve Bank – and, no doubt, many of their peers abroad – got most of the big decisions wrong. It has, after all, been the worst miss in the 32 years our Reserve Bank has been independent, and across many countries probably the worst miss in the modern era of operationally independent central banks (in most countries, after all, monetary policy in the great inflation of the 1970s was presided over by Ministers of Finance not central banks).

But there is no sense in the report at all of the scale of the mistake, no sense of contrition, and – perhaps most importantly in my view – no insight as to why those mistakes were made, and not even any sign of any curiosity about the issue. The focus is almost entirely defensive, and shows no sense of any self-critical reflection. There are no fresh analytical insights and (again) not even any effort to frame the questions that might in time lead to those insights. And no doubt that is just the way the Governor (who has repeatedly told us he had ‘no regrets’) would have liked it. And here we are reminded that this is very much the Orr Reserve Bank: the two senior managers most responsible for the review (the chief economist and his boss, the deputy chief executive responsible for monetary policy and macroeconomics) only joined the Bank this year, and so had no personal responsibility for the analysis, preparation and policy of 2020 and 2021 but still produced a report offering so little insight and so much spin. Silk, in particular, probably had no capacity to do more, but the occasional hope still lingered that perhaps Paul Conway, the new chief economist, might do better. But these were Orr’s hires, and it is widely recognised that Orr brooks no dissent, no challenge, and in his almost five years as Governor has never offered any material insight himself on monetary policy or cyclical economic developments. Even if they had no better analysis to offer – and perhaps they didn’t, so degraded does the Bank’s capabilities now seem – contrition could have taken them some way. But nothing in the report suggests they feel in their bones the shame of having delivered New Zealanders 6 per cent core inflation, with all the arbitrary unexpected wealth redistributions that go with that, let alone the inevitable economic disruption now involved in bringing inflation a long way back down again. It comes across as more like a game to them: how can we put ourselves in the least bad light possible with a mid-market not-very-demanding audience (all made more unserious as we realised that the Minister of Finance had made the decision a couple of months ago to reappoint Orr, not even waiting for the 120 pages of spin).

At this juncture, a good report would be most unlikely to have had all the answers. After all, similar questions exist in a whole bunch of other countries/central banks, and if the Reserve Bank has the biggest team of macroeconomists in New Zealand, there are many more globally (in central banks, academe, and beyond) but it doesn’t take having all the answers to recognise the questions, or the scale of the mistakes. In fact, answers usually require an openness to questions, even about your own performance, first. And there is none of that in the Bank’s report.

Thus, we get lame lines – of the sort Conway ran several times at Thursday’s press conference – that if the Bank had tightened a bit more a bit earlier it would have made only a marginal difference to annual inflation by now. And quite possibly that is so, but where is the questioning about what it would have taken – in terms of understanding the economy and the inflation process – to have kept core inflation inside the target range? What is it that they missed? (And when I say “they” of course I recognise that most everyone else, me included, also missed it and misunderstood it, but……central banks are charged by Parliaments with the job of keeping inflation at/near target, exercise huge discretion, carry all the prestige, and have big budgets for analytical purposes, so when central banks report on their performance, we should expect something much better than “well, we acted on the forecasts we had at the time and, with hindsight, those forecasts were (wildly) wrong”.) The question is why, what did they miss, and what have they learned that reduces the chances of future mistakes (including over the next year or two – if your model for how we got into this mess was so astray, why should the public have any confidence that you have the right model – understanding of the economy and inflation – for getting out of the mess? At the press conference the other day the Governor and the Board chair prattled on about being a “learning organisation” but you aren’t likely to have learned much if you never recognised the scale of the failure or shown any sign of digging deep in your thought, analysis, and willingness to engage in self-criticism. We – citizens – should have much more confidence in an organisation and chief executive will to do that sort of hard, uncomfortable, work than in one of the sort evident in last week’s report.

With hindsight one can make a pretty good case that no material monetary policy action was required at all in 2020. One might be more generous and say that by September/October 2020 with hindsight it was clear that what had been done was no longer needed. But that wasn’t the judgement the Reserve Bank came to at the time – and it is the Bank that has been tasked with getting these things right. Why? (And, of course, the same questions can be asked of other central banks and private forecasters, but the Reserve Bank is responsible for monetary policy and for inflation outcomes in this country.)

I may come back in subsequent posts to look at more detail at a number of specific aspects of the report (including a couple of genuinely interesting revelations) but at the big picture level the report does not even approach providing the sort of analysis and reflection the times and circumstances called for (in some easier times a report of this sort might have not been too bad, although you would always look for some serious research backing even then).

And if you think that I’m the only sceptic, I’d commend to you the comments from the former Deputy Governor of the Bank of Canada. On page after page – amid the politeness (and going along with distractions like the alleged role of the Russian invasion) – he highlights just how relatively weak the analysis in the report is, how many questions there still are, and a number of areas in which he thinks the Bank’s defensive spin is less than entirely convincing.

New Zealanders deserved better. That we did not get it in this report just highlights again that Orr is not really fit for the office he holds. In times like those of the last few years – with all the uncertainties – an openness to alternative perspectives, willingness to engage, willingness to self-critically reflect, and modelling a demand for analytical excellence are more important than ever.

Hello Michael, I am an architect (retired mostly,79 years old) I know very little about economics, but have become more interested in the subject ever since 2009 when I found myself without work for the first time in my life. I read your comments and am amazed at your volume of output.

I have enjoyed my life as an architect and think you must be as fortunate as me, in that your subject, what you have been trained to do, what you have done most of your life, obviously still fascinates you. You are a fortunate man.

Keep up the good work, you are engaging me in the subject.

Regards Keith Leuschke (still Registered Architect, but not looking for any work)

LikeLike

Thanks Keith. Glad you are finding useful material here.

LikeLike

The review by the Bank of Canada official pushes back on the RBNZ spin. He says the BOC assessment is that Canada’s LSAP lowered the yield curve by 10 basis points. A RBA review assessed it at 30bp. So even at the higher end, the RBNZ program cost $300 million + for every 0.01% decline in bond yields ( for a total of $9.5 billion). The RBNZ should have stood aside and yet global forces do the heavy lifting…. instead they’ve lumbered NZ taxpayers with a huge loss.

LikeLiked by 1 person

Reblogged this on Utopia, you are standing in it!.

LikeLike