If you’d been given a great deal of delegated power and had messed up badly – not through any particular ill-intent, but perhaps you’d misjudged some important things or belatedly realised you didn’t have the knowledge to cope with an unexpected circumstance that you thought you had – and if you are anything like a normal decent person you would be extremely apologetic and quite contrite. Heck, borrow a friend’s car for the afternoon and come back with a dent in it – not even necessarily your fault – and most of us would be incredibly embarrassed and very apologetic. Bump into someone (literally) in the supermarket aisle and most of us will be quite apologetic – often enough proferring a “sorry” just in case, even if it is pretty clear it is the other person who knocked into us.

But the apparently sociopathic world of central banking seems to be different. The Reserve Bank (Governor and MPC) are delegated a great deal of power and influence. Back before the days of the MPC I used to describe the Governor as by far the most powerful unelected person in New Zealand (and more powerful individually than almost all elected people too). The powers – exercised for good or for ill – haven’t changed, they’ve just been (at least on paper) slightly diffused among a group of (mostly silent) people whose views we never quite know, and whose appointment is largely (effectively) controlled by the Govenor. (There was a nice piece in Stuff yesterday on the problems of the MPC, echoing many points made here over the years.)

It is not as if the Bank took on these powers reluctantly, or that the Governor had to have his arm twisted to do the job. The Bank championed the delegation (and reasonably enough) and every single member of the MPC took on the role – amply remunerated – entirely voluntarily. But they seem to have long since forgotten that counterpart to autonomy and operational independence that used to feature so prominently in all their literature, that great delegated power needs to be accompanied by serious accountability. Among decent people that would include evident contrition when things go wrong, no matter how good your intentions might have been, even if you thought you’d done just the best you personally could have.

The Auditor-General was reported yesterday raising concerns about the serious decline in standards of accountability in New Zealand public life. Whatever the situation elsewhere – and I have no reason to question the Auditor-General’s view – nowhere is it more evident than around the Reserve Bank, which exercises so much power with so few formal constraints. Much too little attention has been given to the fact that, having delegated them huge amounts of discretionary power to keep (core) inflation near 2 per cent, the Reserve Bank has messed up very badly over the last couple of years.

The issue here is not about intent or lack of goodwill, but about outcomes. When central banks were given operational autonomy it was on the implied promise that they’d deliver those sort of inflation outcomes, pretty much year in year out. The public wouldn’t need to worry about inflation because control of it – under a target set by elected politicians who would hold them to account – had been delegated to a specialist, notionally expert, agency, which would know what it was doing. 20 years ago the expectation on the Bank was fleshed out a little more: that they should do their job while avoiding unnecessary variability in interest rates, exchange rates, and output.

And what do we now have? Roughly 6 per cent core inflation, three years of annual headline inflation above the top of the target range, public doubts about just whether the Bank will deliver 2 per cent in future. Oh, and now the necessity (very belatedly acknowledged by the Bank yesterday) of a recession and a significant rise in unemployment to levels well beyond any sort of NAIRU to get inflation back in check. Add in the arbitrary wealth distributions – that no Parliament voted on – with the heavily indebted (including the government) benefiting from the unexpected surge of inflation the Reserve Bank has overseen, at the expense of those with financial savings. And the huge disruptions to lives and businesses from both the extremely overheated economy we’ve had for the last 12-18 months and the coming nasty shakeout. Oh, and that is not to mention more than in passing the $9.2 billion of LSAP losses the Reserve Bank up entirely unnecessarily (foreseeably).

It has not, to put it mildly, been the finest hour of the Reserve Bank. But there has been no a word of contrition – from the Governor or any of the rest of the Committee – and no real accountability at all (among other things, Orr and two of the MPC have been reappointed this year, with no sign of any searching scrutiny of their records or contributions).

Instead we just get lots of spin, and lightweight analysis. One of Orr’s favourite lines (repeated as I type at FEC this morning) is that the Reserve Bank was one of the very first central banks to tighten “by some considerable margin”, when in fact there were half a dozen OECD central banks that moved before our central bank did. We had claims from Orr a while ago that the macro benefits of the LSAP programme were “multiples” of those mark to market losses to taxpayers – a claim that quietly disappeared when they actually published their review of monetary policy. A few weeks ago Orr was telling Parliament that if it weren’t for the Ukraine war inflation would have been in the target range – notwithstanding the hard data showing core inflation was already very high well before the war – and then nothing more is heard of that claim when the MPS itself was published.

Yesterday we heard lots of bluster about workers, firms and households being enjoined to change their behaviour – even trying to damp down Christmas – as if inflation was the responsibility of the private sector, not the outcome of a succession of Bank choices and mistakes. But not a word from the Bank or Governor accepting any responsibility themselves.

To repeat, I don’t doubt that the Bank was well-intentioned throughout the last few years. Plenty of other people made similar mistakes in interpreting events. But it is the Reserve Bank and its MPC who are charged with – and paid for – the job of keeping the inflation rate and check. They’ve failed. Given that stuff-up they may now fix things up, but it is no consolation or offset to the initial huge series of mistakes. And not a word of contrition, barely even much acceptance of responsibility.

Which is a bit of a rant, but about a serious issue: with great power must go great responsibility, accountability….and a considerably degree of humility. Little or none has been evident here.

But what of the substance of the Monetary Policy Statement? Here I really had only three points.

The first is the glaring absence of any serious in-depth analysis of what has actually been going on with inflation, at a time of some of the biggest forecast errors – and revisions in the OCR outlook – we’ve seen for many years. For example, every chart seems to feature annual inflation, which is fine for headlines but tells you nothing about what has been happening within that one year period. What signs are there, for example, that quarterly core inflation might have peaked (or not) – eg some of the charts I included here? There seemed to be no disaggregated analysis at all, for example of the sort one economic analyst pointed to in comments here the other day. This from the organisation that is responsible for inflation, and which has by far the biggest team of macroeconomists in the country. We – and those paid to hold the Bank to account – really should expect better.

And almost equally absent was any persuasive supporting analysis for the really big lift in the forecast path of the OCR, now projected to peak at 5.5 per cent. My main point is not that I think they are wrong but that there is little or no recognition that having misread badly the last 2-3 years (in good company to be sure), there is little reason for them or us to have any particular confidence in their forecast view now. Models and sets of understandings that didn’t do well in preventing us getting into this mess probably haven’t suddenly become reliable for the getting out phase. But even granting that, the scale of the revision up seems disproportionate to the surprises in the new data of the last few months. It has the distinct feel of just another stab in the dark (but then I’ve been a long-term sceptic of the value of central bank OCR forecasts), with little engagement with either weakening forward indicators or the lags in the system (in the last 6 weeks the Bank has now increased the OCR by as much as it did in the first six months of the tightening cycle. With a recession already now finally in the forecasts based on what the MPC has already done (they don’t meet again until late February and the deepest forecast fall in GDP is in the quarter starting just 5 weeks later – the lags aren’t that short) they can’t really be very confident of how much more (if any) OCR action might be needed.

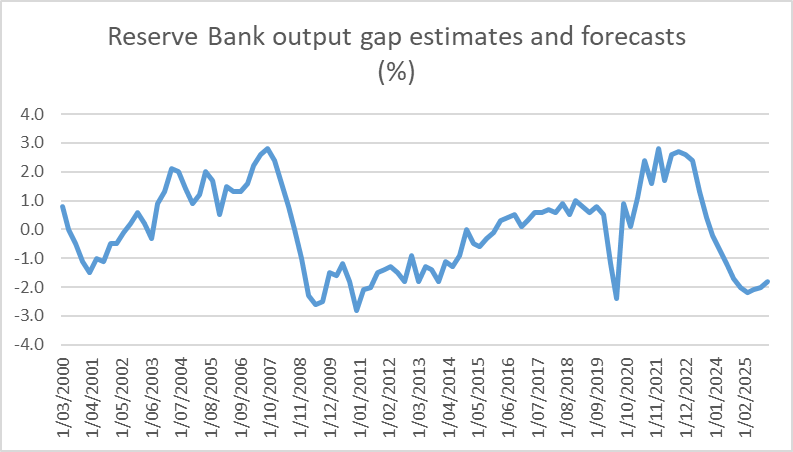

Finally, it is constantly worth bearing in mind the scale of the task. Core inflation has been running around 6 per cent and should be close to 2 per cent. That scale of reduction in core inflation hasn’t been needed/sought since around 1990. In 2007/08 inflation had got away on us to some extent, but a 1.5 percentage point reduction would have done the job of getting back to around 2 per cent. As Westpac pointed out in their commentary, the scale of the economic adjustment envisaged in these forecasts (change in estimated output gap) is very similar to what (the Bank now estimates) we experienced over 2008 to 2010.

The open question then is perhaps whether this sort of change in the output gap is likely to be sufficient: 13 years ago it delivered a 2 percentage point reduction in core inflation, but at present it looks as though we need a 4 percentage point reduction now. It isn’t obvious that other surrounding circumstances now will prove more propitious than then (eg for supply chains normalising now read the deep fall in world oil prices then).

Perhaps it will, perhaps it won’t, but you might have expected a rigorously analytical central bank and MPC to have attempted to shed some light on the issue. But once again they didn’t.

(My own money is probably on a deeper recession next year, here and abroad but……and it applies to me as much as to anyone else … if you got the last 2-3 years so wrong you have to be very modest in your claims to have the current and year-ahead story right.)