Last week I reread Victoria University historian Jim McAloon’s history of New Zealand economic policymaking from 1945 to 1984, Judgements of all Kinds, first published a decade or so ago. Good works of economic history, let alone of the history of economic policymaking, aren’t thick on the ground in New Zealand, and as McAloon himself notes in a journal article published a year or two later:

“Economic history has a relatively low profile in New Zealand. Few economics programmes offer much in the way of economic history, and none of them offer courses in New Zealand economic history. Very few academics in New Zealand economics programmes publish in economic history. Victoria University, once boasting the only New Zealand chair in economic history,

has largely abandoned the field.”

(Actually, when I was at Victoria in the early 80s – and not wise enough myself to have done much economic history – there were two professors of economic history)

Against this background of rather slim pickings, McAloon’s work is a useful contribution, including because he has gone back to at least some of the relevant archives. If you are at all interested in this period of New Zealand history – the backdrop in time to the post-1984 reforms and upheaval – I’d recommend the book, not because it is great or comprehensive but because it is (ie exists). In truth, although the title advertises coverage starting from 1945, there is quite a bit of material on economic policymaking in the 1930s and during the war too.

There is lots of interesting material, including about episodes few people now are particularly aware of (notably around the sterling area after the war). McAloon has his bugbears – not having much time for the British generally, or New Zealand farmers more specifically. And the phrase “the settler economy” keeps popping up, even when referring to events and developments decades after such a label had any more than rhetorical weight. I think he envisages the book as serving a somewhat revisionist purpose, in redeeming the tarnished reputation of the policymakers and advisers of the pre-1984 decades. I’m partial to a little of that sort of thing myself – for all his faults, for example, Muldoon clearly faced some of the most very adverse times to be a Minister of Finance almost throughout the 17 years that his terms spanned – but my sense is that McAloon sets himself rather too easy a target, in pushing back against some of the more florid rhetoric one still sometimes hears (from older politicians, economists, and business people) about the post-war New Zealand economy, and in the process acquits the policymakers, and most of their advisers, rather too readily. There is no doubt that the New Zealand economy in 1984 was a very different thing than it had been in 1945, and there had been plenty of sensible changes of policy made over the intervening decades. But the overall story remains one of deep relative decline, with no evident prospect of reversing that deterioration. And it wasn’t as if policymakers and advisers were innocents, unaware of the decline: by the very early 1960s serious independent reports from respected New Zealand economists were explicitly highlighting the extent of the relative productivity decline.

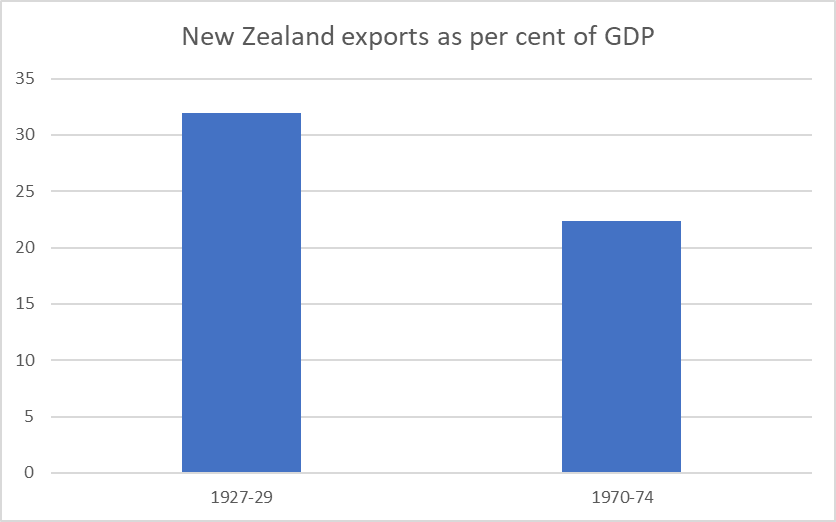

I’ve show numerous graphs here over the years highlighting New Zealand’s relative decline. But perhaps this simple one captures a significant aspect of what was going wrong. Read any book writing about inter-war New Zealand economic developments and it will make the point that per capita exports from New Zealand then were thought to be the highest of any country. That reflected a high level of GDP per capita and a high export share of GDP.

Consistent data over many decades is a challenge, but here are exports as a share of GDP as they were on the brink of the Great Depression (using as the GDP denominator the average of the three historical estimates on Infoshare) and by the early 1970s (using data from the OECD database).

By the early 1970s, not only had exports shrunk markedly as a share of New Zealand’s GDP, but that share was only around the median of the OECD countries (for which the OECD has data back that far), and that despite small countries typically trading more than large ones and New Zealand being in the smaller population grouping of OECD countries. One can debate the various possible causes of this steep relative decline, but New Zealand government policies did not, to say the least, help.

Anyway, the prompt to reading McAloon’s book again was that my son had been enrolled in McAloon’s second year New Zealand history course. If there are no specialist economic history courses at Victoria – which almost beggars belief given the way the university (and especially its commerce etc faculty) used to try to tout itself as preparing young people for careers in the public sector – at least there is some exposure to economic history topics in some of the history courses. Among the many essay topics students could choose from was one about New Zealand economic management from 1929 to 1975, and when my son chose to do that topic I suggested that reading the lecturer’s book might be worthwhile.

And here I divert into proud parent mode. I’ve included below the essay that Jonathan wrote on economic management over that period. I don’t agree with all of it (and had not read it until after the lecturer’s (high) marks came back) but – like the lecturer – I thought it was a pretty strong effort for a second-year student, and some of my readers may find the subject matter of interest. (And if anyone wants to hire a budding macroeconomist, he’ll probably be on the market in a couple of years.)

Controlling into Decline: Assessing government management of the New Zealand economy, 1929-1975.

by Jonathan Reddell

The period from 1929 to 1975 was an age of evolution in the New Zealand (NZ) economy. The upheavals of the Great Depression created a new consensus, while the economy continued to undergo the transition from a colonial to an independent economy. It cannot be said, however, that the period was an age of success. New Zealand’s relative decline during the period should not be understated. In 1939, New Zealand’s GDP per capita was $10,297, ahead of the Netherlands’ $7,079 and Canada’s $7,600. By 1975, both had surged ahead of New Zealand, as had others including Sweden.[1] New Zealand’s per capita growth rate lagged about 1% behind that of other developed market economies throughout the post-war period.[2] From 1929-1975, the performance of governments has been mixed, but that the economy was more often ill-managed than not. There are success stories, such as the diversification from Britain, and New Zealand remained one of the most prosperous countries on the planet, but on balance it was a drift into (relative) decline.

The role of the Great Depression in reshaping consensus economic thought in advanced capitalist economies is well known. The dislocations caused by the worst recession in modern history created the post-war consensus on full employment and the role of the state. This consensus would endure until the 1970s, when it was overturned by another crisis. New Zealand was no exception to this.[3] The following paragraphs will discuss government management of the Depression, and the new economic thought that was put into practice by the First Labour Government. The essay will then discuss the post-war consensus policies and assess how well governments managed the economy to achieve them.

The Depression’s impact on New Zealand was severe. A primary exporter, New Zealand was hard-hit by a shock whose hardest blow fell on commodities. Exports fell between 55-60% between 1928-29 and 32-33.[4] Rankin has estimated that joblessness peaked at over 35% of the workforce in 1932.[5] To compound matters, the New Zealand economy had been weakened by Britain’s anaemic economic performance in the 1920s due to the overvaluation of sterling from 1925.[6] Meanwhile the government’s ability to respond was constrained by the immense burden of public debt. In the 1931 Budget, public debt charges were by far the largest component of state expenditure, amounting to £10.9 million out of £24.7 million.[7] The debt burden and global loss of confidence severely constrained the government’s ability to borrow in London, while the inelastic debt payments meant that other sources of expenditure had to be cut, as a balanced budget was considered key to stability.[8]

While New Zealand did devalue against other currencies when Britain went off gold in September 1931, it did not devalue against sterling until 1933, prolonging the pain for exporters. From 1933, recovery was relatively rapid, as reforms including devaluation and the creation of a new monetary system under the Reserve Bank which allowed the Indemnity Act to lapse and monetary expansion while agricultural exports improved; by 1935 GDP per capita had recovered to the 1929 level.[9] Overall, the Coalition government’s management of the Depression was mixed. Belief in the desirability of a balanced budget constrained policy, as did the debt burden. On the other hand, the recovery was eventually strong, and as Hawke notes, actions were generally “sensible and sometimes imaginative.”[10] While it can be argued that the government could have taken more steps after Britain went off gold, overall, it is hard to argue with his judgement that, given the circumstances, the government did about as well as anyone else would have.[11]

By the time Labour came to power in 1935, the economy had generally recovered. Members of the new government had been greatly affected by the Depression and came to believe in the importance of boosting demand and that unemployment should never be allowed to reach such levels again.[12] Policy would be aimed at stabilisation, at security, at protecting the populace from the swings of the global economy. This would be achieved through polices such as expanded welfare and guaranteed prices for exporters. Nash wrote that the government, “intended to protect the producer…from the uncertainties of price.”[13] For dairy, this was done through the 1936 Primary Products Marketing Act. Labour perceived that the Depression illustrated New Zealand’s excessive vulnerability to the world economy, and aimed to counteract it, to ensure long term full employment. The state would lead industrial development to achieve both full employment and a less dependent economy. Labour’s policies marked a profound departure from the pre-Depression economy and created the basis of the post-war consensus which would last until 1975.[14] Stabilisation policy was locked in through the experiences of World War II (WW2), when the state took strong direct action and was generally successful.[15]

The post-war economic consensus consisted of several elements. National accepted the focus on full employment, and the welfare state, with Holland professing a belief that everyone had the right to employment and necessities.[16] A 1956 Royal Commission laid out the objectives of economic policy as: full employment, price stability, development, and promoting economic, social, and financial welfare of New Zealanders.[17] Governments from 1935 looked to manage the economy in pursuit of these goals, particularly full employment. The following paragraphs will assess their success regarding the economy.

The 1938-39 crisis was important in setting in the controls that would characterise the economy to 1984. From 1935 recovery continued apace, with GDP per capita one of the highest in the world in 1939. This would lead to crisis. The 1938-39 balance of payments crisis was a problem of the government’s own making, and a sign of things to come. Labour’s demand policies had resulted in a red-hot domestic economy, while a slowdown in the world economy resulted in a significant fall in export receipts. The trade balance fell from £10.5 million in 1937 to £2.9 million a year later.[18] Labour, unwilling to take actions that might harm workers like devaluation or fiscal retrenchment, opted for capital and import controls, which in some form would last until 1984. According to Hawke, the controls symbolised Labour’s move to an ‘insulationist’ economy.[19] The story of an overheated, full employment economy leading to a balance of payments crisis would be repeated periodically throughout the consensus period, including the crises of 1957-58 and 1966-67. The controls gave rise to a distorted economy and would have significant future negative impacts. Labour’s stabilisation policies undoubtedly had some value, but the obsession with full employment resulted in mismanagement in the 1930s, as it would again.

Post-depression governments would manage the economy with full employment front of mind. For Labour, it was, according to McAloon, “not negotiable.”[20] Speaking on the Employment Bill in 1945, Fraser said that “there is no greater tragedy than…being denied the opportunity,” to work, and being prevented from “contributing…to the production of goods and services.”[21] This undoubtedly succeeded, at least until the 1970s. From the late 1930s, the number of registered unemployed was incredibly low, bottoming out at 38 in 1950 and 1951.[22] While this number understates the true unemployment rate, estimates of that are as low as 1%.[23] This was a very low number by international standards.

While other countries also looked to achieve full employment, New Zealand’s unemployment was extremely low. For example, the United States, through the 1946 Employment Act declared a goal of “maximum employment.” However, even when the 1960s governments sought to make it a reality, unemployment never fell below 2.5%.[24] Therefore successive governments succeeded at managing the economy to achieve a level of full employment that was very low compared to other countries. A low unemployment rate has obvious benefits, but it also has costs. As was discussed, running a full employment economy with unemployment below the natural rate required import controls, to prevent domestic demand resulting in balance of payments crises. If unemployment had been allowed to rise to its natural level, which, as Gould notes, was likely quite low[25], the economy would have been less prone to fluctuations, whether in fiscal policy or the terms of trade, as demand for imports would have been generally weaker and there would have been less need for controls. Another negative of New Zealand’s extremely low unemployment rate was that fears of unemployment levels like other countries, particularly on the left, delayed NZ’s entry into the International Monetary Fund (IMF). Kirk exemplified those sentiments when he declared during the debate that NZ had “built up a social order that is unique,”[26] which IMF membership would imperil. In fact, non-membership of the IMF raised the cost of dealing with crises, while it did not prevent or cause higher unemployment.

Related to the full employment goal were import controls. As has been noted, successive governments looked to defend full employment while staving off balance of payments crises with import and capital controls, which would minimise the ability for New Zealand’s foreign reserves to drain. While National attempted to liberalise after 1949, controls were reimposed in 1951-52. These stop-go policies would repeat themselves, as the perceived foreign exchange constraint remained strong.[27] Import controls had major negative impacts. One was that import controls gave rise to import-substituting industries like textiles. These were often inefficient and misallocated resources away from potential export sectors. The high capital-output ratio of the economy through the 1950s and 1960s suggests inefficient usage, as it indicates a high level of capital was being used for low levels of output.[28] A 1968 World Bank report argued that “import restrictions are a hidden form of protectionism, which tend to result in a misallocation of resources,” and that they have failed to result in net exchange savings.[29] This seems believable as other sources have identified the high level of effective protection on NZ manufacturing, perhaps as high as 70% by the mid-1960s, and as a result, a functional tax on productive farmers, which weakened the NZ economy.[30]

While some level of control was understandable, particularly after WW2 given dollar shortages, New Zealand’s controls outlasted those of other OECD countries. Australia abolished import licencing in 1961.[31] A significant issue with New Zealand’s approach was the unwillingness to regard interest rates as a meaningful stabilisation tool. While many central banks abandoned interest rate control after WW2, New Zealand did not use interest rates even into the 1970s, while Australia had done so since the 1950s, due to factors including social credit influences and the sensitivity of farmers.[32] This had significant drawbacks because it meant more heavy-handed, distortionary controls were necessary to manage the economy. If interest rates, rather than direct controls, had been utilised as a policy tool, it seems likely that New Zealand’s relative decline would have been less marked. Easton argues that other OECD economies suffered from high protection of their agriculture sectors.[33] However, this mainly held up a dying industry and didn’t constrain the growth of industries like technology, while in New Zealand, controls raised the cost of inputs, effectively taxed agriculture, a growth sector, and allocated industrial capacity away from exports to import substitution.

The management of price stability is a mixed picture. An overheated economy continuously exerted inflation pressure. However, these pressures were mostly well constrained from the late 1940s. Condliffe observed that the New Zealand economy came out of WW2 “taut with supressed inflation.”[34] As wartime controls eased, inflation picked up to about 10% in 1947-48.[35] The government enacted several sensible measures to ease demand pressures and bring inflation down. These included a continued emphasis on national saving rather than overseas borrowing, which took money out of circulation, and the revaluation of 1948, which lowered the prices of exports and imports.[36] The New Zealand experience continued to be shaped by global conditions, as the Korean boom drove inflation to new heights in the early 1950s. While inflation fell and was generally relatively low between 1955 and 1970 it continued to be perceived as a threat. Hawke has observed that “prices rose by 2-3% in most years…worrying to many contemporaries.”[37] This perception is illustrated by a farmer, writing to the Press in 1961 that, “for the genuine farmer inflation is the worst thing that can happen.”[38] Thus, to the extent that governments are responsible for assuaging the fears of their citizens, NZ governments failed in that regard.

However, from a macroeconomic perspective, inflation was well managed until the late 1960s. The breakdown of the consensus between government, employers, and unions, particularly with the Nil Wage Order of 1968 was significant.[39] It combined with the overheated economy to produce significant levels of inflation that was managed inadequately through blunt instruments like freezes, due to ongoing full employment commitments. On balance, controlled inflation with overfull employment endured for a surprisingly long time. It is not clear, however, how much credit can be given to governments. New Zealand’s experience continued to be shaped by the global environment, and the inflation experience was similar to other countries, albeit at a lower level of unemployment.[40] A stronger factor seems to be the enduring legacy of Depression leading to a moderation of union militancy, which constrained wage, and thus price, inflation. However, governments do deserve at least some credit for keeping inflation as low as it was.

The third objective of economic policy was industrial development, which, from the mid-1950s linked with the need to diversify export markets as bulk purchase agreements ended in 1954 and Britain desired to join the European Economic Community. McAloon notes that “industrial development, trade development…were closely related over the decade after 1957.”[41] Industrial development was viewed as desirable from the late 1930s, as part of the quest to make New Zealand more insulated from price swings. This received greater focus under the Second Labour Government from 1957, particularly under the influence of Bill Sutch. Sutch wrote that “rapid and radical action is needed to readjust our economic structure,” towards manufacturing.[42] Sutch’s ideas reflected the flawed but orthodox view that there was a long-term decline in the terms of trade of commodity producers relative to industrial producers, known as the Prebisch-Singer thesis.[43] Its orthodoxy is illustrated by the World Bank’s report which argued that New Zealand’s fundamental problem was being “still too narrowly dependent on a few export commodities.”[44] Successive governments believed that industrial development was a priority, both for reducing balance of payments difficulties and maintaining prosperity.

The success of industrial development is a mixed picture. There were successful developments, such as the Kawerau pulp and paper mill and the wider forestry industry, and the domestic economy diversified throughout the 1960s. However, as was already noted, import controls resulted in misallocation towards import substitution, and experiments such as a cotton mill in Nelson were highly problematic.[45] The belief that too much agriculture was making New Zealand poorer seems particularly strange given that it remained the most productive industry.[46] The dominance of sheep and cow products did decline, from 90% of receipts in the 1930s to 53% in 1977/78, as new industries picked up: manufactured and forest products made up 23.4% of exports.[47] However, these exporters were often heavily subsidised, illustrated by the large incentives put on machinery in 1972.[48] These subsidies created their own inefficiencies. Again, governments were deploying distortionary solutions to questionably real problems. On the other hand, management of the diversification from Britain was successful. Trade agreements were signed with Japan in 1958, and significantly, with Australia in 1965.[49] Britain’s share of New Zealand exports fell from 51% in 1965 to 34% in 1971.[50] While there is much to criticise governments for how they handled the economy, they managed this landmark transition well, even if Britain’s relative economic marginalisation made trade readjustment inevitable.

In conclusion, the Depression shook the New Zealand economy, establishing a new order which sought full employment, price stability, and industrial development. While these were, for a time, achieved, it came at the cost of extensive controls which were a leading contributor to New Zealand’s relative decline. While successes like trade diversification cannot be overlooked, overall government management of the economy cannot be said to have been successful. The fundamental duty of government is to deliver prosperity and while New Zealand remained prosperous, it could have been much more so.

Bibliography

Primary Sources

Forbes, G.W., Minister of Finance. “Financial Statement.” Appendix to the Journal of the House of Representatives. (1931) https://paperspast.natlib.govt.nz/parliamentary/AJHR1931-I-II.2.1.3.8

New Zealand Parliamentary Debates. Vol. 270 (1945) & Vol. 326 (1960).

“Inflation.” Press, 6 July 1961, p. 3. https://paperspast.natlib.govt.nz/newspapers/CHP19610706.2.19.5?end_date=06-07-1961&query=Inflation&snippet=true&start_date=06-07-1961&title=CHP

Royal Commission on Monetary, Banking and Credit Systems. Report of the Royal Commission on Monetary, Banking, and Credit Systems. (1956). https://paperspast.natlib.govt.nz/books/ALMA1956-9915984483502836-Report-of-the-Royal-Commission-o?page_number=1&items_per_page=10&snippet=true

World Bank. The World Bank Report on the New Zealand Economy 1968. (1968).

Secondary Sources

Bernanke, Ben S. 21st Century Monetary Policy. New York: W.W. Norton & Company, 2022.

Bertram, Geoff. “The New Zealand Economy 1900-2000.” In The New Oxford History of New Zealand, edited by Giselle Byrnes, pp. 537-572. Melbourne: Oxford University Press, 2009.

Bloomfield, G.T. New Zealand: A Handbook of Historical Statistics. Boston: G.K Hall & Co., 1984.

Bolt, Jutta,and Jan Luiten van Zanden. “Maddison Project Database 2020.” 2020. https://www.rug.nl/ggdc/historicaldevelopment/maddison/releases/maddison-project-database-2020

Condliffe, J.B. The Welfare State in New Zealand. London: Allen and Unwin, 1959.

Easton, Brian. In Stormy Seas: The Post-War New Zealand Economy. Dunedin: University of Otago Press, 1997.

Gould, John. The Rake’s Progress? The New Zealand Economy Since 1945. Auckland: Hodder and Stoughton, 1982.

Greasley, David, and Les Oxley. “Regime Shift and Fast Recovery on the Periphery: New Zealand in the 1930s.” The Economic History Review 55, no. 4 (2002): pp. 697-720. https://doi.org/10.1111/1468-0289.00237

Gustafson, Barry. From the Cradle to the Grave. Auckland: Reed Methuen, 1986.

Hawke, G.R. The Making of New Zealand: An Economic History. Cambridge: Cambridge University Press, 1985.

Holland, Sidney. Passwords to Progress. Christchurch: Whitcombe and Tombs, 1943.

Kindleberger, Charles P. The World in Depression, 1929-1939. Revised Edition. Berkeley: University of California Press, 1986.

McAloon, Jim. Judgements of all Kinds: Economic Policy-Making in New Zealand 1945-1984. Wellington: Victoria University Press, 2013.

Nash, Walter. New Zealand: A Working Democracy. London: J.M Dent & Sons., 1944.

Rankin, Keith. “Workforce and Employment Estimates: New Zealand 1921-1939.” In Labour, Employment and Work in New Zealand, pp. 332-343, 1994.

Reddell, Michael, and Cath Sleeman. “Some perspectives on past recessions.” Reserve Bank of New Zealand, Bulletin, 71, no. 2 (2008): pp. 5-21.

Singleton, John, Arthur Grimes, Gary Hawke, and Frank Holmes. Innovation + Independence: The Reserve Bank of New Zealand 1973-2002. Auckland: Auckland University Press, 2006.

Statistics New Zealand. “Consumer Price Index.” https://infoshare.stats.govt.nz/Default.aspx

Sutch, W.B. “Colony or Nation? The Crisis of the Mid-1960s.” In Colony or Nation? edited by Michael Turnbull, pp. 163-183. Sydney: Sydney University Press, 1966.

Toye, John, and Richard Toye. “Origins and Interpretations of the Prebisch-Singer Thesis.” History of Political Economy 35, no. 3 (2003): pp. 437-467. muse.jhu.edu/article/46958.

[1] Figures in 2011 constant prices (USD). Jutta Bolt and Jan Luiten van Zanden. “Maddison Project Database 2020.” (2020) https://www.rug.nl/ggdc/historicaldevelopment/maddison/releases/maddison-project-database-2020

[2] John Gould, The Rake’s Progress? The New Zealand Economy Since 1945 (Auckland: Hodder and Stoughton, 1982), p. 25.

[3] Jim McAloon, Judgements of all Kinds: Economic Policy-Making in New Zealand 1945-1984 (Wellington: Victoria University Press, 2013), p. 22.

[4] Charles P. Kindleberger, The World in Depression: 1929-1939 revised edition (Berkeley: University of California Press, 1986), p. 189.

[5] Keith Rankin, “Workforce and Employment Estimates: New Zealand 1921-1939,” Labour, Employment and Work in New Zealand (1994), p. 338.

[6] McAloon, Judgements of all Kinds, p. 34.

[7] G.W. Forbes, Minister of Finance “Financial Statement” (1931) AJHR B-06, p. 4. https://paperspast.natlib.govt.nz/parliamentary/AJHR1931-I-II.2.1.3.8

[8] Michael Reddell and Cath Sleeman, “Some perspectives on past recessions,” Reserve Bank of New Zealand: Bulletin 71, no.2 (2008), p. 7.

[9] David Greasley and Les Oxley, “Regime shift and fast recovery on the periphery: New Zealand in the 1930s,” The Economic History Review 55, no.4 (2002), pp. 709-710.

[10] G.R. Hawke, The Making of New Zealand: An Economic History (Cambridge: Cambridge University Press, 1985), p .158.

[11] Ibid., p. 159.

[12] Barry Gustafson, From the Cradle to the Grave (Auckland: Reed Methuen, 1986), pp. 146-147.

[13] Walter Nash, New Zealand: A Working Democracy (London: J.M Dent & Sons, 1944), p. 130.

[14] McAloon, Judgements of all Kinds, pp. 51-52.

[15] Ibid., p. 52.

[16] Sidney Holland, Passwords to Progress (Christchurch: Whitcombe and Tombs, 1943), p. 7.

[17] Royal Commission on Monetary, Banking, and Credit Systems, Report of the Royal Commission on Monetary, Banking and Credit Systems (1956), p. 19. https://paperspast.natlib.govt.nz/books/ALMA1956-9915984483502836-Report-of-the-Royal-Commission-o?page_number=1&items_per_page=10&snippet=true

[18] G.T. Bloomfield, New Zealand: A Handbook of Historical Statistics (Boston: G.K Hall & Co., 1984), p. 269.

[19] Hawke, The Making of New Zealand, pp. 163-164.

[20] McAloon, Judgments of all Kinds, p. 44

[21] NZPD, 1945: Vol. 270, p. 249 (Rt. Hon P. Fraser)

[22] Bloomfield, Handbook of Historical Statistics, p. 146.

[23] Gould, The Rake’s Progress, p. 56.

[24] Ben S. Bernanke, 21st Century Monetary Policy (New York: W.W. Norton & Company, 2022), p. 18.

[25] Gould, The Rake’s Progress, p. 58.

[26] NZPD, 1960: Vol. 326, p. 1130 (Kirk)

[27] Hawke, The Making of New Zealand, p. 205.

[28] Ibid., p. 176.

[29] World Bank, The World Bank Report on the New Zealand Economy 1968 (1968), pp. 44-45.

[30] Geoff Bertram, “The New Zealand Economy: 1900-2000,” in The New Oxford History of New Zealand, ed. Giselle Byrnes (Melbourne: Oxford University Press, 2009), p. 557.

[31] John Singleton et al., Innovation + Independence: The Reserve Bank of New Zealand 1973-2002 (Auckland: Auckland University Press, 2006), pp. 17-21.

[32] Ibid., pp. 23-26.

[33] Brian Easton, In Stormy Seas: The Post-War New Zealand Economy (Dunedin: University of Otago Press, 1997), p. 178.

[34] J.B Condliffe, The Welfare State in New Zealand (London: Allen and Unwin, 1959), p. 99.

[35] Statistics New Zealand, “Consumer Price Index,” https://infoshare.stats.govt.nz/Default.aspx

[36] McAloon, Judgements of all Kinds, p. 75; Gould, The Rake’s Progress, pp. 52-53.

[37] Hawke, The Making of New Zealand, p. 174.

[38] “Inflation,” Press, 6 July 1961, p. 3. https://paperspast.natlib.govt.nz/newspapers/CHP19610706.2.19.5?end_date=06-07-1961&query=Inflation&snippet=true&start_date=06-07-1961&title=CHP

[39] McAloon, Judgements of all Kinds, pp. 135-136.

[40] Hawke, The Making of New Zealand, p. 174.

[41] McAloon, Judgements of all Kinds, p. 110.

[42] W.B. Sutch, “Colony or Nation? The Crisis of the Mid-1960s,” in Colony or Nation?, ed. Michael Turnbull (Sydney: Sydney University Press, 1966), p. 183.

[43] John Toye and Richard Toye, “The Origins and Interpretation of the Prebisch-Singer Thesis,” History of Political Economy 35, no. 3 (2003), p. 437.

[44] World Bank, Report on the New Zealand Economy, p. 20.

[45] McAloon, Judgements of all Kinds, pp.112-115.

[46] Hawke, The Making of New Zealand, p. 176.

[47] Gould, The Rake’s Progress, p. 159.

[48] McAloon, Judgements of all Kinds, p. 146

[49] Ibid., pp. 121-123.

[50] Ibid., p. 143.

Reblogged this on Utopia, you are standing in it!.

LikeLike

Michael,

It is a very good essay. Like you I would disagree on some points but more in differences of emphasis than anything fundamental. For example, the issue about NZ joining the IMF was not just about Labour’s commitment to full employment, but also National’s inclusion of “British Loyalists”. It was because both political parties were divided that it was difficult get a clear focus. Cf G.R. Hawke and B.A.D. Wijewardane ‘New Zealand and the International Monetary Fund’ Econ. Record 48 (March, 1972), pp. 92-102

There was only one “established” chair of economic history. Mine was a “personal” chair until I succeeded John in his established chair. I think the distinction between personal and established chairs has been discarded but I define retirement as having no concern in university management.

Best wishes

Gary

Professor Gary Hawke 7 Voltaire St., Karori, Wellington Tel + 64 4 4769109 + 64 27 563 5794 ________________________________

LikeLike

Thanks Gary. Yes,I’d had a similar reaction on the IMF point, but always remember being struck reading the 1961 parliamentary debate how much at that point the perceived risk of recessions and unemployment was being played up by Oppn MPs then ( I think Australia was in recession in 1961?)

LikeLike

Super interesting summary – and a great 2nd year essay! This stat caught my eye:

“In the 1931 Budget, public debt charges were by far the largest component of state expenditure, amounting to £10.9 million out of £24.7 million”.

Someone should work out this stat for each of our territorial local authorities. Making that known to local ratepayers might change some of the public opposition to 3 Waters if folks understood that nearly 50% of their rates bill related to interest + depreciation (should that be the case… I’ve never looked at it – so am just guessing some may well be in that kind of financial position).

LikeLike

There’s nothing good about the whole thing Kate. Hoodwinking the public over the costs and liabilities and risks would just be more lies among many.

The councils will, for the most part, still be left with their debt. Meanwhile the new centralised water authorities are set to be borrowing big time.

Three Waters and One Mountain of Debt:

“…..the proposed co-governance structure is in fact the ‘Tainui governance model’. In essence, we are combining Tainui co-governance with Macquarie-style leveraged financing. Such an unusual mix of massive debt allied to an untested model of governance is, in my professional opinion, a recipe for disaster. And a disaster that could easily turn out to be ruinous for the country’s finances.

It is a view supported by the Castalia report to C4LD which concludes:

The mega entities increase Crown fiscal risk. Because the Crown is effectively providing a credit backstop, and creditors’ powers are reduced relative to current local authority borrowing, the Crown is exposed to increased risk of mega entity failure. This risk is increased due to a combination of key factors, which we elaborate on below: complex governance and competing objectives dilute accountability of mega entity management to the directors, and ultimately customers …”

https://cranmer.substack.com/p/three-waters-and-one-mountain-of

LikeLike

Yes, I’m really neither one way or the other on the 3W proposal (and yes, I agree that the governance issues have become more front-of-mind than the infrastructure issues).

I’m just aware of the fact that infrastructure costs going forward have to be met by someone, and it’s probably better funded centrally, given local authorities have to write balanced budgets – meaning they can only raise rates, or decide not to do the maintenance and renewals (which is what has occurred to date).

Whereas central government can write either a deficit or a surplus budget – so has more flexibility in that regard. I certainly agree with the above insights – the debt that will be needed is enormous, and yes, highly risky under an untested governance model.

LikeLike