The Reserve Bank’s Monetary Policy Committee has its final meeting for the year on Wednesday, and then they shut up shop. For a long time. The next scheduled announcement is not until 22 February, a full 13 weeks (3 months) away. Nice job if you can get it, and although I’m sure management and staff will still be working for much of the intervening period, the same is unlikely to be said for the three non-executive members, who are generously remunerated by the taxpayer, utterly invisible, and only need to show up when meetings are scheduled.

This strange schedule has been in place for quite a few years now, having been adopted at a time when the OCR wasn’t being moved much at all (and when the Bank was raising the OCR, it often proved to have been a mistake). But having been in place for a while does not make it any more defensible or sensible. In fact, last year’s three month summer break almost certainly was one factor in how slow the MPC was to get on with raising the OCR once they’d finally made a start. On no reading of the data (contemporary data that is) did it make sense for us to have ended 2021 with the OCR still lower, in nominal terms, than it had been just prior to Covid. And having experienced the issue last summer (when perhaps it caught them by surprise) there was no excuse for not resetting the schedule for this summer.

One can always mount defences (for almost anything I suppose). Monetary policy works with a lag, the OCR adjustments can be just as large as they have to be, perhaps there is a bit of a tradeoff between time doing analysis and time spent preparing for meetings. But none of it is very convincing in this context. And it is out of step with their peers.

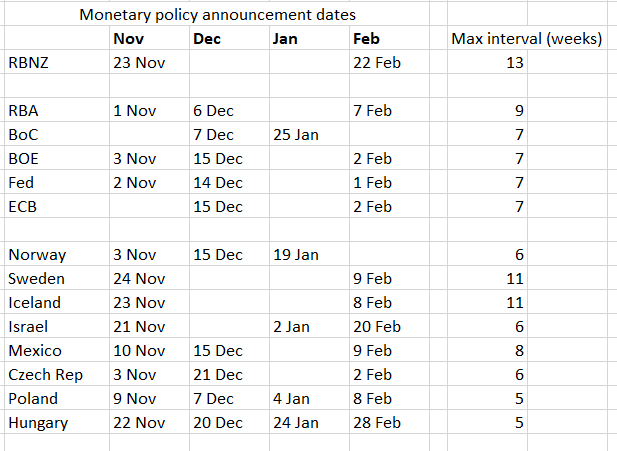

Here is a table of the monetary policy announcements dates over November to February for a fairly wide range of OECD country central banks. None, not even Sweden and tiny Iceland, are taking as long a break as our MPC (and although I didn’t tot up all the northern hemisphere summer meeting dates, it didn’t look as though any took as long a break then as our MPC takes now). The median country has a longest gap of seven weeks between meetings over this period.

[UPDATE: In addition, the South Korean central bank meets on 24 Nov, 13 Jan, and 23 Feb]

There are substantive macroeconomic arguments for (and against) a 75 basis point OCR adjustment this week, but one of arguments some have advanced is that they really need to go 75 basis points this week because they don’t have another opportunity until late February. But whose fault is that? It is entirely an MPC choice. They have a very flexible instrument and just choose to tie their hands behind their backs to give themselves a very long summer break.

The whole situation is compounded by the inadequacies of New Zealand’s key bits of macroeconomic data. We now have the CPI and the unemployment rate for mid-August (the midpoint of the September quarter). Most OECD central banks already have October CPI data, almost all have September unemployment rate data (and several have October unemployment rate data), and three-quarters of OECD countries already have September quarter GDP data (a few even have monthly GDP estimates).

The combination of slow and inadequate data and widely-spaced summer meetings really isn’t good enough, especially at a time when there is so much (perhaps inevitable) uncertainty about the inflation situation and outlook. The inadequacies of our national macroeconomic statistics cannot be fixed in short order (not that the government shows any interest in doing so anyway). But how often, and when, the MPC meets is entirely at the Committee’s discretion, and easily altered with little or no disruption other than to the holiday plans of some appointed and (supposedly) accountable policymakers (people who not incidentially – and pardonably or otherwise – have done such a demonstrably poor job of their main responsibility, keeping core inflation in the target range, in recent times.

The MPC should be announcing on Wednesday (a) an extra OCR review for a few days after the CPI release in January, and (b) a commitment to revisit the meeting schedule for future years to bring the length of the long summer break back to (say) no longer than the one the RBA takes. If they don’t journalists at the press conference and MPs at FEC should be asking why not.

(Writing this post brought to mind memories of Orr 20+ years ago when the OCR was first introduced championing having only four reviews a year. The OCR then was new, inflation was low and stable. One hopes that sort of thinking no longer lurks in the back of the Governor’s mind.)

All very good points.

the speed of the world has changed drastically over the last 20 years. Instant information results in instant reactions.

LikeLike

Reblogged this on Utopia, you are standing in it!.

LikeLike

Michael, this prompts me to follow the MPC’s example and get in early with my end-of-year thanks for your persistent and excellent explanation & analysis of the decisions taken by the Reserve Bank & the Government over the past 3 years. Enabling a non-economist like me to talk about Large Scale Asset Purchases with a fair idea of what they are is quite a feat!

But seriously, you have done incredibly valuable & important work shedding light on actions & behaviour that others, paid and/or elected by New Zealanders, would prefer to gloss over, ignore or hide. If we had a Speaking Truth to Power award for 2022 you would definitely get my vote!

LikeLiked by 1 person

[…] Source link […]

LikeLike

Aside from the fact that the RB is standing at the back of the boat seeing where the waves were earlier then making stabs at the future, it is likely they will only know when they have killed price inflation when the patient (economy)dies. This silly game of institutional independence fools no one and frankly the NZ economy could fall off the face and nobody would care except the government’s fundraising operation ,IRD.

Throw the whole monetary central planning operation out the back and lets see what the market thinks of us.

The real world could be too harsh for an interventionist Finance minister supported by the collective cabinet.

But I thank you for your efforts Michael in making the whole Keynesian circus glaringly exposed to rational thought.

Still think we are on the road to Honiara.

LikeLike

Over the past year, having more frequent meetings might have been beneficial. But, can you imagine the muck-up that would have occurred in 2010 and again in 2014 if the RBNZ had had more frequent meetings, the policy mistakes would have been compounded.

I think the case can be made for a meeting in January, or spacing the meetings slightly differently, but lots of meetings isn’t necessary, IMHO.

Also, right now, there’s a clear panic going on in NZ over inflation, but some of the thinking and chatter on it is just woolly headed. For instance, around 40bp of the CPI up-lift can be explained by StatsNZ going back to pre-pandemic weights and doing price level adjustments to airfares and accommodation, that won’t be repeated. Flow data point to slowing rental cost pressures – rent being one of the two jumbo items in the CPI – petrol price pressures are easing, used car prices are falling back, real estate agent’s fees getting crushed, vegetable prices are up largely on La Nina – cabbage prices up 73%y/y have nothing to do with Adrian Orr – international prices in NZD terms for meat, dairy, cooking oils, tea and coffee are all DOWN and will flow through to the CPI. And underneath all of this are massive base-effects. I’ve not seen ONE story in NZ actually explaining any of this. What I see is panic, alarm and ZERO analysis, including from all four big banks. But then, why am I not surprised?

LikeLike

In general I prefer the RBA model of monthly meetings (but quarterly MPSs) but even 8 a year as the RB used to do would be much better. We can’t fix forecasting/policy mistakes by having fewer meetings, but by (notably) appointing better people and building stronger institutions.

The coverage of the inflation situation in NZ is weak. Nonetheless, and even recognising that the unemployment rate is a modestly lagging indicator, core domestic pressure on resources has remained fairly intense, and it is a long way from 6% (midpoint of the various core measures in annual terms) and 2%. And for better or worse the Bank, having damaged its own reputation, now has to deal with the further risks associated with the recent lift in inflation expectations measures.

LikeLike

Points noted Michael.

I don’t have a strong axe regarding meeting dates, maybe one more meeting slotted in would be useful, but I think the bigger issue is forecasting and policymaking.

I’ve been through the CPI with a fine tooth comb, its not the case that New Zealand might see a drop in inflation, it’s that it absolutely will.

Food prices will contribute about 1.8pp to inflation in Q4, but that should be the peak. As La Nina fades, we should see a correction in fruit & vegetable prices – which have also been impacted by shipping and labour issues, and there’s good reason to expect a zero-to-negative contribution to inflation from them in the coming year. Grocery items have been boosted by rising international commodity prices but wheat, dairy, meat, tea, coffee, cooking oil prices are all well off their highs and that will feed into the CPI. The remainder of the food group tends to follow the volatile items, so that should also soften. And food has big base effects. We could easily see the contribution from Food drop to around 0.2-0.3pp in the next year.

Alcohol prices have been boosted by the re-opening of the economy and I don’t see that ‘adding’ to inflation, it will be a wash, likewise cigarettes. Apparel prices should remain modest and have a modest weigh in the CPI, just not going to move the dial.

Housing is the big one. The flow of new rental agreements is falling and the stock should moderate, so we should see rental inflation ease, not a lot, but some. New Dwelling prices have tracked existing house prices as far back as 1988 (data limitations) and inflation here should come to a screeching halt, which, given base effects, is a big deal. Easing supply constraints and slower residential construction should slow the rate of inflation in construction costs, local authority rates will soften and utilities cost inflation is flat.

… I can go on if you wish…

As for the labour market, labour demand is going to soften – the ANZ Business Outlook is already showing us that, and labour supply will recover as absenteeism drops, migrant workers are coming in, the flood of young NZers leaving slows and students arrive…. wage pressure (LCI) is consistent with the historical Phillips curve. And then we have an absolutely massive payments shock impacting us… 75bp rate hike, yes sure its possible – indeed probable given the nonsense being written by the local banks, but it would be crazy… running from one side of the boat to the other.

LikeLike

Thanks Peter. Entirely agree inflation will fall. But it needs to, a long way, and on a core basis. At this point – and with no meeting for 3 mths – I’m less bothered by 75bps this week (for which there may be little real downside) than where to from there. As things stand at present, there seems a reasonable chance that 75bps now should/could be “one more and done”. (Perhaps one place we differ tho is that I think the NZ macro evidence is strongly supportive of a view that increased net migration inflows will add to excess demand, not relieve it).

LikeLike

As you can tell, I think 75bp at this juncture would be mad.

In retrospect, 75bp may have been justified to get quickly off the effective lower bound last year, but hindsight is a wonderful thing.

As said, I can go on right through the CPI, right through the labour market stats, and the housing stats, and the banking stats, they’re all telling us the same story. The economy is set to slow sharply in GNE (perhaps not GDP because of the export of services), and inflation, including core, is going to come down hard.

For my clients, 75bp would be great as it sets up a wonderful entry point to receive NZD rates vs Australia and to buy AUD/NZD. So im not personally too worried (also have zero personal exposure being located offshore)…but its a mistake.

LikeLike

Certainly agree the compelling time for a really large increase was last November, or even Feb 22.

Time will, as always, tell.

LikeLike

The RB is best described by Robbie Burns comment “ wee sleekit timerous beastie “

Too little too late seems to be their mantra recently.

Results :poor productivity, (destined to get worse with HWEN etc..), a wage / price spiral revving up and getting into 2nd gear. Exchange rate woes as NZD reflects sub par economic activity here ,including out of hand growth in public/ government spending.Government and bureaucratic regulation.

Perhaps the Reserve Bank Monetary Policy and the OCR settings could or even should be taken over by a very sophisticated electronic program which could mean a higher level of genuine independence.

Given man’s ingenuity there is no doubt such a program would be gamed in time but, at least for a while ,there would be some certainty

LikeLike

Ten of the senior executives have anything from $400k to $830k to spend, and it will require an inordinate amount of time and effort (unlike their actual titled jobs) to do this justice. Not for them the stress of paying: interest on mortgages ( on houses that are now in negative equity) or small business loans (which borrowers were to emboldened to be ‘brave’ in taking on); and grocery & fuel bills ( well that’s all the fault of those Russians)….that’s for the common people.

A three-month break to indulge in some discretionary spending seems entirely ‘reasonable’ to compensate for the wearing of the heavy crown of ‘stewardship’ over New Zealand’s economy. And with all that spare time perhaps they might also get a few good books to read over the break as well. Here’s a suggestion: ‘Economics for Dummies. 3rd Edition’….only NZ$ 28.90 on Kindle…buy now before prices go up.

Time for the RBNZ to rebrand their motto of ‘securitas et vigilantia’ to ‘hic manebimus optime’

Chugging on the mahi indeed.

LikeLike

To extent the RB’s Tane Mahuta metaphor, it appears the forest will be ringing with the sound of tātarakihi over the summer break (crickets).

LikeLiked by 1 person