In my post last Friday I highlighted how the Governor of the Reserve Bank had just been making up stuff, and apparently knowingly misleading Parliament, to distract from the Bank’s own responsibility for New Zealand’s current very high core inflation. There may well be a case to be made that central banks did about as well as could reasonably be expected over the last couple of years – “reasonably be expected” here set by reference to the general views at the time of other expert observers (none of whom, admittedly, had chosen to take on statutory responsibility for inflation) but simply making stuff up blaming the Moscow bogeyman helps no one, and detracts from any serious conversation about what went on with inflation – core and headline – and why. To put my own cards on the table, there are many reasons why Adrian Orr should not be reappointed, but the poor inflation outcomes are not the most important of those reasons (of course, a superlative performance on inflation might have covered over a multitude of other sins and shortcomings).

After Friday’s post, someone got in touch to point out that I had not mentioned one other episode in that FEC appearance which could also reasonably be described as “making stuff up” and misleading Parliament. Opposition members were asking questions that included that rather loaded phrase “printing money”, to which Orr responded – apparently in reference to the LSAP – that the Reserve Bank did not create money, that all they did was to lower bond yields, and that banks etc were the people who increased the money supply.

In normal circumstances, the Governor’s comment would not be far wrong. The “money supply” – deposits with financial intermediaries (those included in the Bank’s survey) held by “the public” (ie people and firms not themselves included in the survey) – mostly increases in the process of private sector credit creation. For example, each new mortgage to purchase a house results simultaneously in the creation of either a deposit or a reduction in another mortgage as the house seller deals with the proceeds of the sale. Monetary policy operates typically by adjusting interest rates to influence, among other things, the demand for credit.

Some of the Reserve Bank’s emergency crisis tools don’t have any direct effect on the money supply measures the Reserve Bank compiles and reports. The Funding for Lending programme – a crisis programme that bizarrely is still injecting cheap liquidity now – simply lends money to banks (against collateral). That transaction boosts settlement cash balances held by banks at the Reserve Bank, but those balances aren’t part of “money supply” measures (they are deposits held by one lot of surveyed institutions – banks – at another surveyed institution – the Reserve Bank).

The LSAP is different. If, for example, a pension fund had been holding government bonds and had then sold those bonds to the Reserve Bank. the pension fund would receive payment from the Reserve Bank in a form that adds to that pension fund’s deposits at a bank. Settlement cash balances increase in the process, but so does the money supply (the pension fund’s deposits count in the money supply just the same way that your deposits do). Had the Reserve Bank bought all those tens of billions of dollars of bonds from local banks, the transaction would have boosted only settlement cash and not the money supply measures. But it didn’t. There were plenty of sellers – the Reserve Bank was eagerly buying at the top of the market – and some were local banks, and others were not. And so when the Governor suggested to Parliament that the Bank’s bond-buying did not increase the money supply, he wasn’t really being strictly accurate.

If you are now drumming your fingers are thinking this is all very technical and not really to the point, then in some respects you are correct. We’ve heard a lot about “the money supply” in the last couple of years. Most of it isn’t very accurate, but in many respects the difference doesn’t matter very much. “Money supply” measures (the formal ones referred to above) have not mattered very much to central bankers for decades, and that has been so whether inflation was falling sharply and undershooting inflation targets, or (as at present) proving very troublesome on the high side. The general view has been that money supply measures have not contained consistently useful information about the outlook for inflation, over and above what is in other indicators.

That does not mean – to be clear – that inflation is anything other than a monetary phenomenon for which central banks (and their masters) are responsible. It also does not mean that in extreme circumstances, in which say the government/central bank is flinging huge amounts of money at households without any intention of paying for those handouts now or later through higher taxes, that straight-out government money creation will not be a problem, paving the way for something that could end in hyperinflation. It is simply that specific official measures of the money supply have not proved very useful as inflation forecasters. Decades ago we hoped they did – and money supply growth targets were the rage for a decade or more in some central banks – but they didn’t.

And perhaps you can begin to see why if we go back a couple of paragraphs to the LSAP purchases. If the Reserve Bank purchases bonds from you and me (or our Kiwisaver fund) that will add to the money suply measures the Reserve Bank compiles and reports. If the Reserve Bank instead buy bonds from banks who bank with the Reserve Bank, it won’t add to the money supply measures. Does anyone really suppose there are materially different macroeconomic implications from those two different scenarios? The Reserve Bank doesn’t (from all they have said and written about how they think the LSAP works) and – for what it may be worth – I agree with them. You could add a third scenario, in which the Bank buys a bond from a non-bank entity that itself had bought the bond on credit. In that case, even RB purchasing from a non-bank won’t add to the money supply measures, but will (presumably) reduce any credit aggregates that captured the initial loan.

It might all have been different decades ago when, for example, central banks paid no interest on settlement cash balances, sometimes (as in New Zealand) banks were forbidden from paying interest on short-term or transactions deposits, and where banks were subject to variable reserve asset ratios. That was the world I started work in, but none of that is true today. Money supply measures usually aren’t very enlightening about inflation prospects, and these days neither even is the level of settlement cash balances (since the Reserve Bank pays the full OCR on whatever balances have accumulated). Thus, the LSAP may have been a dumb idea (and a very expensive one so it proved), but not because it may or may not have boosted official measures of the money supply to some extent. The pension fund that sold a government bond and now has bank CD in its books instead is no better or worse off because one asset wasn’t in the money supply official measures and the other one is. Neither are its members.

What matters is (mostly) two things: first, level and structure of interest rates, and second whether or not more purchasing power is put in the hands of public. The LSAP purports to change the former – which it seems was probably what the Governor was trying to claim at FEC the other day – but does not, and does not purport to, change the latter directly.

(By contrast, when for example the government sharply ran down its cash balances at the Reserve Bank and paid out at short notice a huge level of wage subsidy payments, not only did those payments boost the money supply measures (in most cases) but they put more purchasing power in the hands of the private sector (households supported by those payments). That isn’t a comment about the merits or otherwise of the wage subsidy scheme – I thought it was mostly great, directly counteracting what would otherwise have been a huge loss of purchasing power – just a description of how things work technically).

What about some numbers and charts?

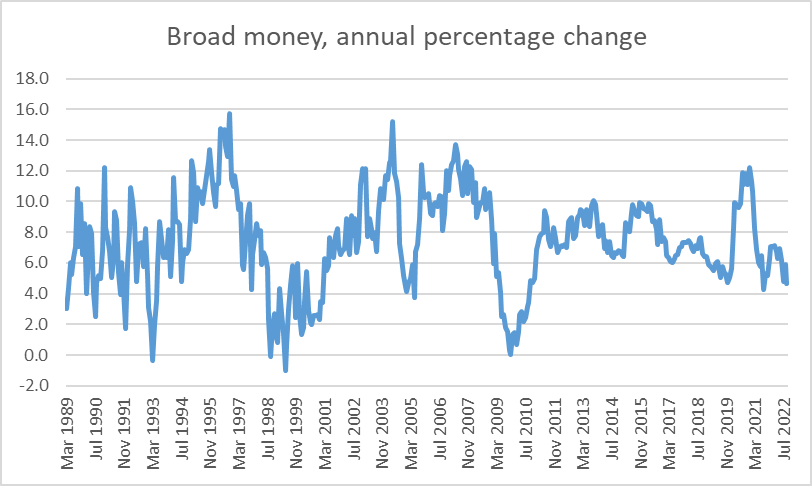

This is a chart of annual growth in the Reserve Bank broad money measure

Annual growth rates have fluctuated a lot. There was a surge in the annual growth rate in 2020 (and a 3.5 per cent lift in the month of March 2020 alone, presumably largely reflecting the wage subsidy payments) but (a) it proved shortlived, (b) the peak was still materially below peaks in the 90s and 00s, and c) core inflation in the mid 90s and mid-late 00s did not get near the current core inflation rates (depending on your measure somewhere between 5 and 7 per cent).

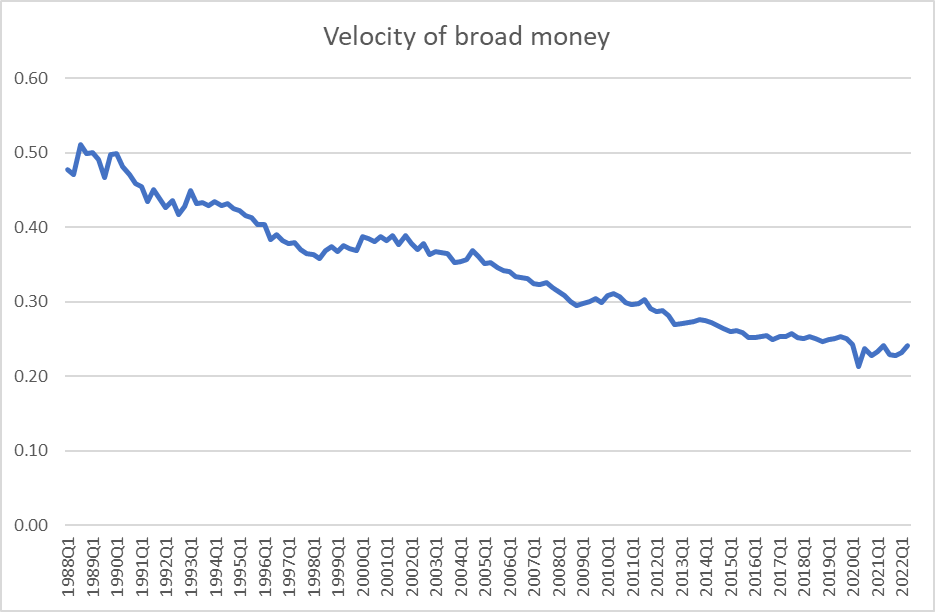

For those of you who remember studying money in your economics courses, here is a measure of the velocity of money (in this case, quarterly nominal GDP divided by the broad money stock at the end of each quarter.

This measure of the money supply has been been growing faster than nominal GDP pretty much every year since 1988 (mostly just reflecting the fact that regulatory restrictions on land use have inflated house prices to absurd levels, driving up both money and credit as shares of GDP). You can see a bit of noise in 2020 – the big initial increase in the money supply I mentioned earlier and the temporary sharp reduction in GDP – but two years on there is nothing now that looks unusual.

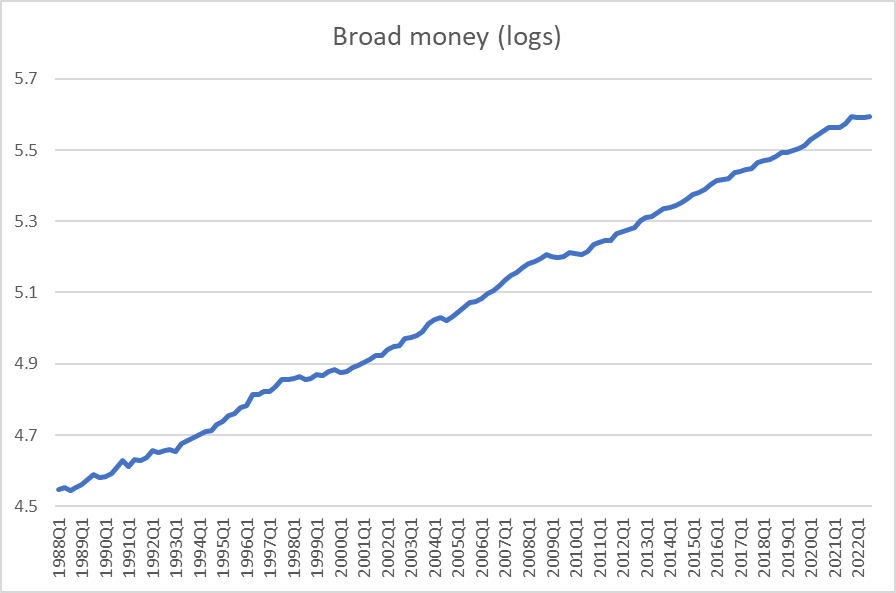

Here is a chart of the level of broad money, expressed in logs (which means that if the slope of the line is unchanged so is the percentage rate of growth in the underlying series).

Nothing particularly out of the ordinary in money supply developments (on this formal measure) over the last few years.

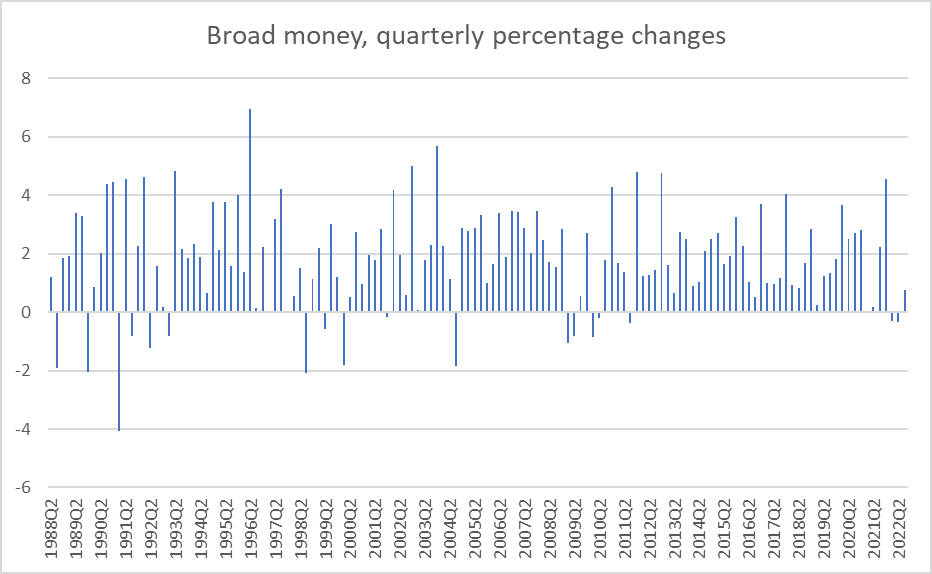

But for anyone out there who still wants to put some weight on this official measure of the broad money supply, here is the chart of quarterly percentage changes.

Eyeballing it, the most recent three quarters (to September this year) appear to have had the weakest growth since 2009. a period when nominal GDP growth and core inflation falling away sharply. Since I don’t put much weight on money supply measures, as offering anything much about the inflation outlook, I wouldn’t emphasise the comparison myself.

Inflation is primarily a monetary phenomenon, and a national phenomenon (that was why the exchange rate was floated, to make it so), and something for which central banks are responsible and should be accountable. Core inflation has been – and still is – at unacceptably high rates, as a result of choices and misunderstandings by our central bank (their misunderstandings were widely shared, among private sector economists and in other countries, but that does not change the responsibility even if it might mitigate the appropriate consequences for those central bank decision makers). Monetary policy choices matter, a lot. But official measures of the money supply don’t usually shed much additional light, and have not done so over the last couple of years.

Reblogged this on Utopia, you are standing in it!.

LikeLike

Friedman s comment that inflation is a tax probably is the reason this Government is encouraging inflation.

This seems a deliberate policy as ever increasing Government spending sustains inflation figures.The RB and Orr cannot escape responsibility ie Funding for lending programs.

Socially this Government is redistributing wealth and this is part of their program!

They will go too far in an economic sense!

LikeLike

Yup, purchasing power in the hand – the overhang from covid stimulus it would seem. Seems plenty of central bankers grappling with the stock vs flow of savings and whether the former is still ‘excessive’/a reservoir of demand. Still, higher interest rates will bite….eventually…..

LikeLike