Legislatures typically take a dim view of efforts to mislead them or their committees. This is from our own Parliament’s online “How Parliament works”

The Governor of the Reserve Bank seems just not to care, treating Parliament’s Finance and Expenditure Committee with as much contempt, and disregard for basic standards of honesty and care as some juvenile delinquent.

Yesterday the Governor and a couple of offsiders fronted up to the FEC, as they always do, following the release of the six-monthly Financial Stability Report. Were one of a particularly generous cast of mind one might almost have felt a little sorry for the Governor at times: the report was about financial stability not monetary policy, and yet most of the serious questioning was more about monetary policy, and then there was the old game of MPs attempting to get officials to say something (whether on tax, spending, immigration policy or whatever) that helps their party in its partisan jostling, even if such matters were nothing to do with the Bank’s own responsibilities. But Orr is paid a lot of money and given a lot of power, and doesn’t even make an attempt to treat elected MPs – from whose legislation flows his power and his office – with even a modicum of respect. As it was, no one forced him to answer monetary policy questions – he responded to most of them by referring MPs to their internal review of the last five years of monetary policy, to be released next week. But when he chose to answer, he had some fundamental obligation to give straight answers, not trail red herrings and other outright spin (or worse) across the path.

Orr has form. Last December, he fronted up for the Bank’s Annual Review and he and a senior offsider actively misled the committee about senior staff turnover (something that became very clear very quickly). It took a little longer, and an OIA request, to show that he had also actively misled the committee with claims that the Bank had done modelling of its own about the (supposed) climate change threat to financial stability, when in fact they’d done none.

You can watch the full hearing here, or you read an account of the relevant bits here. Orr was on the backfoot over the stewardship of monetary policy – and there is at least an arguable connection to financial stability (more so to individual financial stress) given the cycle in both interest rates and house prices, and the likely cycle in unemployment). There are some things Orr (and the MPC) can and should be held accountable for – floating exchange rates mean that what happens with inflation in New Zealand is largely a New Zealand monetary policy (passive or active) choice – and others that the central bank has never been expected to counter (the most obvious example is the price effect of GST increases, but you could think too of exogenous shocks like sudden oil price changes).

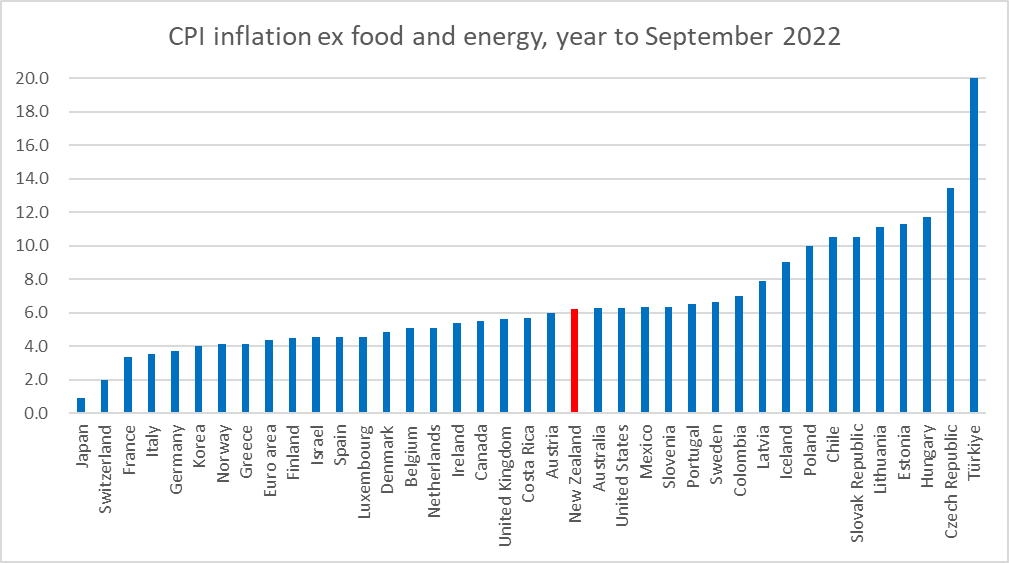

Orr’s first claim in his defence was that New Zealand has one of the “lower inflation rates in the OECD”. That is probably defensible. The ways CPIs are calculated differs across countries but on the headline numbers reported by the OECD for the year to September 2022 there were eight OECD countries with lower inflation rates than New Zealand’s 7.2 per cent (and Australia’s was almost the same at 7.3 per cent). Even if one were to treat the euro-area countries as a single unit (they all have the same monetary policy), the picture doesn’t change much. Not, of course, that we should care too much what inflation rates other countries have when we are so far from target – the exchange rate was floated 37 years ago to give us effective monetary policy independence – but when a bunch of countries have made similar mistakes (not that Orr yet concedes to regretting anything), it is better to be on the less-bad side of the pack.

But not all countries experience the same shocks the same way. Wars, rumours of war, and associated sanctions/boycotts etc have affected energy prices in particular this year. No one has ever expected inflation targeting central banks to prevent the direct price effects of immediate energy price shocks – indeed, mandates (including in NZ) have often explicitly urged central banks to “look through” such effects and focus or core measures and/or any spillover into generalised future inflation).

The CPI ex food and energy is the most commonly used measure for international comparisons of core inflation (not because it is ideal, but because it exists), and is well-suited this year when fuel and (to a lesser extent) food have been in the spotlight in the context of the Russian invasion etc. Some countries are very very heavily exposed to changes in gas prices in particular, and others (notably including New Zealand which for better or worse is not linked into a global LNG supply chain) are not. But here is how CPI ex food and energy inflation for the year to September looked (chart scale truncated – Turkey is worse than that).

New Zealand? Middle of the pack, and almost identical to the numbers for Australia and the United States (a bit higher than the UK, and a lot higher than the euro-area). This is closer to the stuff central banks individually are responsible for.

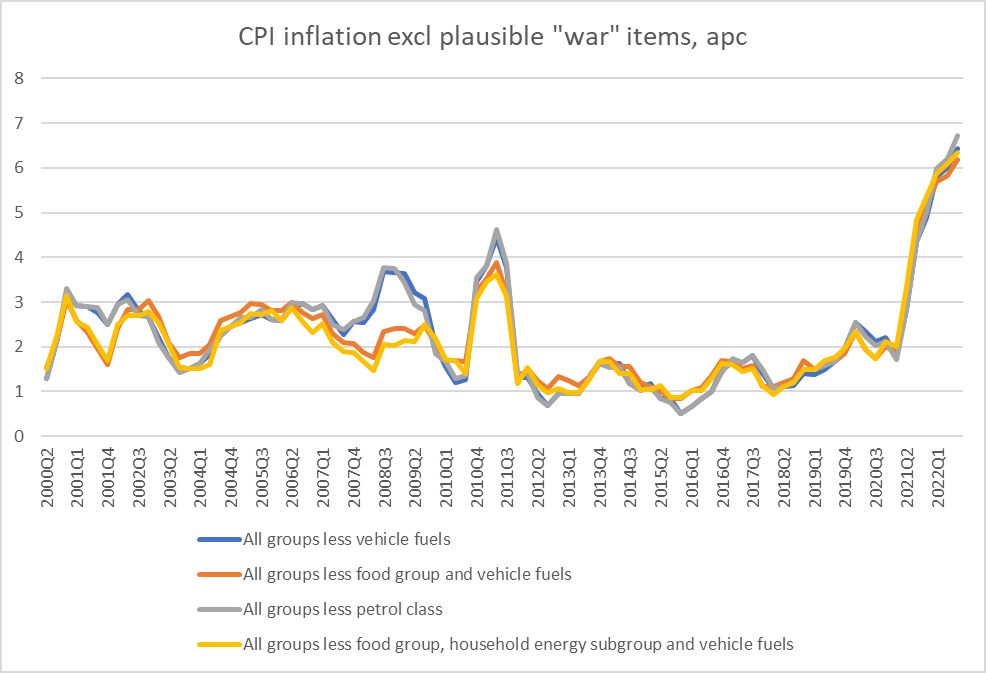

But this is really just scene-setting. Orr’s most egregious claim – and it was particularly egregious for being repeated twice perhaps 40 minutes apart – was that for New Zealand’s inflation to have been inside the target range now, the Bank would have had to have forecast the Russian invasion back in 2020.

It was just a mind-boggling claim – not that any MP on the FEC seemed to be alert enough to notice. It seemed to be implying that if we abstracted from the direct price effects of the war, inflation would otherwise be in the 1 to 3 per cent per annum target range. But here is what those data show, using the SNZ exclusions covering both fuel individually and fuel and food.

For the year to September [2021], all those exclusion measure of inflation were still in excess of 6 per cent, more than double the rate of inflation envisaged by the very top of the target range.

Oh, and when did the war start? The invasion began on 24 February. The March quarter CPI is centred on mid-February, and all those exclusion measures were already between 5.7 and 6 per cent by then. Before the war began. Now, it is certainly true that oil prices had risen in the preceding months as rumours of war mounted but (a) that wasn’t until late last year, and b) these are exclusion measures (ie excluding the direct effects of higher fuel prices). And the best indicator of domestic cyclical stress – the unemployment rate was already at 3.2 per cent in the December quarter last year (and again in March), also before the war began.

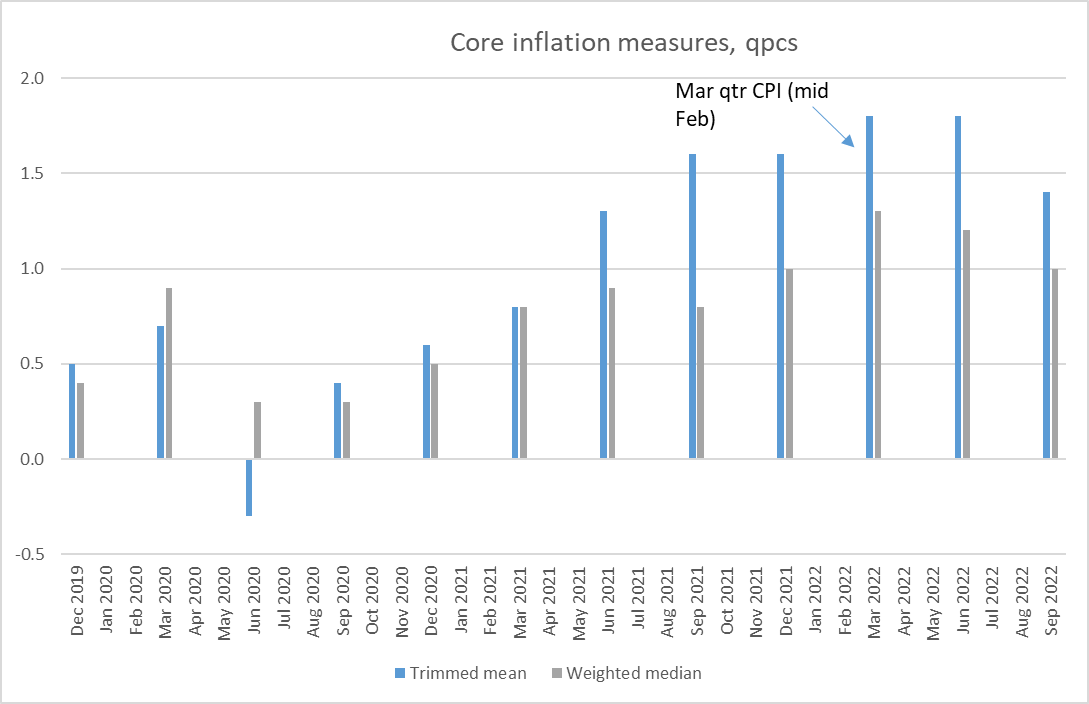

And what about more analytical measures of core inflation here in New Zealand?

For what it is worth, the highest rate of quarterly inflation on these core measures had already been recorded in the March quarter CPI, which (need I remind you) is centred on 15 February (most prices are surveyed mid-quarter), before the war began. Perhaps unsurprisingly, the worst of the (core) inflation was around the time the unemployment rate was falling to its lowest level (at a time when monetary policy was being particularly slow to act – recall that it was not until February that the OCR got back to pre-Covid levels). High core inflation – in annual terms on these measures now between 5 and 7 per cent – is a domestic phenomenon, for which monetary policy is (by default, being the last mover) responsible.

Of course, Orr knows all this (and, linking back to that parliamentary document, ought reasonably to have known it – having chosen to take the job, and accepted the $830000 salary for it). And his staff knew all this. The Governor was appearing at FEC remotely from his office, and it would have been easy for his economics staff to have slipped him a note saying “Governor, you really can’t make those claims about inflation and the war”, but (a) Orr is known to be intolerant of dissent and correction, and (b) if perhaps some brave staffer did slip him such a note, he went ahead and repeated the big and preposterous claim again later in the same appearance.

There are many many reasons why Orr should not be reappointed but simply making out stuff, that he knows – and certainly should know if he holds that job – to be simply false is not one of the least of his offences. Misleading Parliament really should matter, if we care at all about good governance any longer. On the further evidence of yesterday’s performance Orr seems not to. Just imagine if one of the institutions he regulated tried that sort of performance on him.

It’s not just Orr blowing smoke up the Committee’s proverbial:

” Chris McDonald (Manager, Financial System Analysis Team) added that debt servicing costs

are coming from a very low level. He said those costs are not unusually high, noting that in 2008

costs were significantly above that level.”

Never mind that house prices (and mortgages) have doubled since then.

Never mind that in 2008 interest rates dropped off a cliff where now they’re climbing the cliff…

LikeLike

Would have to check that one. When I heard it I thought it was ok. Mortgage rates in early 2008 were still much higher than they are now, so total debt service costs may still be lower. That said, we used to worry about them in 07/08, and as you say actual debt service costs certainly still seem set to rise from here.

LikeLike

[…] Governor who has repeatedly lied to or actively misled Parliament (eg here, here, here, and […]

LikeLike