In my post on Thursday I commented briefly on the appearance by the Governor and his Chief Economist at Parliament’s Finance and Expenditure Committee. They tried to suggest to the Committee that to the extent there had been inflation forecast errors over the last year – responding to a question from Nicola Willis – that much of it was down the summer storms including Cyclone Gabrielle. But then a helpful staffer in the back row – who may not have been so popular with management after that – piped up and explained to FEC that the impact of the cyclone was perhaps 0.1 or 0.2 per cent. The forecasting error Willis had asked the Governor about was 1.9 percentage points (the Bank had last August forecast that inflation would be 4.1 per cent in the year to September 2023, but now think that inflation rate will be 6.0 per cent).

It was pleasing to see yesterday that veteran journalist Jenny Ruth has emerged from her restraint of trade purdah after leaving Business Desk to begin a new Substack newsletter (free for the first few weeks) and that one of her first columns was about the very same Reserve Bank appearance. Her piece is worth reading. She and at least one other journalist have commented on the Governor having “toned down his hostility” towards Nicola Willis in this appearance. The tone may have been less bad, but the substance was just as contemptuous as ever – and not just of Willis but of Parliament itself. That was, once upon a time, treated as a serious matter. This is from Parliament’s own website

My Thursday post was written from listening to the appearance live and scrawling a few notes as I went. Jenny Ruth’s column prompted me to go back and listen to the recording (you can find it here), being able to stop as needed and take fuller notes. I pick up that segment of the appearance with Orr closing his opening remarks declaring that he was very proud of the Monetary Policy Statement document.

Nicola Willis then asked “what is going on? Inflation has been out of the target range for 27 months. Why is it taking so long to get inflation out of our economy?

The Governor responded along the lines of “Good question. It is a global question. The drivers of inflation have been changing through time, but all biased up, There were lockdowns, supply constraints, the Ukraine war and pressure on commodity prices, and now supply shortages in New Zealand, with severe storms. The drivers have changed but we are confident, subject to the next shock, that inflation pressures are easing”.

Nicola Willis asked if the Bank had stimulated the economy too much, and the response was yes.

The Bank’s Chief Economist (and MPC member) Paul Conway added that “it had been one supply shock after another, citing Covid, the Ukraine War, the pressure moving from goods prices to services prices, and all in all a very unusual period.

He added that the Reserve Bank had however been one of the first central banks to tighten and one of the first to signal that they thought they had reached a peak.

Nicola Willis then asked about the contrast with the US, where inflation had come down faster and appeared to be doing better.

Conway responded that he had “been amazed at the performance of the US, that it was a very different economy, a very flexible one”. He noted that unemployment had rocketed upwards when Covid began and then had fallen very sharply with resources being reabsorbed. The US was “leading the globe when it comes to inflation coming down”, but that “without thinking about it too much” New Zealand had been somewhere in the middle of the pack over the last year.

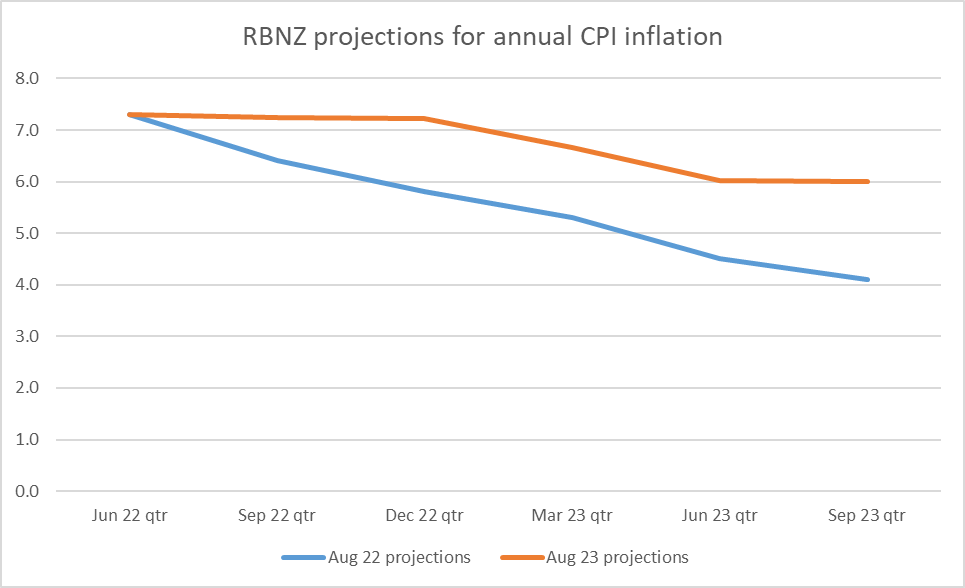

Willis observed “it strikes me how inaccurate the Reserve Bank’s forecasts have been”, citing the August 2022 forecast that CPI inflation for the year to September 2023 had been 4.1 per cent, and that the latest forecast was for 6 per cent. “Have you looked at the inaccuracies and what is going on there?”

Orr responded that “yes, we do so constantly”, stressing that the great thing about monetary policy was that it as a repeat game, reviewed afresh every six weeks, when they could reflect on surprises relative to forecasts. He indicated that the Bank was working across a whole range of different issues on how to improve. Recent forecasts erros had been “very well explained” by supply shocks, noting that a year ago they had not known about cyclone Gabrielle.

Willis then asked “how much of the difference of 1.9 percentage points is down to Gabrielle?”

The Governor responded “I don’t have that”.

Willis responded that “it seemed a stretch” that cyclone Gabrielle could account for that much of it.

Conway responded that they could back the numbers out to look at exactly that question, and then launched into a bit of a defence of the Bank’s inflation forecasting more generally, argued that they were “pretty good” relative to other forecasters but that it was challenging even in normal times, but that these had not been normal times and that the supply shocks had been “incredibly disruptive”. He said that the Bank had an active programme underway to better understand economic dynamics.

Anna Lorck (a Labour backbench MP) then asked “just for clarity, how much lower would inflation be without Gabrielle?”

At this point the Bank’s forecasting manager, who was sitting at the back of the room, piped up. She was invited to come forward and grab a chair. Her response was that the cyclone effect on inflation had been less than initially expected and was probably 0.1 to 0.2 per cent, mostly in fruit and vegetable prices. Conway noted that the cyclone had been a negative supply shock (boosting those prices) but would also be a positive demand shock (rebuild activity), and either he or the forecasting manager noted that they did not have estimates for any eventual effects on construction costs more generally.

At this point discussion moved on to other topics.

There are several things worth noting just from that record:

- not once did the Governor or the Chie Economist suggest that excess demand had had anything to do with inflation. All the talk was about the sequence of supply shocks,

- it was pretty clear from the answers that actually the Bank had done no serious analysis of the forecast errors over the last year or so,

- it was also clear that the Bank had done no serious work on trying to understand lessons from other countries, whether those where core inflation has turned down (US, Canada, Australia) or those where it hasn’t,

- the Governor wanted MPs to believe that the storms/cyclone were a big part of the story for why inflation had been so much higher than the Bank was forecasting just a year ago,

- the Chief Economist seemed more interested in backing up the Governor rather than providing straight answers to the parliamentary committee, and

- they might have gotten away with it (well, even more than they will anyway) if it weren’t for one of their capable staff in the back row giving the answer to the question from MPs, an answer very different from what her bosses had been trying to imply just minutes earlier.

There is no way any of this was simply the result of information not previously having been passed up the line. As Orr had noted in his press conference the previous day, the OCR/MPS decision came as the culmination of “8-10 days” of meetings and deliberations, and paid tribute to staff and MPC members for the work that went in. I’m sure in substance the meetings are little different than they ever were: lots of detailed papers, lots of presentations, lots of opportunity for questions, and lots of little snippets like “we think the direct effects of Gabrielle on the CPI have been about 0.1 to 0.2 per cent, a bit less than we’d initially expected. The Governor and Chief Economist knew (that it was very small, relative to the difference Willis was asking about) and chose to mislead the Committee anyway).

But having listened to the FEC appearance again, I went back to the Monetary Policy Statement itself, dozens of pages of text, charts and tables.

First I searched the document for “storms”, “cyclone” or “Gabrielle”. There were no mentions at all. “storm” did appear once, but only to note some reduction in March quarter horticulture exports (fine and good to note, but…..the Governor was talking about (and being asked about) inflation.

But surely “supply shocks” would appear in the document. After all, the Governor (and chief economist) had just told MPs that the series of supply shocks were the inflation story. Perhaps with pardonable license they only meant a big part of the story (remember that the question was about the last 12 months’ forecast error)? But anyway, “supply shock(s)” doesn’t appear in the MPS either. I did find two references to “supply constraints”, but they were both good news stories

rather than explanations for why the Bank’s forecasts had again so under-forecast inflation. A few references to “supply chains” (bottlenecks etc) were also all positive, with things having markedly improved (so all else equal lowering inflation) rather than explaining why inflation this quarter is now expected to be 6 per cent when a year ago they expected it to be 4.1 per cent.

The contrast is just staggering, and really pretty shameful when one reflects that these were senior public figures, appointed by the Minister of Finance, testifying to a parliamentary committee when inflation is far outside the target band the MPC had been given.

I’m not even sure why honesty and contrition – whatever their innate virtues – need have been so hard. Forecasting at times like these is really challenging: were it otherwise we (and a whole bunch of other countries) wouldn’t have 6% (eg) inflation in the first place. But for reasons known only to them Orr in particular, and Conway, chose just to make things up, rather than provide honest testimony to one of the bodies charged with holding them to account. (I guess they must take lessons from their Board chair, although his just-so story was “only” to The Treasury, another body charged with monitoring the Bank, not to Parliament itself.)

As I noted in the earlier post (and as Jenny Ruth reminded readers at more length) the deceptions and misrepresentations have become a disconcerting pattern under Orr’s watch. For a certain class of person, why wouldn’t one if there are no consequences to doing so. But down that path lies the further erosion of any sort of serious accountability – accountability supposedly being the quid pro quo for operational autonomy and all the power and status that goes with it,

As a reminder, from the earlier post, here were the inflation forecasts Willis had raised

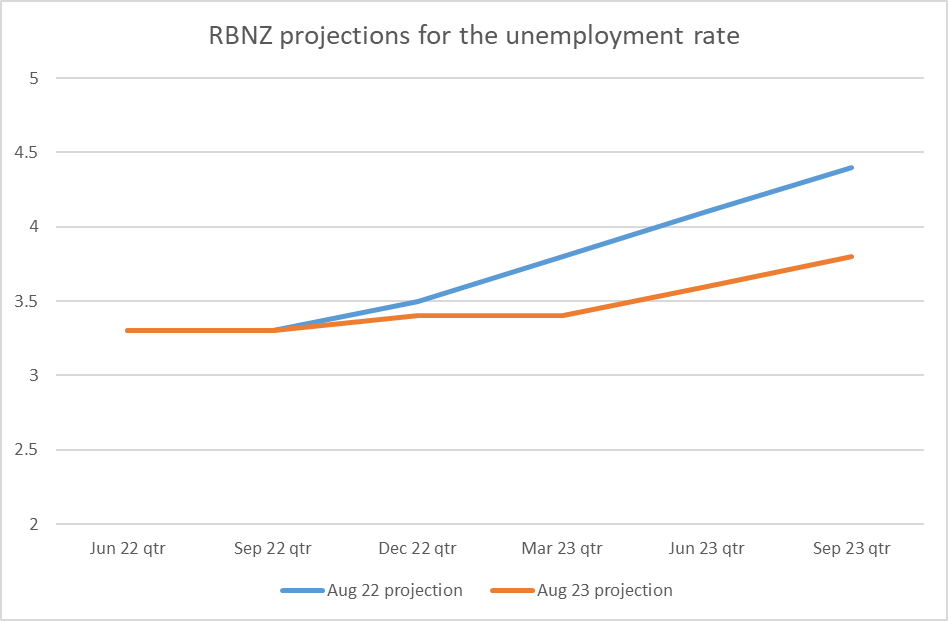

and these were the parallel unemployment projections

It wasn’t mostly about “supply shocks”, but about misjudging the extent of capacity pressures and the speed at which they would ease. But that would have been to have focused attention on the demand side, and the big misjudgements there, by the Reserve Bank, which is charged with cyclical demand management to keep core inflation in check. All these numbers are part of the MPS suite of documents on the Bank’s website.

(There was quite a bit more spin and highly questionable claims in Orr’s soft interview with a Herald journalist, but we really should be able to expect better – straightforwardness, messages actually consistent with the document he was speaking to, serious transparency, and so on; little things lilke that – when the Governor of the central bank faces a parliamentary committee.)

(Oh, and although it is an old line, it is still not true: Conway claiming to FEC that the Reserve Bank had been one of the first central banks to raise rates. There are 21 central banks making their own monetary policy (20 countries and the ECB) in the OECD. Of them, 7 started tightening earlier than our central bank, and another moved on the same day. The Reserve Bank was scarcely a stellar outlier. They did move earlier than the central banks of Australia, Canada, the US, the UK and the euro area, but then it seems now that Australia, Canada and the US have seen core inflation begin to abate earlier and further than it has here. One of the virtues of the MPS itself is that it doesn’t shy away from that fact that New Zealand core inflation is still holding up. And that, surely, is the relevant accountability test.)

This is appalling to read .

The RB is apparently insulting their own professional integrity.

On a professional level it is as bad as a doctor failing to diagnose a patients cancer and not admitting fault.

This Government should be holding them to account , as the oppositions Willis appears to be.

Thank you Mr Reddell for exposing these antics

I wonder.what will be next!?

LikeLike

That Orr and his sycophants continue to mislead and obfuscate is a direct result of the intellectual and moral weaknesses exhibited by a government intent on polishing a turd

LikeLike

Under a market economy, the attributes for getting ahead are skills such as innovation, hard work and honesty. Under the socialist system, different skills are valued, where the object is to loot, mooch and grift your way to wealth.

A role that is very lucrative in the socialist system is the enabler, although sometimes this role is fulfilled due to mental health issues. You can see on reality tv shows about the 600-pound people who are immobile due to their weight. What you invariably find is that there is a skinny enabler, lovingly spooning food into the addicted person, enabling them to continue their destructive behavior.

Alas, over the past six years, there have been a number of enablers for destructive unsustainable economic policy in Aotearoa. The reserve bank near zero interest rate policy, combined with the $11 billion LSAP policy, enabled a huge unsustainable boom, and therefore enabled insatiable government spending.

Of course, this enabling of destructive behavior inevitably leads to disaster, and this is where the skillset of looters, moochers and grifters really comes to the fore.

A successful grifter will have a number of strategies for addressing their failures. The first is bluster. Bombastic and bullying behavior is used to intimidate people from asking questions. The grifter will use straw man and appeals to authority arguments to shield themselves from criticism. This strategy can be particularly successful if you are working in a technical discipline. The grifter never shows any weakness or humility regarding their failures. Instead, they will attack the questioner, dripping with condescension. The grifter will typically answer detailed questions with short, simple answers – that are completely wrong. This gives the appearance that they are answering the issues raised, when in fact they are presenting a straw man, in patronizing fashion, that is completely false. Being “confident” that supply side issues caused our inflation could come into this category.

New Zealand’s institutions have been vandalized by looters, moochers and grifters. The Fourth Estate became the Team of $55 Million, with half a billion government “advertising” (propaganda) spending, to sweeten the socialist pot. The Courts became new age mystics. The police became government stooges. The ghastly so-called “Disinformation Project” was driven by a cabal of neo-Marxists. And the Reserve Bank became enablers of far-left economic policy, such as MMT, which contributed to the destruction of our potential economic growth rates.

The neo-Marxist road is a long one. It starts with mass censorship. Our Internal Affairs Department is trying to shut down free speech. This is the first step. It all ends in year zero, when beatific smilers like Pol Pot take over. The Khmer Rouge busied themselves hurling babies against concrete walls. This is the final neo-Marxist end point or destination.

A new government needs to find a way to purge the shadowy far-left from our institutions. Bringing back accountability and responsibility to our reserve bank would be a good place to start.

Mr. Orr needs to be removed.

LikeLiked by 1 person

[…] Governor who has repeatedly lied to or actively misled Parliament (eg here, here, here, and […]

LikeLike