Regular readers will recall that since June I’ve been on the trail of events surrounding the appointment of Rodger Finlay as, first, a “transitional board” member (attending actual Board meetings) and then a full Reserve Bank Board member, at the same time that he was chair of NZ Post, the majority owner of Kiwibank, an entity subject to Reserve Bank prudential regulation and supervision. From 1 July, the new Reserve Bank Board had legal responsibility for all the powers the Reserve Bank had on prudential policy and implementation. Finlay’s term as NZ Post chair was due to expire on 30 June, but processes were in train that saw Cabinet reappoint him on 13 June.

The most recent post was here. The story gets a little complicated, and there have been various documents (from the Minister of Finance and from The Treasury), and comments from the Minister or his office reported by the Herald. From that 31 August post

In the earlier documents, it was noted that the Secretary to the Treasury had asked for a report from her staff as to what had happened, how, and what if any process changes needed to be made. That report was released to me this afternoon and is here.

Treasury incident report on Rodger Finlay conflicts and appointments

This was the first stage

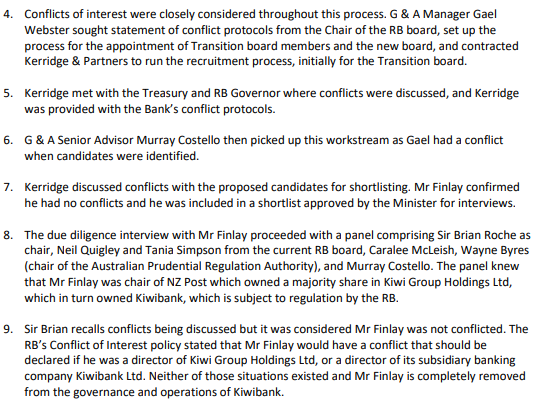

It reflects very poorly on The Treasury staff concerned (Treasury is after all responsible for monitoring reviewing the Bank), the Reserve Bank Governor and Board chair (who seem to have been more interested in some legalistic narrow definition than in either appearances or substance), and the interview panel, including the head of the Australian Prudential Regulatory Authority who, if the issue came up as Brian Roche says, should have been making the point that it should be unacceptable to have the chair of the majority owner of a bank sitting on the board of the prudential regulatory authority.

As I’ve noted before, it reflects poorly on Finlay too, who signed an application stating that he had no conflicts.

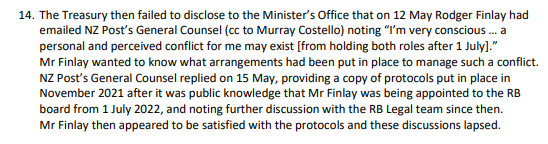

Treasury goes on to note that they did not advise the Minister of the potential conflict issue so that he could make his own informed choice, and nor were other political parties (who had to be consulted) advised.

They go on to note that in the process of planning to reappoint Finlay as NZ Post chair (a process that ran for some months) the issue of the potential conflict was also not advised to ministers.

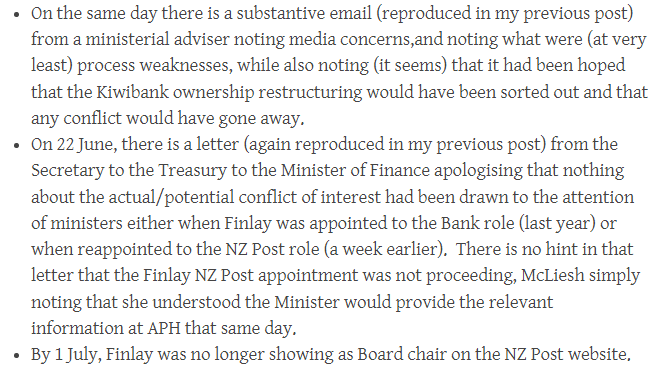

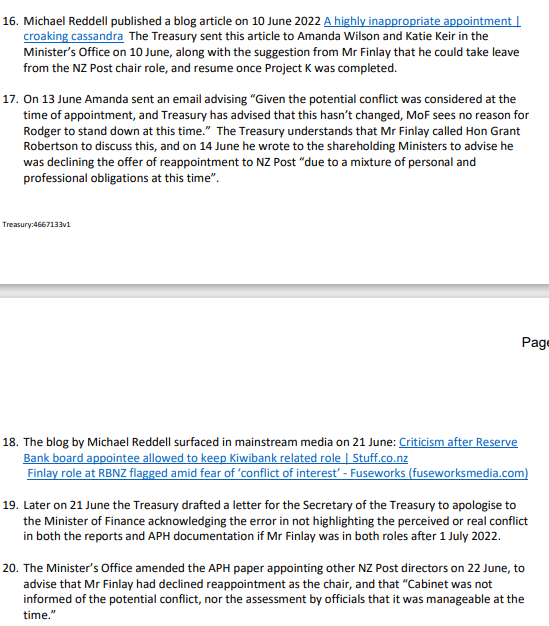

And then we get this

I guess it is encouraging that Finlay belatedly raised the issue, even if he then let the bureaucrats convince him there wasn’t an issue.

Then there was this

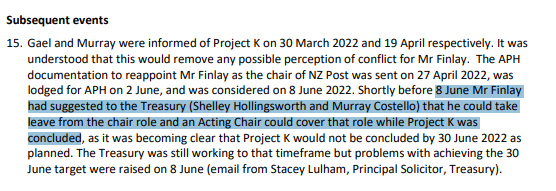

From context, Project K is clearly the scheme to have the Crown buy out the existing (Crown bodies’) shareholdings in Kiwibank. Again, it is perhaps encouraging that Mr Finlay again broached the issue of potential conflicts. It also makes sense of this from the minutes of the RB “transitional board” on 9 June (which I had been puzzling over).

and the story rounds off here (Cabinet having made the NZ Post appointment on the 13th)

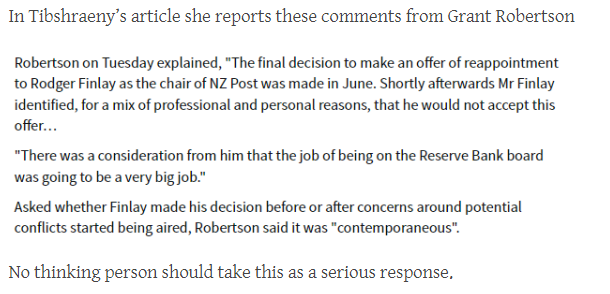

Which, as these things seem so often to do, again sheds particularly poor light on Grant Robertson as Minister of Finance, who was apparently totally unbothered by the actual or perceived conflicts even when Finlay himself had raised the issue – not even to accept the offer from Finlay to stand down from NZ Post until the Kiwibank deal was resolved (although as the RB was the regulator, if he was really serious he should have sought to take leave from that Board).

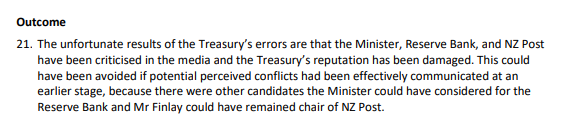

The report sums up

All of which is no doubt true, but it isn’t only (or even primarily) The Treasury’s reputation that should have been damaged by this (even if I now look on Finlay himself a little more charitably).

Anyone interested can read the rest for themselves, including the multi-page note on process improvements.

UPDATE:

It also reflects poorly on Robertson that (extract from my previous post) it is pretty clear that he actively misrepresented the situation to the Herald’s journalist.

Reblogged this on Utopia, you are standing in it!.

LikeLike

[…] Source link […]

LikeLike

Well this is some sorry reading. One feels bad for the Governance & Appointments advisor who has been thrown under the bus by the higher ups at Treasury who will have known full well that the incident report would be discoverable and have gone out of their way to name and shame him.

The truth of the matter is that the error/blame lies with many:

(1)Finlay, for not declaring the conflict as he should have done at the outset. Doing a mea culpa late in the proceedings is simply butt covering (probably he’d been warned that his appointment both on the interim Board & full Board would get some airtime) he’s an experienced director so should know better (see below).

(2)Quigley and the RBNZ, for not following their own conflict of interest guidance rules (see below), and for allowing Finlay to sit on Board meetings. Saying there was no governance or operational concerns is blatantly nonsense as NZ Post had a 53% stake and equity accounts for KiwiGroup Holdings on its balance sheet; and if in doubt this is from KiwiBank’s Annual accounts: “The ultimate holding company of Kiwibank is New Zealand Post Limited.”

(3)Senior Treasury officials, who would surely been aware (as they oversee both NZ Post & The Reserve Bank) that such an appointment would present a perception issue putting it all on a single advisor is really quite cowardly -who else signed off on the appointment?.I wonder if they are in breach of the Privacy Act by disclosing his name in such a manner?

(4) The recruitment firm who surely must have reported the conflict back to Treasury, otherwise why were they even engaged in the first place?

Here is the guidance from both the RBNZ and the IOD NZ on Conflicts:

(1) RBNZ Conflicts of interest for MPC ( assume this would apply to the Board):

“There is a conflict of interest whenever a member’s duty or responsibility to the Bank could be affected by some other duty or loyalty (i.e. the member’s “interest”) that the member may have. Perception of a potential conflict of interest is as important a consideration as an actual conflict of interest. In determining whether a conflict of interest exists, members should ask themselves: does their other interest or loyalty create an actual or perceived incentive for them to act in a way that may not be in the best interests of the Bank? Could it undermine public trust and confidence in a member or in the Bank? Would a reasonable outside observer conclude that a conflict of interest existed? ”

(2) IOD Guidance:

“Perceived conflicts: In certain circumstances, there may be a perception of a conflict

of interests where the interests come close but do not intersect. In

these situations, careful management is still required. Not taking

steps to manage these risks can undermine a company’s reputation

and hiding conflicting interests can give rise to perceptions or

allegations of misconduct.”

and…

“Generally under the Crown Entities Act, a member who is interested in a matter

relating to a statutory entity must not vote or take part in any discussion or

decision of the board or any committee relating to the matter. The interested

member must not sign any document relating to the entry into a transaction or

initiation of the matter and does not count towards a quorum for the part of the

meeting during which the matter is discussed. They must also take no part in any

activity of the entity that relates to the matter in question.”

Equity short sellers who look for malfeasance are fond of the analogy that if you find a cockroach in your fridge you can be certain to find ten thousand more in your kitchen i.e. find one untruth and you can be certain there are many many more.

This looks like that cockroach in that fridge. Definitely more to this squalid episode and probably one for the Attorney General.

LikeLike

I wouldn’t blame Kerridge (Tsy and the Bank were client, they were the ones trying the legalistic defn, and it is clear from the report that the issue was discussed at the interview panel. It isn’t up to the recruitment consultants to impose higher stds than the client).

Agree that the focus should not be on relatively junior Tsy people (altho I think Tsy has a policy of never deleting names from OIAs when it is senior analysts or above), and that is really inexcusable that more-senior Tsy people never recognised and called-out the conflict.

I still have an OIA in with the Bank on this episode (after they initially tried to fob me off claiming Tsy had all the info not them). Am not optimistic they will disclose much, but we’ll see (one day). It is a shame no journalist (or Opposition MP at a select ctte) has yet asked either Orr or Quigley how they could possibly endorse having a Board member who was, and was expected to continue as, chair of the majority owner of a Bank they regulated.

LikeLike

[…] few weeks in the past, I wrote here about (and excerpted) The Treasury’s incident report concerning the Finlay affair, and […]

LikeLiked by 1 person