Regular readers will recall that since June I’ve been on the trail of events surrounding the appointment of Rodger Finlay as, first, a “transitional board” member (attending actual Board meetings) and then a full Reserve Bank Board member, at the same time that he was chair of NZ Post, the majority owner of Kiwibank, an entity subject to Reserve Bank prudential regulation and supervision. From 1 July, the new Reserve Bank Board had legal responsibility for all the powers the Reserve Bank had on prudential policy and implementation. Finlay’s term as NZ Post chair was due to expire on 30 June, but processes were in train that saw Cabinet reappoint him on 13 June.

The most recent post was here. The story gets a little complicated, and there have been various documents (from the Minister of Finance and from The Treasury), and comments from the Minister or his office reported by the Herald. From that 31 August post

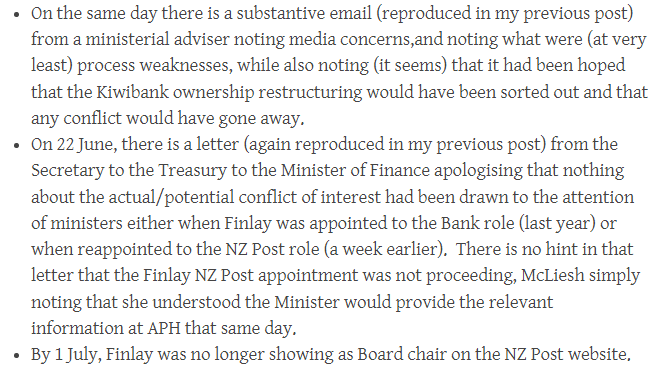

In the earlier documents, it was noted that the Secretary to the Treasury had asked for a report from her staff as to what had happened, how, and what if any process changes needed to be made. That report was released to me this afternoon and is here.

It reflects very poorly on The Treasury staff concerned (Treasury is after all responsible for monitoring reviewing the Bank), the Reserve Bank Governor and Board chair (who seem to have been more interested in some legalistic narrow definition than in either appearances or substance), and the interview panel, including the head of the Australian Prudential Regulatory Authority who, if the issue came up as Brian Roche says, should have been making the point that it should be unacceptable to have the chair of the majority owner of a bank sitting on the board of the prudential regulatory authority.

As I’ve noted before, it reflects poorly on Finlay too, who signed an application stating that he had no conflicts.

Treasury goes on to note that they did not advise the Minister of the potential conflict issue so that he could make his own informed choice, and nor were other political parties (who had to be consulted) advised.

They go on to note that in the process of planning to reappoint Finlay as NZ Post chair (a process that ran for some months) the issue of the potential conflict was also not advised to ministers.

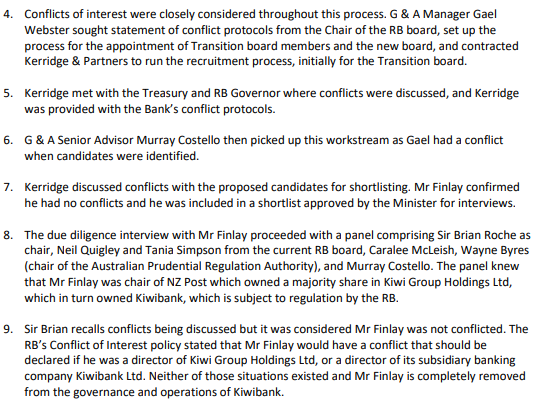

And then we get this

I guess it is encouraging that Finlay belatedly raised the issue, even if he then let the bureaucrats convince him there wasn’t an issue.

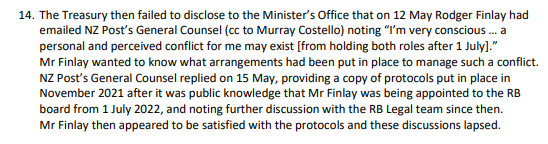

Then there was this

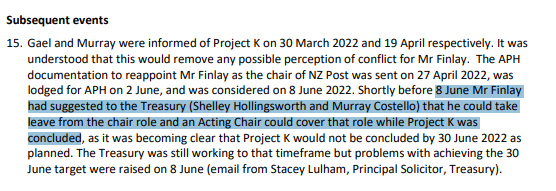

From context, Project K is clearly the scheme to have the Crown buy out the existing (Crown bodies’) shareholdings in Kiwibank. Again, it is perhaps encouraging that Mr Finlay again broached the issue of potential conflicts. It also makes sense of this from the minutes of the RB “transitional board” on 9 June (which I had been puzzling over).

and the story rounds off here (Cabinet having made the NZ Post appointment on the 13th)

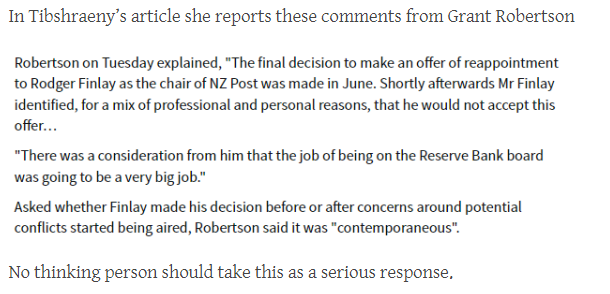

Which, as these things seem so often to do, again sheds particularly poor light on Grant Robertson as Minister of Finance, who was apparently totally unbothered by the actual or perceived conflicts even when Finlay himself had raised the issue – not even to accept the offer from Finlay to stand down from NZ Post until the Kiwibank deal was resolved (although as the RB was the regulator, if he was really serious he should have sought to take leave from that Board).

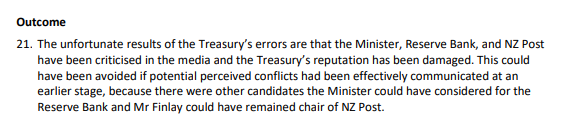

The report sums up

All of which is no doubt true, but it isn’t only (or even primarily) The Treasury’s reputation that should have been damaged by this (even if I now look on Finlay himself a little more charitably).

Anyone interested can read the rest for themselves, including the multi-page note on process improvements.

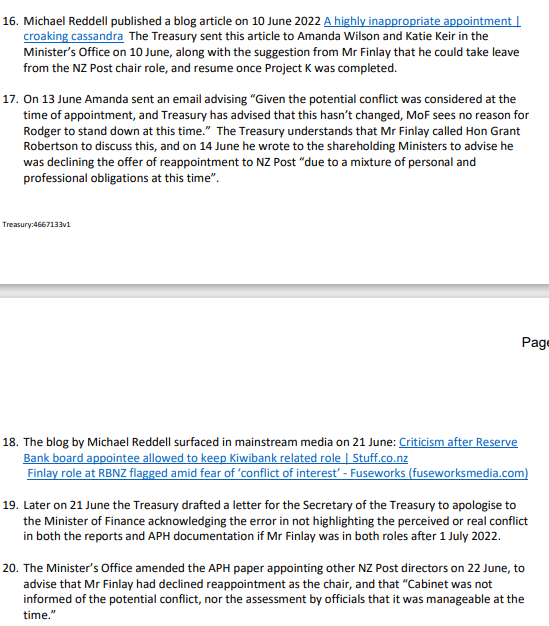

UPDATE:

It also reflects poorly on Robertson that (extract from my previous post) it is pretty clear that he actively misrepresented the situation to the Herald’s journalist.

In my post yesterday I noted in passing that the Reserve Bank Board’s Annual Report had made no mention of their decision to recommend during the year the reappointment of two external MPC members (Bob Buckle and Peter Harris), notwithstanding the huge issues there appeared to be (inflation, and large monetary losses) around the handling of monetary policy. Perhaps it made sense to reappoint them, but the Board gave the public no sense of their reasoning or of what effort they had made to understand the contributions Messrs Buckle and Harris had made. Perhaps, after all, they had fought valiantly but fruitlessly to hold back the Governor’s excesses? (ok, just kidding, but you never quite know).

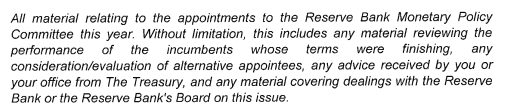

And then I remembered that months ago I had lodged an Official Information Act request with the Minister of Finance

and had not done anything with the response I had received in June.

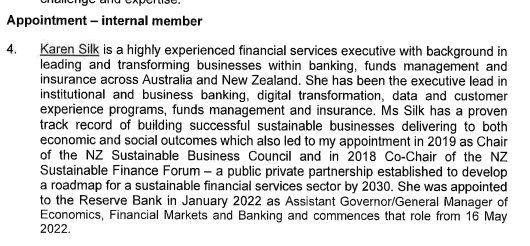

There was 44 pages of material, but not very much insight on the externals (a fair amount of material related to the appointments of internal MPC members – the egregious Karen Silk appointment (having become Orr’s deputy for macro and monetary policy with absolutely no evident subject expertise or experience), the strange six month interim appointment of Adam Richardson, and then the uncontroversial appointment of Paul Conway, the new chief economist).

The reappointments of Buckle and Harris were not announced until February, shortly before their terms expired. However, it turned out that the Minister had accepted the recommendation from the Board back in October.

We don’t have the Reserve Bank report (my request was for 2022 material) but someone else requested the Board minutes from late last year, which are on the Bank’s website. In the minutes of the October 2021 meeting we find this

There is no sign of a paper, no sign of any re-interviewing of Harris and Buckle by the Board, no nothing. What is does reveal is a point I’ve been making since the 2018 reforms were passed that in this model it is the Governor who retains the utterly dominant position, even though formally the recommendation to the Minister comes from the Board. The best way not to get any awkward members on the MPC, anyone who might from time to time challenge a Governor, is to allow the Governor himself to recommend not just which staff should be on the committee, but which externals too. You will recall that in any case, Orr, Robertson and Quigley had previously agreed to bar from consideration anyone with an active ongoing interest in monetary policy or macroeconomic analysis and research (a prohibition that Robertson restated earlier this year).

We know – he keeps telling Parliament, the Board, the public – that even now Orr has no regrets about the handling of monetary policy. I guess that was even more so this time last year, when he was clapping his colleagues on the back and arranging for them to be reappointed. This was Orr and his then chief economist at the September 2021 Board meeting.

The complacency is almost breathtaking.

But that was September/October. The Minister of Finance did not take a paper to Cabinet’s Appointment and Honours Committee, advising his intention to make these reappointments, until February, but there is no sign of any greater scrutiny or reconsideration or questioning, even as the dreadful inflation outcomes emerged and the financial losses mounted. The relevant memorandum isn’t long (just a couple of pages). It has no discussion at all of the Bank’s handling of monetary policy or the contribution these external MPC members had made to undesired outcomes, no mention of the blackball on expertise, no consideration of fresh blood, but……..priorities priorities…..

Ah, and people wonder how Karen Silk came to be appointed……(between sex and her climate change enthusiasms).

In fairness, there was a sentence each about Buckle and Harris. Of Buckle APH was told

That would be welcome if true – and to be clear, Buckle is the least unqualified external MPC member – but of course neither we nor APH have any evidence of it. Buckle is barred (by the research blackball) from any ongoing work, has no particular academic history in monetary policy – more time series macro and tax – has not made a single speech in his time on the MPC or given a substantive interview, has never dissented from an MPC decision (members are in principle free to do so), and there has been no sign in the minutes of any distinctive scholarly insights or perspectives. But Adrian told the Board he was a good bloke, and the Board told Robertson, who told his colleagues. More likely, Buckle is an establishment figure who makes the odd geeky point and, most importantly, doesn’t rock the boat. After all, it is only 7.3 per cent inflation and $9 billion of losses on his watch.

What of Peter Harris, former political adviser in Michael Cullen’s office?

That first sentence is almost demonstrably empty. Harris had had almost no professional background in monetary policy ever. He too has given no speech, has never dissented, and has given one brief and unenlightening interview.

(One of the mysteries of these reappointments is that Harris was reappointed for only 18 months. It does make sense to stagger appointments, and people can only serve two terms, but the APH paper sheds no further light on why Harris’s appointment is set to expire on 30 September next year, most likely in the middle of the election campaign. 31 March 2024 would have seemed much more sensible.)

The following month there is a further APH paper re the internal MPC appointments (although there is an e-mail exchange suggesting it may never have been lodged). I’m not going bother with the overblown spin supporting the Richardson appointment (which was just interim), but here is how The Treasury and the Minister tried to bulk up Karen Silk’s qualifications for being on the MPC, making major macroeconomic stabilisation decisions for the next five years.

In other words, no relevant background at all. And she is the most senior person in the Bank (the deputy chief executive) responsible for its monetary policy and macroeconomic functions (there is the Governor of course, but he has the whole Bank to run, financial regulation etc).

I suppose that in a way one might almost feel sorry for Robertson: he couldn’t very easily refuse to appoint to the MPC the person Orr had chosen as his macro deputy, but…….Robertson appointed the Board, including the Board chair, and appointed Orr in the first place, and has never shown the least interest in holding the Governor, the Bank, or the MPC to account.

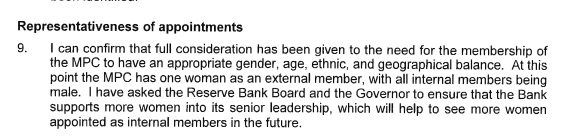

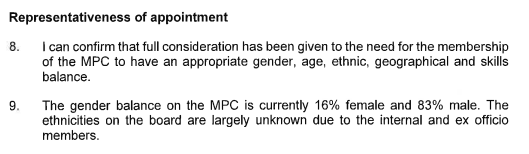

Ah, and of course that “representativeness” paragraph was there again

No mention of course that actual ongoing expertise is a disqualifying consideration, at least for the externals.

What of the future?

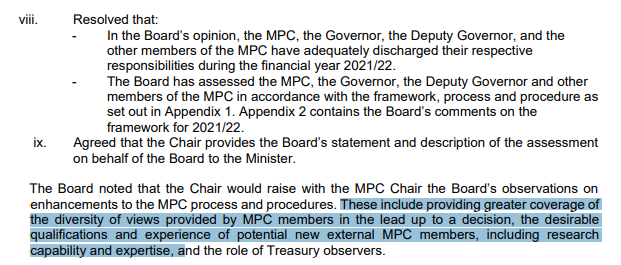

On that point, there was a mildly interesting snippet in the minutes of the very last meeting of the old Board, in June this year. They had a non-executive directors-only discussion, and for once recorded some of the material. In part that was to document their conclusion – for the Annual Report – that the MPC had done just fine, but there was also the bit I’ve highlighted.

Perhaps at the very end they were coming to regret going along with the Orr/Quigley/Robertson research blackball? By then, of course, a few days before their terms ended and their Board disbanded, their views counted for little (less than previously), but I suppose it was better than nothing.

With an even less-qualified Board, whose prime responsibilities are for other matters, we can only wait apprehensively to see what sort of names they come up with – no doubt led by the Governor, looking for tame members above all (at least if Orr is reappointed) – next year and beyond.

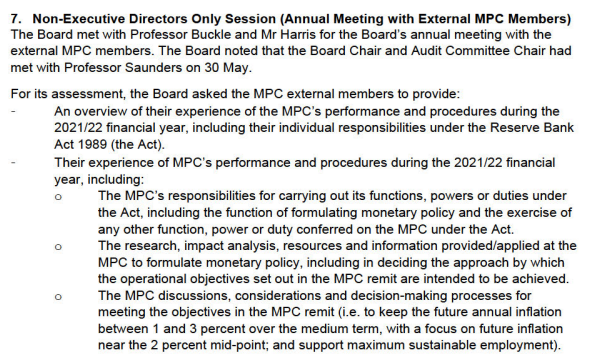

Oh, and in case you were wondering about the (previous) Board’s scrutiny of the external MPC members, there was also this in those June 2022 minutes

Not only is there no record of the substance (almost certainly a breach of the Public Records Act) but note the reference to an annual meeting. Presumably the previous one – the only one preceding the recommendation to reappoint – was around last June, when we can be almost certain no hard questions will have been asked (given the general complacency at the Bank at that stage).

It really isn’t good enough. We have a weak Board (old and new), under the thumb (at least on monetary policy) of a Governor who displays little expertise or interest in monetary policy, really dislikes alternative views or challenge, reappointing with little serious scrutiny external members who are barred from active, ongoing or future research or analysis, and who never seem to either speak or vote in ways that might establish some accountability. All involved share responsibility, but the prime responsibility rests with the Minister of Finance whose creation this system is, whose appointees these people are.

The clock is now ticking on the matter of Orr’s reappointment (or not). There are so many counts on which he should not be reappointed – not least of which is establishing some accountability, of the sort which might reasonably see few global central bankers reappointed at present (but a point warranted more for Orr than most, given his strong “I regret nothing” claims) – but it is now little more than five months until Orr’s term expires. Had he been told he would not be reappointed, or himself decided to seek greener pastures to pursue the things he seems really interested in, you’d think that would have to be announced very soon, if only to enable a proper search process for a replacement (there being no single obvious outstanding candidate to replace him).