The Herald’s Jenée Tibshraeny had a follow-up piece this morning on the Reserve Bank Board, with some interesting new information and (what appears to be) some ministerial spin and simply avoiding straight answers.

First we learn that Byron Pepper, appointed to the Board in late June, has now stepped down from his position as a director of an insurance company (Ando) that – by the vagaries of the details of the insurance legislation – is not an institution regulated by the Reserve Bank but is nonetheless substantially owned by another insurance company which is regulated, and which provides insurance on behalf of that regulated company. Again, it wasn’t illegal for Pepper to have held those two roles simultaneously, but it was quite improper, and it reflects poorly on him, on The Treasury (which made the appointment recommendations), on the Bank (Governor and key Board members), and on the Minister of Finance that it was ever allowed to happen. Reading again through the OIA papers I got back from Robertson the other day, it appears that Rodger FInlay was on the interview panel……so perhaps we should be less surprised. It is as if they have no sense of ethics, or of conflicts of interest in any sense other than the narrowly legal.

We don’t know whether Pepper jumped (volunteered himself to step down from Ando having thought again and realised it was a very bad look for an honourable person) or was belatedly pushed (by the Minister of Finance, Orr/Quigley, or The Treasury). My money would probably be on the Minister and the Beehive but if the conflict should never have been allowed to have arisen, at least it has been sorted out.

The sheer spin comes regarding Finlay.

Here is the timeline we know:

- back in May 2021, Finlay put himself forward for appointment to the Reserve Bank Board (that is when positions for the Transition Board and the real thing were advertised). He was chair of NZ Post then, it owned a majority of Kiwibank then. From the documents Robertson released, we know he then signed a conflict of interest declaration stating “I can confirm that at the time of any Reserve Bank appointment I would not have any relevant conflicts of interest”.

- In October 2021 Cabinet agreed to appoint him to the full Reserve Bank Board from 1 July 2022, and noted that the Minister had appointed him to the “Transition Board” (formally, as a consultant to the Reserve Bank during the establishment period prior to 1 July 2022).

- No political parties raised any objections when they were consulted, as the new law required for Board appointments.

- During the period of the Transition Board, Finlay was participating regularly in meetings of the then Reserve Bank Board.

- On 8 June 2022, Cabinet’s Appointments and Honours Committee considered a paper recommending Finlay’s reappointment from 1 July 2022 as chair of NZ Post

- On 10 June I wrote a post describing as “highly inappropriate” Finlay being both a board member of the prudential regulatory authority and the chair of the majority owner of Kiwibank, 5th largest bank in the country.

- On 13 June, Cabinet approved the reappointment of Finlay as chair of NZ Post from 1 July 2022.

- On 13 June, according to her piece, this morning, Tibshraeny asked Robertson’s office whether Finlay’s NZ Post terms would end on 30 June 2022 (which the existing term did). Her earlier reporting suggested she had been told – either by Robertson’s office or NZ Post – that FInlay’s term was ending on 30 June. (Those messages, highly misleading as it turns out, somewhat allayed her concerns at the time, and mine.)

- On 21 June, Tibshraeny’s first article on the issue appeared.

- On the same day there is a substantive email (reproduced in my previous post) from a ministerial adviser noting media concerns,and noting what were (at very least) process weaknesses, while also noting (it seems) that it had been hoped that the Kiwibank ownership restructuring would have been sorted out and that any conflict would have gone away.

- On 22 June, there is a letter (again reproduced in my previous post) from the Secretary to the Treasury to the Minister of Finance apologising that nothing about the actual/potential conflict of interest had been drawn to the attention of ministers either when Finlay was appointed to the Bank role (last year) or when reappointed to the NZ Post role (a week earlier). There is no hint in that letter that the Finlay NZ Post appointment was not proceeding, McLiesh simply noting that she understood the Minister would provide the relevant information at APH that same day.

- By 1 July, Finlay was no longer showing as Board chair on the NZ Post website.

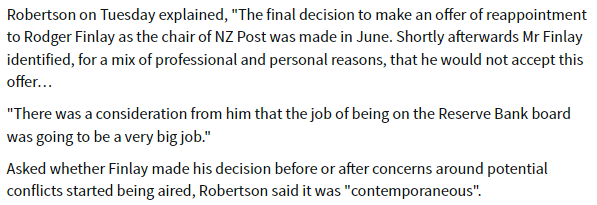

In Tibshraeny’s article she reports these comments from Grant Robertson

No thinking person should take this as a serious response.

We don’t know quite how many days RB Board members are expected to spend (my guess perhaps 25-30 a year) but it is hard to believe he had suddenly discovered it was going to be an unusually large commitment, especially as he had already spent 9 months actively engaged in the establishment phase and had served on various other public and private boards (and he was just an ordinary Board member, not holding the more time-consuming role of chair). And had he had any doubts any serious figure would have resolved them in his own mind before allowing his name to go forward for reappointment to the NZ Post chair role. As late as 22 June, he had been appointed by Cabinet (presumably his NZ Post Board and management colleagues had been told), and people from the Secretary to the Treasury down were still working on the basis the Post reappointment was going ahead. But by 1 July it wasn’t a thing.

I suppose it is always possible that (say) a serious family health emergency arose in those few days that meant he had to consider all his business and professional commitments……but (a) it appears that the NZ Post role (the one involving a serious conflict) appears to have been the only one given up, and (b) it would be quite straightforward to let something like that be known (and we’d all sympathise). But the article goes on “Finlay hasn’t responded to the Herald’s requests for comment”. That’s telling.

Most likely the Beehive jettisoned him at the last minute, realising that with media coverage and serious concerns being expressed by various senior figures, it was just a dreadful look heading into the new RB Board regime – when the new the rest of the Board they’d soon be announcing were in any case likely to be attacked as underqualified – and not worth going ahead with the Post reappointment. I’ve lodged fresh OIAs with the Ministers of Finance and State-owned Enterprises to see if we can learn more.

(One might wonder, if the Beehive story is correct, why they jettisoned him from the NZ Post role rather than the Reserve Bank one. Perhaps they reckoned it would be easier to find just another professional director for NZ Post – although none yet seems to have been appointed – plus his current term was actually expiring on 30 June. They probably hoped to get away without people realising they’d reappointed him just a few days previously. But don’t overlook also that if Finlay seems like a no-better-than-adequate appointee for the Board of the central bank and regulatory authority, the OIA papers make it clear how much difficulty Robertson and The Treasury had had in finding anyone half-qualified to serve, and Finlay is described on several occasions as the best on offer.)

A few other points caught my eye reading through again the OIA I received.

Treasury used two quite separate interview panels for appointing RB Board members. For the second wave, it was mostly Treasury and Reserve Bank people doing the interviews (including Finlay himself). But for the first round (where Finlay was chosen), they used a fairly high-powered panel, chaired by government favourite Brian Roche.

Among the interview panel was the Secretary to the Treasury. I was astonished to find that (so Treasury reported) she was on the panel because the Governor had asked for her to “reflect the seniority of the positions” (shame about that looking at what we ended up with), and “to provide gender representation”. Poor her, picked for purely tokenistic reasons.

But what really caught my eye was the presence of the head of the Australian Prudential Regulatory Authority, Wayne Byres, on the interview panel. Frankly, that seemed a little odd, for several reasons. First, one of the main relationships the Reserve Bank has to manage is that with APRA, and there will often – particularly at times of stress – be conflicting national interests. Second, APRA doesn’t operate with a part-time non-executive board (the sorts of role this interview process was selecting). But more generally, APRA is a pretty well-regarded organisation, and one might have hoped that having him on the panel would ensure at least one “adult in the room”, who really knew his stuff on the prudential side of what the Bank Board would be responsible for. And yet there is no sign that Wayne Byres, chair of a well-regarded prudential regulatory agency, had any qualms about appointing to the board of the prudential regulator, the chair of the majority owner of the 5th largest bank in the country. If he knew, did he really not care (there is no hint in any report to the Minister of any concerns being raised), and if he didn’t, how can it be that Treasury (providing the Secretariat to the process) or the Bank did not tell him? I suppose the head of APRA doesn’t need to know much about NZ-only banks, but it seems like a failure all round (including on his part, as the most prudential governance attuned person in the room) not to have found out, not to have raised concerns.

And finally, the saddest thing about reading through the OIA papers was the gradual diminution in ambition as (presumably) it became clear that (a) it was getting really hard to find any capable people even willing to put their names forward, and (b) that the government/Minister just didn’t really care about the substance at all.

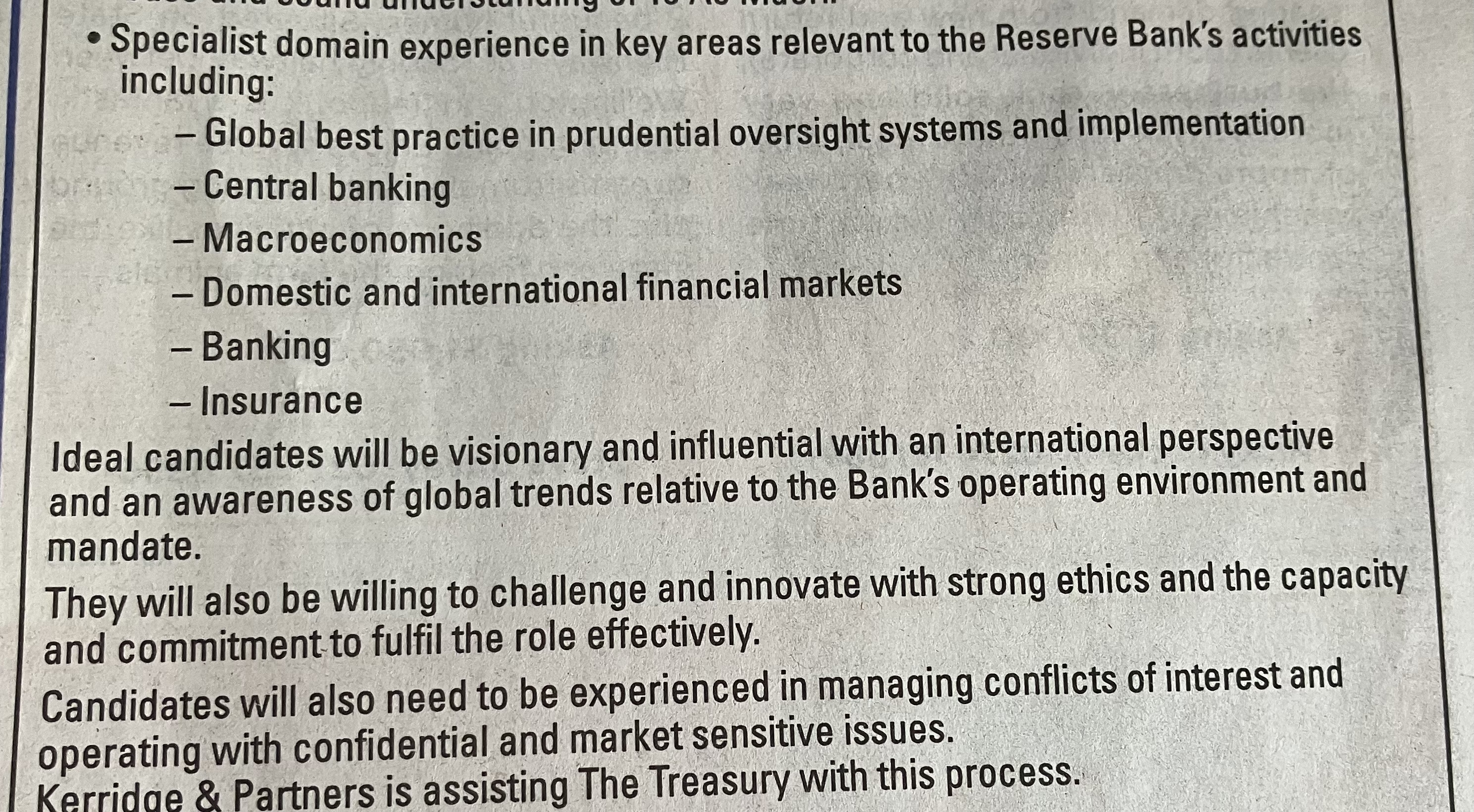

In what comes of not tidying one’s desk very often, I noticed a weathered copy of the newspaper advert from April/May 2021 for directors (transitional and permanent) sitting by my computer. Among the things they were looking for were these

Good stuff you might say.

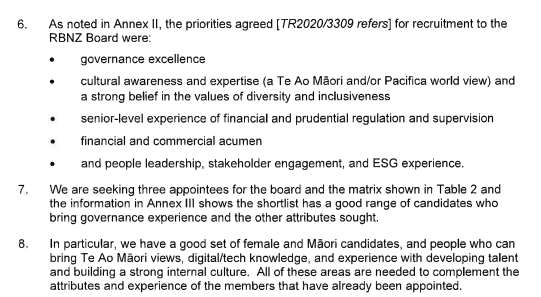

But by February, from a report to the Minister they were reduced to this

and by April, as they were closing in on the final list of those who were actually appointed, we get this summary

Perhaps a bit overqualified for a high-decile school board of trustees, and touching all sorts of political bases, but with no sign that any of them meet those ambitious “domain experience” goals once so prominent in their advertising. Oh, and no sign of any who are “visionary and influential with an international perspective and an awareness of global trends relative to the Bank’s operating environment and mandate”. The least underqualified would be the chair, but he was appointed only for a transitional two-year term. Here I might briefly disagree with Tibshraeny, who describes Finlay and Pepper as the two Board members with “the most experience when it comes to financial policy”: in fact, although both have worked in financial institutions, neither has any apparent background in prudential or related policymaking, financial stability etc, at all

As for “strong ethics” and “experienced in managing conflicts of interest” we ended up with two directors appointed who had clear and evident ongoing conflicts of interest, one of whom was involved in selecting the other. Are these really fit and proper people to be regulating and holding to account financial institutions (and those who run them), let alone the Governor? (And as a reminder, the Board is responsible for appointing and holding to account the Governor and the Monetary Policy Committee: they appear woefully underpowered when it comes to either aspect of their role.)

Then again, neither the Governor, the chair of the Board, the Minister of Finance, the Secretary to the Treasury, nor the Treasury staff charged with doing the donkey-work and actually managing these processes, seems to have seen any problem. Those asked don’t seem interested in straight answers or accountability either. And that should be even more concerning, as a reflection of what public life and governance in New Zealand seems to be becoming like.

New Zealand is seen as relatively corrupt free, and in many respects this is so. However, when it comes to conflicts of interest, we are remarkably blasé. Not recognising that it actually does matter.

LikeLike

[…] Source link […]

LikeLike

Reblogged this on Utopia, you are standing in it!.

LikeLike

The Finlay episode perfectly encapsulates the complete rot at the RBNZ: here is a regulatory institution who loudly berated NZ Banks for their ‘conduct and culture’ failings, (post the Hayne’s Royal Commission) , and criticises & punishes Westpac NZ over its Governance failures on risk management, yet seems unable to understand and display even a modicum of professional conduct, nor possess a scintilla of an idea what ‘Governance’ means.

That Finlay and Pepper both fail to recognise a basic tenent of Governance should, alone, be grounds for their disqualification, and for Quigley to have allowed Finlay to be present at Board meetings for all that time is surely more than enough reason for his removal. Then to read that a former Board member who supposedly lectures on ‘Governance’ (a term that seems to mean so little in a NZ context) sees nothing wrong ….is mindboggling, but perhaps not unexpected.

NZ Politicians shouldn’t be asking for an independent review, they should be asking, and insisting, on an independent & credible Central Bank, because the RBNZ is anything but that.

Do none of those MPs ask, as the Privacy Commission closes it’s compliance notice on the RBNZ two years down the track, why the Governor, who stood up and claimed he ‘owned it’, is still there while others who had flagged the problems are mysteriously not? What was the RBNZ’s own risk management indicator of Cyber Risk in the two years before?…hazarding a guess, given the RBNZ’s warnings to Commercial Banks on Cyber Risks, and their own Accellion data breach, the indicator wasn’t flashing ‘red’ enough…why wasn’t it?

Perhaps MPs could ask why, given the Westpac’s failings and the subsequent cleaning out of the Board & Senior Management, the RBNZ should hire someone who was in the latter group, and must have been keenly aware of those shortcomings?….curiously the mutterings out of Kent St are the RBNZ knew about the shortcommings in Westpac NZ’s risk management for years.

To hear the Governor jump on board the self-pity party train adds insult to injury: he’s paid $300k more than his predecessors, spent $250mio more than his predecessors. But has done a demonstrably worse job to the tune of $8bio plus of losses, inflation at 5% above target, and created a Central Bank with a troubling turnover of staff (usually a sign of poor corporate culture) that is a laughing stock.

New Zealanders, and those that profess to represent them, surely now realise that they have in their Central Bank not a sturdy Tree God, but a character from Shakespeare’s Midsummer Night’s dream, while Jackson Hole participants, who are the ‘Horse’s Mouth’ ( to use the RBNZ’s term) of the International Central Banking Community, will have quickly seen through the magical, fantastical bluster and humblebragging of ‘being first to raise rates’ and realised they were talking to the Donkey.

LikeLike

Thanks for this Michael,

I confess that conflict of interest is something I am really aware of, especially in my role. But at this level of governance, this is a given that transparency is essential.

Keep asking those questions my friend.

Shalom

Bruce

>

LikeLike

Thanks Bruce

(for anyone else reading, this is not the former Rber Bruce White)

LikeLike