In yesterday post, the first in this series, I tried to review and assess the Reserve Bank’s preparedness and its policy response to the Covid economic shock in the first 2-3 months (January to April 2020). They weren’t very well prepared, as it turned out, and this probably contributed to them rushing (and rushing The Treasury and the Minister) into some elements of the response that bore financial risks that were grossly proportionate to the likely economic or financial returns. But on the information they had at the time, and the way most other forecasters and commentators were thinking about the likely economic implications of Covid (and associated other policy responses), there wasn’t much doubt that a significant monetary policy response – easing monetary conditions – was well-warranted at the time. But there were mistakes – some perhaps not that consequential as it turned out (the pledge not to change the OCR, up or down, for a year come what may, but others (the LSAP, concentrated at the long end of the yield curve) much more so (in a variety of ways), and to a considerable extent foreseeably so on the information available at the time. And, as usual (but potentially mattering more in high stakes times) the Bank wasn’t very transparent.

A point I didn’t make explicitly yesterday, but should have, is that a stylised central bank (and among advanced countries there has never been one in recent decades) focused exclusively on inflation would have had no cause to have done anything different, given the data and the beliefs about (a) how the economy would behave, and (b) how the various possible monetary policy instruments would work.

Today I want to focus on the following year or so. Over that period, there weren’t a huge number of monetary policy initiatives (they really didn’t change the OCR at all, up or down, although did ensure that banks could cope with a negative OCR should the inflation outlook require such a rate in the future.

There were two significant policy announcements:

- the extension of the LSAP (and the associated Crown indemnity) to a potential $100 billion of bond purchases, and

- the establishment of the Funding for Lending scheme.

Inflation targeting has long been recognised as relying heavily on forecasts of inflation. Why? Because monetary policy actions don’t affect inflation anything like instantaneously. Prudent policy today will typically (but not always) be substantially informed by best view available on the outlook for inflation some way ahead. The lags matter.

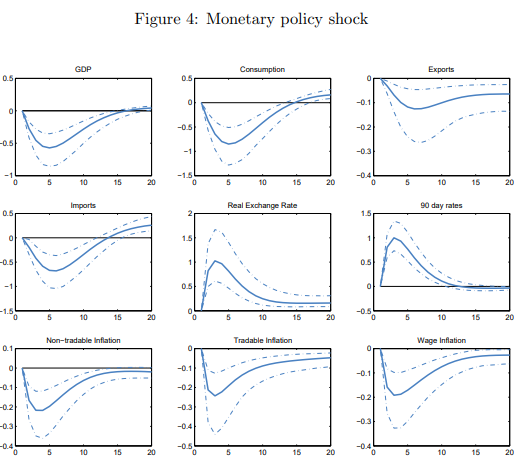

Quite how long those lags are is a matter for some debate. The old phrase was “long and variable”. I had a quick look at the Monetary Policy Handbook the Bank likes to boast of, and which is supposed to give readers a good sense of monetary policy as the Bank sees it. The word “lags” appears only once, and that referring to implementation lags in fiscal policy. I also checked the Discussion Paper in which the Bank’s calibrated economic model, NZSIM, is described, and was a bit surprised to find this chart

which seems to suggest very short lags (compare the 90 day and inflation charts), shorter than most practical discussion assumes. It is likely that the length of lags depends a bit on the shock, and a bit on the circumstances, but most pundits seem to think of the biggest impact of monetary policy on inflation as taking perhaps 12-18 months.

(Note that if the lags were as long as is sometimes rhetorically asserted – two years or more – the June quarter 2022 inflation outcomes (most recent we have) would have been substantially influenced by shocks to monetary policy in the June quarter of 2020, and since there were few/no dissenters then on the information available then, most questions of holding the RB now to account for recent inflation outcomes would be rendered largely moot. But few if any observers act, or consistently speak, as if the lags – for the largest effects – are that long.)

Implicitly or explicitly, all forecasts of inflation (and especially those that incorporate recent or prospective monetary policy changes) have a view on the length of lags, and when the Bank or officials ever discuss lags you also get the impression they have something like 12-18 months in mind.

So what did the Bank’s forecasts look like during this period? (Here, for the record, I an going to assume – I hope uncontroversially – that the published numbers were the Bank’s – or MPC’s – best view at the time.)

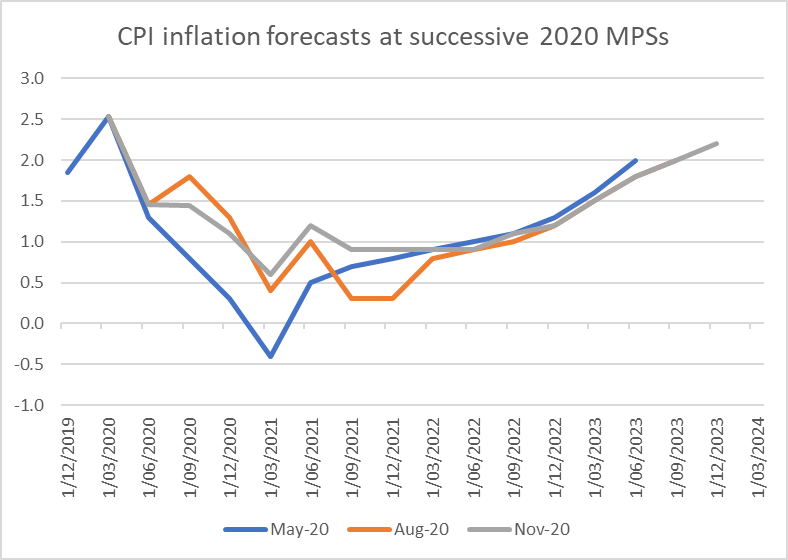

Here are the Bank’s inflation forecasts for the three successive MPSs, May, August and November 2020

Note that Reserve Bank published inflation forecasts almost always come back to 2 per cent eventually – it is the goal set for the Bank, and the default way the models are set up is for monetary policy to adjust endogenously to the extent required to get inflation back to target.

But note that these forecasts appear to have embodied views about the shocks monetary policy was leaning against that were severely disinflationary. Even with endogenous monetary policy, in all three of these sets of forecasts the inflation rates 12-18 months ahead were around 1 per cent, the very bottom of the target range and well below the 2 per cent successive governments required the Bank to focus on achieving. By the February 2021 MPS – not shown – the inflation outlook 12-18 months ahead was for outcomes around 1.4 per cent.

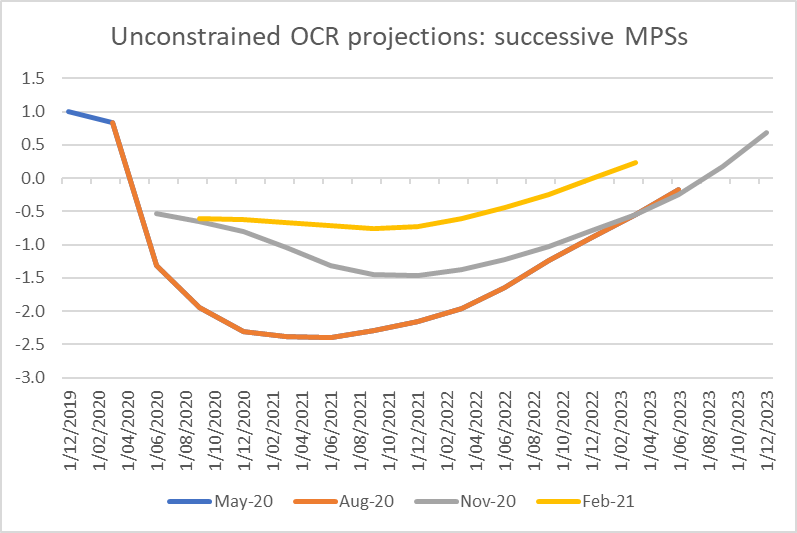

The Bank usually has OCR forecasts, but during this period (a) they had pledged not to change the OCR, (b) they believed the OCR could not yet be taken negative, and (c) they believed (or said they believed) that the LSAP was doing, and would do, a lot of the adjustment . So they published forecasts of what an “unconstrained OCR” would look like if a hypothetical OCR were to be doing its usual job.

Here were those projections (the paths in the May and August MPSs were identical)

So each of the published sets of projections through this period – but particularly those in 2020 – implied inflation well undershooting the target midpoint, even with substantial monetary stimulus (whether coming from the LSAP – which the Bank believed to be effective – or the OCR or – later – the Funding for Lending programme).

On their numbers it was pretty clear cut. The case for an aggressively stimulatory monetary policy was strong, whether considered against some pure inflation target or the Remit the MPC was charged with working towards.

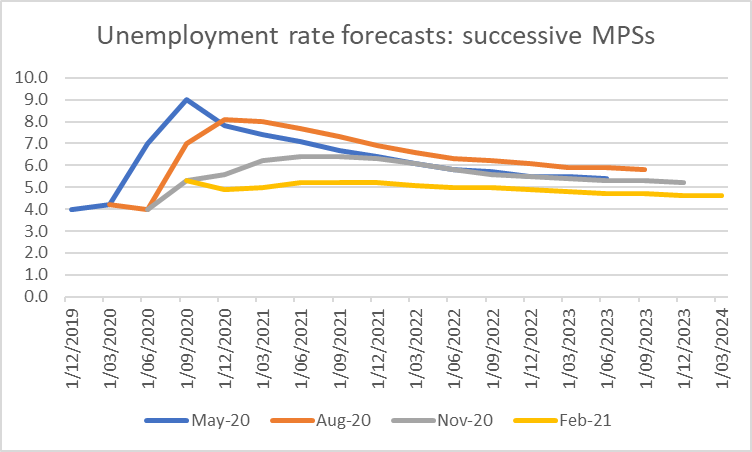

I haven’t mentioned the unemployment or output gap estimates. These were the unemployment rate forecasts, that take into account actual and endogenous future monetary policy

I don’t want to make much of them (in shocks like this most of the information is already in the inflation picture) but their best view through 2020 was the unemployment into 2022 would still be 6 per cent or thereabouts (well above any credible NAIRU estimate). By the Feb 2021 MPS there was a big revision downwards, but they reckoned then that this week’s unemployment number would be about 5 per cent (best guess a day out, something like 3 per cent).

The forecasts were, of course, wildly wrong. But (a) there is no reason to suppose they were anything other than the best view of the MPC/Governor at the time, and (b) on those forecasts, the purest of inflation targeters would have taken a similar view on how much monetary policy stimulus was required (arguably – it was an argument I made at the time – the projections argued for more).

It isn’t very satisfactory that an organisation we spend tens of millions of dollars a year on, and set up a flash new statutory committee to make the decisions, did that poorly. There is no getting away from the fact that they had the biggest team of macroeconomists in the country, and access to every bit of private or public data they would have requested.

But, they weren’t the only ones doing forecasts, putting their money and/or reputations on the line. Long-term bond yields, for example, were barely off their lows in early November 2020, when the Bank was finalising the last projections of 2020.

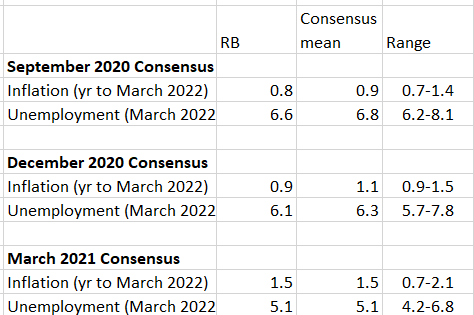

What were the published forecasts of other forecasters showing. Conveniently, NZIER each quarter publishes a collection in their Consensus Forecasts. Those numbers include projections from the five main retail banks, NZIER itself, the Reserve Bank and The Treasury. There are limitations to the comparisons – they report numbers for March years (as distinct from rolling horizons) – and each institution’s forecasts are finalised at different dates (and Treasury publishes numbers only twice a year). The data are slightly biased against the Reserve Bank, which typically finalises forecasts in the first or second week of the second month of the quarter, while the compilation is published in the middle of the final month of the quarter (so some will probably have updated their forecasts after the Reserve Bank publishes its MPSs).

But for what it is worth here are the comparisons for forecasts done in late 2020 and the first quarter of 2021.

In the September 202 comparison, the Reserve Bank’s numbers for both inflation and unemployment are very much middle of the pack (just a little less inflation and a little less unemployment than the mean response (NB: note to NZIER: medians are probably better)).

By the final quarter of 2020, the Reserve Bank had the lowest March 2022 inflation forecasts,,,,,,but not by much. 1.1 per cent – the mean response – was still a very long way below the target midpoint.

And in the March 2021 comparison – where those focusing on the Reserve Bank’s failures might have hoped to find them at odds with their peers, on the wrong side – the Bank’s inflation and unemployment forecasts sit right on the respective means (and the least-wrong forecaster – credit to them – still proved to be off on inflation by just less than 5 percentage points).

I think it is no small defence of the Reserve Bank, in making the monetary policy that was driving core inflation outcomes now, that it had very much the same sets of views as its local forecasting peers. There are other forecasters (eg Infometrics) but it isn’t obvious anyone doing and publishing forecasts was doing much better than the Bank when it mattered. If you disagree that it is “no small defence”, all I can really offer is “well, they’d be really culpable if the central tendency of private forecasters – each with fewer resources – had been materially less bad than them”.

Another comparison is with the NZIER’s Shadow Board exercise, which for each monetary policy review invites six economists (and a few others) to offer their views on what the Bank should (not “will”) be doing. Several of the bank chief economists are in the Shadow Board panel, as are Viv Hall (retired macro academic, and former longserving RB Board member), Prasanna Gai, macro professor at Auckland (and former overseas central banker/adviser), and Arthur Grimes (former chief economist of the RB and the National Bank).

Shadow Board members used to just be asked for an OCR view, with probability distribution, and given the chance to make comments (some take regularly, some occasionally, some hardly at all). So I look through each release starting with the June 2020 (non MPS) review. The question was posed about the degree to which respondents thought the RB should use (a) a negative OCR, and (b) further QE (ie an expansion of the announced QE programme) at each of (a) the upcoming meeting and (b) the coming 12 months.

In June 2020, of the six economist respondents two thought there was a strong chance that a negative OCR would eventually be required. Arthur Grimes thought there was a near-zero chance. Four of the six strongly favoured an eventual expansion of the QE programme. Prasanna Gai put that chance at 50 per cent. Arthur Grimes again assigned a near-zero probability. Sadly, neither Prasanna nor Arthur offered any comments in elaboration, so we don’t know whether they felt the LSAP would be ineffective, they had a more robust macroeconomic (inflation and/or unemployment) outlook, or what.

By the next review, enthusiasm for more stimulus had begun to fade somewhat (although Arthur – again with no comment – modestly increased his very low probability on more QE being appropriate.

By the September review the LSAP programme had been significantly expanded, but respondents views about the future hadn’t changed much. A couple thought a negative OCR quite likely to be required, but no one was keen on a further increase in the LSAP programme. Nothing much had changed in respondents’ views going into the November MPS (and none of the comments suggest a robustly different macro outlook).

By the February 2021 exercise, the question had changed. Respondents were now asked about the likely need for “tighter policy”, now and in the coming year. There was growing sense that a tighter policy stance would be required over the coming year, but only one respondent – Grimes – was confident that an immediate tightening was warranted.

Ah, you say “see, an academic who doesn’t even do monetary policy stuff these days bests the Reserve Bank”. Except for the awkward fact that this was the time Grimes chose to make comments and explain his stance. His explanation?

The RBNZ loosened monetary policy too much through 2020, causing soaring house prices (as well as other asset prices) which is very damaging for disadvantaged New Zealanders and for the next generation…..The tightening should continue until such time as house prices return to a much more affordable level provided the goods market does not enter deflation.

In other words, whatever the merits of Grimes’s stance may or may not be, he wasn’t at all focused on the outlook for the CPI. Instead he favoured using monetary policy to target house prices, with the explicit proviso that deflation might be a risk for general consumer prices. But – whatever merits or otherwise there may be to his argument – the target he was proposing was not the one the government had charged the Bank with pursuing.

(To look ahead, in the April survey Grimes again focuses on house price inflation but does talk about a need to “head off incipient goods market inflation pressures).

Again, maybe someone can point to some other commentators who did better, but from among the usual range of suspects there was little or nothing marking out the Bank’s overall view on inflation or monetary policy in the second half of 2020 or even early 2021. What there had been of course was a huge kerfuffle over house prices – where at times the Bank didn’t help itself (the chief economist once suggesting the higher prices were good and helpful), but where mostly I agree with Governor: house prices were not something the monetary policy arm of the Bank was supposed to focus on (construction costs are) and that it would be an inferior approach to monetary policy to make house prices a focus of monetary policy. It is not irrelevant that no other central bank does.

So there was massive forecasting failure, and a widely shared one. The good side of that was that the economy got back to capacity much faster than expected/feared. The (very) bad side is that the economy grossly overheated and substantial core inflation pressures compounded – in headline CPI terms – various one-off price levels shocks that orthodox monetary policy generally encourages central banks to “look through”. It wasn’t a forecasting mistake unique to New Zealand. it was, it appears, about how Covid, the resulting stimuli etc would work out – something for which neither central banks nor private forecasters had many useful precedents.

None of that means that there were not significant mistakes made by the Bank during the period in this post.

If – as the forecasts suggested – more monetary policy stimulus was warranted in August and November 2020, there was still no good reason for a massive expansion of the LSAP programme, still focused at the long end of the yield curve (where little borrowing occurred), still boosting the level of settlement cash (in a way that had next to no macroeconomic significance, given the settlement accounts paid a full OCR interest rate, but which fed a frenzy around “printing money” – from both several journalists on the left, and a few economists on the right. The Bank had the option of cutting the OCR further – 25 points isn’t nothing, even if perchance a modestly negative OCR might have created a few residual systems problems for a few banks. Sure, some weren’t keen in the abstract on negative rates, but the beauty of conventional monetary policy (the OCR) is that it comes a little or no financial risk to the taxpayer. Massively expanding the LSAP programme – when even the Bank will acknowledge uncertainty about the strength of transmissions mechanisms – opened the way to potential for further massive losses to the taxpayer, with no sign still (months on, crisis passed) of serious risk analysis or indications of the losses taxpayers might face in the worst case, if things went bad and bond yields (and then the OCR) rose sharply.

(A common excuse (I even used it once or twice myself) is “well, it doesn’t matter too much if the economy is so much stronger”, except that (a) there is little serious evidence (and the Bank has published none) that the LSAP was what produced the strength, and (b) things have so overheated, that if the LSAP did contribute much there are now two strikes against it. At worst, the Bank should have been much for focused on managing yields at the 2 and 3 year parts of the yield curve, where any potential good would have come at much less financial risk.)

And then there is the Funding for Lending programme. There have serious issues around the fact that that crisis scheme is still lending now, but that is an issue for the next post.

Again, given the macro forecasts (see above, very similar to those of private forecasters), it isn’t unreasonable for the Bank to have been seeking to ease monetary conditions a bit further. And that is what the Funding for Lending programme did – helped (mostly in the announcement effect, more than in actual lending) to lower term deposit rates relative to the OCR. It was conceived at a time when the Bank thought the OCR could not go negative, but was only finally put in place by a time when (so the Bank told us) those issues had largely been sorted out.

I wrote a post about the launch of the Funding for Lending scheme in November 2020 (“Funding for lending and other myths”). I stand today by everything in that post. The scheme wasn’t harmful, didn’t carry material financial risks, and probably helped ease conditions a bit (the Bank has claimed it is latterly equivalent to one 25 basis point OCR cut, which sounds plausible). But by the time it was deployed it simply wasn’t necessary – adjustments could have been made simply to the OCR (if the Bank had not been dogmatically wedded to the ill-advised March 2020 pledge not to change the OCR come what may). And, if you refresh your memory, the scheme fed narratives that somehow banks were settlement cash constrained (they had never been), and led to loud but futile arguments about whether access to the funds should be tied to expansions of particular favoured types of lending (when banks were more opportunity-constrained, were never cash constrained, and where if such access rules had been put in place the scheme would not have worked to the limited extent it did. The Bank itself was a significant part of the problem – it was the party that devised the misleading name, presumably in same wish by the Governor to be seen, again, “doing stuff”.

I’m going to stop this post here, and am not going to attempt a summing up except perhaps to suggest that in the broad thrust of monetary policy (stimulus provided) this period the Bank did no worse than anyone much else (and if that isn’t saying much, so many people inside and outside of government and of New Zealand misread how the economy would behave). Lags are a problem. A mechanical inflation targeter with that not uncommon view of the world might reasonably have counselled more. Where the Bank is more culpable during this period – both with hindsight and with perspectives available at the time – was in its use of unconventional instruments.