I mentioned this morning that talk of slow and controlled adjustment down in house prices reminded me of a cartoon from the 1980s, contrasting the Douglas and Anderton approaches to economic reform. Having dug around in my garage, here is the cartoon.

There are no totally easy or fail-safe ways to unwind the disaster that the New Zealand – especially Auckland – housing market has become. But this is a clear example where the sooner it happens the better. If house prices rose sharply one day and were reversed the next, almost no one suffers. If prices rise sharply for six months and then fully reverse, a few people will have difficulty – but the losses will be isolated and limited, posing no sort of systemic threat. But if real house prices stay at current levels for the next 20 years, most of the housing stock will have been purchased (and borrowed against to finance) at today’s incredibly high prices. There will have been a massive real wealth transfer to this generation of sellers (sellers, not owners). And that transfer itself simply can’t be unwound no matter what happens to house prices. If house prices were to fall now, there has still been quite a redistribution, but four years of turnover is quite different from 20 years of turnover.

In the Douglas-Anderton debates illustrated in the cartoon there were some real and legitimate choices about timing. If one is stripping away industry protection, or substantially restructuring government agencies, there are some reasonable questions about how much notice one gives people to reorient their lives, and businesses, and find new options. The protected industries were mostly pretty static, and a signal that protection would be stripped away over five years would call a halt to most new investment anyway. The house price situation is different. Even if prices go no higher from here – the sort of the thing the government and Labour Party seem to want – more and more people are getting caught in the web of paying (and borrowing) too much for houses with every passing month, just through normal housing turnover. For each new borrowing family, that choice will affect their consumption options for the rest of their lives.

But lets take a deliberately extreme contrast: on the one hand, house prices fall 50 per cent tomorrow, and in the alternative scenario they fall 50 per cent steadily over the next five years. Who would gain from the gradual adjustment? There is no obvious gains to banks – the debt is what it is, and at least conceptually they’d want to mark down the value of the collateral straightaway. There is no obvious gain to existing owner-occupiers. There is no obvious gain to the economy as a whole – indeed, arguably a climate of expected continuing falls in house prices might be worse for activity than a single sharp adjustment. Of course, there would be some winners and some losers – the losers would be the people who for some reason simply had to buy a house in the next few years (they’d pay more than in the sudden adjustment scenario) and the winners are the few smart or lucky people who manage to offload their properties before the full adjustment occurred. In fact, what we would see is turnover in the housing market dry up for several years, which would also make it more difficult for those who simply had to transact to do so. Again, not an obvious social gain.

Sadly, it isn’t going to happen, but given the mess successive governments have created a 50 per cent fall in house prices tomorrow as a result of land use liberalisation would be one of the single best things that could happen – and much better than the false promise of some sort of controlled gradual fall (such things just don’t happen). Sure, it wouldn’t be easy for some, but the number of people who will be adversely affected if the housing problems are ever really resolved grows by the day.

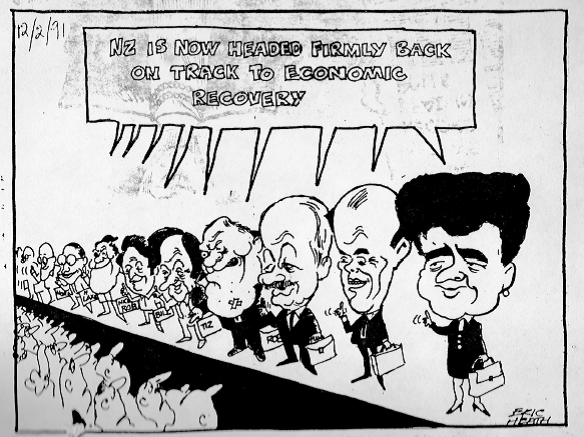

Changing tack, on the front cover of my cartoon collection I have this cartoon from early 1991.

For some years, I had it pinned to the wall in my office – the sad procession of successive Ministers of Finance who for decades (this cartoon implies back to the 1950s) had promised that New Zealand’s decline would be reversed (made worse in this case in that Ruth Richardson must have said something along these lines in February 1991, just as the severe recession of that year was taking hold). Since then, we’ve had Bill Birch, Winston Peters, Bill English, Michael Cullen, and Bill English again, and although we’ve had plenty of cyclical ups and downs, never at any time have we looked like successfully or sustainably reversing our relative economic decline. It saddens me every time I look at this cartoon – so many decades, so much failure.

The market is the market and its pretty smart.

Perhaps you could argue that the apparent overvaluation of inner city Auckland residential prices simply reflects the current and likely future unitary plans which are now being unravelled.

One good anecdotal example is that a real estate neighbour just bought the house opposite me in St Marys Bay at full whack of $5,000 per sq m, and it would seem he can now take some part of it 4 stories high, but for the pre 1944 protection afforded the 1890’s frontage.

So, maybe the market is saying that eventually all the desirable existing land stock will be intensified one way or another because there is no available or acceptable transport solution either

LikeLike

It is a plausible argument for some sections, but since the population (and the need for accommodation) will be what it will be – largely independent of planning regulatory changes – any surge in value for sites like the one you refer to should, all else equal, be offset by plummeting prices on peripheral land (whether on the fringes of the existing built area or further out). I don’t have the data, but I haven’t heard of anything like that occurring.

And I agree that the market is mostly pretty smart – it is why I argue that there is no evidence this is a “bubble”, but rather a rational outcome of a fairly crazy and costly combination of policies that seem unlikely (unfortunately) to be tossed out.

LikeLike

It has not happened because we have moved people out to the periphery through high density in periphery towns, eg Manukau, Albany, Slyvia Park, New Lynn instead of focusiing all of our high rise a a big central core. Under the current plans and also the Unitary plan, these periphery cities are now 18 level buildings which now is part of our Highrise central core spread out too far and too wide. The periphery is now cities like Huntly where you can buy property at $250k for a full section.

LikeLike

The “periphery” does not have to be Huntly, it is only deflected as far as Huntly because the land over the dozens of kms closer in than Huntly, is not allowed to be developed.

The classical land rent curve sloping gently up from true rural values to a peak at city centre, was a real-life norm for several decades. A growth boundary always violates this norm, creating discontinuities at the fringe that are increased by numerous factors, including upzoning.

Ironically, cities like Boston that have a “boundary” (even if it is a de facto one rather than a centrally planned one), but very severe density restrictions within that boundary, do not experience anything like the same inflation in land values inside that boundary. The median multiple does rise to the level of other boundaried cities – compare with UK cities, for example; but the median home is several times larger and on an exponentially larger section. The price of the land is obviously quite an exponential variable.

LikeLike

The Narrative of Everything is Awesome is failing…..

Some fantastic ideas in the below well argued observations….

http://www.salientpartners.com/epsilon-theory/when-narratives-go-bad/

To use a poker analogy, we were dealt some bad cards, the Central Banks waaay overplayed the hand, and now we’ve got to figure out how to extricate ourselves without losing our entire stake.

LikeLike

Good analogy but its way worse, the central banks have gone all in since 2008 on a GFC busted flush and are hoping the fire alarm goes off before the hand is seen

LikeLike

There is, to cop a phrase from the People’s Bank of China, a massive “one-way bet” on negative rate sovereign debt today. The momentum trade has crystallized to perfection in negative rate bonds, which has grown to become a $10+ trillion (yes, that’s trillion with a T) asset class. I think it’s the most crowded trade in the world from a behavioral or investment DNA perspective, and the moment you get even a whiff of the ECB or BOJ backing down from or reaching its limit of greater foolishness, you are going to get a rush to the exit on ALL sovereign bonds that will shake global capital markets to their core. It’ll be good times till then, as it always is, and I am seeing zero signs of Central Bankers backing down from their greater foolishness. But we have once again set up the global financial system as an inverted pyramid, with a $10 trillion asset class poised on a single, solitary piece of Common Knowledge —– what everyone knows that everyone knows. In 2008, the $10 trillion asset class of residential mortgage backed securities (RMBS) was entirely based on the Common Knowledge that it was impossible to have a nationwide decline in U.S. home prices. When that Narrative failed, the entire inverted pyramid came crashing down. In 2016, the $10 trillion asset class of negative rate sovereign bonds is entirely based on the Common Knowledge that there is no limit to the greater foolishness of Central Banks. If this Narrative fails, the entire inverted pyramid will come crashing down again. Hence my punchline: monitoring this and related status quo protecting Narratives (like the concerted effort to paint Brexit as a one-off blunder, just like Bear Stearns was painted in 2008) is the only thing that really matters for our investment reality.

LikeLike

Its common knowledge – Auckland house prices can’t fall as there is a lack of supply….

Even JK knows this he has said as much…. all the answers are … more supply

LikeLike

The house I live in, opposite the one just bought and sold, cost my partner as many 1994 NZ$ priced ounces of Gold as it is worth today

LikeLike

Great points Michael about the issue of the assets changing hands, and the people who bought high are those that get stung.

As an important aside — a similar issue applies to infrastructure projects. Take Auckland Transport’s plan for light rail fingers from the CBD out to the isthmus. There should be a discussion up front about a beneficiaries pays approach, and the fact that land values along the corridor will capture most of whatever benefits there are. (Arthur Grimes has been big on this for ages.)

The general challenge is to target those that bought low (relatively), rather than those that bought high.

If the funding discussion is the last kid off the block (like it usually is), then by the time anyone thinks about trying to capture the land value uplift, it’s too late. Much of the land would’ve changed hands, possibly even multiple times, and many land owners would’ve bought in high at top dollar, and didn’t get a windfall benefit. Many that did would then be long gone.

The funding discussion for such projects should be had before any information is signalled to the market. If the beneficiaries then argue not to have the project, then great — down-tools already.

The challenge is how to make public sector agencies and councils that provide such services to think like this, by sufficiently internalising the problem of paying for it fairly and efficiently.

LikeLike

Thanks for those comments Chris. I guess I’ve been slightly uneasy about Arthur’s approach (while recognizing the significance of the issue). of course, if all land within 100kms of downtown Akld were automatically buildable, we’d see a sharp fall in land values, and can then think about capturing subsequent uplift.

LikeLike

Thanks Michael. Yes I’m in a similar camp, both in terms of the view to open up land supply to get competitive urban land markets, and in the past not being overly proactive about value capture from land owners. But I’ve come to appreciate that Auckland’s (and progressively much of NZ’s) urban land market is quite a beast, and so much public policy just seems to unwittingly feed the beast.

LikeLike

Well, the first land mass you would have to take out would be the Waitakere Ranges where you have thousands of natives and also kauri laden forests. Then you have to remove 57 sacred mounts. Of course there is the land reserves associated with Maori Land court and not on LINZ as that is Maori Land reserves and not in private or even government ownership. Take out the 4 metres Queens chain along each and every river, stream, lake, pond, beach, swamp, any waterway etc. And you would find theres not much leftover of that 5000skm.

LikeLike

I think if that piece of infrastructure is fairly priced on a user pays basis, much of that uplift in land values goes away. If I put a lovely new freeway conveniently to your suburb which you don’t have to pay for, then the price of the house is going to internalise the net present value of future utility you get from the road – but if the road is fully tolled and you only benefit from it if you pay for it, I’m not so sure. Just like that nice school and its collection district – it’s adds value to your land only if you’re not paying full tilt school fees.

Asking for a slice of land value uplift seems like a second best solution to another problem that could have been fixed more easily.

And honestly, if the user pays revenues is inadequate to fund the project, then it probably shouldn’t go ahead anyway.

LikeLike

Straight-out land taxes presumably just capture some part of “value” regardless of where it came from, without the need for armies of bureaucrats to try and do “special assessments” of the nexus between land prices and public projects.

There is a crucial difference, though, between two types of transport infrastructure investment. One focuses value in land, the other disperses it. The system of automobility, roads and cars, is uniquely responsible for urban land rent on the whole, being maintained in a condition of “differential” rent. Without it, urban land rent is of the “monopoly” type that economists back in the time of Marx and George were so worried about. Prior to automobility, land extracted from the real incomes of participants in the urban economy, the maximum they could stand to pay. Once automobility was a mature system, land values became pretty much derived from the minimum uplift at which developers in competition with each other, could bring rural land into urban use. The urban land rent collapse from 1920 to 1950 was massive. The 1920’s was the last bubble in a series; after that, the process never resumed, urban land values were anchored at a new low. The Great Depression post-bubble “land value trough” was actually a new norm.

What we are seeing today is the reversal of this beneficial effect, by urban planners.

Fixed-route public transport investments have the opposite effect on land values, because the supply of land is not being rendered superabundant thereby like it is with expansion of the system of automobility. Pre-automobile sprawl along rail routes was over very long distances from the city, and accompanied by frenzies of speculation in the narrow ribbons of benefiting land. We see this in developments permitted along the commuter rail spines dozens of kms outside the city fringe proper – the migration of “within boundary” urban land values, into pockets of land dozens of kms out amid an abundance of $20,000 per acre rural land.

LikeLike

Phil – I’d agree with lots of your points there, I think they’re quite valid. And yes, I agree with your point on the function of land value taxes; though I consider that the real appeal of land value taxes is really just that it is a very efficient and largely equitable tax base for governments to raise revenues.

On those fixed route investments in transport infrastructure though, the point I was making was that the general approach for these in the past was to provide these for no marginal user charge, and because there is no user charge the benefit goes fully to the landowners. I’d argue that popular pressure for more free infrastructure (in combination with planning rules which outlaw increases in density around those assets). Even with wide disaggregated transport networks, distance costs money, but if those transport networks come with bigger user costs, then transport costs even more (and land at the end ought to be cheaper).

Just like if you wanted to make some houses cheaper in Auckland, you could just turn Auckland Grammar from a free school based on collection district into a full fee paying school with no district. Though obviously the political pain to do this would be … nightmarish.

LikeLike

Ryan, I appreciate that you are following my argument, very few people get it about the varying relationships between transport systems and land rent.

You are absolutely correct that charging users more correctly for the costs of a transport service, in the case of a fixed supply of land like that around a rail route, will lower the “value” captured by the owners of that land.

But in the case of automobility, in which the whole trend is the other way, I believe the real world evidence is that the cheaper it is to go further, the stronger the effect at diluting “land rent” in the whole urban economy. It is US cities with cheap petrol and underpriced highways, that have the lowest land costs of anywhere. Compare especially with Germany, where allowed speeds are substantially higher and the highway network intensity almost as great, but petrol taxes and pump prices are very much higher (and in fact more than pay for roads and externalities). It is the US cities that have the cheapest land. (Not, I hasten to add, the ones that have a regulatory growth containment distortion; I mean the ones that are still freely growing at low density at the fringes – even Philadelphia would suffice as an example, let alone Houston).

However, it would still be true in the case of the city CENTRE, that if the cost of access to it is raised, the land values there would be lowered. Cordon tolls, higher parking charges, whatever. The difference is that inbound traffic is being concentrated in the direction of the aready-most concentrated land rent, while outbound traffic is being dispersed in the direction of the already-most diluted land rent – and beyond, to where land rent in completely non-urban uses is infinitesimal.

LikeLike

Michael I am somewhat confused by your ‘communities have legitimate interests’ view alongside your ‘ two storeys within a 100km’ view. My understanding is that the old communities are the ones resisting the building up or ‘changing the character of the neighbourhood.’ so wouldn’t allowing building up run counter to their views/interests?

LikeLike

As I said to someone else, my line may partly reflect living in a street with only two storey houses – I just treated them as default/normal. I still think it might be a reasonable starting point, but would be happy enough to apply it as default in any area in that 100km radius circle that hasn’t had urban development already, and apply the current planning rules in existing urban areas (my 500 houses at a time model, whereby those rights could be traded, and sold – to developers, or if govts were determined to go the intensification route, to govts). There aren’t perfect solutions, but it seems like a starting point for discussion – and I should acknowledge drawing on (while extending) Donal Curtin’s proposal.

http://economicsnz.blogspot.co.nz/2016/07/heres-one-solution-to-aucklands-housing.html

LikeLike

I would like to get off my chest. All this talk about x number of new houses will lead to y amount of price drop is b.s.

Unless the government builds all the new houses no one knows with any degree of precision how many new houses will be built, where they will be built -infill vs. periphery, what size and at what price point.

A change in a planning map, allowing x number of new houses to be built, does not equal one for one, x number of houses actually being built. Individual choice/decisions play a part.

Ultimately unless we become a communist country the government cannot dictate house prices. Like other industries -bread for instance -governments can enforce competition, quality (fair advertising, health stds…), they can remove vested interests and cartels. These fair and publicly minded policies will influence price, the land component of house prices may fall, but at the end of the day the government is not in charge of bread supply and it is not in charge of house supply.

I think we should have a goal of giving future generations choices about competitively supplied housing. We should be ok with prices dropping if that is the market response to these reforms, but the policy is not to drop prices, the policy is to remove unnecessary restrictions -which do more harm than good. This is a subtle but important point -there is a difference between providing policies which will improve fairness and competitive.Versus a policy to target a specific house price movement. When journalists asks politicians whether they want house prices to fall -why do they not answer ‘is the next question going to be what the price of bread should be’ or ‘do you want to know who is in charge of Wellingtons bread supply’.

I am not a raving free market ideologue. I know government intervention is sometimes needed. The private sector for instance does not build infrastructure. But sometimes I think people are really naive about what markets do and what governments do.

LikeLike

Brendon

Yes, I mostly agree with you. The policy should to remove restrictions and roadblocks, but I think it is important for people to be honest about the fact that – starting from the current rigged market – that policy change should lead to a fall in prices and, indeed, that such a fall in prices is a necessary part of housing been “more affordable” (the politically salient point).

When we had milk subsidies, it was reasonably to say that subsidies should be removed and prices could be expected to rise. And when we protected domestic car assembly, reform offered cheaper cars. But starting from freer markets in milk and cars now it would be absurd for politicians to talk about desired changes in either set of prices. Same goes for houses/land if we can ever get a fairly free market established.

LikeLike

Yes you are right. Just voicing a frustration.

I kind of feel sorry for politicians because once you open the pandoras box, by saying such and such set of housing policies are likely to cause a drop in house prices, journalists and the public will be all over them with questions of how much, when, where, what houses -new/old etc.

The politician then has difficulty expressing this is the result of policies allowing more market competition and they cannot give exact details because house prices is not something they control directly.

It is a difficult message to frame Michael and I suppose the point of your two articles is none of our politicians have quite got it right. Although I would give Metiria Turei points for trying.

LikeLike

One of the biggest threats to house prices is a better economy. If we had a year or two of above-average growth, we would see a lot of migration out of Auckland to regional centres, as labour markets tightened. We would also see a rise in mortgage rates.

LikeLike

But also a rise in wage and price inflation, and a readier availability of jobs (incl second jobs and extra hours) in Akld – recall that Akld’s unemployment rate is above the still-uncomfortably-high national rate.

But assuming the “better economy” was in parallel with an improvement in Aus, we’d also see a resumption of larger outflows from NZ to Aus, which would reinforce your point. It is probably still a cyclical factor, rather than something that would lead to price to income ratios falling back to 5, let alone 3

LikeLike

Thinking of a house like a 30 year bond, an increase in mortgage rates from 5% to say 8% would decrease the value by about a third, I’m guessing. So, not a solution by itself, but helpful.

LikeLike

But only if a thirty year rate were to rise that much…..which it could, but it would take a much larger OCR increase than that to get a 30 year rate up by 300bps. And remember the numerator – presumably it will take materially higher income growth (incl expected growth in nominal rents) to support so much higher long-term interet rates

LikeLike

Both cartoons are terrific. Had to go to Wikipedia to find out about Harry Lake (the only mystery minister to me in that line-up). Brought back some fairly gruesome memories like Warren Freer’s (not a MoF) Maximum Retail Price scheme and Muldoon’s famous wage & price freeze (just a wage freeze in reality and even then not a very effective one).

LikeLike

Nice to see a change to Urban dwelling from Single dwelling by the IHP but with such a long list of overlays I dont think I am going to get any additional dwellings. The IHP speaks with forked tongues and collect a fat cheque. Nothing new here. It is total rubbish that we would get more dwellings.

Zone

Residential – Mixed Housing Urban Zone

Precinct

Overlays

Natural Resources: Quality-Sensitive Aquifer Management Areas Overlay [rp] – Auckland Isthmus Volcanic

Natural Heritage: Regionally Significant Volcanic Viewshafts And Height Sensitive Areas Overlay [rcp/dp] Height Sensitive Areas

Natural Heritage: Regionally Significant Volcanic Viewshafts And Height Sensitive Areas Overlay [rcp/dp] – R1, Viewshafts

Natural Heritage: Regionally Significant Volcanic Viewshafts And Height Sensitive Areas Overlay [rcp/dp] – R2, Viewshafts

Natural Heritage: Regionally Significant Volcanic Viewshafts Overlay Contours [i]

LikeLike

With 1600sqm I could have built a score of apartments but with the overlay conditions I would be lucky to get one more house onto the site. The IHP would have counted 20 additional properties when there is only 1 extra property.

LikeLike