Pottering around the web, and working my way through my emails, on my return from holiday, I found a couple of things from The Treasury that caught my eye.

The first was the release of new risk-free rates and CPI inflation assumptions – inputs that are required to be used in preparing the government financial statements. Treasury releases these every few months. They don’t get much attention – presumably outside government agency accounting departments – but out of curiosity I opened the latest one. And as I dug into the history of these assumptions what I found was really quite startling.

When I was at the Reserve Bank we often used to bemoan the fact that Treasury’s published inflation forecasts never seemed to settle anywhere near the midpoint of the target range. In fact, for a long time the Treasury approach seemed quite reasonable – after all, in the first 15 years or so of inflation targeting, the average annual inflation outcomes had been around 0.5 percentage points higher than the (successively revised) target midpoints. Reasonable people can debate why that happened, but it did. It was unusual – in most inflation-targeting countries, out-turns had averaged nearer the midpoint of the respective targets – but as the midpoint wasn’t mentioned in the PTA it wasn’t a major accountability issue. Don Brash took the midpoint quite seriously, while Alan Bollard wasn’t too bothered by it, but under both Governors inflation had averaged higher than the midpoint.

The Treasury’s continued assumption/forecast that inflation would settle back to around 2.5 per cent had become more frustrating, and questionable, in the years since the 2008/09 recession. Actual inflation outcomes had begun to persistently undershoot the midpoint of the target, and the midpoint of the target range had been explicitly added to the Policy Targets Agreement in 2012. The Bank, the Treasury, and the Minister of Finance all agreed that the focus of monetary policy should be the midpoint.

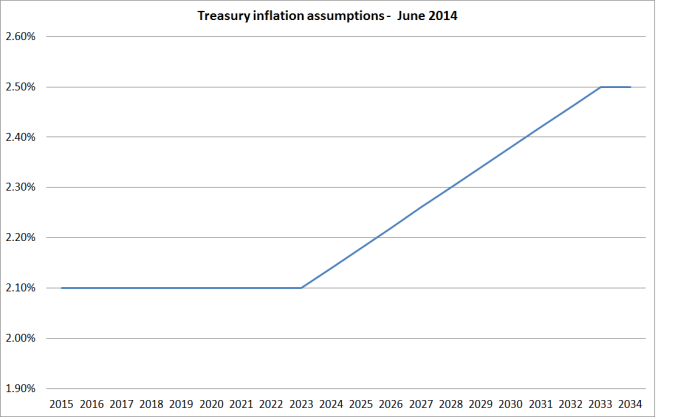

These are the assumptions Treasury published two year ago.

At the time, it seemed like the ultimate in very slowly adapting, backward-looking, expectations. By this time last year, they had markedly revised down their assumptions for the next few years (it wasn’t until 2030 that they assumed that inflation got back above even 1.75 per cent), but still assumed that in the very long-term inflation would eventually revert to 2.5 per cent. If the Reserve Bank was, as it said, concerned to see long-term expectations centre on 2 per cent, there was still some (rather limited) cover in the Treasury assumptions for a moderately “hawkish” stance. “Not even Treasury yet takes the 2 per cent midpoint that seriously” they might have argued.

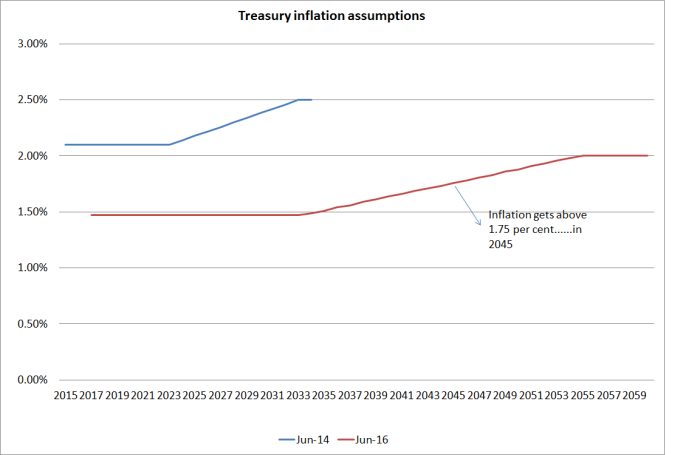

But not any more. Here are latest CPI inflation assumptions from The Treasury.

They have had to dramatically extend the horizon they provide numbers for to encompass the eventual return to their long-run assumptions. But it is 30 years from now before they assume inflation gets back even to 1.75 per cent, and almost 40 years to get back to 2 per cent.

I’m not sure quite what is going on here. On the one hand, Treasury is the chief adviser to the Minister of Finance, who has signed a Policy Targets Agreement with the Governor of the Reserve Bank requiring him to focus on a 2 per cent midpoint. And on the other hand, it is pretty much common ground that monetary policy works with a lag of perhaps a couple of years. Anything beyond, say, 2018 is definitely an outcome monetary policy can control. The PTA needs to be renegotiated next year, but not long ago the Secretary to the Treasury was quoted saying that he didn’t think Treasury would be suggesting major PTA changes. And yet Treasury thinks the best guess for inflation for the next 25 to 30 years is something well below the target they and the Minister are asking the Reserve Bank to achieve.

Of course, with yet another surprisingly weak CPI outcome just released, building on years of undershooting the target, Treasury might yet be right (between Reserve Bank policy (mis)judgements and the global deflationary environment). But whether they are or not, what should disconcert the Governor – and the Board, and those monitoring the Bank, such as Parliament’s Finance and Expenditure Committee – is that not even Treasury believes him any longer. They might say otherwise in their official advice – which we haven’t seen – but these are the numbers they consciously chose to publish.

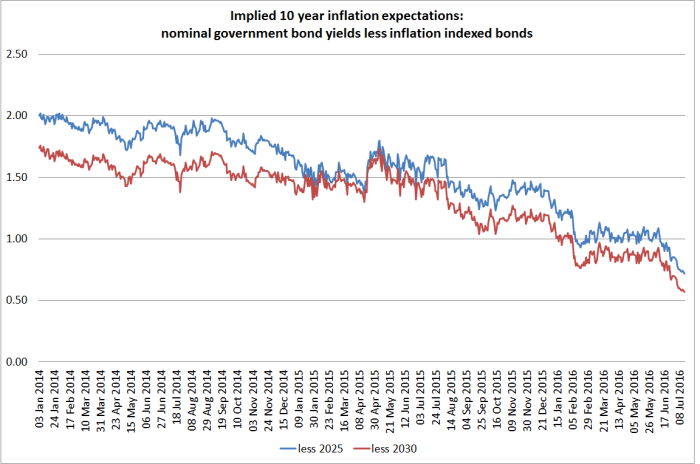

And, of course, it is not as if Treasury is alone in its doubts. For all that the Reserve Bank likes to quote surveys of a handful of local bank economists, the market has its own approximate “price” for implied future inflation. This chart takes the 10 year nominal government bond yield, and subtracts the yields on inflation-indexed bonds. It isn’t a precise measure for various reasons, including the changing maturity dates on the various bonds, but the picture is pretty clear and persistent.

As late as two years ago, the implied inflation expectations for the next 10 years were very close to 2 per cent. Now they are around 0.65 per cent.

A persistently easier stance of monetary policy is much overdue. Not even Treasury seems to take the 2 per cent midpoint very seriously now.

(UPDATE: Someone at Treasury pointed me to their relatively recent – and useful – methodology note, which explains the relatively mechanical approach they currently take to updating the CPI inflation asumptions. I don’t think it really changes my story, since the considered judgement has gone into the decision as to how best to represent a reasonable future path for inflation. The Treasury has consciously chosen to put a considerable weight on indexed bond pricing, while the Reserve Bank excludes that information completely from the inflation expectations curve it regularly cites in its updates.)

On another matter, I have lauded the Treasury’s approach to the Official Information Act issues. They seem to take seriously their obligation under the Act, and although they receive a lot of requests (about 350 in the last year) have not sought to charge anyone. They withhold material from time to time, but I’ve had enough confidence that they were playing by the rules that I have never sought to challenge those decisions, asking the Ombudsman for a review. That changed this morning.

A while ago I asked for

Copies of any material prepared by The Treasury this year on regional economic performance, particularly in New Zealand. I am particularly interested in any analysis or advice – whether supplied to the Minister or his office, or for use internally – on the economic performance of Auckland relative to the rest of the country (whether cyclically or structurally).

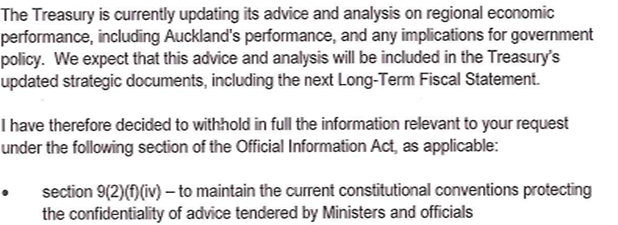

I wasn’t expecting much; perhaps some anodyne comments on some or other aspect of recent data, including perhaps the regional GDP data released in March. But while I was away, I got this reply

It is all very well and good for Treasury to be updating its analysis and advice. But I asked for what they have already provided, not what they might (or might not) include in future “strategic documents”, such as the next Long-Term Fiscal Statement, which does not have to be published until July next year.

Given that they are not even willing to publish the titles or dates of any documents (whether internal or provided to the Minister) it does raise the question as to what Treasury has to hide. Given the woeful underperformance of Auckland – considered in per capita GDP terms – perhaps Treasury is finally awakening to the fact that something is wrong with the Think Big Auckland strategy? That might be awkward for the government, but isn’t a good basis – under the OIA – for withholding material, especially in such a blanket way.

As a reminder, here is how badly Auckland has done

Over time

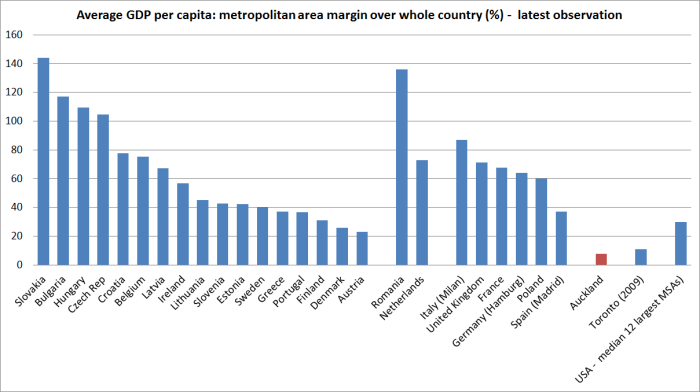

And in comparison to the largest cities in other advanced countries

I’m not sure what Treasury is hiding, or why. Perhaps the Secretary is reacting defensively to my criticisms of his recent speech? But it was that speech that prompted my original request, to see what analysis lay behind his upbeat claims about Auckland.

As an organization Treasury is better than the standard being displayed here: we see the good side of Treasury again in the recent pro-active release of Budget background papers. It is time for them to reconsider, and to release any analysis or advice they have prepared on the Auckland’s economic performance. I’ve asked the Ombudsman to review the decision.