Just before I went on holiday I wrote sceptically about the “five point economic plan” speech given by the then National leader Todd Muller.

We were promised then a series of major speeches fleshing out the framework Muller enunciated. Among the five points was this

Delivering infrastructure had this promise

Before the end of this month, I will announce the biggest infrastructure package in this country’s history. It will include roads, rail, public transport, hospitals, schools and water.

My heart sank somewhat. A new and different Think Big? But lets see the specifics.

Of the five points Muller had outlined, this seemed to be one where they were investing any hopes they might have of lifting New Zealand’s medium-term economic performance.

New leader Judith Collins started on the details with a speech given on Friday and some supporting documents. This announcement had (a) some big headline numbers for spending over the next decade, (b) the “roads, rail, public transport” components for the North Island north of Tauranga, several of which are mainly about periods well beyond the next decade, and (c) some material on how they propose to replace the RMA, and to fast-track some of these projects in the meantime. I think there had already also been a promise to build an expressway between Christchurch and Ashburton.

I don’t have any particular problem with building more and better roads where they make sense. Same goes for rail within cities, again where such proposals make robust economic sense. (I’m much more sceptical of things like cycleways, whether across the Waitemata Harbour or locally.) And clearly congestion is a major issue in Auckland and – for what is really a pretty-tiny city by international standards – to some extent in Wellington too. Congestion has real economic and welfare costs. National’s leader referred to one estimate of those costs in Auckland (presumably this one) at around $1 billion a year – and since the study was done a few years ago, perhaps it would be reasonable to use a higher estimate now.

But we have tools that can deal with congestion. Pricing. It is a tool that seem to work when tried in other countries/cities. Of course, simply pricing congestion doesn’t mean building no more roads ever, but it (among other things) helps give a better steer as to what the real price of congestion – and the value people put on avoiding it – and it deals with the congestion directly in the meantime. Even the current government’s Minister of Transport has been on record suggesting that congestion pricing is “inevitable” at some point, just not now.

And what is National’s stance, to address what Collins calls a “congestion crisis”?

Looking further ahead, if we and Auckland Council ever look at congestion charges in the future, my Government will insist they are only ever revenue neutral, with other fuel taxes reduced to compensate.

“If we ever”….Not exactly a ringing endorsement, looking to shift the ground in the debate. Perhaps congestion pricing isn’t easy electoral politics, but it is the direction we need to be heading. It might actually make a material difference within five years, unlike (as far as I can see) most other things in the National plan.

Instead the focus seems to be a flinging around some big numbers, not being too bothered about how robust any analysis supporting the mooted projects is, and all with little or no sense of decent mental model of what has gone wrong with New Zealand’s economic performance, And yet it is, supposedly, “the Plan that New Zealanders – including Aucklanders – have been waiting for, for generations”.

Pretty sure that last sentence isn’t true. Collins, for example, talks up the “if onlys”, in her case around Sir Dove-Myer Robinson’s “rapid rail” proposal, that got lots of attention in Auckland in the early 70s. We moved to Auckland about that time, but I was 10 and can’t claim to have given it huge attention. But here’s the thing: the population of the Auckland urban area then was about 650000, the birth rate had been dropping for a decade, and the new government was just about to markedly tighten up on immigration access, a policy that carried through for the following 15+ years. And even with all the New Zealand tendencies to boosterism, neither central nor local government was persuaded that Robinson’s scheme made economic sense. Nor, most likely, did it. Collins also talks up the City Rail Link project, the costs of which have escalated greatly since the government she was a part of first signed off on the project, which didn’t look very economic even then.

The promise seems to that this big infrastructure spend-up is going be pretty transformative in economic terms. There are these quotes

This city is broken by congestion. Every Aucklander and every visitor to Auckland knows it. Congestion costs Aucklanders over $1 billion per year. That’s the strict economic loss. It represents lost production, lost productivity, lost opportunity.

But congestion is far worse than that. Congestion means unreliable journey times. It means frustration at sitting idle on the motorway. It means goods being delivered late to our ports. It means Mum being late to pick up the kids from rugby practice. It means a tradie only doing two, rather than four, cross-town trips per day. That’s fewer jobs for him; less income, and less economic activity.

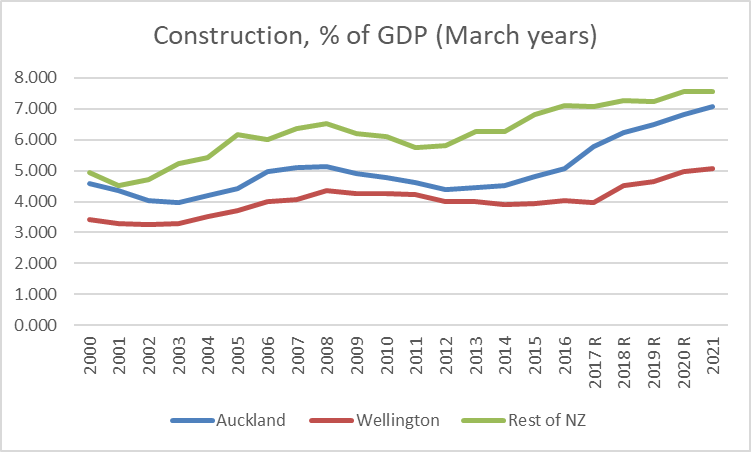

I guess $1 billion per annum is supposed to sound like a big number. In fact, it is about 1 per cent of Auckland’s GDP. Fixing the problems is probably worth doing, but 1 per cent of GDP is tiny in the context of either Auckland’s gaping economic underperformance, let alone that of New Zealand as a whole (recall that the productivity leaders are more than 60 per cent ahead of us).

And yet, according to Collins, there are really huge gains on offer.

National’s approach to infrastructure is simple: Make decisions, get projects funded and commissioned, and then get them delivered, at least a couple of years before they are expected to be needed. That is the approach that transformed the economies of Asia from the 1960s.

Quite possibly, some east Asian cities/countries did infrastructure better than New Zealand has, but I’d be surprised if National can cite any authoritative development studies suggesting that the catch-up of that handful of successful east Asian economies was primarily about moving things/people more easily around their own countries. They are typically regarded as outward-oriented, tradables-sector led, growth stories, perhaps with improving infrastructure going hand in glove with those flourishing outward-oriented opportunities.

But, as least as far as we can tell from this speech, or the framework one Muller gave, National’s policy approach is now primarily inward-looking? That has long been the practical effect of the policy approach they (and Labour) have adopted over 25+ years, but it isn’t usually so blatantly put.

Collins went on. Build these roads, rail etc and

Half of New Zealand lives in the Upper North Island region. We want a genuinely integrated region of 2.5 million New Zealanders. Our vision is to transform the four cities to be one economic powerhouse. We will unlock their potential so that the upper North Island becomes Australasia’s most dynamic region.

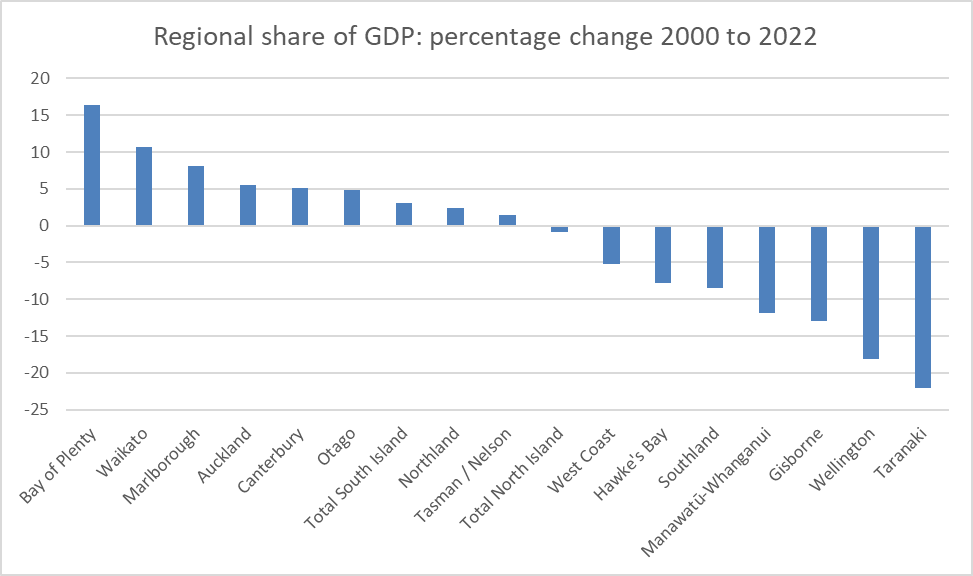

Recall that the expressway to Whangarei, complete with possible tunnel under the Brynderwyns, is – even on this plan – well over a decade away. And recall that in the regional GDP per capita data, Northland has the lowest per capita GDP in the entire country, suggesting that if Whangarei has any part in some future “Australasia’s most dynamic region” it has a very very long way to come. But even forget about the Whangarei bit of the fairytale for now, do the National caucus have any serious idea how far behind key bits of Australia productivity levels in New Zealand actually are (and Australia is no great OECD productivity success story)? As a hint, that 1 per cent of GDP Collins talked about fixing won’t even begin to make a visible dent in the productivity gap – a gap only likely to continue to widen for the next few years, even if Collins plan did eventually make some small helpful difference.

National – like Labour really – seems to have no idea at all what has gone wrong with the New Zealand economy, what has taken us from among the very richest and most productive countries on earth to be some slightly embarrassing laggard, increasingly unable to offer the best to our own people. But they’ll just fling some more cash at things – as Labour does, just a slightly different make-up – in the hope of getting elected, and the vague sense then the something must be done, and anything is something.

Here is the Collins approach to project evaluation

The economists will tell you we should build projects only when they’re needed. My sense from my time in politics is that you just want the government to get infrastructure projects built. You just want them done. And you want them done ahead of time.

My Government will be informed by processes like NZTA’s Benefit-Cost Ratio analysis, and by advice from the Infrastructure Commission. But we will not consider that analysis or that advice to be holy writ when making decisions about major transformational projects. Think about all of the Roads of National Significance the National Government built.

I don’t think Transmission Gully passed a decent cost-benefit test, even when it was going to be operational by now.

Now I’m not about to suggest that officials and appointees to government boards should be making the decisions, but any well-done cost-benefit analysis should be a key hurdle in any proposed commitment of large amounts of public money. Perhaps there are reasonable arguments about methodology or about specific assumptions used in the calculations. All that can and should be debated, but a project that cannot return a decently positive benefit-cost ratio is one the public should be very sceptical of. Simply waving your hands and talking about “major transformational projects” should be no more acceptable now than ever. And having projects in place “ahead of time” – when few projections about the future, including about population, are that robust – also has significant economic costs, even at today’s lower public sector discount rates.

One other questionable aspect of National’s plan is what they call “intergenerational funding”. This is fancy language for borrowing, in this case off the core Crown accounts and having NZTA borrow instead. As far as I can see there is almost nothing going for this particular approach – one already indulged in by Labour, with Housing New Zealand now borrowing on-market. It will be a (a bit) more costly than the central government borrowing itself, with no more likelihood the debt will be defaulted on, it is less transparent, and unless the government is proposing to delegate all final decisions on projects to officials (which they – rightly in my view – show no sign of) there is no reason to think it will either tap new sources of capital (the NZ government not being debt-constrained) or introduce new disciplines on Crown capital spending. There is, or can be, a place for government borrowing, but decisions on that are better taken, and managed, centrally.

So there were big numbers in the announcement, some big projects (which may or not be economic, may or may not ever happen even if National winds), but little or no sense of a credible economic model lying behind it, grounded in the specifics of New Zealand’s underperformance. And if there is such a model at all, it just seems to be more of the same – rapidly growing, but quite volatile, population – the strategy that has so comprehensively failed for the last few decades. More and better roads aren’t going to materially change that. Nor – although it should be done as a matter of priority – are the sorts of land use reforms that might make house prices more affordable. The new Leader of Opposition suggests a National government might do something there. But we’ve heard that story before – whether from National in Opposition in 2008 or from Phil Twyford in Opposition in 2017. Perhaps this time really would be different, but I’m certainly not counting on it.

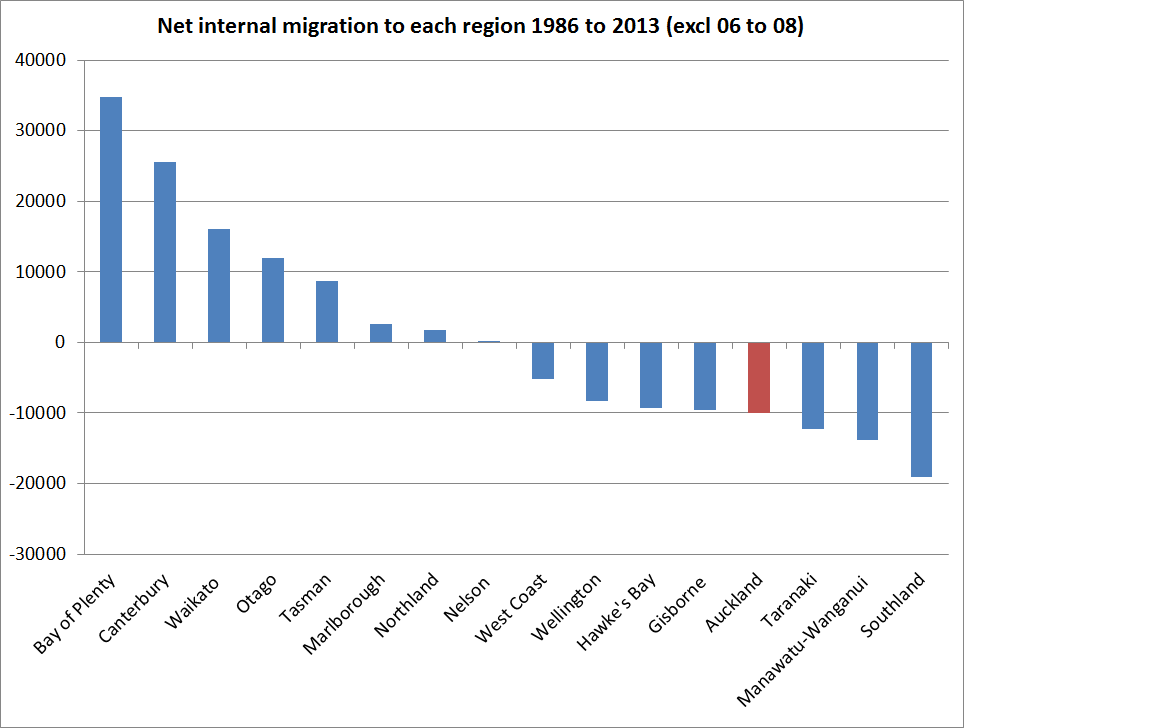

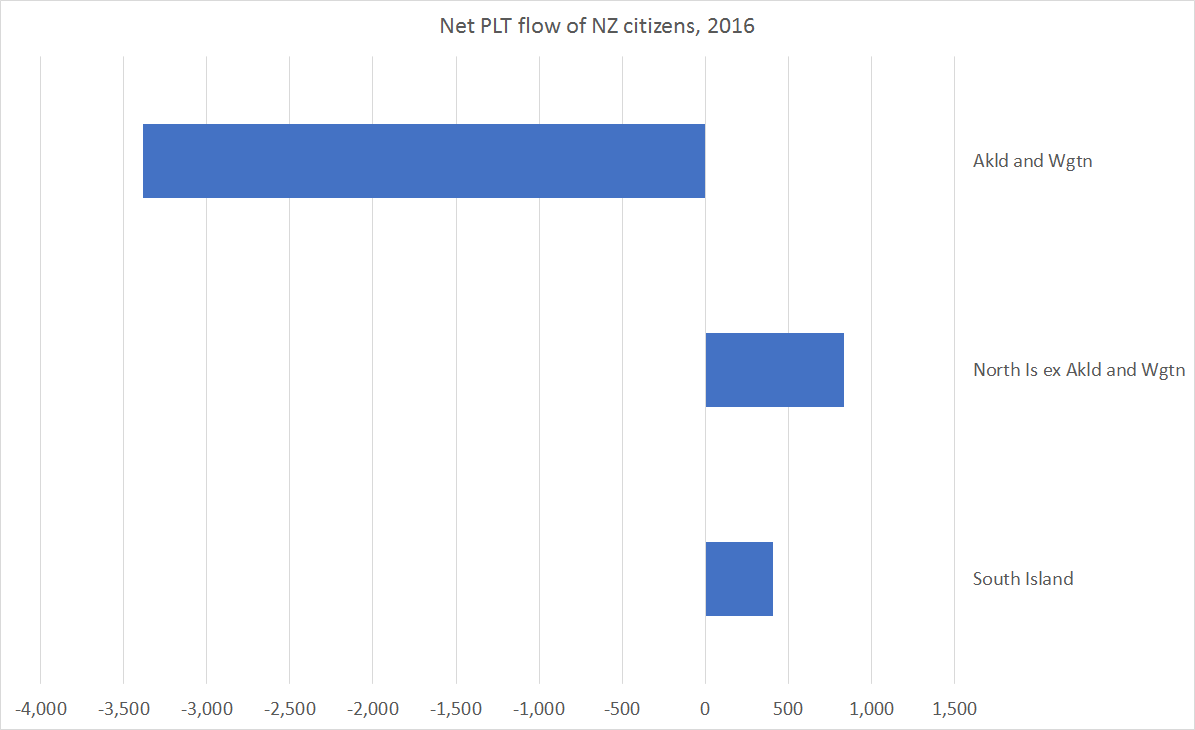

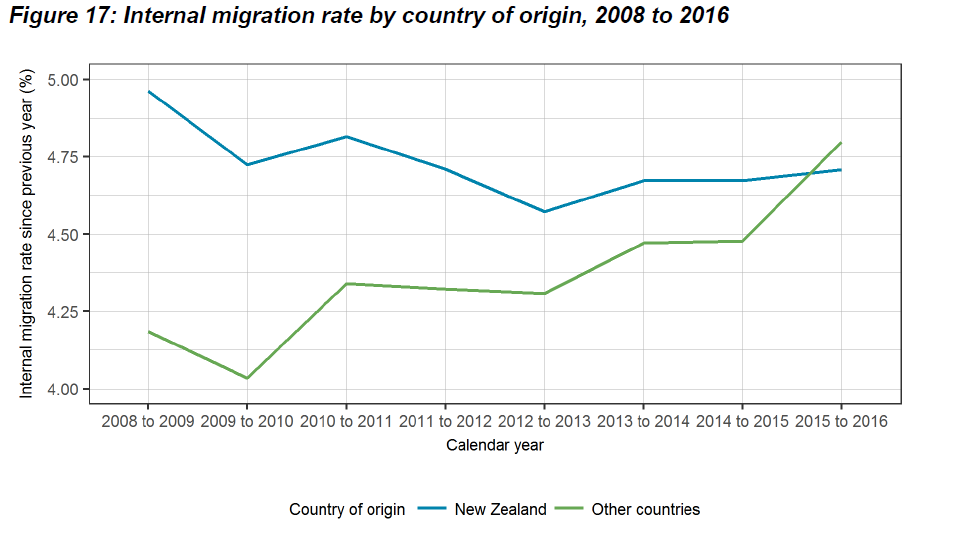

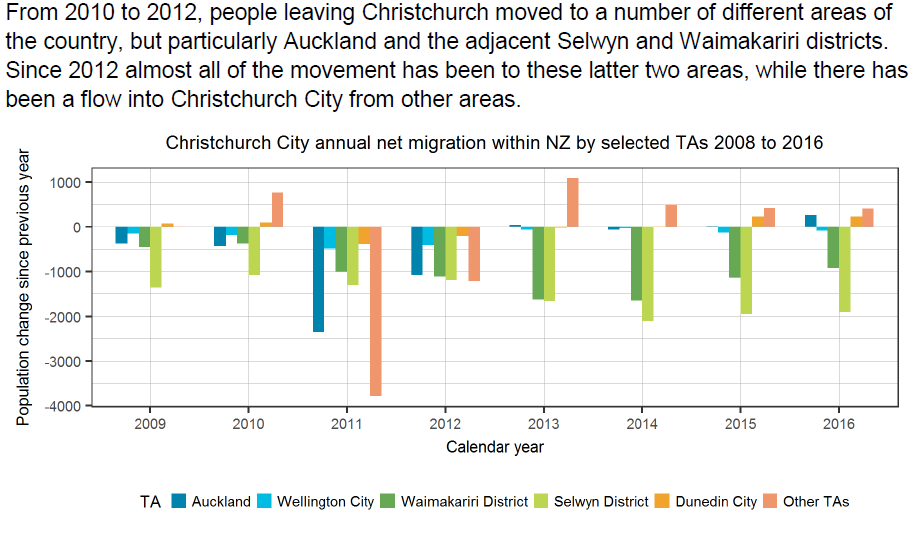

There is a fascinating picture of Christchurch following the earthquakes, including the continuing losses in recent years to neighbouring Selwyn and Waimakariri.

There is a fascinating picture of Christchurch following the earthquakes, including the continuing losses in recent years to neighbouring Selwyn and Waimakariri.

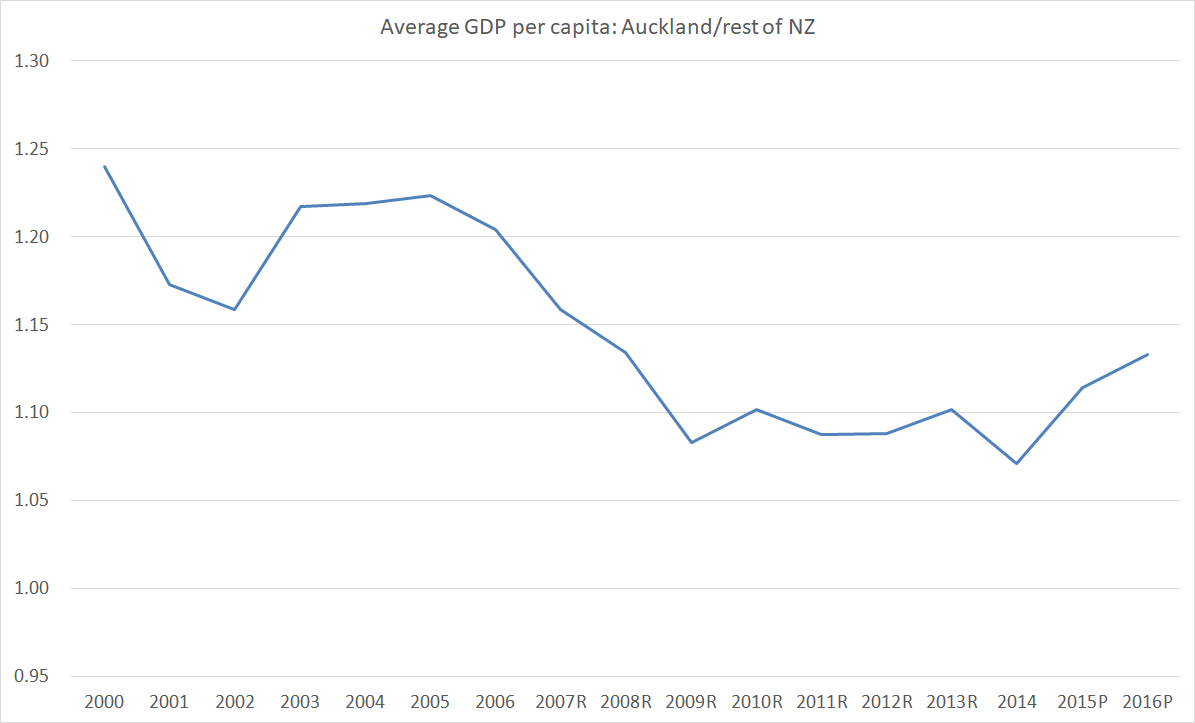

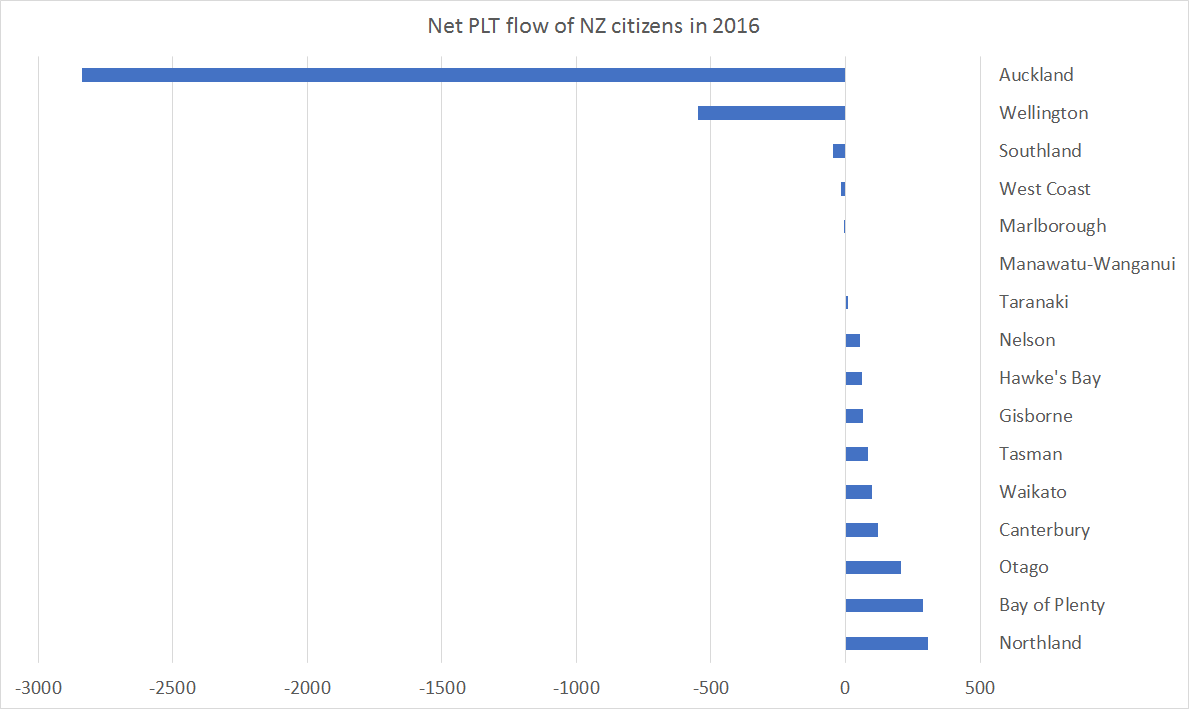

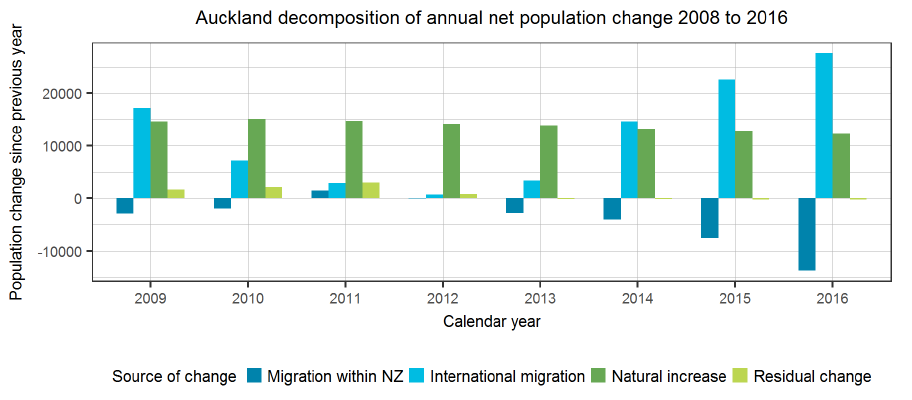

As I observed then, we didn’t know what had happened since 2013. Perhaps things had turned around? But the new Treasury estimates suggest that if anything the outflow – still modest each year – may have accelerated.

As I observed then, we didn’t know what had happened since 2013. Perhaps things had turned around? But the new Treasury estimates suggest that if anything the outflow – still modest each year – may have accelerated.