There aren’t many New Zealand political memoirs/autobiographies – and even fewer diaries (although I was recently reading John A Lee’s for 1936-40) – and most of them aren’t that good. Voracious book buyer that I am, I usually don’t buy them until they turn up very cheap in a charity shop or community book sale. After all, sometimes there are interesting snippets and you never know when some angle on some event might prove at least somewhat enlightening.

But I thought I’d make an exception for Michael Cullen. He had, after all, been an academic historian in an earlier life, and was unquestionably smart and funny, and had been Labour’s finance/economics spokesman for 17 years and Minister of Finance for nine years (terms really only rivalled in modern New Zealand by Walter Nash and Rob Muldoon). I’d probably have been better off waiting for the charity shop copies to turn up.

There were interesting bits and pieces. Early chapters of autobiographies are often complained about but I almost always like them. There was, for example, the ancestor who was the last person burned at the stake in England for heresy (twice actually). Or the snippet of Cullen and his first wife buying their first house in Dunedin in 1971 for $10500 – “only twice my annual gross salary” as a new lecturer (lecturers at Otago now seem to start at about $82000). Or the prize he won at about the same time for the best University of Edinburgh PhD history thesis that year – enough to pay off in full the 30 per cent deposit they’d borrowed from his wife’s parents. Or the picture of the Dunedin Labour Party in the 70s – including the raffle organiser (“Labour used to be a raffle-funded party”) who “made a Ponzi scheme look positively generous” by offering a first prize in one raffle a full book of tickets in the next raffle.

And there were the national politics snippets, including the observation/claim that David Lange had persuaded Roger Douglas to stay in politics in 1981 by promising that if/when Lange became leader Douglas would be his Minister of Finance. As Cullen notes, some things might have been quite different…..although it is interesting to wonder just how much. Cullen’s perspectives – as senior whip and then junior Cabinet minister (often written in counterpoint to Michael Bassett’s book on the period) – on the Lange/Douglas tensions over 1978/88 were worth having, including his suggestion that (given the tensions, that only built further) perhaps Lange should have sacked Douglas in April 1987.

But it tended to go downhill from there, dramatically so for his treatment of the nine years of the 5th Labour government, which takes up almost half the book. Much of it has about it the character of a family Christmas letter from proud parents who just don’t know when to stop. If you want a canter through the things the government did during those nine years, trivial and not, I guess this is the book for you. Almost everyone did everything ably. But to anyone who was around New Zealand at the time, you simply aren’t going to learn very much (although I was surprised to read that Jim Anderton had been – so Cullen claims – one of the ministers most keen on lower company taxes late in the government’s term).

Two things in particular struck me. The first was that while Cullen was a Labour Party MP and minister, clearly he was not a Labour Party person (consistent with this in the early days his then wife had been more active than he was), and there is very little on the internal ructions that convulsed the party a few decades ago. More generally, there is little insight anywhere in the book on the many really significant political figures Cullen worked with over the years, none at all on Helen Clark (or Heather Simpson for that matter). There was almost no insight on some of the key public servants, or anything on the tensions. interactions etc. And this 12 years after he left office. Cullen seems to have reasonably kind words for most people – exceptions I think being Richard Prebble, Don Brash and (mixed with some admiration/envy at his success) John Key – but no insights. And if he ever worked with Grant Robertson, Jacinda Ardern or Chris Hipkins when he was Deputy Prime Minister and they were in Clark’s office, you wouldn’t know it from the book.

Presumably Cullen kept no diaries, and he notes somewhere in the book that he hadn’t been very good at answering questions from researchers over the years about past events because his mental approach was to compartmentalise and then move on (and of course he carried a formidably huge load during those Clark years). And writing the book can’t have been helped by the knowledge that his time might be very short (as it turned out to be) and that between illness and Covid he was only able to make a single trip to Dunedin to consult his papers in the Hocken Library. In a bigger country, he’d almost certainly have had a research assistant he could have drawn on. As it was, he tells us he drew heavily on what happened to be available on the web.

But there is also a sense of someone who – despite the training as an historian (which he often reminds us of) – just wasn’t that reflective. 50 years on from that house purchase he told readers about, house prices are appallingly high – and these developments were going on on his watch too – but there is nothing on how, technocratically and politically, his generation bequeathed that disaster. He was Labour’s finance spokesman for 17 years, beginning as the reforms (which he mostly supported) were supposed to be starting to pay off in reductions in the productivity gaps between us and the rest of the advanced world. Under his watch there were various bows in the direction of aspiring to make a difference. And yet here we are, with the gaps wider than ever. There is no sign anywhere in the book of any reflection, self-questioning, or even curiosity about the failure. Perhaps the only note of regret about policy I recall is a regret that the government had not been more active in determining the strategy of Fonterra, the behemoth they enabled but which also failed to deliver.

Perhaps it would have been different if he’d had more time. Even on the text he did write it is not hard to see where a good editor could have insisted on cutting out at least 50 pages (of a 400 page book) – perhaps including the line that knighthoods were a good thing because they gave a lot of pleasure to the recipients.

Of course, part of my interest in the book was in its treatment of Reserve Bank issues, he having been the Minister responsible for the Bank through nine sometimes difficult years, and Opposition spokesman beginning little more than a year after the 1989 Reserve Bank Act had come into effect. The Reserve Bank monetary policy framework has not, shall we say, been without its controversies over those 30 years – including the often very antagonistic approach taken by Jim Anderton whose party at times rivalled Labour on the left in the 1990s.

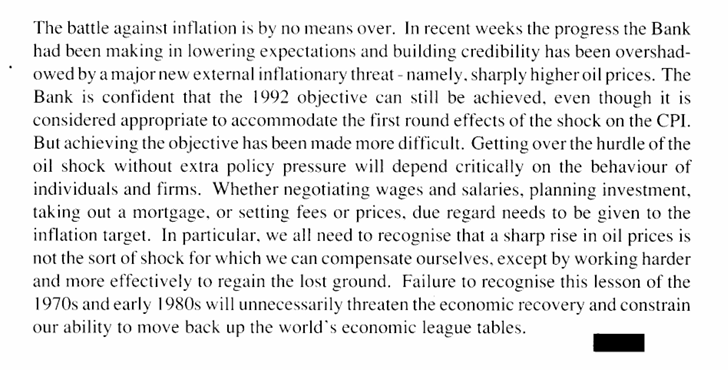

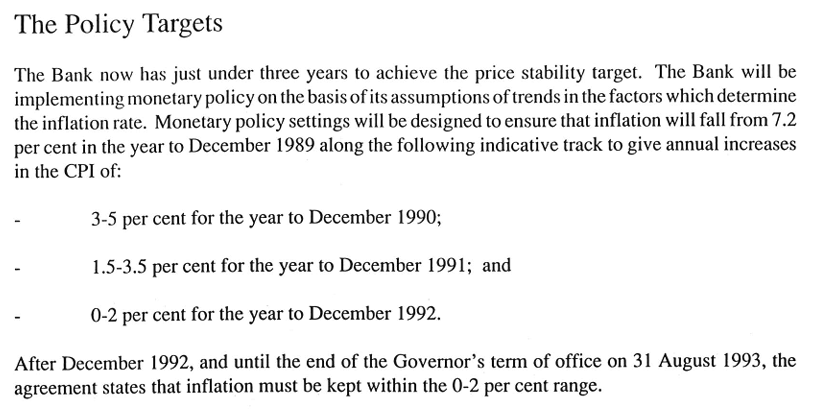

But again, it was curiously bloodless. You’d not have known, for example, that in his early days (perhaps as late as the 1996 election, as I recall us debating it at the Bank at one election and I was working overseas in 1993)), he (as Labour’s spokesman) championed a change to the inflation target (then 0-2 per cent annual inflation, with caveats). But Labour’s proposal – they needed product differentiation from National, the Alliance, and New Zealand First – was to adopt a target range of -1 to 3 per cent inflation. As I recall it, part of the aim was to capture more of the headline inflation shocks (oil prices, tax changes etc etc), but it could have led to the curious world in which the Bank was supposed to be more or less indifferent to inflation going negative, which didn’t seem as though it would prove very robust at first confrontation with experience.

Perhaps charitably, Cullen does not mention the (frankly fairly incompetent) way we ran monetary policy over 1997 and 1998 (the infamous monetary conditions index) but nor does he mention his oft-expressed (and somewhat valid) concerns about the volatility of both the exchange rate and interest rates, or his calls for changes to the Policy Targets Agreement and/or for an independent inquiry into the conduct of monetary policy. As it happened, the PTA was changed when Cullen took office, to add a new form of words that was supposed to appear substantive but which, to this day, no one really knew what the words actually meant for policy (I’ve long argued “precisely nothing”). At the Bank we were sufficiently uneasy that in the first few weeks of the new government I was sent on a whistle-stop 10 day tour of the RBA, the Monetary Authority of Singapore, the Bank of Japan, the Bank of England, the Bank of Canada, the Federal Reserve and the US Treasury to brush up our knowledge of, and perspectives on, operationalising foreign exchange intervention.

Out of office Cullen had called for an independent inquiry – which went over well with the left of his own party, and with the Alliance, with which Labour was mending fences. In office, he commissioned an inquiry, but consciously and deliberately chose as his reviewer someone who could be counted on not to make trouble – a leading academic author on inflation targeting, Lars Svensson (he could quite readily have chosen as reviewer any number of other quite reputable people – just one example being Bernie Fraser the former Governor of the RBA (and known as somewhat left-leaning). As it was, Svensson predictably made no difficulties and at times we (I was one of the small secretariat) had to talk him into revising down his effusive praise of Don Brash. He did propose adopting an MPC – but made up solely of executive staff of the Bank – a proposal that Cullen rejected, and what came out of the review were very minor changes indeed (the Governor to no longer chair the Bank’s Board, the Board to write an Annual Report). But he’d been seen to have had a review.

If there were ongoing government niggles re the Bank’s monetary policy they must have been quite limited for a while. In 2001 we’d been quite pro-active in easing monetary policy (somewhat burned by 1997/98) both in response to the global tech slowdown and after 9/11 (decisions I still think were warranted, but which some more hawkish people differ on). But Don Brash was still a bit of an issue. He’d made a high profile controversial speech to the government’s Knowledge Wave conference in 2001, stepping well outside areas he had any policy responsibility for (and, not surprisingly, championing policy approaches that weren’t really to Labour’s liking). Powers that be in the Beehive were understood to be not best pleased.

Nothing of all this in in the book.

Don Brash resigned as Governor on 26 April 2002 to seek selection as a National Party candidate at the forthcoming election (having been pro-actively recruited and given to understand he’d get a high list place, and perhaps a reasonable chance of being Minister of Finance – in the unlikely event National was to win). Cullen writes about this resignation, but comments only that he was “flabbergasted”, proceeding to write some generalised negative comments about Brash and his self-belief. As Don records in his own autobiography of his conversation with Cullen “I don’t think he was pleased but he was polite”, but he goes on to note “much more polite than Helen Clark was later in the day”. As I understood it, the PM had been (understandably in my view) outraged, felt it was something of a betrayal (to step straight out of high public office onto the campaign trail) and was specifically very aggrieved at the Bank’s Board (and specifically the then chair of the non-executive directors) – responsible to Cullen – for having written an employment contract that did not enforce a decent stand-down period. All of which might have been useful points for Cullen to have included, rather than just glib remarks (true or not) about Brash’s “extraordinary sense of self-belief”.

Appointing a new permanent Governor was a challenge. Under the law, the Governor had to be someone the Board nominated, but the Minister could reject a nomination and ask (endlessly, in principle) for another. Brash’s deputy, Rod Carr, filled in as (statutory) acting Governor including through the election campaign period, and assiduously sought to get the permanent role. Cullen records – and this I did not know – that the Board had formally recommended that Carr be made Governor.

I had nothing personal against Rod, but he was so dry that he made even Brash look slightly moist. I was not in the least convinced that he could adopt the somewhat more flexible approach I was looking for. I rejected the recommendation….Finding a replacement posed a problem, especially if my action was interpreted to mean a lack of commitment to the basic principles of the Reserve Bank Act. I was saved by Alan Bollard. He offered to put his name forward.

Of course, it would not have been hard to have found someone else, except that the understanding was that the word had gone out that no one associated with the Brash Reserve Bank was to be appointed. Thus, Murray Sherwin – until recently Deputy Governor, then Director General of Agriculture – would have made a good Governor, but he’d been of the Brash era. Less plausibly – though probably with politics more akin to Labour’s – another former Brash Deputy Governor Peter Nicholl (then Governor of the central bank of Bosnia) might have been keen (although I know the Bank’s Board wasn’t).

Again, what Cullen doesn’t record was the fascination with the RBA in the Beehive (including the 9th floor at the time). In some ways it was understandable – the RBA was run by a succession of competent people, the Australian economy was generally doing better than New Zealand’s, real interest rates were generally a bit lower (visiting RBA people would even encourage us to be more like them and we might get our interest rates down to “world” levels) and had been less volatile. My diary records a conversation with someone who had been to visit Peter Harris – now an MPC member, then Cullen’s main economic advisor – during this period, and Harris had apparently even toyed (perhaps not fully seriously) with the idea that they could get Glenn Stevens (then Deputy Governor of the RBA) as Reserve Bank Governor. The Prime Minister was known to want a policy target mirroring the Australian one (centred on 2.5 per cent inflation), something that Alan Bollard successfully resisted).

(Cullen goes on to record that he also knocked back SSC’s recommendation of Mark Prebble to be Secretary to the Treasury, primarily on ideological grounds. That was interesting but he never tells his readers that at the time – when Cullen was deputy PM – Prebble was chief executive of DPMC, that Clark had attacked that appointment in 1998 (again on ideological grounds) but had acquiesced in Prebble’s reappointment in 2000). It might have been interesting to have read some reflection on what changed.)

The period from late 2003 to the end of Labour’s term was a difficult one for monetary policy. Cullen does a little bit of sniping in the book – mainly at the idea that the Bank was engaged in targeting inflation forecasts (he words it a little differently but it is the implication of his repeated comments about an output gap focus) – but he displays almost no awareness of what was going on (including the sustained and significant rise in actual core inflation, the demand effects of rapid growth in population, the demand effects of the housing market (prices and volumes), the strong growth in the terms of trade, or the implications of fiscal policy. And I don’t think he once mentions the exchange rate, which became an increasing bugbear through this period, both for him and for his handpicked Governor. The best evidence for the proposition that throughout those years we did not tighten aggressively enough early enough is that core inflation moved to and beyond the top of the inflation target range (as benchmark, in the subsequent decade core inflation undershot, but never quite fell outside the bottom of the band).

There was an increasing search for some sort of circuit-breaker, with a particular focus then on things that might help dampen housing market pressures without necessitating further OCR increases and further rises in the real exchange rate. This culminated first in the Supplementary Stabilisation Instruments project, which Cullen claims to have known almost nothing of. This is the relevant extract from his book.

Both the Reserve Bank and the Treasury realised that in that situation [economic imbalances] the use of the official cash rate as almost the only means of dealing with such imbalances was far from satisfactory. It was rather like many anti-cancer drugs in causing significant collateral damage, so they had decided to work on what they called a Supplementary Stabilisation Instruments Project. This was their initiative, not mine, but it got John Key excited and he managed to invent all kinds of malign intentions the government had. I have no idea where the project went since it did not seem to produce any results.

Which simply wasn’t true. House prices became such a political problem there was a special unit set up in DPMC to look at what might be done, and John Whitehead and Alan Bollard agreed with Cullen to commission the SSI work. In a release at the time, Cullen claims that

He expressed concern at the impact of the high dollar on the export sector but said the Supplementary Stabilisation Instrument Project, the terms of which were drawn up by the Treasury and the Reserve Bank and released without reference to the government, would explore options to reduce pressure on the exchange rate by reducing monetary policy reliance on the OCR.

I can’t remember if the precise Terms of Reference were cleared by his office, but it was made very clear (from the Beehive) that difficult political options (capital gains taxes, public sector savings programmes, anything around the welfare system) were out of scope. These specific exclusions are mentioned in the published Terms of Reference (page 39 here). Cullen’s hands were all over this commission (my diary records a week or two prior an observation that Cullen, Bollard, and Whitehead had all apparently been keen on some particular tweaky tool I’d devised – I can’t recall what it was but am embarrassed that it seems to have been an LVR-based control).

The Minister goes on to claim that “I have no idea where the project went since it did not seem to produce any results”. Except that, readily available on the web, is our report to him on the analysis and possible tools, from March 2006.

And did it go no further then? Well hardly. Instead there was some considerable interest in the idea of a Mortgage Interest Levy – a scheme under which we might raise the cost of mortgages without raising the OCR – and I and a Treasury counterpart spent (what seems like) months devising something that might be workable, exploring fishhooks etc etc. That paper is here, as is the report to Dr Cullen.

And was this simply a bureaucratic conceit, or no interest to a busy Minister of Finance? Well, no. Actually, Cullen tried to persuade the National Party to go along. I knew this was so, but looking through some old papers found a press release from Michael Cullen, as Minister of Finance (9 February 2007), saying so and attacking Bill English (new National finance spokesperson) for not being willing to go along.

National leader John Key and finance spokesman Bill English are clearly at odds over the concept of a mortgage levy, which could potentially ease pressure on exporters, Finance Minister Michael Cullen said today.

…I can now reveal that Mr Key and Mr English were invited to a meeting in my office before Christmas to discuss alternatives to existing monetary policy instruments to tackle inflation.

…At that meeting Mr Key took a balanced and serious approach. Mr English though largely remained silent and his body language spoke volumes about his willingness to embrace new measures that may have a chance to help the New Zealand economy

And so on.

And at that Cullen requested that further work be discontinued.

Cullen was a busy man, but it wasn’t as if this was an isolated project. The Minister continued to express concerns – quite serious ones. Not six years after his Svensson review had reported, Labour initiated a full-scale Finance and Expenditure Committee review of monetary policy (quite possibly intended more for shown than substance). More than once Cullen opened mused about the powers open to him under the Reserve Bank Act (but never used) to direct the Bank to pursue a different target (I wrote the internal paper musing on how we should respond, what options the Minister had, what constraints there were on him) and he also became increasingly critical of our public line that fiscal policy was adding to demand and inflation pressures, all else equal putting the real exchange rate and the OCR higher than they otherwise would be. Labour was on its late-term fiscal splurge (helped by Treasury advice that concluded the boom-time revenues were mostly permanent) and although the budget was still in surplus, running down that surplus actively added to the imbalances in the rest of the economy. For Cullen no doubt it was politically awkward – Labour was well behind and the polls, and the money was there. We were reduced to (among other things) writing boxes in the Monetary Policy Statement to explain our (entirely conventional view).

My point here is not that Cullen would necessarily have remembered all of this – busy man etc – but there is not even a hint of any of it. The book would have been much better with at least some of it, rather than the Christmas letter type of account.

Out of curiosity, I also looked for Cullen’s account of the genesis of deposit guarantee scheme. It is a somewhat self-serving account, including his attempt to blame the entire South Canterbury Finance situation on the National government that took office the following month. I wrote my own account of those few days here (I was very closely involved), and included this paragraph.

The main, and important, area in which Dr Cullen departed from official advice was around the matter of fees. We’d recommended that the risk-based fees would apply from the first dollar of covered deposits (as in any other sort of insurance). The Minister’s approach was transparently political – he was happy to charge fees to big Australian banks (who represented the lowest risks) but not to New Zealand institutions (including Kiwibank). And so an arbitrary line was drawn that fees would be charged only on deposits in excess of $5 billion. Apart from any other considerations, that gave up a lot of the potential revenue that would have partly offset expected losses. The initial decision was insane, and a few days later we got him to agree to a regime where really lowly-rated (or unrated) institutions would have to pay a (too low) fee on any material increases in their deposits. A few days later again an attenuated pricing schedule was applied to deposit-growth in all covered entities. But the seeds of the subsequent problems were sown in that initial set of decisions.

They were his calls to make, and it was an election campaign, but perhaps a political memoir would be more helpful in revealing some of the tradeoffs, tensions, risks etc (or even the fact that – especially with Parliament dissolved – a Minister of Finance could issue such blanket guarantees with few/no checks and balances.

These were just the areas that I know something about in depth. So I’m left wondering what weight I should put on any of the rest, other than as chronology (which I too could get from the web).

On the front cover of the book, Helen Clark describes Cullen as “one of our greatest finance ministers”. There aren’t that many (relatively long-serving ones) to choose from but I’d hesitate to endorse the accolade. Running down the public debt was an achievement but (a) demographics, (b) a prolonged, but productivity-lite, boom, and (c) the terms of trade ran strongly in his favour, and the dam burst in the final three years of his term. I guess he has monuments to his name – Kiwisaver and the NZSF (“Cullen fund”) – but then so does Bill Birch from his time as Minister of Energy, and the best evidence to date is that Kiwisaver has not changed national savings rates, and it isn’t clear what useful function the big taxpayer-owned hedge fund has accomplished. Meanwhile Cullen – and Clark herself of course – bequeathed to the next government (who in turn bequeathed it to this one), the twin economic failures: house prices and productivity (the latter shorthand for all the opportunities foregone, especially for those nearer the bottom of the income distribution).

In that sense, what marks him out from a generation or two of New Zealand politicians, who have spent careers in office, and presided over the continuing decline?