There was a great deal of debt defaulted on during the Great Depression. Businesses failed, farms went bust, and some mortgage borrowers defaulted too. But a huge number of governments also defaulted on their obligations, not just in places like Greece or Argentina which had form in that regard, but including many of the governments of the richest countries in the world. You could read about the New Zealand episode here. Most countries in Europe (including the UK and France) defaulted on their (substantial) war debts to the United States – in fact, only Finland paid in full. But even the United States government defaulted.

There is an interesting and accessible new book out about that experience, American Default. It is written by UCLA Chilean academic Sebastian Edwards (who has been used as an adviser and author here, including this paper at a Treasury/Reserve Bank conference a few years ago), who got onto the subject after acting as an adviser to law firms involved with sovereign defaults by Argentina after 2001.

Going into the Great Depression most countries were, directly or indirectly, on the Gold Standard (indirect in New Zealand’s case, where the banks managed the exchange rate to maintain parity with sterling which was fixed to gold). But the US situation was a bit different than most. After the experiences with inflation (and fiat money) during the Civil War, in the subsequent decades – right up to the early 1930s – US government bonds were issued with a provision (the “gold clause”) that entitled the borrower, at his/her own option, to be repaid in gold. Many corporate bond contracts had similar provisions. They were intended as a protection for the lender against unexpected inflation (arising when the fixed parity between dollars and gold was broken, or abandoned), and at least in the early decades must have allowed US borrowers to borrow more cheaply, and/or for longer-terms than they would have otherwise been able too. In that respect, they were similar to the way in which many countries with a track record of high or variable inflation found it difficult to borrow in their local currency, and borrowed in foreign currencies instead.

By 1933, many countries (notably the UK) had already broken the link to gold. But the US (and France and several other smaller European economies) hadn’t. Breaking the link was part of what enabled those countries to begin recovering from the Depression (both by devaluing against gold-based currencies, and by allowing interest rates to be cut further). By 1933, there was plenty of gold in the US, but no recovery – indeed, Roosevelt took office in the midst of a banking panic. As in many other countries, the price level had fallen significantly, such that the real value/burden of any debt contract outstanding was materially greater than had been expected only a few years earlier.

That said, the US government itself was not particularly heavily indebted. Economic historian Peter Temin’s book on the Great Depression includes a table suggesting that gross debt of all level of US government in 1929 had only been about 35 per cent of GDP. (By contrast, in New Zealand, Australia, and the UK general government public debt in 1929 had been in excess of 170 per cent of GDP.) Corporate bonds outstanding seem to have been of a similar size. Of course, in all cases these debt ratios rose as economies moved towards the depths of the Depression, as both real GDP and the level of prices fell.

It seems that Roosevelt didn’t have a clear strategy in mind when he took office (and the tie to gold hadn’t been a campaign issue). The actual approach unfolded gradually over the year or two after he took office. What did the US government do?

The first major step – extraordinary in a free society – was to simply outlaw private sector holdings of gold. All but trivial amounts of gold had to be delivered to the government, with less than a month’s notice, for which holders were paid at the then still-current official price of gold (US$20.67 an ounce). Private holdings of gold were forbidden for decades. A few weeks later Congress passed a declaration explicitly prohibiting gold clauses in future securities issues, and abrograting (voiding) existing provisions. The government then began buying up gold (in the international market) steadily raising the US dollar price of gold until in January 1934, with Congressional authorisation, the official price was reset at $35 an ounce (where it remained until 1971). US citizens couldn’t get hold of gold, but the US remained willing to buy at the price from overseas sellers.

In effect, the US was off the Gold Standard and had devalued its exchange rate. Gold purchases were increasing the domestic monetary base. In combination, such measures should, and did, support a lift in US economic activity and in prices (commodity prices in particular, in USD terms, rose quite quickly and substantially as one might expect).

And, in the process, the US government managed a huge windfall gain for itself. As another recent treatment of this episode (by Richard Timberlake, not referenced by Edwards) records, the book profits on the revalued gold was roughly equal to total Federal government revenues in 1934. Compel citizens to sell you an asset at one price and then re-set the price, more in line with economic realities, and in the process transfer a great deal of wealth from citizens to the government. It isn’t the sort of approach one would normally expect in a country with the rule of law.

But, of course, the interesting thing about the United States is the way the constitution sometimes intrudes in the freedom of governments to do just as they want. Had a New Zealand, Australian, or British government adopted measures like those in the US, there would have been nothing much anyone could have done about it, once the parliamentary battle was lost. But in the US many of these sorts of issues are only finally resolved at the Supreme Court, testing the validity of congressional or executive actions against the provisions and protections of the Constitution.

And that is what happened in this case, although only in respect of the abrogation of the gold clauses. There were several cases taken, each with slightly different factual bases, covering both private and government obligations. The claim wasn’t to be paid in physical gold – private holdings of which were now illegal – but to be paid the dollar value of the gold equivalent when the bond had been issued. In dollar terms, that would be 69 per cent (35/20.67) more than otherwise. There were substantial sums at stake.

As Edwards illustrates, the Supreme Court hearings were closely followed by markets and the press (and at the time the court was perceived to be roughly evenly divided between what might loosely be described as “conservatives” and those of a more moderate or “progressive” disposition). Media coverage suggested that the government’s lawyers had not had the best of the hearings themselves. The Court’s ruling was eagerly awaited, and with some trepidation by the government. Contingency planning had been undertaken, and in Roosevelt’s papers is the draft text of an address he intended to deliver had the Court ruled comprehensively against the government, and papers outlining the actions he intended to initiate in response. An adverse outcome wasn’t going to be acceptable. Roosevelt seems to have regarded the abrogation of the gold clauses as an essential element in his overall strategy to lift economic activity and prices; indeed one of the key arguments made to the Supreme Court was around a justification of national emergency.

As it happens, the government won in practice. The abrogation of the gold clauses, at least as applied to Federal government debt, was ruled unconstitutional (by an 8 to 1 margin). But by a 5 to 4 margin, the Court ruled that the abrogation had not produced any damages to bond holders, and so those bondholders were prevented from taking further action (in something called the Court of Claims) against the government. In other words, there were to be no practical consequences for having passed an unconstitutional law (I’m not entirely clear – it isn’t discussed in the book – why having ruled it unconstitutional the Court didn’t overturn that provision, but clearly they didn’t).

Had the gold clauses in private and government bonds been allowed to stand, issuers would have been required to pay 69 per cent more (dollars) than otherwise (but, in effect, the same amount of gold). In his book, Edwards seems to accept that this would have been a highly damaging, undesirable, and unacceptable outcome. I’m less convinced.

For a start, they were the terms on which contracts had been entered into (at numerous different dates), and the cases before the Supreme Court all involved substantial and sophisticated issuers including the US government itself (although I understand that some residential mortgages at the time may also have contained the clause). And it is not as if changes in gold parities and prices had never happened before (indeed, in other countries they had been frequent during World War One and the subsequent decade). No one, in contracting – or purchasing – these bonds could credibly claim to have put no weight at all on the possibility of the US ever changing the gold price of dollars. In fact, the US was still issuing bonds containing the gold clause into 1933, 18 months after the UK (for example) had gone off gold.

It is probably fair to suggest that no one really anticipated a deflationary event as severe and sustained as the Great Depression, but there is at least an arguable case that bankruptcy courts and limited liability exist to handle cases where things turn out unsustainably far from expectation. But that is a case-by-case procedure, not a blanket transfer of wealth from lenders to borrowers. In the US government case – see the numbers earlier – federal debt was not large and even Roosevelt acknowledged that losing the case would not have bankrupted the government. Quite possibly the situation would have been different for some corporates. But it is also worth remembering the whole point of the Roosevelt strategy (not so different in its end aims from those in many other countries), which was to markedly raise the economywide price level and reverse the sharp falls that had happened during the Depression. To the extent that strategy was successful, the abrogration of the gold clauses would clearly leave lenders materially worse off than they would have been otherwise. For borrowers in the tradables sector (admittedly probably a minority), the depreciation in the exchange rate itself markedly (and immediately) improved their capacity to service the debt, so it is even less obvious what the case was for the arbitrary use of government power to provide debt relief.

One of the government’s other arguments was that since the price level in the mid 1930s was materially lower than it had been a decade earlier, anyone who held the bonds throughout would be getting an unexpected windfall gain simply being paid out in dollars (since the purchasing power of those dollars was greater than it had been), let alone being paid out at the new higher gold price. But even to the extent that argument was valid, it doesn’t take any account of secondary market trading in the affected securities. A person who purchased a new issue bond in (say) 1926 might indeed be getting a windfall gain – and windfall gains and losses happen all the time in economic life – but a secondary market purchaser who’d purchased that bond in late 1932 would have lost out badly (and might well have put a high value on the gold clause as protection against just such an eventuality).

(To illustrate the windfall point, in the late 1980s and early 1990s New Zealand governments were determined to get inflation sustainably down. There wasn’t a great deal of confidence that would happen. As late as November 1990, the 10 year bond yield averaged 12.96 per cent. Actual CPI inflation in the subsequent 10 years averaged 1.8 per cent. Similar windfall losses happened when inflation unexpectedly rose, and stayed up, in the 1970s.)

The sorts of revaluation effects the Roosevelt administration successfully tried to overturn happen not infrequently in systems where borrowers – especially those not in the tradables sectors, without an export revenue hedge – have taken on considerable foreign currency debt, only for a substantial devaluation or depreciation in the exchange rate to occur. It happened, for example, in New Zealand in 1984: much of the government’s debt was in foreign currency terms, and a 20 per cent devaluation immediately increased the servicing burden by 25 per cent. Granted that New Zealand wasn’t in the depths of a depression in 1984 , but no one thought it would fair, reasonable (or even possible) to default on that additional servicing burden.

But in the early 1930s, both New Zealand and Australia were in the depths of really rather severe economic depressions – perhaps not quite as bad as in the US, but certainly much worse than in, say, the UK. Both countries had really large volumes of central, local (and state, in Australia) government debt issued abroad – debt burdens far heavier than those facing the US government when Roosevelt took office. The distinction between New Zealand or Australian pounds and pounds sterling wasn’t that clear in those days, but as the exchange rate diverged during the Depression, initially with government acquiescence and then at government direction (our own formal devaluation happened in early 1933) debts payable in London were suddenly costing the borrowers far far more than they had envisaged (in New Zealand pound terms). And the price levels in New Zealand, Australia, and London were all quite a bit lower than initially envisaged. New Zealand and Australian governments would have welcomed some debt relief on their overseas debts, but it never came: the powerful counterargument was “well, if we are going to successfully boost global price levels such relief won’t end up being necessary”. And it wasn’t.

The big difference perhaps between the New Zealand and Australian cases and the US one in the 1930s is that the US debt was almost entirely held by domestic investors and was issued wholly under US domestic law. The US didn’t need to tap international markets on a continuing basis, unlike both New Zealand and Australia. And so New Zealand and Australia imposed defaults in respect of government debt issued to domestic holders, but not to foreign ones, and the bulk of the (public) debt was foreign. But rereading the account of the New Zealand (and Australian) experience in the 1930s, what is striking is the extent to which lenders were willing voluntarily to write down the value of their claims, voluntarily converting to less valuable (government) securities, apparently from some sense of “fairness” or the “national interest”. One can wonder what sort of response Roosevelt would have achieved had he tried moral suasion rather than legislative coercion. Perhaps it wouldn’t have worked for private sector issuers – and for example, the New Zealand government used various legislative interventions in the 1930s to relieve farm debt – but some case-by-case approach still seems preferable than the rather arbitrary use of legislative instruments to relieve all corporate borrowers from obligations they voluntarily entered into. Especially, when the economy and the price level were just about to recover, improving (markedly) future servicing capacity.

Of course, had the US recovery subsequently been strikingly more robust and successful than those of other countries, there might be a stronger prima facie case for this (distinctive) debt relief component of Roosevelt’s strategy. But it wasn’t. As is well-recognised, it wasn’t until around 1940 that real GDP per capita in the US got back to 1929 levels (years behind, say, New Zealand, Australia, and the UK in that regard). And the recovery in the price level also lagged.

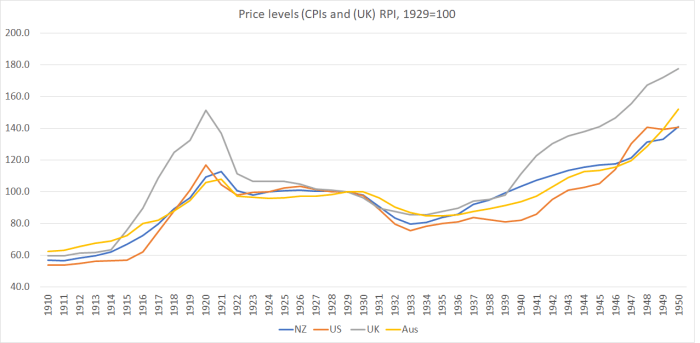

Here is a chart of the price levels, indexed to 100 in 1929.

Prior to World War One, price level movements tended to be quite slow and gradual. There was little sign anywhere of entrenched expectations of future trend changs (up or down). After World War Two, inflation became an entrenched feature of the system. In this period, things were in transition. There were windfall gains and losses, falling heavily on different groups at different times. But if deflation was the story of the Depression specifically, across all four countries the dominant theme of the period is a lift in the price level. Even by 1939, in New Zealand and Australia and the UK price levels were more or less back to pre-Depression levels (it took a few years longer in the US). There seems little obvious case for a borrower, not initially over-indebted, to use legislative powers to abrogate contracts freely entered into to remove significant value from lenders, at a time when the entire of macro policy was to drive up the price level.

A fair, and interesting, point Edwards makes (and which I also make in the treatment of the New Zealand default) is that there were few obvious adverse consequences from this US default. There is little sign that borrowers became more reluctant to lend, or charged higher risk premia. If so, that suggests that perhaps people in aggregate really did see it as a step not unjustifed in the extraordinary circumstances.

It is an interesting book about a now little-known episode in US history. Edwards combines history, economics, and legal analysis, but presents in a way designed to appeal to the intelligent lay reader, not just to the geeky economic historian. Debt default episodes – here, there, and everywhere – should be better understood. We surely haven’t seen the last of sovereign defaults perhaps – the way fiscal policy is going – even in the United States.

interesting stuff. Well done

LikeLike

Hi Michael

Arthur Nussbaum, “A history of the dollar” 1957 has a very good coverage of this whole episode, including the reason why there were gold clauses in all the private contracts (the devaluation of the dollar during the Civil War). His whole book is fascinating and gives a lot of insights into the legal theory of money. I used his treatment of this example in my undergraduate international finance course from 2000 – 2005 – as evidence of the time that even the US defaulted on its obligations and changed the rules on private contracts. It used to surprise the students (but I didn’t have the wit to write a book about it.) from my lecture notes, Nussbaum suggests $75 billion of private contracts were affected – an enormous sum.

This episode had much longer ramifications as it explains why the US took so long to develop indexed financial contracts. As Nussbaum makes clear, this episode showed that since 1792 the US government had the authority to arbitrarily change financial contracts In 1939 the Supreme Court extended the Gold Clause case to to rule void all forms of debt indexation This ruling was not repealed until 1977. Theis (1995) covers this history – I quoted him in a paper I presented at the RB in 2004 about the desirability of indexed contracts. (Somewhat surprisingly, the Bank and the Treasury were little interested in indexed debt at the time. Indeed, the New Zealand Treasury was shamefully slow to consistently reissue index-linked debt, finally doing so well after a decade after many other countries.)

Theis, Clifford (1995) Introduction pp v-xix in

Money and Banking: The American Experience (Fairfax, Va: George Mason University Press, 1995)

Andrew

LikeLike

Thanks Andrew. Edwards does use Nussbaum’s book. The govt’s case to the Supreme Court argued that there were $80bn of private contracts with gold clauses (around 75-80% of GDP equivalent), but what seems lost sight of in that discussion is that those debts were payable over decades (not all in 1933), and since the whole strategy qas to raise the price level, the borrowers would – most likely – not have impaired capacity to pay over the decades ahead.

I did think about pulling down this morning the box with articles about the connection to indexed debt more broadly, but didn’t do so. I’ve always been rather sceptical that even if indexed debt had been lawful between 1939 and 1977 there would have been material amounts issued. After all, there was little or no such issuance in other advanced countries with similarly moderate inflation problems.

On indexed debt in NZ, I think you are a little unfair. The NZ govt first issued indexed debt in the 70s (retail bonds), and issued its first wholesale indexed bonds in 1983, and then again for a while from 1995 (that effort driven from the RB, altho we tended to lose interest later because of the tax treatment). By the early 00s, there was an arguable case that the govt would struggle to maintain any material debt issuance outstanding.

(None of which is intended as a general defence of Tsy or its DMO wing over the decades.)

LikeLike

Reblogged this on Utopia, you are standing in it! and commented:

Nz defaulted in the early 1930s

LikeLike