12 October 2008 was a frantic day. It was a Sunday, and I never work Sundays (well, two financial crises, one in Zambia, one in New Zealand, in 30+ years). There was a call in the middle of our church service summoning all hands to the pump, to put in place a retail deposit guarantee scheme that day. We did it. My diary later that night records that we’d “delivered a brand spanking new not very good deposit guarantee scheme”, announced a few hours earlier. It was a joint effort of the Reserve Bank and The Treasury.

I had recently taken up a secondment at The Treasury. I’d been becoming increasingly uneasy about the New Zealand financial situation for some months (flicking through my copy of Alan Bollard’s book on the crisis I found wedged inside a copy of an email exchange he and I had had a month or so earlier about Lender of Last Resort options for sound finance companies, potentially caught up in contagious runs) but I hadn’t had any material involvement in the unfolding sequence of finance company failures. But it was the escalating international financial crisis – this was four weeks after Lehmans, 3.5 weeks after the AIG bailout, two weeks after the US House of Representatives initially voted down TARP, and two weeks after the Irish government surprised everyone by announcing comprehensive deposit guarantees – that really accelerated interest in the question of what, if anything, New Zealand should do, or might eventually be more or less compelled to do. The initiative for some more pro-active planning came from The Treasury, but with some parallel impetus – including around guarantees – from the then Minister of Finance, Michael Cullen (who, a few days out from Labour’s campaign launch, was also looking for pre-election fiscal stimulus measures).

On Tuesday 7 October, there was a long meeting at the Reserve Bank, attended by both the Secretary to the Treasury, John Whitehead, and the Governor of the Reserve Bank. My memory – and my contemporary diary impression – is that the Governor was considerably more focused on the managing the Minister’s political concerns than on any sort of first-best response. But the outcome of that meeting was agreement to quickly work up a joint paper for the Minister which would not, at that stage, recommend introducing a deposit guarantee scheme, but which would outline the relevant issues and operational parameters, giving us something to work from if the situation worsened.

Which it quickly did, both on international markets, and with the political pressure, with the Prime Minister signalling that she wanted to be able to announce something about guarantees in her campaign launch that coming Sunday afternoon.

I and a handful of others on both sides of The Terrace scurried round for the next few days. I see that in my diary I wondered what the best approach was: do nothing, allow some risk of the crisis engulfing us, and then pick up the pieces afterwards, or be more pro-active and take the guarantee route. My conclusion – and even today I wince at the parallel (but this was a late-at-night comment) – “I suspect that if the pressures really come on, the Irish approach is best”. As relevant context, although much of the finance company sector was in solvency trouble (many had already failed) there were no serious concerns about the solvency of the banking system. (Liquidity was, potentially, another issue.)

At Treasury we had recognised the importance of the Australian connection – most of our banks being Australian-owned. I’m not sure of the date, but we had taken the initiative – at Deputy Secretary level – of approaching the Australian Treasury to see if they were interested in doing some joint contigency planning around deposit guarantees, and had been told that the Treasurer had no interest in such guarantees and so our suggestion/offer was declined.

But even Australian authorities could look out the window and see that the global situation was deteriorating rapidly, and by late in the week that recognition was being passed back to authorities on this side of the Tasman. Alan Bollard always kept in close contact with his RBA counterpart Glenn Stevens, and on the Friday my diary records (presumably told by some RBNZ person I was working with) “apparently Glenn S[tevens[ told Alan this afternoon that the RBA/authorities might fairly soon have to consider a blanket guarantee”. In the flurry and uncertainty, one other senior RBNZ person – still holding a senior position there – told me that in his view nothing should be done here unless there were queues outside New Zealand banks.

Between a handful of people on the two sides of the street, we got a paper on deposit guarantee scheme possibilities out to the Minister of Finance on the Friday afternoon. It was a mad rush, with some uneasy negotiated compromises (and everyone’s particular hobbyhorse concern got its own mention). I was probably too close to it to tell, and noted I wasn’t that comfortable with it, but when I got Alan Bollard’s signature he indicated he was happy with it. I noted “lots of small details to sort out next week – we hope only that, not implementation”. To this point, we were focused mostly on retail deposits, but I see in my diary that in The Australian on the Saturday there was talk from bank CEOs of a possible need for a wholesale guarantee scheme.

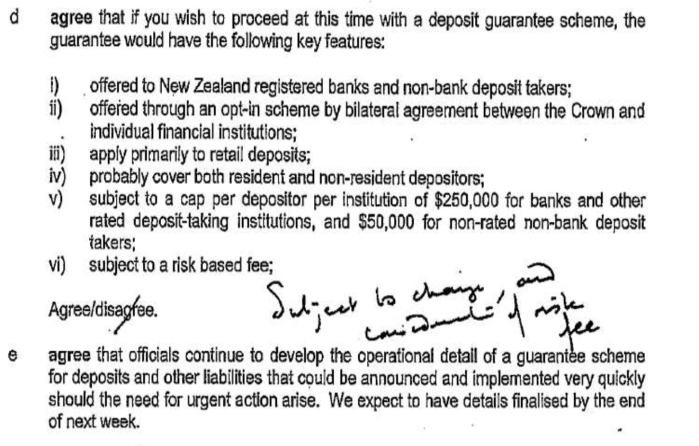

The full, unredacted, paper we wrote is available on The Treasury’s website. The thrust of the advice was that (a) action was not necessary immediately, but (b) that should conditions worsen a scheme could be put in place at quite short notice. The rest of the paper outlined the relevant issues, and the recommended features of any such scheme, and we advised against announcing a scheme until the remaining operational details had been sorted out, something we suggested could be done in the folllowing week.

These were the key features we suggested, largely accepted by the Minister.

One thing that puzzles me looking back now is why we were focused on guarantee options, rather than lender of last resort options. The latter would have involved lending on acceptable collateral to institutions that we judged to be solvent, perhaps at a penal rate. It was the classic response to the idea of a contagious run – troubles elsewhere in the financial system spark concerns about other institutions, and people “run” – cashing in deposits, retail or wholesale – just in case. A sound institution could, in principle, be brought down very quickly by such a run (empirically there are few such examples – most actual runs end up being on institutions that prove to be at-best borderline solvent).

In the paper we sent to the Minister on 10 October we don’t seem to address that option at all. I presume the reason we didn’t was twofold. First, guarantees were beginning to proliferate globally. And second, there probably is a pretty strong argument that if (a) you are convinced your banking system is sound, and (b) there are nonetheless doubts in the wider environment (in this case, a full scale global crisis, and a domestic recession), a guarantee is likely to be considerably more effective in underpinning confidence. Not so much depositor confidence, as the confidence of bankers (and their boards). Even if lender of last resort funding, on decent collateral, had been available without question, few bankers would have been happy to rely on that, and many would have been very keen to cut exposures, pull in loans, and reduce their dependence on the good nature of the Reserve Bank Governor. A guarantee – where the Crown’s money is at stake – is a much stronger signal than a loan secured on the institution’s very best assets. On the other hand, as the paper does note, once given a guarantee may not leave one with much leverage over the guaranteed institution.

Almost all of the subsequent controversy around the deposit guarantee scheme related in one form or another to one key choice.

All the systemically significant financial institutions in New Zealand were banks (not that all banks were systemically significant). But they were not, by any means, the only deposit-taking institutions, and we were in the midst at the time of a finance company in which many companies were proving to be insolvent and failing. Other finance companies appeared – not just to the Reserve Bank, but to the market, and to ratings agencies – just fine.

Treasury and the Reserve Bank jointly recommended to the Minister that any deposit guarantee scheme include finance companies. Why did we do that?

The simple reason was one of both fairness and efficiency. Had we proposed to offer a guarantee only to banks (let alone only the big banks) then in a climate of uncertainty and heightened risk, there would have been an extremely high risk that such an action would have been a near-immediate death sentence for the other deposit-taking institutions, including ones with investment grade ratings, and in full compliance with their trust deeds. We knew that finance companies (while small in aggregate) were riskier than our banks, but that was no good reason to recommend to the government a model that would have killed off apparently viable private businesses. It still seeems, with the information we had at the time, an unimpeachable argument. Classic lender of last resort models, for example, don’t differentiate by the size of the borrowing institution.

We weren’t naive about the risks – including that there was still no prudential supervision of finance companies and the like – and we explicitly recommended that risk-based fees (tied to ratings) be adopted, and the maximum coverage per depositor be much lower for unrated entities. We included in the table an indicative fee scale, based credit default swap pricing for AA-rated banks in normal times, scaling up (quite dramatically) based on the much higher default probabilities of lower-rated entities.

We even included a indicative, totally back of the envelope, guess as to potential fiscal losses – drawing on the experience of the US S&L crisis. As it happens, actual losses were to be less than that number, even though the scheme as adopted by the Minister of Finance was less good than the one we recommended. (Treasury provided some other – but lower – loss estimates a few days after the actual announcement, but I can’t see those on the Treasury website and can’t now recall the approximate numbers.)

But all that was just warm up. We’d been under the impression that the Prime Minister was going to announce, in her campaign launch speech, that preparatory work was underway on a deposit guarantee scheme. That was probably her intention. But that didn’t allow for the Rudd effect. The Australian Prime Minister decided that he was going to announce an actual retail guarantee scheme for Australia that day – the Sunday. And so it was concluded that New Zealand had little choice but to follow suit. As a matter of economics, there probably was little real choice but to follow the Australian lead. But the timing was all about politics. Neither economic nor financial stability would have been jeopardised if we hadn’t had a deposit guarantee scheme announced before the banks opened on Monday morning. We’d have been much better to have taken a bit more time and hashed out some of the details with the Minister in his office in Wellington, not at campaign launches and then, as the day went on, airport lounges (at one point late that afternoon I – who’d talked to the Minister perhaps twice in my life previously – was deputed to ring Dr Cullen and get his approval or some detail or other of the scheme). But I guess it might have left open a brief window in which critics might have suggested that New Zealand politicians were doing less for their citizens and their economy than their Australian counterparts.

The main, and important, area in which Dr Cullen departed from official advice was around the matter of fees. We’d recommended that the risk-based fees would apply from the first dollar of covered deposits (as in any other sort of insurance). The Minister’s approach was transparently political – he was happy to charge fees to big Australian banks (who represented the lowest risks) but not to New Zealand institutions (including Kiwibank). And so an arbitrary line was drawn that fees would be charged only on deposits in excess of $5 billion. Apart from any other considerations, that gave up a lot of the potential revenue that would have partly offset expected losses. The initial decision was insane, and a few days later we got him to agree to a regime where really lowly-rated (or unrated) institutions would have to pay a (too low) fee on any material increases in their deposits. A few days later again an attenuated pricing schedule was applied to deposit-growth in all covered entities. But the seeds of the subsequent problems were sown in that initial set of decisions.

The weeks after the initial announcement were intense. We rushed to get appropriate deed documents drawn up, dealt with endless request from institutional vehicles not covered who sought inclusion (property trust, money market funds etc), and set up a monitoring regime. In parallel, we quickly realised that the way wholesale funding markets were freezing up suggested that a wholesale guarantee scheme was appropriate, and got something announced in a matter of weeks – a much more tightly-designed, better priced scheme, operating only on new borrowing (but I’m biased as that scheme was mostly my baby). As it happens, that scheme provided the leverage to actually get the big banks into the deposit guarantee scheme. Once the government had announced the retail scheme the big banks had little incentive to get in – they probably thought of themselves (no doubt rightly) as sound and as too big to fail – and the scheme was an opt-in one (we couldn’t just by decree compel banks to pay large fees). But the Minister of Finance – probably reasonably enough – insisted that if banks wanted a wholesale scheme (which they really did) it would be a condition that they first sign up to (and pay for) the retail scheme. Perhaps less defensible was the Minister’s insistence that any bank signing up to the guarantee scheme indicate that it would avoid mortgagee sales of home owners in negative equity but still servicing their debt (the ability of banks to do so is a standard provision of mortgage documentation).

After the first few weeks of the retail scheme I had only relatively limited ongoing involvement, and so I’m not going to get into litigating or relitigating the South Canterbury Finance failure, and whether – even the constraints the Minister put on – and how that could by then have been avoided (the Auditor-General report some years ago looked at some of those issues). The outcome was highly unfortunate, and expensive. Nonetheless, it is worth remembering that the total cost of all the guarantee schemes – retail and wholesale – was considerably less than officials had warned was possible. And it is simply not possible to know the counterfactual – how things might have unfolded here had either no guarantees been offered, or if the finance companies and building societies had been excluded from day one. Personally, I think neither would have provided politically tenable, but we’ll never know that, or how that alternative world played out.

But with the information we had at the time – including, for example, the investment grade credit rating for SCF (which had outstanding wholesale debt issues abroad – and actually my only meeting with SCF was about their interest, eventually not pursued, to try to use the wholesale guarantee scheme) – the recommendation made on 10 October seem more or less right. Given the same information I’m not sure I’d advise something different now. And once Australia had made the decision to guarantee retail deposits, there was little effective economic or political choice for New Zealand. Had they not done so – and there was real data, regarding increasing demand for physical cash in Australia, supporting Rudd’s action (rushed as timing was) – perhaps we could have got away with a well-designed wholesale guarantee only. That would have been a first-best preferable world, but it wasn’t the set of facts we actually had to work with.

Funny comment that about lines outside in the street. Yes that’s how bank runs used to operate in our grandparents day but make no mistake there were severe runs on banks – leading ultimately to their collapse – in the wholesale market. Any bank with wholesale market funding requirements, which means nearly all Western banks, faced the difficulty of obtaining term funding (which essentially ceased to exist regardless of the spread offered over LIBOR) and all banks need overnight funding either time to time or on a continuous basis and this too dried up and was only available at userous rates. Any bank seem to go to the Bank Window had their CDS punished.

What does this experience tell me?

Regardless of what market purists might say, there will always be a deposit guarantee in the system, either explicitly set up and appropriately funded by the banks themselves, or implicit and thrown over the banks by frightened politicians in time of crisis.

Rather than have an implicit bank deposit guarantee system thrown together at the last minute on a Sunday morning we would be far better to have a formal, funded system.

LikeLike

In respect of deposits, I entirely agree, and have argued that case previously here, My impression is that that change is coming.

Having said that, I think the wholesale funding situation is different and I don’t know what the complete answer is there. In cases like the NZ/Aus banks in 08/09, where there was no serious doubt at all about solvency, I have no problem with instruments like the wholesale guarantee (at the margin) and significant liquidity support. Where there is doubt about solvency, I want wholesale creditors to lose. OBR is supposed to help make that credible, altho I’d argue that without an established retail deposit insurance model it will never be credible. While Aus has a TBTF approach, it may not be politically credible to allow any NZ creditor to lose and the NZ subs to enter statutory mgmt.

LikeLiked by 1 person

Not too sure what you mean by wholesale creditors because $170 billion in local savings deposits by ordinary mum and dad creditors are also creditors. The rest of it would be bond investors around $60 billion that would be made up mainly by overseas mum and dad savers. Then of course there are the preferential stock holders and the secured bond holders that will have first recourse on the banks assets ie performing loans by borrowers. So the only losers would have to be mum and dad saving depositors whether local or overseas.

LikeLike

Our political process doesn’t, and shouldn’t, care much about the foreign “Mums and Dads” whose savings are intermediated to the NZ banking system via sophisticated managers. What we cared about was the confidence of the NZ banks in continuing to be able to tap those savings. Thus, we introduced a wholesale guarantee scheme – details are one of the links in my comments – focused on new issues. Existing outstanding wholesale debt was never guaranteed – there was no political or economic need to do so.

LikeLike

I was hoping never to see the name SCF cross my line of sight ever again

Post the GFC and the Deposit Guarantee and the Court Case against the directors is leaves a sour taste that will never go away. How you could make the decisions you did given the “information available at the time” is comical

Knowing you were going to re-visit the Guarantee I looked up the Wikipedia entry on SCF and find that there were unknown entities coming out of the woodwork years later that the auditors knew nothing about and the tame auditor of the time was fined $35000 and barred from doing audit work again. Old-boys-network.

I always felt SCF was included in the guarantee scheme because someone powerful further up the line was protecting “him”

LikeLike

“How you could make the decisions you did given the “information available at the time” is comical.”

Easy to say, but what specifically would you have pointed to – in information that was, or could have been, available to ministers/officials – to have excluded an investment-grade rated finance company, in full compliance with its trust deed?

It is a genuine question. And it is no answer to say that the regulatory regime should have been different than it was so that some official supervisor might have uncovered the problems

LikeLike

“How you could make the decisions you did given the “information available at the time” is comical”.

Fine, but that is easy to say. What specific bits of information – individually and collectively – that officials and ministers could reasonably have known in Oct 08 would you point to as grounds for us to have excluded an investment-grade rated finance company, whose rating had been reaffirmed only quite recently, and which was in full compliance with its trust deed?

Genuine question……

LikeLike

I am not questioning your decision

Perhaps you have mis-understood and/or I have been unclear. What was in hindsight comical was the information available in the public domain – and how SCF was considered (at that date) “investment grade” is comical. Obviously the Auditors were at war with SCF but kept it hidden, finally revealing it to the Securities Commission

Simply SCF were not keeping proper accounting records as they are obligated to under Company regulations

As stated above, even the (small-town) auditors were oblivious of assets and entities that crawled out of the woodwork at late as 2014. It would appear SCF were less than forthcoming with the Auditors who were obviously seriously hindered in producing Consolidated Accounts. What was published and produced was patently false

Letters from local Timaru Accountants Woodnorth Meyers to Securities Commission in April 2009 obviously referring to matters relating to the 2008 published accounts

Securities Commission NZ December 2009

… a number of seríous concerns relating to both specific accounting issues as well as broader issues around corporate governance and record keeping. …. Concerns for the Commission about the reliability of the information disclosed by SCF.

In light of the matters raised by the auditors, please provide your comnents as to whether you are satisfied with the quality of the information that is being provided to you by SCF

https://www.rbnz.govt.nz/-/media/ReserveBank/Files/OIAs/scf/4217250.pdf?la=en

LikeLiked by 1 person

Ok, sorry to have misunderstood your point.

LikeLike

Michael

Im reading Adam Tooze’s book Crashed at present and it includes a very good description of the “remediation” cascade … US bail outs…Irish guarantee… German guarantee… English guarantee… etc etc.

Unless you have very very tough guys like Geithner and Poulson running the show it has great potential to descend into a mess. Australia may have left NZ in the lurch, but no more than the Germans did the French.

NZ’s regulator/politician scramble was to be expected. I feel the real problem emerged later when the contingent liability in respect of SCF was very poorly managed.

A feature of the NZ approach, which is apparent from your recollection (and Bollard’s in his book), is the poor engagement with the big banks. The US scheme was executed with lots of bankers in the room. It seems to be a feature of NZ officials and politicians (especially Labour Party ones) is that they prefer to keep the practitioners and experts at arms length.

On a totally different point, I have a question. You note a “wholesale guarantee scheme”. What was that?

In NZ most larger companies do most of their borrowing via securities issuance (notes and bonds). My recollection of the GFC period is that RBNZ was hopeless in managing liquidity in these markets. As it happens NZ corporate bond issuance was incredibly resilient (because it is orientated towards retail investors and because no one thought Contact or Fonterra would go bust … even if banks were at risk), but the note market was closed for a long period.

I recall no help at all from RBNZ. They seemed oblivious (and still do) to the local debt capital markets, which are a darn size bigger than SCF. Apparently circa $100B now (Im told by BNZ).

Tim

LikeLike

Tim

Yes, that cavalcade of interventions is one thing Tooze does well (mostly I thought the book was quite disappointing – a bit of a leftist tirade, with reliance solely on secondary sources. He should probably stick to history from primary sources (where he is excellent).

On the practitioners point, and your contrast between NZ and the US, I’m not sure that is a fair characterisation. My read of all the US books is that typically the bankers were in the room either when the officials/politicians wanted something (eg the Lehmans weekend, where their presence came to nothing) or were going to force bankers to do something (the ambush recap where even sound banks were forced to take more – subsidised – capital).

Re the wholesale guarantee scheme, here is the key link https://treasury.govt.nz/publications/information-release/wholesale-funding-guarantee-facility-guarantees (start from the bottom). It was a scheme – similar to those in various countries – designed to allow banks to issue into the wholesale term funding markets with (priced) guarantees on those specific issue.

Re the NZ corporate bond market, yes I recall sitting in the office of the CEO of one banking operating here (prob around Dec 08) and being told ‘the only corporate bond market in the world still open is NZ’ – and, as you say, that retail orientation was very important to that. (There was, however, a lot of worry behind the scenes about Fonterra’s potential situation – redemption risk was still a big issue back then.)

Some of the details are hazy now, but I think the RB did move to take a much wider range of collateral during the crisis period (arguably too wide in some cases).

On the $100bn, I presume that number includes mainly the banks’ own debt issues and some offshore NZD issuance. Actual NZ corporate issuance – while not trivial at all (and historically bigger, as % of GDP, than in Aus) – isn’t that large. You are right it has rarely been an RB focus – Adrian may be a bit different – but then what would suggest for any enhancement to that role?

LikeLike

“As a matter of economics, there probably was little real choice but to follow the Australian lead. ”

Can you elaborate on this a bit Michael? We did not follow the Irish lead, so why follow the Australian lead on retail? (As I recall, the 10 October paper did not rebut the fallacy that money would flood out of NZ and into Australia if NZ did not follow suit. Under a freely floating exchange rate net capital flows must equal the current account balance in the balance of payments, which was not going to change overnight,)

LikeLiked by 1 person

Bryce

Had there been a move by NZ retail to shift to Aus (and there was no certainty any such shifted deposits would have been covered by the Aus guarantee), we’d have seen a significant fall in the exchange rate. Total bank liabilities wouldn’t have changed, but the funding structure would – from retail to very short-term wholesale – at a time when market and rating agencies were turning very sour on wholesale and demanding much more retail. The NZ subs would have had even more difficulty in foreign wholesale markets than rthey already had (in a climate of extreme uncertainty, the signalling around retail trying to get out of NZ would have been terrible). You’d have seen banks pulling in their horns much more aggressively, and business confidence falling more sharply (and the APS222 limits were binding for some banks, so it isn’t even as if the parents could have provided more term support).

You are probably right that we didn’t make the floating exch rate point in the 10 Oct paper, but that was probably for two reasons: first, the paper wasn’t mainly in the context of an “Aus moved, so what do we do” choice, and second (to the extent i was a partial author) perhaps a “too obvious to need to be stated” sense. Thru the entire crisis period the risk was never that the NZ banking system would literally run out of money, but terms, sources, and forms of funding – and confidence in those arrangements continuing – mattered a lot.

LikeLiked by 1 person

VV Chari wrote a nice paper on the myth of credit drying up https://www.minneapolisfed.org/research/working-papers/facts-and-myths-about-the-financial-crisis-of-2008

LikeLike

Yes, I recall that note now. I thought this quote from the conclusion was relevant:

“Our main point is that policymakers have not done the hard work of convincing the

public or even academic economists of the precise nature of the market failure they see,

of presenting hard evidence, not speculation, that di⁄erentiates their view of the data from

other views, and the logic by which the particular intervention they are advocating will x

this market failure4. We feel that a trillion dollar intervention warrants a bit more serious

analysis than we have seen.”

It is one of the unfortunate aspects of NZ – such thin policy debate, ex post policy review, weak academics – that we haven’t seen rigorous independent review and analysis of past financial crises, and crisis interventions. It lessens the chances of learning correctly the lessons.

LikeLike

Jim ,I happen to know the largest bank in OZ at the time even with a government guarantee could get any money outside Australia. No myth at all.

LikeLike

There was a superb essay in Vanity Fair on the folly of the Irish bondholders guarantee including a willingness to accept 50 cents on the dollar the day before.

https://utopiayouarestandinginit.com/2018/03/07/the-gfc-did-not-bring-down-the-celtic-tiger-the-irish-government-did-by-overreacting-in-a-crisis/

LikeLike

Yes, altho in time the ECB (and entire EU system) became a much bigger obstacle to doing what really should have been done.

LikeLike

On the notion of New Zealand retail deposits going to Australia, I put in an OIA to check if they looked into what type of identification and money-laundering hurdles New Zealanders might have to pass as they carried their cash with them on the plane to be identified at the bank counter in Australia before they can make any withdrawals. I looked it up and found out you really don’t exist in Australia if you don’t have a Medicare card when it comes to getting your hundred points for the anti-money laundering test. New Zealanders don’t have the necessary to Australian identification documents to easily open a bank account in Australia.

It should be remembered that the problem with the bank run is when depositors asked for cash.

Asking for a bank draft in Australian dollars made out of themselves that has 30 days to clear once it is deposited at an Australian retail bank is hardly likely to cause a nz bank firesale of assets causing them to fold. That is the liquidity risk that deposit insuranced stems. Everyone asking for cash, for cash and the bank having to sell part of its portfolio at distressed prices and so much so that the capital ratios are exhausted.

I spent much of alert level 4 last year reading up on bank crises, bank runs and deposit insurance for some work I was doing the Taxpayers Union. We got a nice reply to a letter to the Minister of Finance about his bat crazy plan to offer deposit insurance to the Ponzi scheme prone finance company sector. There can be up to 5 prosecutions every year in New Zealand for Ponzi schemes. Not necessarily in the finance company sector, but it will be if they had Crown deposit insurance.

LikeLike

Michael

Thank you for your reply to me earlier query.

Its easy to get diverted into blind alleyways on something like this:

1. NZ and Australia came through the GFC in good shape because our banks were solvent. The NZ authorities didn’t need to do anything to help the Australian owned banks. There was zero chance ANZ was going to watch its NZ subsidiary get into trouble, ditto the others.

2. The dumb stuff we saw here involved guarantees to insolvent institutions (SCF) and turning a blind eye to the debt capital markets (which surprisingly didn’t matter)

With regards to your “what should they do next time?”. My belief is that central banks should stick to lending large at high rates on good collateral. There is a lame scheme here where bond issuers can pre-qualify bonds for RB funding eligibility. So if you own a Contact Bond you may find you have the capacity in certain situations to use it as collateral against a RB loan. I haven’t read all the details of how it works. I was told that Wellington Airport bonds were not eligible because the Airport has the right to repay its bonds early.

From what I know of the scheme it sounds like a good idea, but poorly implemented.

With regards to BNZ’s estimates of $100B of bond/note issuance, I can only assume that is corporate, bank and NZ$ bonds issued by multinationals. But as the banks have been discouraged from by RB rules providing corporate funding, the bond market will continue to grow in popularity and importance.

Tim

LikeLike

Thanks Tim

I disagree about the Aus banks and their NZ subs. The viability of the Aus banks and the NZ subs wasn’t ever in question, but what was (or could have been) was their continued willingness to extend credit and support borrowers thru a recession (as markets/agencies demanded more secure funding structures). The channels I worry about were partly outlined in my response to Bryce Wilkinson’s comment on this post.

Bear in mind that Aus regulatory restrictions limit the ability of parents to support subs, and this (the APS 222 restriction) was a very real consideration during the 2008/09 crisis. It was a significant element in the move at the time to create the separate ANZ branch structure.

With a proper fee structure and (probably) a cap on the ability of a guaranteed institution to grow its balance sheet more than, say, 5% under guarantee, even the SCF issue would have been much much smaller (for the taxpayer) than it turned out to be.

LikeLiked by 1 person

What I’m missing here is what this insanity has cost the taxpayer. Are we already near $2 billion? interest.co.nz has been tracking that, and last time we were over $1 billion.

I call it an insanity because you don’t have a market, if you can’t have losers. If the government decides that some companies cannot go bankrupt you build the GFC right into the system.

LikeLike

From memory the final net cost was about $1bn, perhaps a bit less (once fees were taken into account, as they need to be). That was unfortunate, altho less than the numbers politicians were warned to expect.

Market discipline is important – and you may recall that the govt stood by while dozens of unguaranteed finance companies failed (and rightly so). But so is macroeconomic stability. The argument for the guarantee scheme is without it we might have lost more output, in a worse recession, than otherwise. No one can conclusively prove that would have been so, but an additional 0.5% loss of GDP would have been around $1bn too, and that loss would have been to society as a whole, and largely irretrievable, while the cost of the bailouts was almost entirely a transfer from one lots of NZers (most of us) to a smaller group (guaranteed depositors).

I’m sure no one involved in the guarantee scheme ever really wanted such a scheme – even those of us who support deposit insurance want proper pricing/funding – but it was an on-balance judgement in the circumstances – backwash to a global event, with few solvency risks in NZ – about least bad/least costly alternatives.

LikeLiked by 1 person

Thank you for that memoir Michael. Very interesting. Cheers

LikeLike

Reblogged this on Utopia, you are standing in it!.

LikeLike