12 October 2008 was a frantic day. It was a Sunday, and I never work Sundays (well, two financial crises, one in Zambia, one in New Zealand, in 30+ years). There was a call in the middle of our church service summoning all hands to the pump, to put in place a retail deposit guarantee scheme that day. We did it. My diary later that night records that we’d “delivered a brand spanking new not very good deposit guarantee scheme”, announced a few hours earlier. It was a joint effort of the Reserve Bank and The Treasury.

I had recently taken up a secondment at The Treasury. I’d been becoming increasingly uneasy about the New Zealand financial situation for some months (flicking through my copy of Alan Bollard’s book on the crisis I found wedged inside a copy of an email exchange he and I had had a month or so earlier about Lender of Last Resort options for sound finance companies, potentially caught up in contagious runs) but I hadn’t had any material involvement in the unfolding sequence of finance company failures. But it was the escalating international financial crisis – this was four weeks after Lehmans, 3.5 weeks after the AIG bailout, two weeks after the US House of Representatives initially voted down TARP, and two weeks after the Irish government surprised everyone by announcing comprehensive deposit guarantees – that really accelerated interest in the question of what, if anything, New Zealand should do, or might eventually be more or less compelled to do. The initiative for some more pro-active planning came from The Treasury, but with some parallel impetus – including around guarantees – from the then Minister of Finance, Michael Cullen (who, a few days out from Labour’s campaign launch, was also looking for pre-election fiscal stimulus measures).

On Tuesday 7 October, there was a long meeting at the Reserve Bank, attended by both the Secretary to the Treasury, John Whitehead, and the Governor of the Reserve Bank. My memory – and my contemporary diary impression – is that the Governor was considerably more focused on the managing the Minister’s political concerns than on any sort of first-best response. But the outcome of that meeting was agreement to quickly work up a joint paper for the Minister which would not, at that stage, recommend introducing a deposit guarantee scheme, but which would outline the relevant issues and operational parameters, giving us something to work from if the situation worsened.

Which it quickly did, both on international markets, and with the political pressure, with the Prime Minister signalling that she wanted to be able to announce something about guarantees in her campaign launch that coming Sunday afternoon.

I and a handful of others on both sides of The Terrace scurried round for the next few days. I see that in my diary I wondered what the best approach was: do nothing, allow some risk of the crisis engulfing us, and then pick up the pieces afterwards, or be more pro-active and take the guarantee route. My conclusion – and even today I wince at the parallel (but this was a late-at-night comment) – “I suspect that if the pressures really come on, the Irish approach is best”. As relevant context, although much of the finance company sector was in solvency trouble (many had already failed) there were no serious concerns about the solvency of the banking system. (Liquidity was, potentially, another issue.)

At Treasury we had recognised the importance of the Australian connection – most of our banks being Australian-owned. I’m not sure of the date, but we had taken the initiative – at Deputy Secretary level – of approaching the Australian Treasury to see if they were interested in doing some joint contigency planning around deposit guarantees, and had been told that the Treasurer had no interest in such guarantees and so our suggestion/offer was declined.

But even Australian authorities could look out the window and see that the global situation was deteriorating rapidly, and by late in the week that recognition was being passed back to authorities on this side of the Tasman. Alan Bollard always kept in close contact with his RBA counterpart Glenn Stevens, and on the Friday my diary records (presumably told by some RBNZ person I was working with) “apparently Glenn S[tevens[ told Alan this afternoon that the RBA/authorities might fairly soon have to consider a blanket guarantee”. In the flurry and uncertainty, one other senior RBNZ person – still holding a senior position there – told me that in his view nothing should be done here unless there were queues outside New Zealand banks.

Between a handful of people on the two sides of the street, we got a paper on deposit guarantee scheme possibilities out to the Minister of Finance on the Friday afternoon. It was a mad rush, with some uneasy negotiated compromises (and everyone’s particular hobbyhorse concern got its own mention). I was probably too close to it to tell, and noted I wasn’t that comfortable with it, but when I got Alan Bollard’s signature he indicated he was happy with it. I noted “lots of small details to sort out next week – we hope only that, not implementation”. To this point, we were focused mostly on retail deposits, but I see in my diary that in The Australian on the Saturday there was talk from bank CEOs of a possible need for a wholesale guarantee scheme.

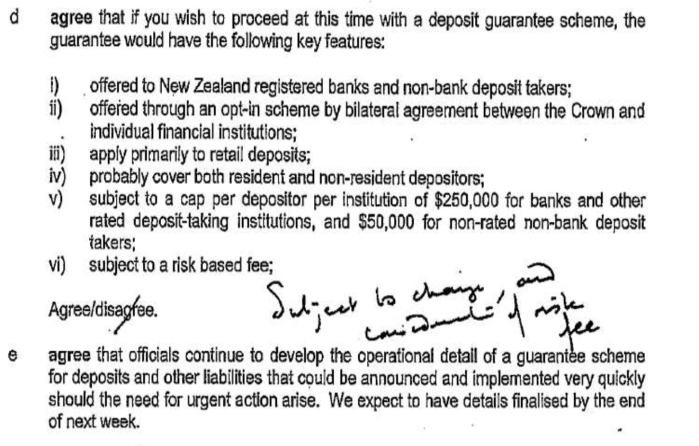

The full, unredacted, paper we wrote is available on The Treasury’s website. The thrust of the advice was that (a) action was not necessary immediately, but (b) that should conditions worsen a scheme could be put in place at quite short notice. The rest of the paper outlined the relevant issues, and the recommended features of any such scheme, and we advised against announcing a scheme until the remaining operational details had been sorted out, something we suggested could be done in the folllowing week.

These were the key features we suggested, largely accepted by the Minister.

One thing that puzzles me looking back now is why we were focused on guarantee options, rather than lender of last resort options. The latter would have involved lending on acceptable collateral to institutions that we judged to be solvent, perhaps at a penal rate. It was the classic response to the idea of a contagious run – troubles elsewhere in the financial system spark concerns about other institutions, and people “run” – cashing in deposits, retail or wholesale – just in case. A sound institution could, in principle, be brought down very quickly by such a run (empirically there are few such examples – most actual runs end up being on institutions that prove to be at-best borderline solvent).

In the paper we sent to the Minister on 10 October we don’t seem to address that option at all. I presume the reason we didn’t was twofold. First, guarantees were beginning to proliferate globally. And second, there probably is a pretty strong argument that if (a) you are convinced your banking system is sound, and (b) there are nonetheless doubts in the wider environment (in this case, a full scale global crisis, and a domestic recession), a guarantee is likely to be considerably more effective in underpinning confidence. Not so much depositor confidence, as the confidence of bankers (and their boards). Even if lender of last resort funding, on decent collateral, had been available without question, few bankers would have been happy to rely on that, and many would have been very keen to cut exposures, pull in loans, and reduce their dependence on the good nature of the Reserve Bank Governor. A guarantee – where the Crown’s money is at stake – is a much stronger signal than a loan secured on the institution’s very best assets. On the other hand, as the paper does note, once given a guarantee may not leave one with much leverage over the guaranteed institution.

Almost all of the subsequent controversy around the deposit guarantee scheme related in one form or another to one key choice.

All the systemically significant financial institutions in New Zealand were banks (not that all banks were systemically significant). But they were not, by any means, the only deposit-taking institutions, and we were in the midst at the time of a finance company in which many companies were proving to be insolvent and failing. Other finance companies appeared – not just to the Reserve Bank, but to the market, and to ratings agencies – just fine.

Treasury and the Reserve Bank jointly recommended to the Minister that any deposit guarantee scheme include finance companies. Why did we do that?

The simple reason was one of both fairness and efficiency. Had we proposed to offer a guarantee only to banks (let alone only the big banks) then in a climate of uncertainty and heightened risk, there would have been an extremely high risk that such an action would have been a near-immediate death sentence for the other deposit-taking institutions, including ones with investment grade ratings, and in full compliance with their trust deeds. We knew that finance companies (while small in aggregate) were riskier than our banks, but that was no good reason to recommend to the government a model that would have killed off apparently viable private businesses. It still seeems, with the information we had at the time, an unimpeachable argument. Classic lender of last resort models, for example, don’t differentiate by the size of the borrowing institution.

We weren’t naive about the risks – including that there was still no prudential supervision of finance companies and the like – and we explicitly recommended that risk-based fees (tied to ratings) be adopted, and the maximum coverage per depositor be much lower for unrated entities. We included in the table an indicative fee scale, based credit default swap pricing for AA-rated banks in normal times, scaling up (quite dramatically) based on the much higher default probabilities of lower-rated entities.

We even included a indicative, totally back of the envelope, guess as to potential fiscal losses – drawing on the experience of the US S&L crisis. As it happens, actual losses were to be less than that number, even though the scheme as adopted by the Minister of Finance was less good than the one we recommended. (Treasury provided some other – but lower – loss estimates a few days after the actual announcement, but I can’t see those on the Treasury website and can’t now recall the approximate numbers.)

But all that was just warm up. We’d been under the impression that the Prime Minister was going to announce, in her campaign launch speech, that preparatory work was underway on a deposit guarantee scheme. That was probably her intention. But that didn’t allow for the Rudd effect. The Australian Prime Minister decided that he was going to announce an actual retail guarantee scheme for Australia that day – the Sunday. And so it was concluded that New Zealand had little choice but to follow suit. As a matter of economics, there probably was little real choice but to follow the Australian lead. But the timing was all about politics. Neither economic nor financial stability would have been jeopardised if we hadn’t had a deposit guarantee scheme announced before the banks opened on Monday morning. We’d have been much better to have taken a bit more time and hashed out some of the details with the Minister in his office in Wellington, not at campaign launches and then, as the day went on, airport lounges (at one point late that afternoon I – who’d talked to the Minister perhaps twice in my life previously – was deputed to ring Dr Cullen and get his approval or some detail or other of the scheme). But I guess it might have left open a brief window in which critics might have suggested that New Zealand politicians were doing less for their citizens and their economy than their Australian counterparts.

The main, and important, area in which Dr Cullen departed from official advice was around the matter of fees. We’d recommended that the risk-based fees would apply from the first dollar of covered deposits (as in any other sort of insurance). The Minister’s approach was transparently political – he was happy to charge fees to big Australian banks (who represented the lowest risks) but not to New Zealand institutions (including Kiwibank). And so an arbitrary line was drawn that fees would be charged only on deposits in excess of $5 billion. Apart from any other considerations, that gave up a lot of the potential revenue that would have partly offset expected losses. The initial decision was insane, and a few days later we got him to agree to a regime where really lowly-rated (or unrated) institutions would have to pay a (too low) fee on any material increases in their deposits. A few days later again an attenuated pricing schedule was applied to deposit-growth in all covered entities. But the seeds of the subsequent problems were sown in that initial set of decisions.

The weeks after the initial announcement were intense. We rushed to get appropriate deed documents drawn up, dealt with endless request from institutional vehicles not covered who sought inclusion (property trust, money market funds etc), and set up a monitoring regime. In parallel, we quickly realised that the way wholesale funding markets were freezing up suggested that a wholesale guarantee scheme was appropriate, and got something announced in a matter of weeks – a much more tightly-designed, better priced scheme, operating only on new borrowing (but I’m biased as that scheme was mostly my baby). As it happens, that scheme provided the leverage to actually get the big banks into the deposit guarantee scheme. Once the government had announced the retail scheme the big banks had little incentive to get in – they probably thought of themselves (no doubt rightly) as sound and as too big to fail – and the scheme was an opt-in one (we couldn’t just by decree compel banks to pay large fees). But the Minister of Finance – probably reasonably enough – insisted that if banks wanted a wholesale scheme (which they really did) it would be a condition that they first sign up to (and pay for) the retail scheme. Perhaps less defensible was the Minister’s insistence that any bank signing up to the guarantee scheme indicate that it would avoid mortgagee sales of home owners in negative equity but still servicing their debt (the ability of banks to do so is a standard provision of mortgage documentation).

After the first few weeks of the retail scheme I had only relatively limited ongoing involvement, and so I’m not going to get into litigating or relitigating the South Canterbury Finance failure, and whether – even the constraints the Minister put on – and how that could by then have been avoided (the Auditor-General report some years ago looked at some of those issues). The outcome was highly unfortunate, and expensive. Nonetheless, it is worth remembering that the total cost of all the guarantee schemes – retail and wholesale – was considerably less than officials had warned was possible. And it is simply not possible to know the counterfactual – how things might have unfolded here had either no guarantees been offered, or if the finance companies and building societies had been excluded from day one. Personally, I think neither would have provided politically tenable, but we’ll never know that, or how that alternative world played out.

But with the information we had at the time – including, for example, the investment grade credit rating for SCF (which had outstanding wholesale debt issues abroad – and actually my only meeting with SCF was about their interest, eventually not pursued, to try to use the wholesale guarantee scheme) – the recommendation made on 10 October seem more or less right. Given the same information I’m not sure I’d advise something different now. And once Australia had made the decision to guarantee retail deposits, there was little effective economic or political choice for New Zealand. Had they not done so – and there was real data, regarding increasing demand for physical cash in Australia, supporting Rudd’s action (rushed as timing was) – perhaps we could have got away with a well-designed wholesale guarantee only. That would have been a first-best preferable world, but it wasn’t the set of facts we actually had to work with.