Three heads of central banks feature in this (perhaps rather bitsy) post.

The first is one of the heroes of modern central banking, Paul Volcker. Now aged 91, and clearly ailing, he has a new (co-authored) book out tomorrow, part memoir and part (apparently) his perspectives on various public policy challenges now facing the US. (His successor Alan Greenspan, now aged 92, also had a new book out a couple of weeks ago. At this rate, Don Brash – a mere stripling at 78 – could be just getting going.)

There are various articles and interviews around (I liked this one with the FT’s Gillian Tett) but what I wanted to write about was an extract from the Volcker book, published last week by Bloomberg (and which a reader drew to my attention), under the heading “What’s wrong with the 2 per cent inflation target”. Volcker was, of course, the person who as head of the Federal Reserve from 1979 to 1987 took the lead role in ensuring that monetary policy was finally run sufficiently tightly, for long enough, to get US inflation enduring down. One can debate how much was the man, and how much was an idea whose time had come, but it was on his watch that the hard choices were made.

This was, of course, before the days of formal inflation targeting. Volcker has never been a supporter, citing approvingly in his article Alan Greenspan’s famous response to a mid -1990s challenge from Janet Yellen.

Yellen asked Greenspan: “How do you define price stability?” He gave what I see as the only sensible answer: “That state in which expected changes in the general price level do not effectively alter business or household decisions.” Yellen persisted: “Could you please put a number on that?”

The Fed finally came to do so, now adopting its own numerical target (2 per cent annual increases in the private consumption deflator.

Volcker takes the opportunity to blame us, writing of his visit to New Zealand in 1988 (when I recall meeting him).

The changes included narrowing the central bank’s focus to a single goal: bringing the inflation rate down to a predetermined target. The new government set an annual inflation rate of zero to 2 percent as the central bank’s key objective. The simplicity of the target was seen as part of its appeal — no excuses, no hedging about, one policy, one instrument. Within a year or so the inflation rate fell to about 2 percent.

The central bank head, Donald Brash, became a kind of traveling salesman. He had a lot of customers. After all, those regression models calculated by staff trained in econometrics have to be fed numbers, not principles.

He is probably a little unfair. Rightly or wrongly, the rest of the world would have got there anyway (eg Canada adopted an independent inflation target very shortly after we did), and in time it was the New Zealand inflation target that was revised up to fall more into line with an international consensus centred on something around 2 per cent. His bigger point is that he doen’t like tight numerical targets: some of his reasons are defensible, but it is also worth recalling the Volcker was in his prime in an age when there was much less transparency and accountability more generally.

But my bigger concern with the article, and argument, is about what comes across as complacency about the risks the US (and many other countries) face when the next serious recession hits. He is opposed to any steps to push inflation up to, or even a bit above, 2 per cent, and he also doesn’t propose doing anything to remove, or even ease, the constraint posed by the near-zero lower bound on nominal interest rates.

Deflation, or even a period when monetary policy is constrained in its ability to bring the economy back to normal levels of utilisation following a serious recession, just doesn’t seem to be a risk that bothers him, provided financial system risks are kept in check.

The lesson, to me, is crystal clear. Deflation is a threat posed by a critical breakdown of the financial system. Slow growth and recurrent recessions without systemic financial disturbances, even the big recessions of 1975 and 1982, have not posed such a risk.

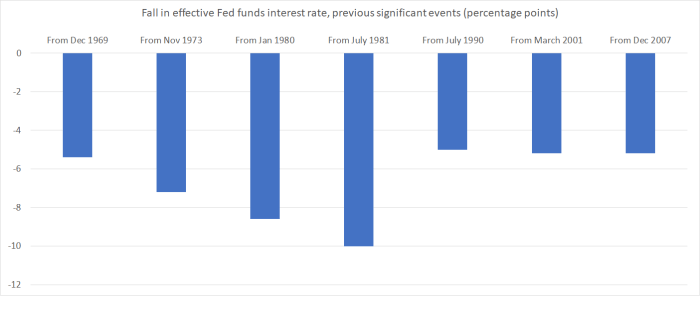

I found that a fairly breathtaking claim. After all, the effective Fed funds interest rate in 1974 had peaked at around 13 per cent, and in 1981 it had peaked at around 19 per cent. There was a huge amount of room for real and nominal interest rates to fall. Right now, the Fed funds target rate is 2.0 to 2.25 per cent.

For most of history the Federal Reserve didn’t announce an interest rate target, but in this chart I’ve shown the change in the actual effective Fed funds rate (as traded) for each of the significant policy easing cycles since the late 1960s.

The median cut was 5.4 percentage points (not inconsistent with the typical scale of interest rate cuts in other countries, including New Zealand, faced with serious downturns). Some of those falls were probably falls in inflation expectations, but even in the last three events – when inflation expectations have been more stable – cuts of 5 percentage points have been observed. (I was going to use the word “required” there, but there seems little doubt that policy rates would have been cut further after 2007 – consistent, for example, with standard Taylor rule prescriptions – if it had not been for the lower bound on nominal rates.)

And what of the current situation? With a Fed funds target rate of about 2 per cent, if a serious recession hit today the Federal Reserve has conventional policy leeway of perhaps 2 percentage points (if they treat 0 to 0.25 per cent as the floor next time as they did last time) or perhaps as much as 2.75-3 percentage points (if they treat the effective floor as more like the -0.75 per cent a couple of European countries have operated with). The Fed has given no public hint that they would actually be prepared to take policy rates negative in the next recession, so for now markets can only guess – and perhaps hope. But either way, the conventional monetary policy leeway is much less than was used in any of the significant US downturns of the previous 50 years. That should be worrying someone like Paul Volcker more than it seems to, especially when three other considerations are taken into acount:

- when markets know those limitations – and firms and households will quickly learn them when the recession comes – inflation expectations are likely to drop away more quickly than usual, because no one will be able to count on the Fed being able to keep inflation near target,

- US fiscal policy has been so badly debauched that there is going to be little (political) leeway for material discretionary fiscal stimulus in the next recession, and

- most other advanced countries have even less conventional monetary policy capacity now than the US does (and even less than usual relative to past history).

Reasonable people can quibble about the place of formal inflation targeting, but there needs to be much more urgency in planning to cope with the next serious recession, whatever its source or precise timing.

As readers know, I was not one of the biggest fans of former Reserve Bank Governor Graeme Wheeler. But in Herald economics columnist Brian Fallow’s article last Friday there was some quotes from a recent speech Wheeler had given in Washington that had me nodding fairly approvingly as I read.

If the advanced economies face a recession in the next few years, much of the burden for stimulus will fall on fiscal policy, Wheeler says. The scope to cut interest rates is limited as policy rates in several countries remain at or near historic lows. Countries accounting for a quarter of global GDP have policy rates at or below 0.5 per cent, whereas policy cuts in recessions have often been of the order of 5 percentage points.

“In such a situation central banks would rely on additional quantitative easing and governments would face considerable pressure to expand their budget deficits through spending increases and/or tax cuts.”

They are words that need more attention even in a New Zealand context, where the OCR is only 1.75 per cent. It was 8.25 per cent going into the last serious downturn.

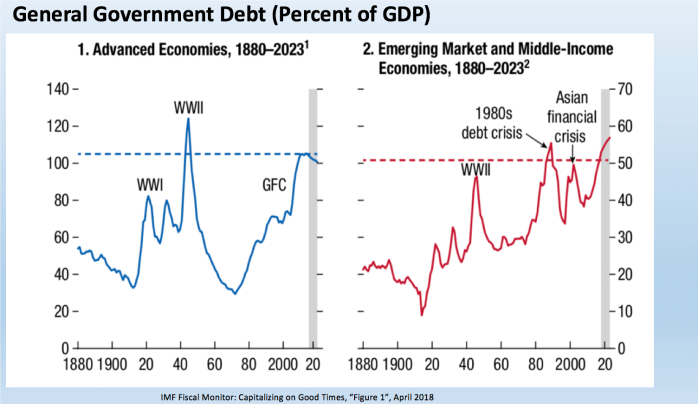

Wheeler’s speech (a copy of which Brian Fallow kindly, and with permission, passed on) – to a conference on sovereign debt management – is mostly about debt management issues. It has a number of interesting charts from various publications, including this sobering one.

Perhaps what interested me was that in his discussion of the issues and risks, Wheeler seemed not to touch at all on the two approaches often used in very heavily indebted countries – even advanced countries – facing serious new stresses: default and/or surprise sustained inflation. To the credit of successive New Zealand governments, fiscal policy here is in pretty good shape, and debt is low, but looking around the world it would perhaps be a surprise if Greece is the only advanced country to default on its sovereign debt (or actively seek to inflate it away) in the first half of this century.

And finally, our own current Governor. He has just brought up seven months in office without a substantive public speech on the main policy areas he has responsibility for; monetary policy and financial stability. It is quite extraordinary. He has been free with his thoughts on climate change, infrastructure financing, tree gods, and so on and so forth, while batting away questions about the next serious recession and its risks in a rather glib, excessively complacent, way (hint: QE and its variants is not – based on international experience – an adequate answer).

Anyway, the Governor has repeatedly told us about his commitment to greater openness and communications. I’ve been a sceptical of that claim – both because every Governor says it in his or her own way, but also because of the track record that is already building. There have been, as I said, no substantive speeches from Orr on his main areas of legal responsibility. Speeches that are published apparently bear little or no relationship to what the Governor actually says to the specific audience. There have been no steps taken to, say, match the RBA in making generally available the answers senior central bankers give in Q&A sessions after speeches, and we heard not long ago of a speech Orr gave to a private organisation, commenting loosely on matters of considerable interest to markets and those monitoring the organisation, but with no external record of what was said.

And it seems that there is likely to be another example today. The next Monetary Policy Statement is due next week, as is the joint FMA-RB statement on bank conduct and culture (FMA responsibility that the Governor has barged into), both surely rather sensitive matters. And yet the Governor is giving a significant speech this evening at the annual meeting of the lobby group Transparency International.

Guest Speaker: Adrian Orr

Adrian’s speech will encourage discussion about the relevance of transparency, accountability and integrity in the New Zealand financial sector.

Adrian Orr will be introduced by State Services Commissioner, Peter Hughes, and thanked by new Justice Secretary, Andrew Kibblewhite.

And yet his speech – to Transparency International, introduced by the State Services Commissioner, thanked by the head of the Prime Minister’s department – on transparency, is to be, well, totally non-transparent. From the Reserve Bank’s page for published speeches

Upcoming speechesThere is nothing scheduled.