Back in June the Minister of Finance (and the coalition government more generally) surprised many/most observers by reappointing, for another two-year term, the chair of the Reserve Bank Board, Neil Quigley. Quigley, you may recall, has been on the Bank’s Board since 2010, has been chair since 2016, and in 2022 (when the new Act and Board structure came into effect) had been appointed for what then seemed like a two-year transitional (ie final) term by then Minister of Finance Grant Robertson.

I wrote about this astonishing (to put it politely) reappointment at the time, and then lodged an Official Information Act request with the Minister of Finance for any and all material relating to Board appointments or non-appointments (there are still vacancies on the Board and to date the Minister appeared to have done nothing about filling them either). Nothing about either the conduct or the policy performance of the Reserve Bank over recent years suggested that simply reappointing the Board chair would make a lot of sense, at least for a government that cared two straws about institutional quality, massive losses to the taxpayer, let alone debacles like the worst outbreak of core inflation in decades (recall the “cost of living crisis” that helped see off the previous government).

It took the Minister a long time to reply, running over her own extended deadline, but the results finally turned up last week. The response didn’t shed much light on the reappointment, but I’ll come back later to what little we did learn. There was, however, some interesting snippets on other aspects of the Minister and the Reserve Bank.

The first was about appointments to the Monetary Policy Committee (there were two new external appointments earlier in the year). I hadn’t asked about MPC appointments, but I guess they must have got caught up in the response because the Board recommends these appointments.

The new appointees – Carl Hansen and Prasanna Gai – represented a step forward (including final confirmation that the absurd Quigley blackball on expertise on the MPC had well and truly gone). They were announced on 28 March, four months into the government’s term. But what the OIA response showed was that the nominations had been delivered to the Minister in a paper dated 15 December 2023, just a couple of weeks after the government took office. It confirmed, what had seemed likely, that the MPC appointees had been selected by the Labour-appointed Board to selection criteria that had been developed much earlier last year, under Labour. My OIA response doesn’t specifically show that Gai and Hansen were those nominated in December, but there is no hint in any of the papers that the Minister of Finance pushed back at all on those nominations, or did anything about seeking to reconfigure the way the MPC works to encourage more openness and accountability. Instead, the pre-election nominations simply worked their way slowly through the system, and were finally announced just before the first appointee needed to take office. Neither appointee was, on the face of it, bad (although we have yet to see any evidence that either has made a positive difference), but the process revealed a Minister who wasn’t very interested and just went along.

The other unrelated aspect that the OIA revealed something about was the government’s approach to Reserve Bank spending. I’ve previously noted my surprise that there had been nothing in the 2024 Letter of Expectation from the Minister to the Board calling for expenditure savings or strongly stating that the next five-yearly funding agreement (from 1 July 2025) would do something about the bloat that had grown up under Orr/Quigley/Robertson.

But it turns out that there were actually two letters of expectation, only one of which has been disclosed pro-actively.

The mention of a “savings target” for next year and beyond of 7.5 per cent is, I guess, a start, and better than nothing from the Minister, although seems rather light given the huge increase in spending and staff numbers the Bank has undertaken over the last few years, including (for example) the 27 comms staff.

But then there is no sign at all of anything pro-active in the Reserve Bank’s response, or even in the Minister’s follow-up. The contrast with ACC is stark. It also isn’t directly Budget funded so also wasn’t included in this year’s fiscal savings targets but this was the CEO in February

Seemed like the approach of a responsible CEO and Board.

But very different from the Orr/Quigley approach. As they are required to by law, the Reserve Bank at the end of June released its Statement of Intent and Statement of Performance Expectations. The draft Statement of Intent has to have been provided to the Minister early, the Minister can provide comments, and the Bank must consider those comments. But there is little or no substantive mention in either the Statement of Intent or the Statement of Performance Expectations of the forthcoming new funding agreement, nothing at all about cuts, savings targets or anything of the sort. And, you may remember that for 24/25 the Board had approved budgets with a further 21 per cent increase in staff expenses.

Doesn’t quite seem to compute, against the reported talk of a 7.5 per cent savings target from next year.

(One person I discussed this with suggested – flippantly I think – that perhaps the 21 per cent increase included big redundancy costs, but I think we can discount that rather charitable interpretation.)

Where was the Minister of Finance in all this? Why, she was finalising the further reappointment of the Board chair. It seems to speak to an extraordinary degree of indifference.

What do we learn from the OIA about that reappointment. To be honest, not a great deal. We do learn that the Opposition political parties (who she was required by law to consult) raised no objection (but then Robertson had appointed Quigley in the first place and run defence for the Bank over recent years, backing the Board’s recommendation to reappoint Orr).

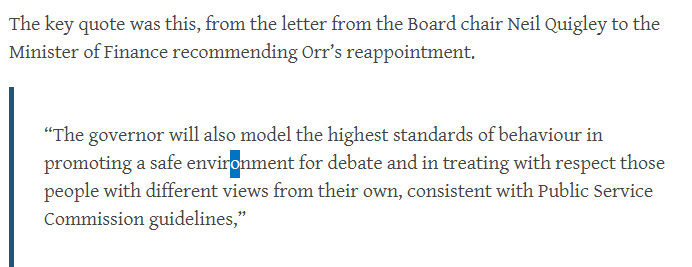

But there was also this line in the talking points provided by The Treasury to the Minister of Finance to accompany the reappointment paper she was taking to Cabinet’s Appointments and Honours Committee in early May (this sentence was the only content on reasons for the proposed reappointment).

It was pretty staggering stuff really. A Governor whose personal conduct leaves a great deal to be desired, who repeatedly misleads (or worse) FEC, treats MPs (including Willis when she was in Opposition) with disdain, and who had presided over the worst monetary policy failures in decades, with not a word of contrition or straightforward reflection and ex post analysis……and what is supposed to commend the Board chair (himself with a fairly shady record, misleading Treasury) is that he works well with the Governor. Just astonishing. Now, to be sure, one would not want a Board chair who was perpetually unnecessarily at odds with the Governor, but one of the prime jobs of the Board and its chair is to hold the Governor and MPC to account, and – in the wake of failures of recent years – you might hope that things between the Board and Governor were actually a bit tense, with pressure on the Governor to markedly lift his game. (Cabinet in early May wasn’t to know that they were just about to be treated to another example of MPC/Governor very poor performance, with the baffling MPS in May, the quick U-turn, and then the attempt by the Governor to suggest that anyone suggesting there’d been a U-turn shouldn’t be taken seriously.)

It is always easier to reflect on what is in documents (and OIA releases) than what isn’t there. But reflecting on this bundle of documents, what is striking is that there is no written advice at all from The Treasury to the Minister on the performance of the Board or the Board chair (and my request specifically encompassed such advice). Part of the overhaul of the Reserve Bank Act was to give Treasury a clearer and more explicit (and better-funded) role in monitoring the Bank and its Board. And yet……there was just nothing when it came to the decision whether or not to reappoint the incumbent, who’d presided through the years of woe (and whose Board Annual Reports, supposedly providing accountability, never expressed any concerns whatever). Whether this was Treasury falling down on the job (quite badly) or just keeping quiet because the new Minister had been clear from the start that she was reappointing Quigley anyway is impossible to tell from this set of documents. Even if it was the latter, you might have hoped that a fearless Treasury, serious about its new monitoring role, would have recorded some advice anyway. But apparently not.

When Willis announced the reappointment of Quigley, her statement included this line

You were left wondering why a new Minister of Finance wouldn’t have just got on and made appointments when she could (she’d already been Minister of six months then, and pretty everyone outside thought the current Reserve Bank Board was seriously underqualified).

On 29 May, Treasury provided some advice to the Minister about future Board appointments, notably a “late 2024 appointment round” that they were proposing. Much of it is fairly sensible stuff, and they clearly had in mind the eventual replacement of Quigley proposing to find a new member “with specialist domain knowledge and the potential to succeed Professor Quigley as chair”, and noting later again the need for a succession plan for Quigley’s position as chair.

The paper has a timetable, that envisaged getting onto things pretty promptly, with nominations/applications to fill the various vacancies to close on 24 June, appointments to be formally made late last month, with the appointees taking up their new positions on 9 September. Which would have been all well and good, but…..there is no sign (either in the release, or in anything seen in public since) that the Minister accepted this advice or that anything has anything has yet happened.

And so we are just left with not much further insight, but perhaps a confirmation that the Minister of Finance really didn’t care much. Which really shouldn’t be good enough, in an institution (management, Board, and MPC) that has done so poorly in recent years on so many dimensions.

I don’t usually find cynical explanations that convincing, so I’ve been reluctant to take very seriously the line that Quigley was reappointed because he was in league with National Party figures (be it Steven Joyce, the very expensive lobbyist Quigley had hired, or Shane Reti and the promise of “a present” for a second term in government that a new medical school would be). If I had a cynical explanation of my own it might be along the lines that National really had no reason to be concerned about all those Reserve Bank failures because, after all, the dreadful inflation outcomes helped them win the election. What wasn’t to like? But I don’t really believe that is the answer either.

And so I fall back on the idea that Willis just doesn’t care very much. There might be no political price to pay for making a start on sorting out the Reserve Bank, but there probably is no price to pay among the general public for doing nothing about it all. So, if you really are mostly just a political operative, why bother? Who cares? That should be a fairly damning indictment of the individuals involved, and of the system, but it is hard to think of a better story. (Lines about needs for succession planning ring pretty hollow: plenty of Crown entity chairs have been replaced in short order, and it is hardly as if anyone outside the Bank seems to think the Orr/Quigley Bank had been doing a good or professional job.)

I’m not going to repeat all the text I wrote when the Quigley reappointment was first announced, but I’ll end with just a few sentences from that post

Even among those with low expectations of the current Minister of Finance, it was pretty astonishing news. It isn’t really possible to get rid of the Governor – unless he had been inclined to do the honourable thing, including accepting responsibility for the macro mess, and resign – but the Board chair’s term expired just six months after the new government took office. Of the three parties in the government, the two who had been in Parliament last term – ACT and National – had both objected to Orr’s reappointment when, as his new law required, Grant Robertson had consulted them. And it was the Board, led by Quigley, that was responsible for choosing to recommend Orr.

Just astonishing. But remember that “excellent working relationship” he has with Orr…..

PS Not that is a particular concern of mine, but I noticed in the documents that Quigley is getting paid $2300 a day for his Reserve Bank role. Last year’s Annual Report showed that he received $170127, or about 74 days at that approved daily rate. That seems like a large chunk of time for someone with a fulltime chief executive role, as a university Vice-Chancellor, to be able to devote to an outside Board position