Paul Krugman had a piece on his blog a day or two ago making the case for increased (“much more”) public investment spending in the US.

There are three strands to his case.

The first is a proposition that the US is still “in or near” a liquidity trap. I’m not sure I’d use the term, but the general point is one I sympathise with. Under current legislation and central bank practices (easy convertibility into banknotes on demand), few countries are very far from the effective lower bound on nominal interest rates. And if a new downturn comes, that could make it very difficult for central banks to do much to help stabilize economies. To me, that argues for action (legislative and administrative) to remove (or greatly ease) the lower bound constraint.

The second is a proposition that the last few years of disappointing real economic growth are helping to bring about a sustained reduction in future potential growth – in his words,

demand-side weakness now breeds supply-side weakness later, so that there are big payoffs to boosting the economy through public spending

In principle, it might be a plausible idea. But there is no real evidence that things turned out that way during the Great Depression when, extremely weak as demand was, TFP growth remained strong.

The third – actually first in Krugman’s list – is that public spending as a share of GDP is now very low:

Government borrowing costs are at record lows; markets are in effect pleading with the government to borrow and spend. So why not do it? It’s completely crazy that public construction as a percentage of GDP has declined to record lows even as interest rates have done the same

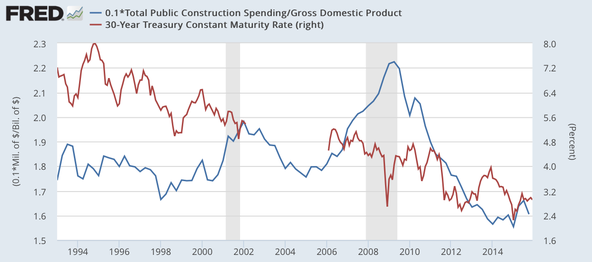

And he includes this chart

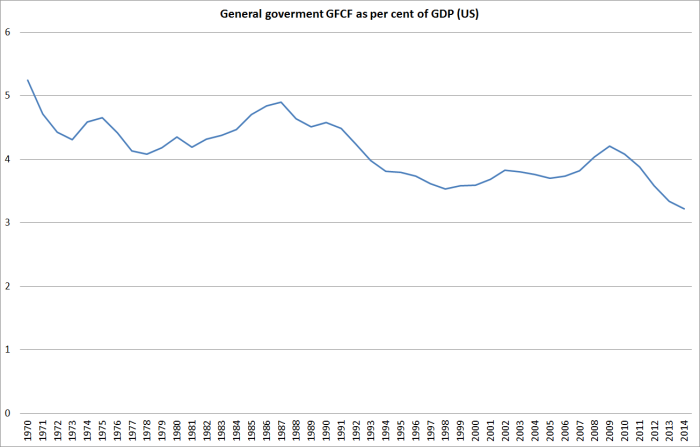

That chart only goes back to the early 1990s. But here, for the US, is general government gross fixed capital formation as a per cent of GDP since 1970.

It is at a record low, which might seem to support Krugman’s case.

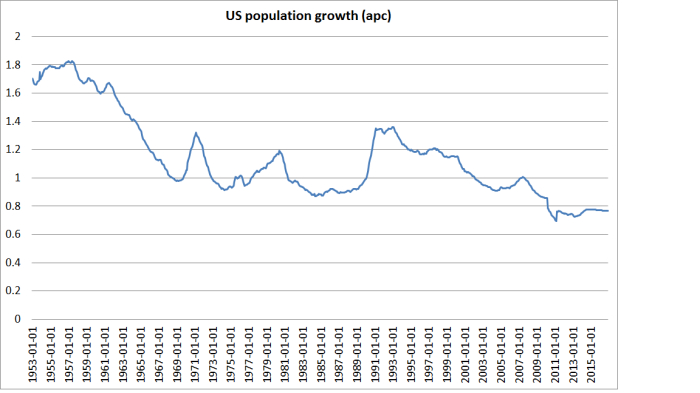

But then here is the annual rate of growth in the US population, in this case going back as far as the FRED series went, to 1953. And what do we find, but that population growth is also estimated to be at its lowest for decades – quite possibly in the entire history of the US.

If the population growth rate slows, less investment (as a share of each year’s GDP) is needed to maintain a desired stock of capital per person. That is a good thing, on the whole – available resources can be used for other stuff. These effects are quite large. Much of the government capital stock is in the form of quite long-lived assets, which depreciate slowly (schools, hospitals, roads etc). Depreciation is one – quite substantial – component of the gross fixed capital formation spending, but a large share of government capital spending is about supporting the needs of a growing population.

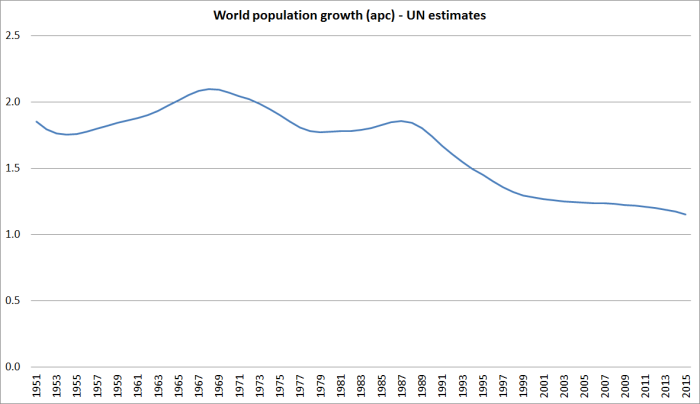

It isn’t just the US population growth rate that is slowing – global population growth rates have been slowing markedly too.

A lower rate of population growth, and associated lower need for investment, is now pretty widely recognized as one of the factors that has been driving real interest rates down around the world. One could argue, with Krugman, that markets are “begging governments to borrow and spend”, but it might be better to interpret is as markets as reflecting the twin declines, in population growth and in underlying multi-factor productivity growth. There simply aren’t as many attractive projects around as there were. It can take time for (desired) savings rates to adjust to that deterioration in investment prospects – and that is usually where monetary policy has a part to play. More government capital expenditure, if the remunerative projects aren’t there, doesn’t look like a particularly attractive way to boost the country’s longer-term economic fortunes. And as the US government is still running deficits, cuts in government savings don’t look particularly sensible either.

Perhaps the US is different, and the high-returning public projects (covering not just the low cost of debt but the overall cost of citizens’ equity) are there and able to be implemented effectively in a way that achieves those returns. But the political process is such that even if, in principle, a large pool of such projects are there, there is no guarantee that those would be the projects that would be picked.

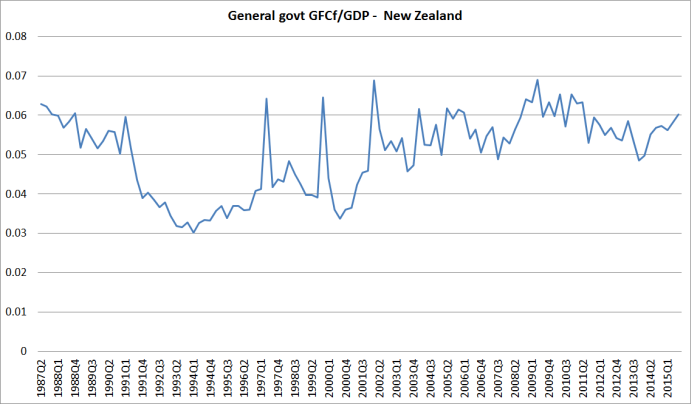

What of New Zealand? Here is the chart of general government gross fixed capital formation as a per cent of GDP back to 1987.

It hasn’t fallen, but then again our population growth – while volatile – has recently been higher than at any time since the 1970s. There is an awful lot of wasteful public capital spending here, that fails to pass reasonable economic tests – Transmission Gully, the Auckland rail projects, the Dunedin stadium, and the fearful prospect of large amounts of ratepayer money extending Wellington Airport’s runway – and we should be wary of the siren calls, even here, to increase government capital expenditure as a way of stimulating the overall economy. Poor quality projects make us poorer.

Are there exceptions – cases where demand might be so weak that perhaps even poor quality projects might help kickstart the economy (Keynes’s example of paying people to dig holes and fill them in again). I’m not sufficiently doctrinaire as to say “never”, but equally it is difficult to think of any actual historical episodes where “sorting out monetary policy”, and complementing that with growth-oriented structural reforms, would not have been a better option. It was in the Great Depression. It would have been in 1990s Japan. It looks that way in most of the world, including New Zealand, now.