The Reserve Bank included this chart in a prominent place (the end of the policy chapter) in the Monetary Policy Statement.

They never explicitly state, but clearly want us to notice, that the Reserve Bank’s errors have been a little less than those of each of the other twelve forecasters. (And we might be curious who forecaster L was.)

It would have been more helpful if the analysis from which this chart was drawn had been published with the MPS, rather than simply being described as “forthcoming”. I’m a little sceptical of exercises of this sort, especially ones covering such a short period (three years of forecasts, which in the case of two year ahead forecasts means not even two non-overlapping observations), but it is consistent with the impression I developed sitting round the monetary policy table during that period: the Reserve Bank was constantly expecting inflation pressures to pick up, but most other private forecasters expected either more inflation or more interest rate increases than we did. We were wrong, but they were more wrong.

But I was a little curious. The Reserve Bank was at pains to tell us that their modelling suggests long-term private inflation expectations are still well-anchored at 2 per cent.

For two-year ahead forecasts, the RMSE for the Reserve Bank’s forecasts was 1.29. If the Bank had simply forecast that inflation would have been at the midpoint of the target, each and every two year-ahead forecasts, their error would only have been 1.22. Other forecasters must all have been projecting outcomes even further above the midpoint, on average, than the Reserve Bank did.

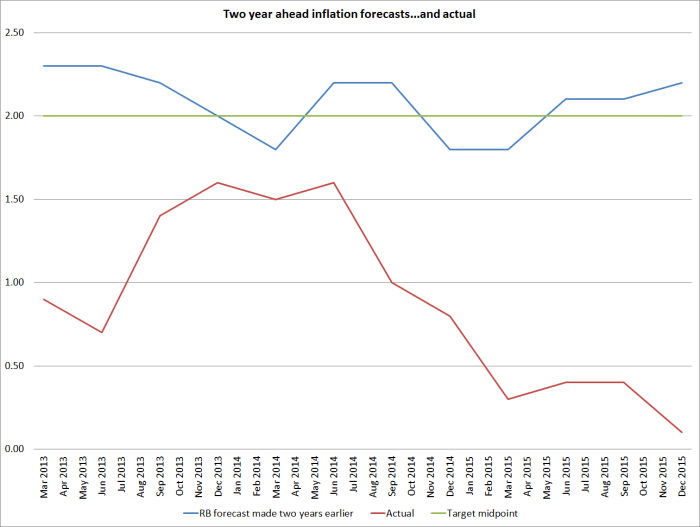

Here are the Bank’s two-year ahead inflation forecasts done over 2011 to 2013 and the associated inflation outcomes.

It isn’t a pretty picture.

The Reserve Bank would no doubt respond that its medium-term inflation forecasts will always be near 2 per cent – the interesting information is really in their view of what interest rate will be required to keep inflation around 2 per cent. But we know they’ve been persistently too high on those forecasts as well – albeit perhaps less so than the private forecasters.

One other problem with the analysis is that there was a “regime change” halfway through the period. A new Governor took office, and the 2 per cent midpoint was added to the PTA. Private forecasters had previously often operated on the (empirically reasonable) assumption that the Bank had been content for inflation to settle in the upper part of the inflation range, and may have been forecasting on that basis. The Reserve Bank couldn’t credibly produce those sorts of forecasts – at least when inflation was already near 2 per cent – so it might in part be just luck that made the Reserve Bank’s errors less than those of the private forecasters.

But as a reminder, when the Reserve Bank asserts that longer-term inflation expectations are securely anchored at 2 per cent, it is relying on forecasts produced by exactly the same set (or a subset of this group) of private forecasters. Since they were producing worse forecasts than the Bank’s own poor forecasts in recent years, it is a mystery to me as to why we should take any comfort from their views of what inflation might be over 10 years – a subject to which they probably devote little effort, and have little expertise or incentive to be right. Perhaps the other “forthcoming” papers will shed light on that puzzle too?