The Reserve Bank included this chart in a prominent place (the end of the policy chapter) in the Monetary Policy Statement.

They never explicitly state, but clearly want us to notice, that the Reserve Bank’s errors have been a little less than those of each of the other twelve forecasters. (And we might be curious who forecaster L was.)

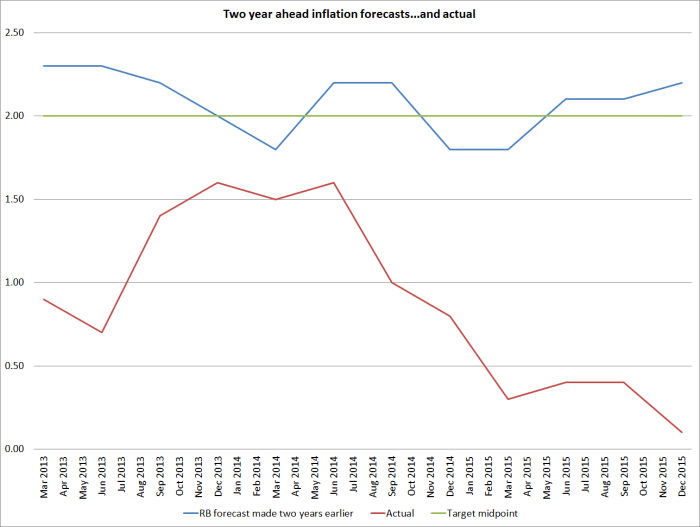

It would have been more helpful if the analysis from which this chart was drawn had been published with the MPS, rather than simply being described as “forthcoming”. I’m a little sceptical of exercises of this sort, especially ones covering such a short period (three years of forecasts, which in the case of two year ahead forecasts means not even two non-overlapping observations), but it is consistent with the impression I developed sitting round the monetary policy table during that period: the Reserve Bank was constantly expecting inflation pressures to pick up, but most other private forecasters expected either more inflation or more interest rate increases than we did. We were wrong, but they were more wrong.

But I was a little curious. The Reserve Bank was at pains to tell us that their modelling suggests long-term private inflation expectations are still well-anchored at 2 per cent.

For two-year ahead forecasts, the RMSE for the Reserve Bank’s forecasts was 1.29. If the Bank had simply forecast that inflation would have been at the midpoint of the target, each and every two year-ahead forecasts, their error would only have been 1.22. Other forecasters must all have been projecting outcomes even further above the midpoint, on average, than the Reserve Bank did.

Here are the Bank’s two-year ahead inflation forecasts done over 2011 to 2013 and the associated inflation outcomes.

It isn’t a pretty picture.

The Reserve Bank would no doubt respond that its medium-term inflation forecasts will always be near 2 per cent – the interesting information is really in their view of what interest rate will be required to keep inflation around 2 per cent. But we know they’ve been persistently too high on those forecasts as well – albeit perhaps less so than the private forecasters.

One other problem with the analysis is that there was a “regime change” halfway through the period. A new Governor took office, and the 2 per cent midpoint was added to the PTA. Private forecasters had previously often operated on the (empirically reasonable) assumption that the Bank had been content for inflation to settle in the upper part of the inflation range, and may have been forecasting on that basis. The Reserve Bank couldn’t credibly produce those sorts of forecasts – at least when inflation was already near 2 per cent – so it might in part be just luck that made the Reserve Bank’s errors less than those of the private forecasters.

But as a reminder, when the Reserve Bank asserts that longer-term inflation expectations are securely anchored at 2 per cent, it is relying on forecasts produced by exactly the same set (or a subset of this group) of private forecasters. Since they were producing worse forecasts than the Bank’s own poor forecasts in recent years, it is a mystery to me as to why we should take any comfort from their views of what inflation might be over 10 years – a subject to which they probably devote little effort, and have little expertise or incentive to be right. Perhaps the other “forthcoming” papers will shed light on that puzzle too?

A couple of links you have probably already read; if not, may be of interest –

* http://www.bbc.co.uk/programmes/p002vsxs – “Are economists always wrong”

* Expert predictions have been shown to be right with about the same odds as a chimpanzee making a pick – see Expert Political Judgment: How Good Is It? How Can We Know? by Philip E. Tetlock – http://press.princeton.edu/titles/7959.html

A pithy summary of this book by Tim Harford – http://timharford.com/2011/12/of-foxes-hedgehogs-and-the-art-of-financial-forecasting/ – The psychologist Philip Tetlock, author of the modern classic Expert Political Judgement, conducted a two-decade investigation into the accuracy of expert forecasts in social sciences. He discovered that regardless of academic field, practical experience, gender or political persuasion, experts make very poor forecasts. By some measures, the “chimp strategy” of randomly predicting that things will get better, or get worse, or stay much the same, matches the best the experts can do. Mr Tetlock did find one way of dividing up his experts in a way that correlated with less-awful forecasting ability: that of “cognitive style”. Harking back to an essay by Isaiah Berlin, and before him to the Greek poet Archilochus, Mr Tetlock points to the “hedgehogs”, people who view the world through the lens of a single, powerful, logical idea. They make hopeless forecasters. Less hopeless are intellectually promiscuous, self-doubting dabblers. They are called, of course, “foxes”.

Best wishes

Tony

LikeLike

Thanks Tony. I’ve just been reading a no-longer-new book applying the hedgehog vs fox image to an explanation of the relative economic performance of the Anglo world on the one hand and the Latin American countries on the other.

I reckon short-term macro forecasting is mostly futile – expert or not- and that in practice most central banks, ours included, act as if they are simply looking at the window and getting a rough feel on where things are right now. I guess corporates (and govts) need some assumptions to plug into planning spreadsheets, but better call them that and not pretend they are forecasts with any real potential for accuracy.

LikeLike

Agree. What’s the book you’ve been reading?

LikeLike

The author is Chilean but spent much of his life in Australia (where at an advanced age he still writes for Quadrant from time to time)

http://www.amazon.com/The-New-World-Gothic-Fox/dp/0520083164

LikeLike

Will take a look

LikeLike

Matrices, permutations and possibiities

The economics profession have trapped themselves into a deadly-handshake of their own making – and now they can’t get out of the trap

I’m a (non-bank) low-level down-at-the-coal-face economist. I have always considered economics a valuable tool for analysing and understanding past events. When it comes to guiding and directing the future path of an economic activity (read economy), it is not a good idea to be too doctrinaire about it. One can prognosticate about possible outcomes of various choices. I gave up forecasting outcomes years ago for the following reasons: (a) An “economy” comprises 1000’s of input components (b) The international card game of bridge, each of 4 players receives 13 cards from a deck of 52. The chance of any player receiving the same combination of 13 cards again is 1 in 635,013,559,600. That’s 635 billion.(c) Take 5 components, and using just one, there are 5 alternatives. Take 5 components and using any 2 together there are 32 possible outcomes. With 20 components the possible outcomes exceed 1 million. At any moment in time. And that assumes each component in each example is applied in fixed measure

I knew this not – until a professor (with a Phd) from Melbourne University pointed it out to me

They just don’t teach that in Economics

More recently it was calculated that in the game noughts-and-crosses with nine 9 positions there are 366,000 possible outcomes

And doh-rag-wearing rugby international Peter Fitzsimons – Mind googoling

Interesting. TFF has been browsing Adam Spencer’ latest book, World of Numbers – which is sort of mathematical quirks and concepts, explained by a geek who can also write bloody well. The one that most stunned me is this. Spencer says that if you truly shuffle a deck of cards, properly, you will have in your hands one of the 52 x 51 x 50 x … x 3 x 2 x 1 =8065817517094387857166063685640376697528950544088327782 4000000000000 different ways you can shuffle a deck. A big number, I know. But what fascinates me is his contention that, “you can be assured that the order of cards you hold in your hands, has never happened before in the history of the universe … and will NEVER happen again! If a billion people, shuffled a billion decks of cards every day for a billion years they would not scrape the surface of the total number of ways a deck can be arranged.” Try adamspencer.com.au for the book

http://www.smh.com.au/comment/enough-already-of-tony-abbott-20151211-gll9j3.html

LikeLike

Wow, we live in the era where we are witnessing the death of neo classical economics that we were all bought up in through our university education, some now realise it was a load of maths based garbage, and the Reserve Bank is focusing on Inflation Forecast Errors. Look at the window, deflation is knocking on the door.

Perhaps they should be doing CIA scenario testing…what the f*** do we do if capital adequacy is a fantasy, how do we fund the banks, how much of a hair cut will the public take. Should be offering Fonterra Patriotic Bonds, with a guaranteed 3% return rather than corporate welfare via the tax payer.

The list is endless.

Their conversation is not even on the right page of the right book, imo…. 🙂

LikeLike

Interesting. But what we (the public) need to know whether the forecasts beat the random-walk. This applies to GDP and the exchange rate too. Because if the RB forecasts do not beat the RW model we have a problem; we invested too much in the model…

LikeLike

I haven’t read the MPS, so I don’t know the context in which the chart was produced. It makes a valid point. But I hope the larger context was something like: –

We haven’t been very good at our job and we’ll try harder. But for the record we’ve been better than everyone else, which is what you’d expect because it’s what we get paid for!

LikeLike

Humble opinion: seems much focus on outcomes rather than process. The RBNZ is not alone when it comes to central banks getting the inflation dynamic wrong post GFC – in part, because ‘easy’ policy conditions should, based on convention, lifted the general price level by now. And I guess that reflects the notion that the inflation ‘process’ is a lot more uncertain than it once was : is it demand pull, is it cost push, is it wage driven, expectation led or ultimately still caused by too much money? Clarity of thought on the process of inflation in a world that is much changed from the pre crisis period would be more credible than a few pretty pictures….

LikeLike

There is inflation. It just went into assets rather than consumables. Consumable pricing may be affected due largely to the internet and open borders that allow the cheapest products to be available at short notice from anywhere around the world. Your local shop is no longer competing locally but globally.

LikeLike