Various media outlets over the last day or so have asked for my views on whether banks will, or should, pass through yesterday’s 25 basis point cut in the OCR into lower retail rates.

My bottom line was

“I think there will be political pressure on the banks to cut to some extent, but I’d be surprised if it [any cut in floating mortgage rates] was anything like 25 basis points.”

It didn’t even seem a terribly controversial point.

After all, the Reserve Bank had included this chart in the MPS yesterday

And they could have included one of credit default swap spreads for Australasian banks (as per this one at interest.co.nz).

The Bank even commented in the MPS that:

the cost of funding through longer-term wholesale borrowing has risen with the pick-up in financial market volatility (figure 4.3). The increase in longer-term wholesale costs this year adds to the increasing trend since mid-2014, which reflects a mix of global regulatory changes, concerns about commodity markets and emerging economies, and broader financial sector risks. To date, strong domestic deposit growth has limited the need for New Zealand banks to borrow at these higher rates. However, acceleration in credit growth over the past year might increase banks’ reliance on higher-cost long-term wholesale funding, leading to higher New Zealand mortgage rates.

It has been a commonplace in the recent Australian discussion that unless the Australian cash rate is lowered higher mortgage rates seem quite likely because of the rising funding spreads.

And so I was slightly taken aback to see the Governor, and his offsiders, quoted as having told Parliament’s Finance and Expenditure Committee that

“I’d expect the floating rates to come down by 25 basis points,” Wheeler told the select committee.

and that

“Banks are only raising a relatively small share of their funding from overseas at this point in time. They’re continuing to see very strong deposit growth. Most of the credit expansion that’s going on has been funded through deposits,” Hodgetts said.

Central bank governors aren’t there to provide defensive cover for banks’ pricing choices, but neither should they be winning cheap popularity points in front of committees of politicians by calling for specific cuts in retail interest rates that don’t even look that well-warranted based on their own analysis (eg the MPS quote above).

Bernard Hodgetts, head of the Bank’s macro-financial stability group, argues that rising offshore funding costs aren’t really relevant because banks haven’t raised much money in those markets recently. But surely he recognizes the distinction between average costs and marginal costs? For the banking system as a whole, the place where they can raise additional funding – much of which has to be for term, to satisfy core funding ratio (and internal management) requirements – is the international wholesale markets. And what banks would have to pay on those markets in turn affects what they are each willing to pay for domestic term deposits.

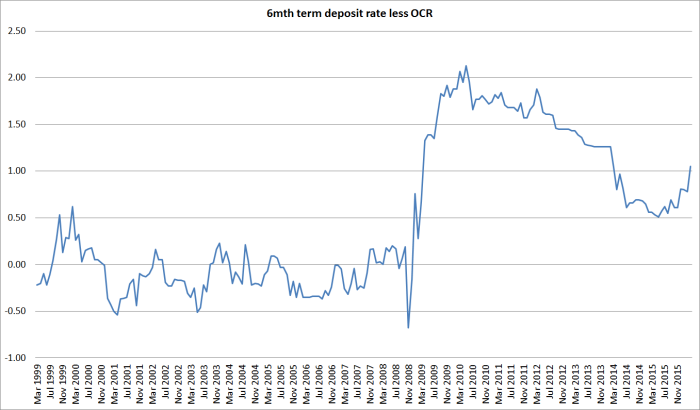

There isn’t a one-to-one mapping between rises in indicative offshore funding spreads and spreads of domestic terms deposits, but hereis a chart showing the gap between term deposit rates (the indicative six month rate on the RB website) and the OCR.

Unsurprisingly, it looks a lot like the indicative offshore funding spreads chart above.

And what about the relationship between floating mortgage rates and the OCR? Here I’ve shown the gap between the floating first mortgage new customer housing rate and the OCR. I’ve included yesterday’s OCR cut and assumed that banks eventually cut their floating mortgage rates by the 10 basis points the ANZ, the biggest bank, announced yesterday.

The resulting gap doesn’t look particularly surprising. The gap between mortgage rates and the OCR blew out during the 08/09 crisis when funding spreads and term deposit margins blew out. It came back from those peaks and has been fairly stable since – narrowing a bit further a couple of years ago, when it looked as though funding spreads might continue to narrow (and when banks were trying to get loans on their books in face of the new LVR controls). And now, perhaps, those spreads are widening out again – as one might expect given the persistence of the rise in the offshore funding spreads.

All these points are really illustrative only. I don’t have access to more precise data. But as in any business, pricing involves some judgements. Perhaps the political and customer pressures will mount and banks will find themselves having to pass more of yesterday’s OCR cut into lower retail lending rates than they would really like. But this is a repeated game. Even the Reserve Bank expects one more OCR cut before too long, and many of the banks now expect at least one beyond that. Over the course of the rest of the year, it seems likely that unless those international funding spreads start sustainably falling again, that retail interest rates will fall by less than the fall in the OCR. It has happened before – most notably in 2008/09 – and will happen again. And it works both ways: if funding spreads ever go back to pre-2008 levels, retail rates will fall further than (or rise less than) the OCR. The Reserve Bank takes those factors into account when it sets and reviews the OCR every few weeks.

From my perspective, the prospect that retail rates might fall less than the OCR is neither good nor bad, it just is. As in any business, costs are an important consideration in pricing, but retail mortgage banking is also a pretty competitive business. Banks don’t need our sympathy, but we also don’t need populist anti-bank cheap shots.

The right answer for the Governor, asked by MPs whether banks would pass on the lower OCR, would surely have been something along the lines of “That is up to them. They operate in a competitive market, and they face a variety of cost pressures. We’ll be keeping an eye on each stage of transmission mechanism – between OCR changes and eventual changes in medium-term inflation – and will adjust the OCR as required to deliver on the target set for us in the PTA”.