Back on 27 August 2015, I wrote about the Reserve Bank’s refusal (having taken almost two months to consider the matter) to release anything material from the extensive work it had been doing on possible reforms to the governance of the Reserve Bank.

Somewhat frustrated by the obstructionism, I commented then

If the Official Information Act really provides protection for every single one of the papers covered by my request, including the titles of those papers, the Act is even more toothless than most had realised. In fact, I suspect that this is a case of instititutional arrogance and over-reach by the Governor, who doesn’t really seem to regard himself as accountable to the public. Perhaps the Governor is embarrassed, or frustrated, that the Minister of Finance or Treasury were not convinced by his particular arguments? Perhaps he had staff simply look at one option, and ruled out of court any serious consideration of the wide range of options used internationally and elsewhere in the New Zealand public sector to govern powerful public agencies? Whatever the explanation, he doesn’t want us to know.

And

As I’ve said previously, the Reserve Bank is much less transparent than it likes to make out. This is just another example. We’ll see whether the Ombudsman agrees with their interpretation of the Act. Whether or not she does, this decision by the Governor is not the hallmark of an open and accountable public institution, committed to scrutiny and debate and to improving policy and institutions through the contest of ideas.

I had also requested information on any work on Reserve Bank governance from The Treasury. With their accustomed more positive approach to the Official Information Act, they released a reasonable amount of material, which I wrote about here. A paper dated 5 June 2015 confirmed (what I already knew) that the Reserve Bank work programme had ceased, and Treasury’s advice to the Minister (in a note on the Reserve Bank’s draft Statement of Intent) that work should be continued apparently went nowhere.

Several times since then, I have highlighted the Reserve Bank’s refusal to release any of the material on governance, despite it being a completed project. I had lived in hope that one day the Ombudsman’s office would get to my complaint, and that the Bank might be compelled to release at least some of the material.

And then, out of the blue this afternoon, an email arrived from the Bank (apparently released simultaneously, and before I had even had a chance to read it, on the Bank’s website). Here is the heart of their letter

At the time we responded to you in August 2015, we withheld information under section 9(2)(f)(iv) of the Act, on the basis that advice was being considered by the Minister and had been tendered to him. In September, Associate Minister of Finance Steven Joyce told Parliament that the government had no plans to reform the governance structure of the Reserve Bank – meaning the advice to the Minister was no longer under active consideration. This is a change in circumstances that provides an opportunity for the Reserve Bank to revisit its decisions on your request. The Reserve Bank considers it now appropriate to release to you the following documents:

- Terms of reference: Moving to committee decision making;

- Sections of RBNZ Act subject to revision with a change in decision-making framework;

- Central bank decision making committee design;

- Email from Minister’s office (with “out of scope” material redacted);

- Governance arrangements: decision making committees. Some information has been withheld under the provisions of section 9(2)(g)(i) of the Act, to maintain the effective conduct of public affairs through the free and frank expression of opinions by or between or to members of an organisation or officers and employees of any department or organisation in the course of their duty; and

- Best practice structure and governance of central bank decision making committees. Please note that the “best practice” referred to is as per the literature (specifically Blinder), and not subjective opinion of the paper’s authors.

The Reserve Bank holds other information within the scope of your original request that we are continuing to withhold, as provided by the following sections of the Act, for the reasons described:

- 9(2)(g)(i), to maintain the effective conduct of public affairs through the free and frank expression of opinions by or between or to members of an organisation or officers and employees of any department or organisation in the course of their duty;

- 9(2)(h), to maintain legal professional privilege; and

- 8(d) – the information is publicly available here – www.rbnz.govt.nz/research-and-publications/reserve-bank-bulletin/2014/rbb2014-77-01-02.

Back in September I had written about those comments from Steven Joyce, answering questions for the Minister of Finance from Greens spokesperson Julie Anne Genter.

I welcome the Bank’s change of heart. But I doubt it is entirely sincere. After all, it is now March, and the Associate Minister’s comments were made in September. I know the Reserve Bank is busy, but really….. Moreover, they are not being straightforward in claiming that the matter had been under active consideration by ministers up to that point. As the Treasury document, from June, already showed, the Bank had already ceased work on governance, and we can be pretty confident that cessation had occurred when the Minister of Finance had told them some time earlier still that he did not want to do anything about Reserve Bank governance. To reinforce the point, when they originally withheld all this material, back in August last year, they did not seek to invoke the argument that the material was under active consideration by the Minister (even though they included a laundry list of reasons for withholding).

I suspect the Ombudsman may finally have gotten round to investigating my complaint, and the Reserve Bank has decided to try to minimize its reputational losses by releasing this material now (and just prior to a long weekend etc), rather than wait for the Ombudsman to compel them to do so. Even having done so, the Ombudsman will still have to decide on the other material which they have withheld.

I haven’t had a chance to read the papers the Bank has released. They are all available at the link above. I will probably write about the contents at some stage next week.

Meanwhile, Reserve Bank governance still needs reform, and it is disappointing that the current government has been so reluctant for the Treasury and the Reserve Bank to continue work on reforming an outdated model, that doesn’t align well with (a) the current functions of the Bank, (b) international practice in the governance of monetary policy and financial regulation, or (c) the governance of other entities in the New Zealand public sector.

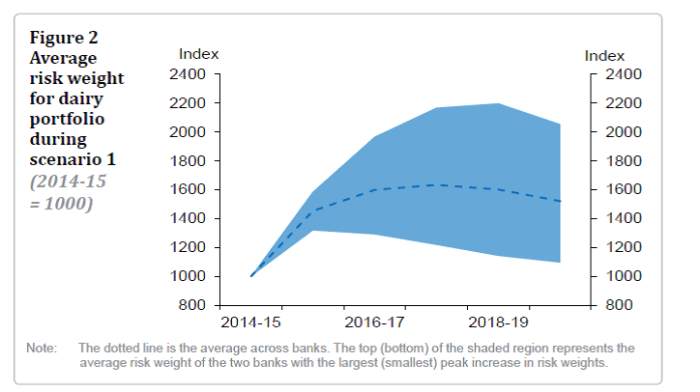

I’m largely going to ignore Scenario 1 from here on. As the long-term average real milk price is probably only around the assumed 2017/18 level, Scenario 1 doesn’t represent much of a stress test at all. The banks and the industry would have to be have been very rickety for a scenario like that to have presented a banking system problem. I think the Reserve Bank should also have discounted these results, rather than highlighting them in their press release.

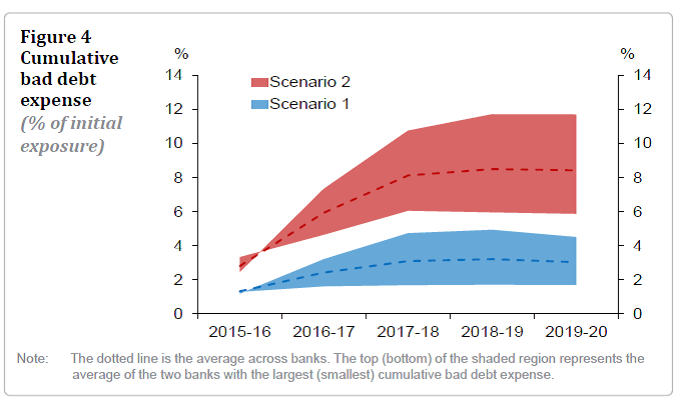

I’m largely going to ignore Scenario 1 from here on. As the long-term average real milk price is probably only around the assumed 2017/18 level, Scenario 1 doesn’t represent much of a stress test at all. The banks and the industry would have to be have been very rickety for a scenario like that to have presented a banking system problem. I think the Reserve Bank should also have discounted these results, rather than highlighting them in their press release. In a single year, dairy land prices fell by more than 30 per cent – and that was a severe, but very short-lived, fall in milk prices, and a rise in dairy non-performing loans that was still moderate compared to what we see in Scenario 2 in the current stress test. Perhaps deliberately, the Reserve Bank’s stress test does not seem to have taken account of a second round of selling (forced or voluntary), and the potential for that to drive land prices well below what might be a longer-term equilibrium level. Overshoots routinely happen in such markets, where liquidity is thin to non-existent, uncertainty is rampant, and potential buyers are few. As

In a single year, dairy land prices fell by more than 30 per cent – and that was a severe, but very short-lived, fall in milk prices, and a rise in dairy non-performing loans that was still moderate compared to what we see in Scenario 2 in the current stress test. Perhaps deliberately, the Reserve Bank’s stress test does not seem to have taken account of a second round of selling (forced or voluntary), and the potential for that to drive land prices well below what might be a longer-term equilibrium level. Overshoots routinely happen in such markets, where liquidity is thin to non-existent, uncertainty is rampant, and potential buyers are few. As