I’ve been a bit slow to get around to writing about the material the Reserve Bank released last week about the dairy stress test it conducted with the five largest dairy-sector lenders late last year.

I’ve long been of the view (and on record here) that, almost no matter how severe the dairy situation becomes, dairy loans would not represent a threat to the soundness of the New Zealand financial system. That is a top-down analysis based on

- the size of capital of the New Zealand banking system (around $36bn),

- the overseas ownership of all the main dairy-lending banks, and the absence of correlated exposures in most of them (dairy loans aren’t a big part of the Australian parents’ books),

- the fact that any losses on the dairy book will crystallise gradually, allowing other retained earnings, or outside injections of new capital, to buttress the overall position of the New Zealand banks, and

- that while dairy losses could in time be a part of a wider set of banking system losses (eg if severe losses also mounted on the housing portfolio), it is almost inconceivable that in such a scenario New Zealand’s exchange rate would not fall a lot further. A NZD/USD exchange rate of, say, .39 (where it got to in 2000) covers over quite a lot of weakness in the international prices of whole milk powder (in turn mitigating the severity of the dairy losses themselves).

There are counters to each of these points, but in the end I think they come down to this: if the Australasian banks ever face really large losses on their housing loans, the banks could be in trouble. I think that is very unlikely: house prices are held up by a combination of regulatory land use restrictions and population pressures, and vanilla housing lending has rarely if ever collapsed a banking system (as the Reserve Bank itself has acknowledged). You might disagree, but my real point is that dairy loans themselves aren’t going to threaten the soundness of the system. Much wealth will be lost. And many of the individual loans may have been ill-judged (by borrower and lender) but that is a different issue, and almost in the nature of a market economy operating under (the real world) conditions of uncertainty.

That is all top-down perspectives. But the stress test was useful precisely because it aims to be a bottom-up approach: working with the banks on how their actual dairy portfolios would behave under two pre-specified scenarios. Note what the exercise wasn’t: it didn’t look at the implications for loans to dairy companies themselves, or to suppliers to the dairy industry (companies or farmer), and also didn’t look at the impact on loan losses elsewhere in the portfolio resulting from the stresses on the dairy sector itself (eg retailers or builders or residential mortgages or… in dairy-dependent towns). Note that it was also only a rather provisional exercise, indicative more than definitive, and a basis for ongoing discussions between the Reserve Bank and individual banks.

That does tend to suggest we should use the higher loss estimates rather than the lower ones (since banks have fewer incentives to overstate the loss implications than to understate them).

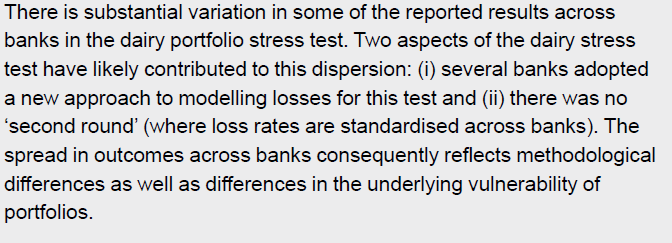

Here are the scenarios the Reserve Bank specified.

I’m largely going to ignore Scenario 1 from here on. As the long-term average real milk price is probably only around the assumed 2017/18 level, Scenario 1 doesn’t represent much of a stress test at all. The banks and the industry would have to be have been very rickety for a scenario like that to have presented a banking system problem. I think the Reserve Bank should also have discounted these results, rather than highlighting them in their press release.

I’m largely going to ignore Scenario 1 from here on. As the long-term average real milk price is probably only around the assumed 2017/18 level, Scenario 1 doesn’t represent much of a stress test at all. The banks and the industry would have to be have been very rickety for a scenario like that to have presented a banking system problem. I think the Reserve Bank should also have discounted these results, rather than highlighting them in their press release.

Scenario 2 does look much more like a real stress-test. But even if one thought the series of payout assumptions might be reasonable (2015/16 won’t have been that low, but some of the out years could still be lower than assumed here), I was surprised by the dairy land price assumptions. Despite a really severe adjustment in the payout path (absolutely, and probably relative to farmer expectations), dairy land prices are assumed to fall by just under 40 per cent (the cumulative effect of those three annual falls).

That might sound like a lot, but:

- when the Reserve Bank did its housing stress test, it assumed a 50 per cent fall in Auckland house prices. People still need to live somewhere, while they don’t need to farm cows.

- we’ve already a dairy land price scare not long ago. Here is a chart of the (“hedonic”)dairy land price index the Reserve Bank developed for REINZ (despite which, we don’t have general access to the series).

In a single year, dairy land prices fell by more than 30 per cent – and that was a severe, but very short-lived, fall in milk prices, and a rise in dairy non-performing loans that was still moderate compared to what we see in Scenario 2 in the current stress test. Perhaps deliberately, the Reserve Bank’s stress test does not seem to have taken account of a second round of selling (forced or voluntary), and the potential for that to drive land prices well below what might be a longer-term equilibrium level. Overshoots routinely happen in such markets, where liquidity is thin to non-existent, uncertainty is rampant, and potential buyers are few. As Eric Crampton’s discussion highlights, one difference between now and 2009 will be that potential buyers are probably much more aware of how significant the barriers are to any offshore buyers (who might otherwise be a stabilizing force in the market).

In a single year, dairy land prices fell by more than 30 per cent – and that was a severe, but very short-lived, fall in milk prices, and a rise in dairy non-performing loans that was still moderate compared to what we see in Scenario 2 in the current stress test. Perhaps deliberately, the Reserve Bank’s stress test does not seem to have taken account of a second round of selling (forced or voluntary), and the potential for that to drive land prices well below what might be a longer-term equilibrium level. Overshoots routinely happen in such markets, where liquidity is thin to non-existent, uncertainty is rampant, and potential buyers are few. As Eric Crampton’s discussion highlights, one difference between now and 2009 will be that potential buyers are probably much more aware of how significant the barriers are to any offshore buyers (who might otherwise be a stabilizing force in the market).

Loan losses evaluated on total dairy land prices falls of perhaps 60 per cent might be a more realistic stress test – recall, that stress tests aren’t central predictions, they are a scenario to test robustness against. Loan losses went up by 5 percentage points on the move from the (not very stressful) Scenario 1 to Scenario 2. The pattern of losses on loans should rise non-linearly as the test gets more stressful, and moving from a 40 per cent land price fall scenario to a 60 per cent scenario is a bit more of a land price adjustment than moving from Scenarios 1 to 2.

There are lots of other points of detail I could question (some things in the article just aren’t made as clear as they could be), but will just highlight one.

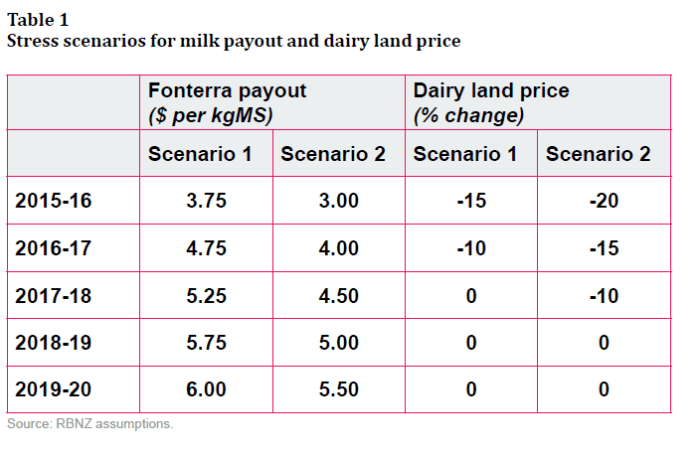

The Reserve Bank has long emphasized the desirability of having a capital framework for banks in which risk weights (whether imposed by the Bank, or flowing from the internal models of the major banks) do not have the effect of making capital requirements pro-cyclical. If capital requirements fall in asset booms and rise in shakeouts, the capital requirements will tend to amplify credit and asset price cycles (an existing stock of capital will go ever further as the boom proceeds, and ever less far – encouraging banks to rein in lending even more – as the bust proceeds). And yet the stress-testing article suggests that pro-cyclicality is deeply embedded in the modelling, at least for the dairy portfolio – itself the largest single chunk of banks’ commercial lending.

Here is what I mean.

This chart shows the average risk weight for the banks’ dairy portfolios under Scenario 1. Recall that Scenario 1 was not very demanding at all, and yet the average risk weight on dairy loans increases by 60 per cent (eg, from, say, 70 per cent to 112 per cent). No doubt deliberately, the Bank does not reveal how much further risk weights increase in the much more onerous Scenario 2. Even if it is not that much further, this sort of highly pro-cyclical pattern of risk weights looks like a bug that needs some serious attention.

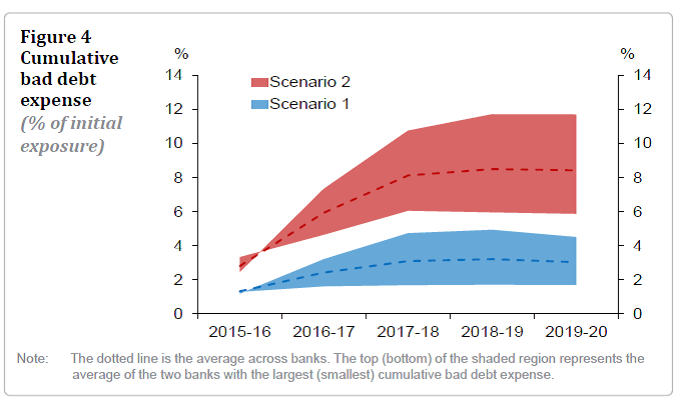

To recap, in Scenario 2, bad debt expenses average 8 per cent of dairy exposures.

But, as the Bank noted (see extract above), not all banks were as conservative as others. If we take the pessimistic end of the Scenario 2 range, we would have bad debt expenses of perhaps 11.5 per cent of dairy exposures. But, as noted above, the near-40 per cent fall in land prices in Scenario 2 still looks too shallow for such a fully-worked-through scenario. If land prices were to fall 60 per cent would it be implausible that in such an scenario, with all the second round effects accounted for and allowing for the non-linear loss profiles, the banks could face losses not of the “3 to 8 per cent of their total dairy exposures” that the Reserve Bank highlighted, but something more like 20 to 25 per cent of their total loans to dairy farmers? I deliberately pose it as a question, rather than a confident assertion, and it is – deliberately – the result of a stressed scenario, but it is probably a question people should be posing to the Reserve Bank.

Usually with land, a bank would require 50% equity to 60% equity which means land prices would have to drop by 50% to even begin to affect a Banks Balance Sheet. It is usually a second tier lender that would have their Balance Sheets wiped out as they are the high risk lenders that take 2nd security over and above a normal bank priority lending amount. Wheeler is correct that losses to banks would only be a tiny percentage.

When Allan Bollard moved interest rates to a record 9% he basically decimated 60 plus Finance companies balance sheets wiping out $6 billion in investor funds without understanding the implications. Thoughtless actions driven by an academic mindset.

LikeLike

We know – see the RB article – that there is quite a bit of diary debt in excess of 70% LVR, and bank exposure is rising not falling because of the need to provide additional working capital.

LikeLike

Capital of $36 billion by itself really has no meaning. It is how that capital is utilised that should be stress tested. What is important on a Banks balance sheet is the assets and the liabilities. The market value of capital is driven by speculation in the sharemarket. Capital only really matters in the initial capital raising or in a rights issue where that capital is raised and then is used and available to the operating entity.

LikeLike

Also not to forget the off balance sheet exposure, ie the promises the bank makes, eg the derivative market

LikeLike

I’m not sure I understand your point. $36bn isn’t a market value – after all, our banks aren’t listed – but a book value, and decent banks typically above book (brand value etc).

LikeLike

A – L = C therefore it is is how that capital is used, “A” can be Investments, cash, receivables or loans to bprrowers and “L” can be payables and depositors savings which then equates to “C”. Therefore what should be stress tested is the assets or the liabilities. Capital is received by the operating entity initially in the form of cash. The operating entity then decides what it wants to do with that cash ie put into investments, buy assets or lend it out to borrowers. Therefore capital by itself really has no meaning.

LikeLike

But shareholders funds which is capital plus retained earnings can have a risk that should be stress tested and that is the dividend payment policy which is the distribution of the previous years profit.

LikeLike

$36bn of capital relative to a total loan book of $407bn. Assuming there might be some knock on effect, the equity cushion seems quite thin. Then again, the ability to play with an internal ratings model could allow the cushion to stay inflated for a while yet.

LikeLike

Again the reference to $36 billion capital. Capital by itself has no meaning. A operating entity can only draw from other asset categories to fund a loan book write off ie what other investments can it liquidate to fund a loan book write down or it cuts its liabilities(OBR) or it lowers its dividend payment policy? It can’t draw on capital because capital is already recorded as assets and liabilities.

LikeLike

….my real point is banks can use “smoke and mirrors” more than any other sector and ultimately, trade largely on ‘confidence’. Not relevant to NZ but I’ve lost count how many times the Greek banking sector has been deemed solvent only to be short capital a few months later….

LikeLike

No, capital is the proportion of assets funded by the owners rather than by depositors or other creditors. Lose money on some loans (assets) and the nature of a fixed interest contract is that those losses reduce the claims of the owners, and don’t materially affect creditors/depositors until those owner claims are exhausted.

LikeLike

No No No Micheal, Capital is a historical record of the initial cash that goes into a operating entity it really has zero impact to an operation other than to determine how dividends is distributed. Thats why owners are the last in line on liquidation.

Day 1 A = C

Day 2 when the operating entity starts trading A-L = C

Day 3 when the operating entity makes a profit A-L = C+ R(Retained Earnings)

Therefore Capital by itself has no meaning. It exists in the form of Assets and liabilities.

LikeLike

well sure (more or less – remember retained earnings) but it doesn’t change the analysis. At present, the book value of assets is $36bn more than the book value of liabs. If say $6bn is written off dairy loans, that is a hit to recorded capital (and the real wealth of owners). recall that this stress test wasn’t a full institution one – it was a test of a particular book, and I reckon their analysis (and my negative spin on it) justify the conclusion that – all else equal – capital is large enough that dairy loans don’t threaten the health of the institutions individually (or the system).

Are we actually disagreeing about any point of substance?

LikeLike

It boils down to whether economists actually understand what is being stress tested.

LikeLike

….stress test ‘L’: game over i.e. bank run.

LikeLike

Under Open Bank Resolution(OBR) bank runs do not occur. In a possible bank run disaster scenario, the RB has the power under OBR to exercise a freeze on a banks operations. effectively preventing a run on savings.

LikeLike

Well, sure but rational runs happen (and most runs are rational) when asset losses are such that people think there is a high risk that the owners’ equity won’t be enough to absorb asset losses.

LikeLike

OBR prevents a run. Capital is never ever enough because Capital is a historical record. The cash initially received ie Dr bank, Cr Capital. gets invested or lent out. Cash is always committed because the owners/shareholders has a expectation of dividend payments for his investment into the banks initial capital base.

LikeLike

“Gareth Vaughan argues if we look at banks’ housing loan exposure from a financial stability perspective they simply must hold more capital against it”

http://www.interest.co.nz/opinion/80760/gareth-vaughan-argues-if-we-look-banks-housing-loan-exposure-financial-stability

The problem with increased capital is that there is also the investment side of the equation. If you increase the capital adequacy requirements you effectively raise more cash. What do you do with that additional cash? You can’t on lend it but now you have to meet owners dividend payments expectations. If don’t then you end up with declining share values and shareholders rantings at Annual Meetings.. There is a cost attached to that increased capital therefore what do you expect the bank to do? Investment in the currently highly volatile sharemarkets that are potentially collapsing? Invest in cash that have zero or negative returns? Or lend extensively to higher risk commercial ventures such as Dairy? or become a small business lender that has a 80% chance of failure?

Higher capital requirements do not mean less bank stability risks because it is wholly dependent on what the bank does with that additional cash raised. At a time when money is devaluing, you do not want to hold cash so it means higher risk investments and if it is not into housing then where does it go? If that investment risk is too high then that additional capital adequacy requirement drives higher Bank Stability Risks.

LikeLike