Statistics New Zealand this morning released the annual regional GDP data. My former colleagues at the Reserve Bank were never very keen on money being spent on producing this relatively new data – it is nominal rather than real, and is only available with a fairly long lag. The data are no use at all for short-term analysis of macroeconomic trends – and of course it would be better if we had regional real GDP data, and real income data – but there are plenty of other uses for even not-that-timely nominal data. It has brought together the range of other regional data in a useful summary form, and provides us data back as far as the year to March 2000 (which conveniently coincides with the terms of last two governments).

To listen to much of the New Zealand debate in the last 20 years or so, you might suppose that Auckland has been the stellar economic performer. After all, we often hear about the benefits of agglomeration, the importance of cities and so on (all of which are, in general, valid and important perspectives). Auckland is our one moderately large city, its population has continued to grow strongly, and central government – in the form of an ACT Party minister – even created a single council to help realise all these benefits. Population growth in Auckland in recent times has largely resulted from immigration (there has been a small outflow of New Zealanders from Auckland to the rest of the country). And successive governments, advised by The Treasury and MBIE, tout the economic benefits of a high rate of immigration, under our skills-based immigration policy – it is, we are told, a critical economic enabler.

Against that backdrop, the actual regional data look pretty disappointing, to say the least.

As a reminder, Auckland’s population (estimated at 1.55 million in the year to March 2015) is more than twice that of next largest region (Canterbury).

And its population has been growing much more rapidly (more than twice as fast) as the population in the rest of New Zealand.

As one would expect, nominal GDP per capita is higher in Auckland than in most other regions – but it is only third highest, behind Taranaki, somewhat “artificially” boosted by oil and gas production at high prices in recent years, and Wellington. In the most recent year, Canterbury’s GDP per capita is about the same as Auckland’s – but that is no doubt a temporary rebuild-related phenomenon.

And the trend has been going against Auckland, despite (?) all that rapid population growth. Here is a chart of Auckland per capita GDP divided by the GDP per capita of the median region in New Zealand. It is a bit noisy from year to year – Auckland looks to have done quite badly during the 08/09 recession and regained a little ground since – but the trend has clearly been modestly downwards (compare the latest observation with one from 10 years ago).

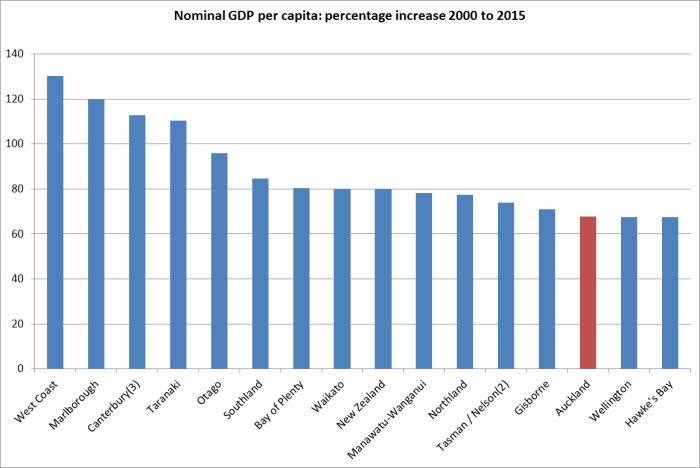

And which regions have done best? Well, here is the percentage growth in nominal GDP per capita, by region, for the 15 years to the March 2015 year. (The picture for just the last 10 years is pretty similar – although Wellington has done notably better in that subperiod.)

Of course, these are GDP per capita measures, and the age structures of regions do differ. But it doesn’t look as thoough that helps much. The labour force participation rates in Auckland and the rest of the country are almost identical (a higher labour force participation rate helps boosts GDP per capita in Wellington). Working age population as a share of total population is a little lower in Auckland than in the country as a whole, but over the 15 years for which we have data the working age population share has changed by much the same amount in Auckland as in the country as a whole.

Perhaps there are good answers to why Auckland appears to have underperformed – not over a year or two, but over 10 or 15 years – that would leave intact the story about the gains to New Zealanders from a large scale immigration programme, and the emphasis on the centrality of our largish city, Auckland, to New Zealand’s overall economic success.

But for now, it just seems to add to the increasing number of straws in the wind that suggest that the whole population and immigration-based approach to economic policy – and our immigration policy is one of the largest discretionary levers of government economic policy – is flawed. Productivity growth has been consistently poor, tradables sector production per capita has recorded no growth in a decade, and our largest and fastest-growing city (in both cases, by some considerable margin) has been recording lower per capita growth than most of the rest of the country, and average incomes in Auckland have, if anything, slowly been converging towards the median.

An alternative narrative of New Zealand’s economic performance and policy, of the sort I have been running now for several years, would find little or none of this surprising. Disappointing yes – this is our country’s prosperity, and the future of our children – but no more surprising than the failure of other flawed economic strategies in the past, here and abroad. Our immigration programme for the last 25 to 30 years might better be reassigned the label once given to the ambitious, deeply flawed, energy projects of the early 1980s, Think Big. Like that programme, it was put – and kept – in place by well-intentioned people, genuinely seeking the best interests of their country. But like the earlier Think Big, this one has failed, and goes on failing. Outcomes matter a great deal more than good intentions.