One last post prompted by the quarterly national accounts release last week.

I’ve shown charts highlighting how weak our per capita income growth has been, and how the volume of business investment per capita has only just got back to near pre-recessionary levels.

But what about exports? In many respects they are the longer-term life blood of our economy – the success New Zealand firms have in selling in the rest of the world shapes, over time, what we can afford to buy from the rest of the world. And for a very small country, the rest of the world is most of the potential market. I highlighted last week how little growth there has been in New Zealand’s export share of GDP over decades.

Real per capita exports in the September 2015 quarter were 8.5 per cent higher than they had been in December 2007, just prior to the recession. In some ways, that doesn’t seem too bad – plenty of components of GDP have been weaker.

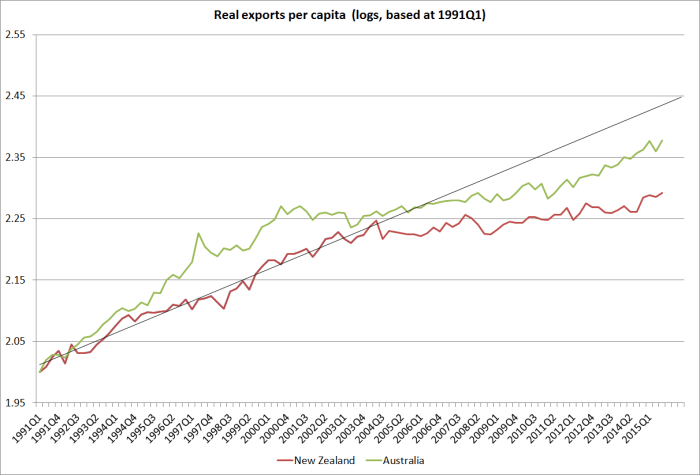

But here are real per capita exports for both New Zealand and Australia since the start of 1991. The starting point is determined simply by when the SNZ quarterly population series for New Zealand begins.

The trend line shows the trend in New Zealand per capita exports from the start of the series to the end of 2003. There is a visible fall in the trend rate of growth of exports after that point, but it also coincides with the sharp rise in New Zealand’s real exchange rate which has not been sustainably reversed since then.

What about the comparison to Australia? Australia achieved faster growth in real per capita exports in the first decade (around 1 per cent per annum faster). Australia’s real exports per capita then went sideways for a number of years (and more or less moved parallel to ours over perhaps 2002 to 2012) before once again growing materially faster than New Zealand’s exports over the last few years. Over the whole period since 1991, Australia’s exports per capita have risen 21.8 per cent faster than New Zealand’s.

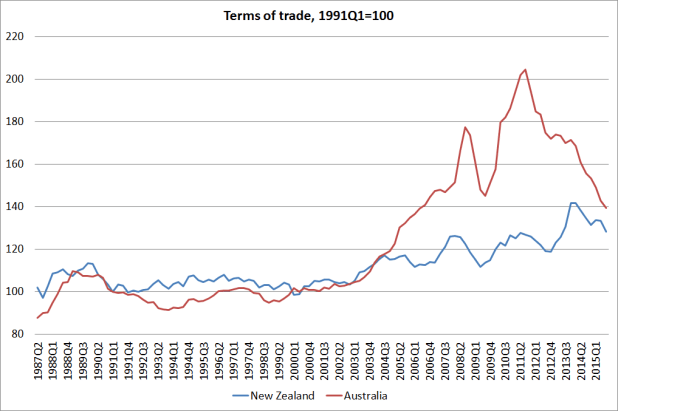

One story sometimes told is that if the terms of trade rises then a country doesn’t need to export as much (by volume) – if prices do the work, real resources can be used for other purposes (economic life is about consumption, not exports – which are just a means to an end). A higher exchange rate, on the back of the stronger terms of trade, redistributes resources away from the export sector.

Even if there is something to this point in principle, in practice it doesn’t look as though it explains much of the difference between the New Zealand and Australian performance. After all, Australia had a much bigger terms of trade surge than New Zealand did. Even now, whether we count from 1991 or from when the terms of trade started moving up strongly (around 2003/04) Australia has had a stronger terms of trade than we have.

Of course, Australia is still in the midst of an adjustment: exports are growing quite strongly on the back of the huge investment boom in the resources sector. But, on the other hand, the global prices of the commodities Australia exports are still falling, taking the terms of trade with it. If the terms of trade continue to fall much further, and stay low, some (much?) of that Australian investment might yet be regretted by the firms that undertook it – and might not, with hindsight, have helped Australia much. Only time will tell.

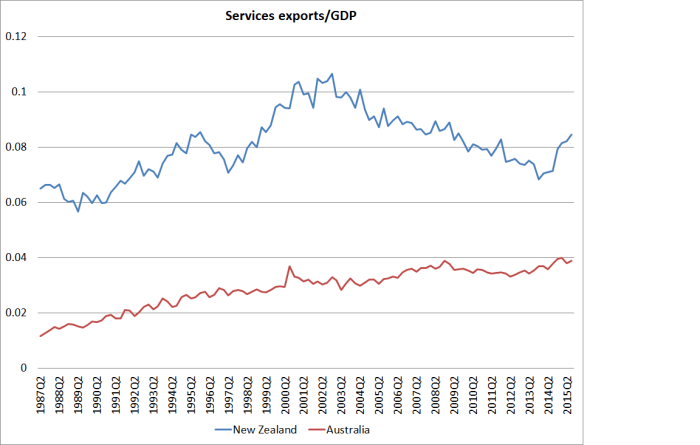

But lest anyone think Australia’s strong export performance is just about the resources sector, I found the chart comparing services exports in the two countries sobering (this reverts to nominal ratios to GDP because I couldn’t quickly find volume data for Australian services exports). New Zealand – the smaller country – still has a higher foreign trade share of GDP. But despite the way the terms of trade boosted the exchange rates in both countries (making for tough conditions for exporters of non commodity goods and services), services exports in Australia are now around the historic peak. But in New Zealand – despite the impressive surge in the last few quarters – services exports as a share of GDP are now barely 80 per cent of the previous peak.

Not a particularly cheery note for the approaching Christmas season, but then in the church’s year it is still Advent, a solemn season of reflection, preparation, and self-examination. So perhaps not so inappropriate after all.

When we have a RB that has intentionally decimated most of our local manufacturing we really end up mostly exporting milk. At some point we just run out of land that we can convert to dairy. The 44% drop in dairy prices would have driven our economy into recession however we have John Key to thank as he has quietly driven our tourism and international students into record breaking territory. At the moment our GDP is being held up by tourists, international students and the building industry.

Hopefully our latest space industry in Gisborne can redirect us towards a new direction. But I am pretty sure Wheeler is already planning to stamp on any growth in our economy with a rapid succession of interest rate rises as soon as we see any green shoots of growth.

LikeLike

Merry Christmas to you and your family Michael.

Why do you think the real exchange rate went up so much from 2001-2006? One theory I haven’t seen discussed, but is interesting to imagine in light of the writings of Michael Pettis, is that changes in the capital account can drive changes in the current account, with the RER being the transmitter.

LikeLike

Thanks Blair – and thanks for your contribution in commenting here over the year.

I’m boring and stick to changing interest differentials as the dominant story: we entered 2001 with the OCR at the same level as the Fed funds target, and (on average) that gap markedly widened (to and beyond something more normal) as (a) we avoided the US 2001 recession, and (b) had a lot of pressure on domestic resources – a not insignificant part of that was immigration, altho much of the swings in immigration was endogenous to strong domestic demand. I tend to discount capital account stories, at least for NZ (which was already pretty integrated with world markets in the late 80s and 90s) – prob more valid in the areas Pettis focuses on (ie emerging markets).

LikeLike

The RBNZ moved interest rates from 6.5% to 7.25% between 2001-2006 with an easing in 2002 to 4.75% and then aggressive increases to 7.25% even with an average and declining economy. The RBA in 2001 maintain the cash rate(OCR equivalent) at 5.75% in 2001 with an easing bias to 4.25% in 2002 and then up to 6.25% in 2006 a full 1% lower than the RBNZ even when faced when the biggest commodities boom in Australia. No wonder we do not have much of a manufacturing industry left.

LikeLike

The NZ Inflation Index averaged 2.6% between 2001 to 2006 and Australian inflation in that same period averaged 3.1%. It is clear that the RBNZ is way more aggressive than the RBA in squeezing inflation into a 2% target with the RBA keeping interest rates a full 1% lower than the RBNZ even when Australia’s inflation is more than a full 1% above the target inflation of 2%.

LikeLike