A financial markets participant who lost money in the market moves following Thursday’s Monetary Policy Statement got in touch yesterday to ask where I ranked Thursday “hawkish easing” – an OCR cut that actually tightened monetary conditions by prompting a 1.5 per cent increase in the exchange rate – among policy mistakes.

He may well have had an international context in mind, but my mind went back to various episodes in New Zealand since I got closely involved in 1987. As I pointed out to my correspondent, even if one counted Thursday as a mistake – and I certainly thought the policy stance was wrong, and the communications pretty unconvincing – there had been many worse over the years. Making mistakes, either in communications on the day or in the wider stance, is pretty much inevitable in the sort of discretionary monetary policy management most countries adopt. Unfortunately the Reserve Bank of New Zealand seems to have more black marks against its name than most. One could think of the MCI debacle in the late 1990s – which led directly to the troublesome clause 4b of the PTA – or the two lots of policy reversals (tightenings that had to be unwound) since 2010. Misjudging the overall appropriate stance of policy matters more (whether too tight or too loose) but it takes time for those errors to become apparent. My mind went back specifically to a “hawkish easing” fifteen years ago, when the market’s adverse verdict was immediately clear.

By May 2000, the Reserve Bank had been tightening monetary policy quite aggressively for some time. It was the first ever OCR cycle – the OCR was only introduced in early 1999, and we’d been raising the OCR by 50 basis points at a time. The OCR was at 6 per cent, the same as the Fed funds target rate – which itself was raised to 6.5 per cent on the morning of our MPS.

The May 2000 Monetary Policy Statement was released on 17 May. We raised the OCR by another 50 basis points to 6.5 per cent, and the projections foreshadowed the likelihood of another 75 basis points of increases over the next few quarters.

The exchange rate had been relatively low for some time by then (around 58 on the TWI as it is currently measured, but 54-55 on the index as it then was). When returns on USD assets were basically equal to those in the NZD, that weakness was hardly surprising (it is the example I use to illustrate why I’m pretty sure that if our OCR ever gets cut to near-zero our exchange rate will have fallen a long way).

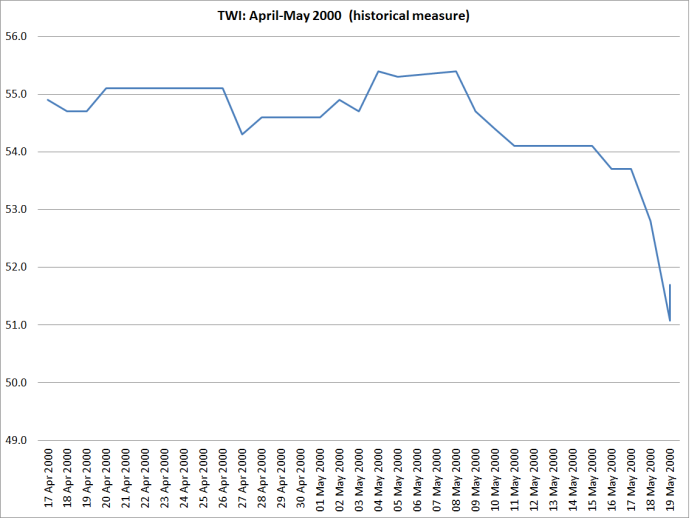

Running into the MPS release, the TWI had been weakening a little. I was deputy head of the Financial Markets Department at the time, and I recorded in my diary the night before the release that we were “likely to see the TWI lower” following the release.

In those days, we met at 7:30am on the morning of the release, to give final advice to the Governor and enable him to confirm his OCR decision. It was to be stressful day, but my diary records that at the meeting “just as well everyone, with more or less enthusiasm, on the OCR group endorsed 50bps – and at our morning meeting at 7:30 no one expressed even the least qualms”.

As I went on, “I’d expected the exch rate to ease off – not to 52.8. Over the following day or two, it fell as low as 51.08 – on a 50 point OCR increase, we saw the exchange rate fall by almost 5 per cent at worst, and around 4 per cent when things had settled down. Our widely-expected tightening ended up materially easing monetary conditions. We were more than a little flustered, and my diary records us hoping “without success, that one of the wire service reporters would ring so we could point him in Murray [Sherwin’s] direction for a [clarifying] comment”.

What was going on? Basically, the market (particularly offshore) did not believe us. They took the view that if we continued to raise the OCR that aggressively we would “kill the economy and hence exacerbate the future easing”. I was pretty sceptical at the time (as I imagine were my colleagues), but as it happened we tightened no further, and were cutting the following year. And as it happened there was a “growth pause” in 2000 that we had not anticipated. The exchange rate was to fall by a further 10 per cent over the following few months and headline inflation went briefly to 4 per cent by the end of the year.

The May 2000 OCR increase, and the hawkish path it continued to portray, was a pretty material misjudgement by the Reserve Bank. But what made it particularly bad was the strength of the immediate adverse reaction. We badly misjudged that reaction. There were a couple of local economists who were more hawkish than we were, but the market as a whole spoke – and it did not believe us, or believe that we would be able to carry through our envisaged policy. Even politicians weighed into the debate (Prime Minister and Minister of Finance).

By contrast, the only way to read the overall reaction since Thursday, has been that Graeme Wheeler’s latest policy announcement, and flat forward track, has been treated as credible. Only time will tell whether the OCR, and with it the exchange rate, will eventually have to go lower, but for now the Governor’s stance, that he does not envisage further cuts, is being taken seriously. And although there are some sceptical commentators (including – at least – Westpac, your blogger, my correspondent, and some macro advisory firms), there has been no controversy in the local media, nothing very critical in the commentaries from the local bank economists, and no comment at all from politicians on either side. If anything the tone of the questioning in the press conference was slightly sceptical of the need to have cut at all. So if I were Graeme Wheeler, I’d probably have got to the end of Thursday a bit disappointed that the exchange rate had risen by 1.5 per cent, but thinking that overall the reaction hadn’t been bad at all. After all, the (never very likely) alternative might have been that people treated the flat rate track, and end of the easing cycle story, as not very credible at all. If so, the exchange rate might have fallen significantly – an excessively hawkish stance increases the need for easing in the future.

Credibility matters a lot to decision-makers. Since no one can be 100 per cent sure what the right policy is, having the consensus with him probably matters a lot. After May 2000, Don Brash didn’t. For now, Graeme Wheeler does.