A financial markets participant who lost money in the market moves following Thursday’s Monetary Policy Statement got in touch yesterday to ask where I ranked Thursday “hawkish easing” – an OCR cut that actually tightened monetary conditions by prompting a 1.5 per cent increase in the exchange rate – among policy mistakes.

He may well have had an international context in mind, but my mind went back to various episodes in New Zealand since I got closely involved in 1987. As I pointed out to my correspondent, even if one counted Thursday as a mistake – and I certainly thought the policy stance was wrong, and the communications pretty unconvincing – there had been many worse over the years. Making mistakes, either in communications on the day or in the wider stance, is pretty much inevitable in the sort of discretionary monetary policy management most countries adopt. Unfortunately the Reserve Bank of New Zealand seems to have more black marks against its name than most. One could think of the MCI debacle in the late 1990s – which led directly to the troublesome clause 4b of the PTA – or the two lots of policy reversals (tightenings that had to be unwound) since 2010. Misjudging the overall appropriate stance of policy matters more (whether too tight or too loose) but it takes time for those errors to become apparent. My mind went back specifically to a “hawkish easing” fifteen years ago, when the market’s adverse verdict was immediately clear.

By May 2000, the Reserve Bank had been tightening monetary policy quite aggressively for some time. It was the first ever OCR cycle – the OCR was only introduced in early 1999, and we’d been raising the OCR by 50 basis points at a time. The OCR was at 6 per cent, the same as the Fed funds target rate – which itself was raised to 6.5 per cent on the morning of our MPS.

The May 2000 Monetary Policy Statement was released on 17 May. We raised the OCR by another 50 basis points to 6.5 per cent, and the projections foreshadowed the likelihood of another 75 basis points of increases over the next few quarters.

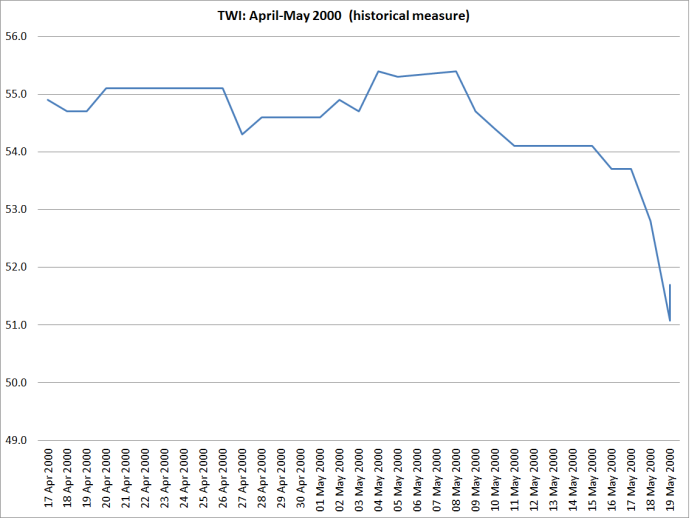

The exchange rate had been relatively low for some time by then (around 58 on the TWI as it is currently measured, but 54-55 on the index as it then was). When returns on USD assets were basically equal to those in the NZD, that weakness was hardly surprising (it is the example I use to illustrate why I’m pretty sure that if our OCR ever gets cut to near-zero our exchange rate will have fallen a long way).

Running into the MPS release, the TWI had been weakening a little. I was deputy head of the Financial Markets Department at the time, and I recorded in my diary the night before the release that we were “likely to see the TWI lower” following the release.

In those days, we met at 7:30am on the morning of the release, to give final advice to the Governor and enable him to confirm his OCR decision. It was to be stressful day, but my diary records that at the meeting “just as well everyone, with more or less enthusiasm, on the OCR group endorsed 50bps – and at our morning meeting at 7:30 no one expressed even the least qualms”.

As I went on, “I’d expected the exch rate to ease off – not to 52.8. Over the following day or two, it fell as low as 51.08 – on a 50 point OCR increase, we saw the exchange rate fall by almost 5 per cent at worst, and around 4 per cent when things had settled down. Our widely-expected tightening ended up materially easing monetary conditions. We were more than a little flustered, and my diary records us hoping “without success, that one of the wire service reporters would ring so we could point him in Murray [Sherwin’s] direction for a [clarifying] comment”.

What was going on? Basically, the market (particularly offshore) did not believe us. They took the view that if we continued to raise the OCR that aggressively we would “kill the economy and hence exacerbate the future easing”. I was pretty sceptical at the time (as I imagine were my colleagues), but as it happened we tightened no further, and were cutting the following year. And as it happened there was a “growth pause” in 2000 that we had not anticipated. The exchange rate was to fall by a further 10 per cent over the following few months and headline inflation went briefly to 4 per cent by the end of the year.

The May 2000 OCR increase, and the hawkish path it continued to portray, was a pretty material misjudgement by the Reserve Bank. But what made it particularly bad was the strength of the immediate adverse reaction. We badly misjudged that reaction. There were a couple of local economists who were more hawkish than we were, but the market as a whole spoke – and it did not believe us, or believe that we would be able to carry through our envisaged policy. Even politicians weighed into the debate (Prime Minister and Minister of Finance).

By contrast, the only way to read the overall reaction since Thursday, has been that Graeme Wheeler’s latest policy announcement, and flat forward track, has been treated as credible. Only time will tell whether the OCR, and with it the exchange rate, will eventually have to go lower, but for now the Governor’s stance, that he does not envisage further cuts, is being taken seriously. And although there are some sceptical commentators (including – at least – Westpac, your blogger, my correspondent, and some macro advisory firms), there has been no controversy in the local media, nothing very critical in the commentaries from the local bank economists, and no comment at all from politicians on either side. If anything the tone of the questioning in the press conference was slightly sceptical of the need to have cut at all. So if I were Graeme Wheeler, I’d probably have got to the end of Thursday a bit disappointed that the exchange rate had risen by 1.5 per cent, but thinking that overall the reaction hadn’t been bad at all. After all, the (never very likely) alternative might have been that people treated the flat rate track, and end of the easing cycle story, as not very credible at all. If so, the exchange rate might have fallen significantly – an excessively hawkish stance increases the need for easing in the future.

Credibility matters a lot to decision-makers. Since no one can be 100 per cent sure what the right policy is, having the consensus with him probably matters a lot. After May 2000, Don Brash didn’t. For now, Graeme Wheeler does.

So economics is as much about human psychology as it is about the laws of economics we learnt ?

LikeLike

Public policy even more so.

But the old line was that the great physicist Max Planck started studying economics and gave it up for physics because economics was too hard (too many moving parts – eg people). I’ve never known whether the story was just apocryphal or not, but either way it captures an important insight.

LikeLike

Max Planck was dead right

I’m a (non-bank) low-level down-at-the-coal-face economist. I have always considered economics a valuable tool for analysing and understanding past events. When it comes to guiding and directing the future path of an economic activity (read economy), it is not a good idea to be too doctrinaire about it. One can prognosticate about possible outcomes of various choices. I gave up forecasting outcomes years ago for the following reasons: (a) An “economy” comprises 1000’s of input components (b) The international card game of bridge, each of 4 players receives 13 cards from a deck of 52. The chance of any player receiving the same combination of 13 cards again is 1 in 635,013,559,600. (c) Take 5 components, and using just one, there are 5 alternatives. Take 5 components and using any 2 together there are 32 possible outcomes. With 20 components the possible outcomes exceed 1 million. At any moment in time. And that assumes each component in each example is applied in fixed measure.

LikeLike

Enjoyed this post Michael,

If I don’t catch up with you in the next couple of weeks

Have a great Xmas

Kind regards K

Sent from my iPhone

>

LikeLike

Thanks Kirdan. You too.

LikeLike

Micheal, promise to leave you alone soon but for a dummy, the Reserve Bank in its paper AN2015/05 estimates the neutral interest rate at 4.5%, as they say with current settings,( ie OCR at 2.5% and has been at similar rates for some time ) we should have strong expansionary settings, so why are we not at full employment and why is inflation so low ?

LikeLike

Alastair

A good question. Many people would say that the answer is that the “true” neutral interest rate in New Zealand is quite a bit lower than 4.5 per cent now (and the RB has acknowledged the possibility). No one has very good ways of estimating these things, but with the recovery having been quite insipid over recent years, and even credit growth pretty subdued, it doesn’t suggest that monetary policy has been highly stimulatory in any meaningful sense. Of course, the exchange rate muddies the picture somewhat (it is probably above a long-term sustainable level).

LikeLike

People interpret the lowering of the OCR as low expected inflation. They also expect US to increase the federal fund and interpret it as higher expected inflation. But in general there is alot of uncertainty. Should wait and see what the fed does. Exchange rate movements are difficult to forecast.

LikeLike

So with a low OCR “people” expect low inflation, believe the economy is sluggish, businesses lack confidence, won’t invest, people save because they are uncertain about future wages, won’t spend, we have to lower the OCR further …………

LikeLike

I wonder if there shouldn’t be too much focus on market movements in and around current central bank meetings. From my working experience, the market often wakes up on ‘decision day’ in a state of extraordinary tension and restlessness that can spill over into trigger happy reactions to written & spoken words which surely can only be used for investment (or speculative?) decisions over a time period greater than 24 hours. Short term horizons still dog the investment industry and given regular central bank meetings, such horizons seem even shorter in fixed income and currency markets. Typically, the initial bark is greater than any eventual bite: perhaps the market should also be questioned on the issue of credibility..!

LikeLike

A fair observation (and certainly one that central bankers would be keen to adopt). An alternative perspective is that financial market prices tend to jump on news, and don’t subsequently revert – ie there isn’t much sign of very short-term overshooting.

LikeLike

The only way to read the overall reaction on (since) Thursday, has been that Graeme Wheeler’s latest policy announcement, and flat forward track, has been treated as credible

There is another explanation, particlularly the violent 200 pip rise against the AUD

Users of electronic trading platforms run algorithms which constantly enter, wihdraw and cancel orders in the order book either side of the market, anything up to 300 or 400 pips both sides of the market, comprising both the market maker and natural participants. In the minute prior to major announcements nearly all the orders sitting in the order book are withdrawn. They evaporate. There are no orders available to be met, except for a few stragglers. The order book is empty 200 pips either side of the market. The instant the announcement is released anyone who has a protective stop in the market will be stopped out at a painful point where orders are available anything up to 200 points away from the market

Observation of the events of the day indicates there a large number of bets that got it wrong.

LikeLike

Short-term market positioning probably does explain some of the movements around any of these sorts of announcements. If it were the bulk of the story on this occasion though, I’d have thought we might have seen signs of an initial over-reaction unwinding by now.

When I describe the MPS stance as having been treated as credible, I guess I mainly had in mind the domestic audience. In the offshore markets, many people seem quite sceptical (and worse) about Graeme Wheeler, but even if so it hasn’t got to the point where people have been willing to place large bets that he is wrong. Some of that is no doubt that there is less risk capital around for macro trades than there might once have been, but it is still quite a contrast to the reaction I described in the 200 episode.

LikeLike

http://www.economist.com/news/business-and-finance/21679720-new-system-paying-civil-servants-puts-banks-through-their-paces-its-jungle-out-there

LikeLike

I don’t think Wheeler has the same superstar status that Don Brash or Allan Bollard commanded, which I do not think is a bad thing. We really do not need a superstar governor. The RB office already commands too much power and any mistake it makes affects hundreds of thousands of lives.

What I like about Wheeler is that he is prepared to quickly use macro prudential tools to target specific problem areas. Don Brash and Allan Bollard did not propose alternatives and were very much purists in pursuit of a theoretical ideal.

Until this day I am unable to forget the number(practically most) of building projects just went under due to interest rates being pushed by Allan Bollard up to 9% – 10% which then had domino effect on the 60 plus finance companies collapsing with a loss of $6 billion of NZ investor funds(no wonder there is a big bunch of baby boomers unable to retire). I could not believe the amount of carnage that a Reserve Bank Governor would be prepared to undertake to try and force inflation into a target band to the extent of driving the economy into a forced recession.

A lot of economists point to the GFC as the cause. But the previous NZ recession was not caused by the GFC but by Allan Bollard in a frenzied attack on the NZ economy wielding a 10% interest axe to bludgeon us into a recession. The GFC actually saved what was left of a decimated economy when interest rates dropped rather suddenly and it was not to save the NZ economy but it was because Allan Bollard was reacting to what the other Central Banks were doing in response to the GFC and it felt like he was out there to put up a show for his other Central Banker mates.

LikeLike

Certainly agree we don’t need a superstar as Governor, and to be honest your comment is the first time I’d ever heard anyone suggest Alan Bollard was someone warranting that label.

I’m not Alan’s greatest fan, but on this occasion I’m going stick up for him. Re policy alternatives, both Don Brash and Alan Bollard proposed practical alternatives to issues that had their roots in places outside the RB’s own remit. They don’t think a reversion to intense banking controls, when there was little banking risk, was a particularly appealing option. Read, for example, the joint SSI report by senior RB and Tsy staff (2006 – should be easy to google).

Also, the last 100 basis points or so of the pre-2008 tightening cycle was largely a response to the surging diary prices. Tightening policy to counter the demand effects of the unforeseen shock inevitably has distributional consequences – in the same way that tightening to lean against the house price and demand boom after 2003 also had spillovers that adversely affected the export sector. Was the tightening aggressive? Not really: rates peaked materially below the peak in the 1990s boom, even though the pressure on resources was greater, and core inflation was up around 3 per cent, and policy was only ever set to bring it back to around 2.5% (as distinct from the 2% mid-point.

Oh, and there was no way Alan was cutting the recession to impress other central bankers, altho it is probably true that his trips abroad highlighted just how serious the global downturn actually was. We’d probably have had a mild recession even without the so-called GFC, but equally the severity of what happened here was almost certainly attributable in part to the global downturn.

LikeLike

In the context of ivory tower well paid economists, I guess the decimation of almost the entire building industry, the loss of $6 billion of investor funds from the collapse of 60plus financial companies due to the domino effect of the collapse of the building industry, the breakup of hundreds if not thousands of relationships and marriages due to financial stress of a deep recession is considered not aggressive?? For NZ, the GFC saved the NZ economy and put us back on the path of growth and recovery.

Of course Wheeler was quite keen to stamp out the green shoots of the recovery last year with 4 rapid fire trigger happy interest rate rises.

LikeLike

I guess we aren’t going to agree on this one (again) but i’d argue that most of the finance company losses resulted from bad lending, not bad monetary policy. As for the path of growth and recovery, recall my chart from last week – real GDP in NZ is probably 15% below the path it was on pre 2008. Not euro-area bad, but not remotely good either.

LikeLike

NZ economists in general tend to rely on interest rates to control property prices. There was a reason why back in the 1990s, land prices was stripped out of the CPI equation. You cannot raise interest rates to try and control property prices. Land is a scarce resource(and scarcer due to land regulations) and as population grows that resource become more and more valuable as you try and fit more and more people in a limited space.

Auckland prices may look high but if you bring into account the fact the Unitary Plan allows for a secondary dwelling minimum with a minimum size of 40sqm on all the Mixed Housing zones which is virtually all existing Auckland properties it means that Auckland properties in the future will allow for a minimum additional income property when the Unitary Plan is approved.

LikeLike