A couple of weeks ago I wrote about the results of the Reserve Bank’s Survey of Expectations – the quarterly survey of relatively well-informed participants and commentators. Those expectations were still very subdued, with little sign of any expectation that (for example) core inflation would soon return to the 2 per cent target midpoint, which the Governor has undertaken to focus on.

Since then a couple of other inflation expectations surveys have come out. Both the ANZBO business survey and the Reserve Bank’s household expectations survey question on inflation have had an upward bias for many years. Reported expectations are, on average, well above both actual inflation at the time the survey was taken, and above the actual inflation rate for the period to which the expectations related. Both are measures of year-ahead expectations.

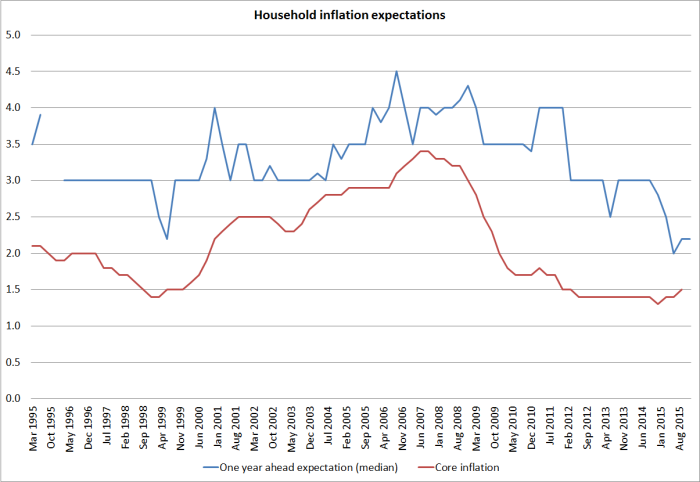

The Reserve Bank’s household expectations measures remain very subdued. In the 20 year history of the survey median year ahead expectations have never been lower than they have been over the last few quarters. And when the survey started, the inflation target midpoint was 1 per cent inflation not 2 per cent. Unless the relationship between core inflation (ie excluding the “noisy” bits like swings in oil prices) has suddenly changed, if inflation actually picks up materially over the coming year – as the Reserve Bank keeps telling us it will – these respondents will be surprised.

The survey also asks respondents directly whether they think inflation over the next year will go up, down, or stay the same. Again, there is a systematic bias in the survey – net, respondents have always expected inflation to rise. But outside the depths of the 2008/09 recession – the inflation effects of which people then thought would be short-lived – expectations for headline inflation rising have never been weaker. And, as a reminder, the most recent headline annual inflation rate was a mere 0.3 per cent

The survey now also asks about five year ahead expectations. We only have data since December 2008, but for what it is worth these longer-term expectations have never been lower than they are now.

The latest ANZBO survey came out yesterday. Inflation expectations dropped slightly, and looking at the chart that also seems to be a record low for the series. The Reserve Bank might claim to take comfort from the fact that expectations are still 1.6 per cent, not too far from the target midpoint. They shouldn’t. Again there has been a persistent bias in this series, and no obvious reason to think that that relationship has changed.

At the other end of the range of measures, New Zealand has a 10 year conventional government bond and a 10 year inflation indexed government bond. The gap between the two isn’t a pure measure of inflation expectations, but in normal circumstances it won’t be too far from what investors are implicitly thinking that inflation will be. The monthly average difference for November, as reported on the Reserve Bank website, was 1.40 per cent.

There is talk today of business confidence being a little stronger than it was. Perhaps, but the Reserve Bank’s job is to target inflation, near 2 per cent. It hasn’t done that successfully for some years now, through the ebbs and flows of business confidence, commodity prices, and the Christchurch repair process. And there is no sign in any of the recent surveys and related measures that that failure is about to remedied any time soon.

As the Governor contemplates his final OCR decision for the year, he should be thinking very carefully about these rather disconcertingly low expectations. The Governor often tells us that he wants to stabilise the business cycle. But if inflation expectations do become, in effect, entrenched at levels inconsistent with the inflation target, it can be very difficult – and potentionally quite destabilising – to get them up back again.

On a slightly different topic, I noticed the other day that the Bank of Canada has a page on its website about the extensive research programme it is planning in advance of next year’s quinquennial review of the Canadian inflation target (a non-binding agreement reached with the Minister of Finance). The Bank of Canada has a strong track record of undertaking serious research in advance of these reviews. They plan to undertake significant work on each of the following three topics:

- The level of the inflation target

- Measuring core inflation, and

- Financial stability considerations in the formulation of monetary policy.

The first of these topics particularly caught my eye. As they note:

Canada targets 2 per cent inflation, the midpoint of a 1 to 3 per cent inflation-control target range. Since the last renewal of the agreement in 2011, the experience of advanced economies with interest rates near the zero lower bound has put the 2 per cent target under increased scrutiny. After taking all factors into consideration, the Bank will undertake a careful analysis of the costs and benefits of adjusting the target.

The process is an admirable one. I have previously urged that, with the next (legally binding) PTA due to be negotiated in New Zealand in not much more than 18 months that a similar, open, process should be getting underway here – commissioned jointly by the Minister of Finance, the current Governor, and the Secretary to the Treasury. That would be quite a contrast to the very secretive way these things are typically done in New Zealand – in the case of the 2012 PTA, secretive even after the event.

Doing the work is vitally important, but so is getting it out into the public domain and ensuring open scrutiny and debate of material that will influence the key document in short-term macroeconomic management for the next five years. It would be valuable at any time, but should be particularly so now, after years of undershooting the target, and as the near-zero lower bound moves uncomfortably close again. For example, with the benefit of hindsight was the move to a focus on the midpoint a mistake for New Zealand? I don’t think so, but in view of his track record the Governor may, and there could be reasonable arguments on either side of the issue – particularly in view of the potential interaction with financial stability considerations.

But what I thought was particularly praiseworthy was the Bank of Canada’s willingness to openly acknowledge that questions should be asked, in the light of changed circumstances, as to whether the 2 per cent target midpoint is still appropriate. The issues are a little more pressing for them than for us, since Canadian interest rates are much near zero than ours are, but we cannot afford to be complacent. And if it was decided that a higher inflation target was appropriate, the time to make that call is when there is still conventional monetary policy leverage available. I’d probably still prefer authorities to take serious legislative steps to remove the zero lower bound, but the questions and issues should be asked and examined. In New Zealand to date – including in the Bank’s Statement of Intent – the issues and risks are not even acknowledged.