When I heard yesterday that the now-former Economic Development minister David Parker had made an encore appearance to launch something called “From the Knowledge Wave to the Digital Age”, I wondered why he would want to remind anyone of the Knowledge Wave, a conference held under the previous Labour government in late 2001. Of course, my impression of that event was somewhat jaundiced by the fact that my boss, then-Governor of the Reserve Bank Don Brash, had made a “courageous” and somewhat ill-judged speech at the conference – against the advice of many of his senior staff, at least as to content – that with hindsight could have been read as an audition for his post-Bank forays with the ACT and National parties (although I’m 100 per cent sure it wasn’t intended that way).

But the bigger problem is that, for all the talk, all the ink spilled, at that conference and through the subsequent Growth and Innovation Framework nothing much changed for the better. The productivity gaps (New Zealand vs other advanced countries) didn’t start to close, the economy didn’t become more foreign trade (outwards and inwards) oriented, there were no fresh waves of greenfields FDI. Instead, we had a reasonably strong cyclical upswing (rapid house price inflation, general inflation showing signs of getting away)…..followed by a nasty recession and a sluggish subsequent decade.

David Parker gave a speech at the launch of what is supposed to be “the Government’s Industry Strategy”, and that is going to be my focus here. I haven’t read the full 50 page document, but I’ve skimmed through it and will include a few observations drawn from that.

Perhaps how people react to “Industry Strategy” is one of the ways one tells them apart. I was a bureaucrat for a long time (but in the era in which the Reserve Bank believed in letting markets work and eschewed direct government interventions as much as possible), but when I hear the words “Industry Strategy” my heart does not leap with excitement, rather I think of the Soviet Union, the eastern-bloc, the People’s Republic of China (that not-overly-productive middle income country), or even – more mundanely – New Zealand’s own past failures in this regard: plans and conferences and strategies, often with little to show for it (when we are fortunate) but often enough with white elephants to mark the landscape, or memories of money just poured down the drain. But I guess it is different in today’s Labour Party, or in today’s MBIE – the modern version of the Department of Industries and Commerce (too many in the National Party seem to have had the same inclinations). The government has a plan, a strategy – or a whole series of them – not for the economy as a whole (getting the basic structures right etc) but for individual industries. And, with little accountability and no market discipline at all, they are keen to use your money and mine to back those strategies, boldly going where private investors have, thus far, decided not to.

As often with David Parker, there are sometimes glimpses of recognition of real problems.

I believe there is no doubt we inherited an economy based on excessive property speculation and high rates of immigration driving consumption led growth. The latest OECD report on New Zealand confirms this.

The infrastructure deficit left behind – not just schools, hospital, roads and public transport, but also private and public housing – will take a decade to catch up.

This is serious, but the adverse effect on productive investment was also profound.

Low per capita investment in our productive businesses has inhibited the diffusion of technology, and the development of innovative new products and services.

I wouldn’t frame some of it quite that way (notably that Labour trope about “excessive property speculation”) but, broadly speaking, he isn’t wrong. Perhaps a shame there is no mention of the real exchange rate, at all, but it isn’t nothing.

The problem is, though, that this is buried deep in a speech which is mostly full of breathless energetic accounts of great things already done and great stuff the government (and industry) are about to do.

The flip side of the enormity of the 4th industrial revolution on the future of work, is the correspondingly huge potential for business.

It is an exciting time.

A myriad of new ways of new products and services are being made possible.

Most improve productivity.

Many are needed to decarbonise the world to avoid catastrophic climate change, or to combat pollution of our rivers and oceans. Others will overcome debilitating disease, improving the lives of millions.

I believe that it is the duty of every government to address both the future of work, and to maximise the up-side by chasing down as many of these commercial opportunities as we can, so as to harness the new jobs and value.

(I’m still old-school enough to think of outrages when I see the word “enormity” but let that pass).

Notice that second to last line, it is the “duty” of governments to “chase down” commercial opportunities. In part, presumably, because in the Minister’s view it is all some sort of zero-sum game.

It is a race. Others want the prizes that we seek.

Which isn’t the way most economists think of economic growth and development, perhaps especially not in a country that start so far behind the global productivity frontiers.

And then it just becomes completely delusional

Since the 1970s successive governments have wrestled with our productivity challenges; how we add value, upskill and diversify our economy.

We should acknowledge the important milestones and efforts of yesteryear.

They show that when we together have a plan and chart a direction, our economy strides forward.

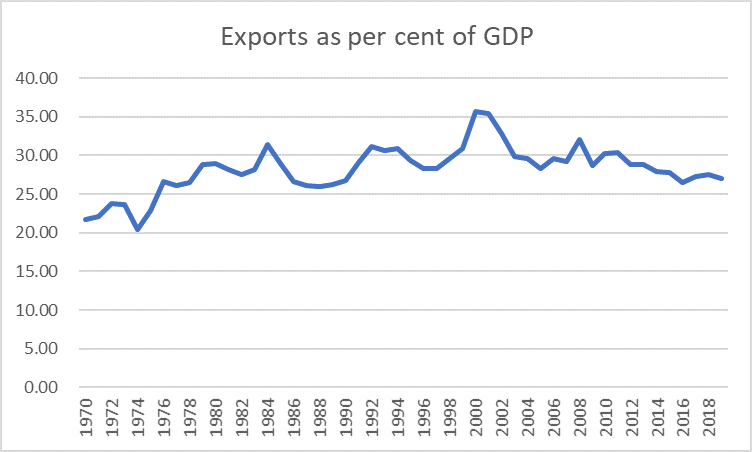

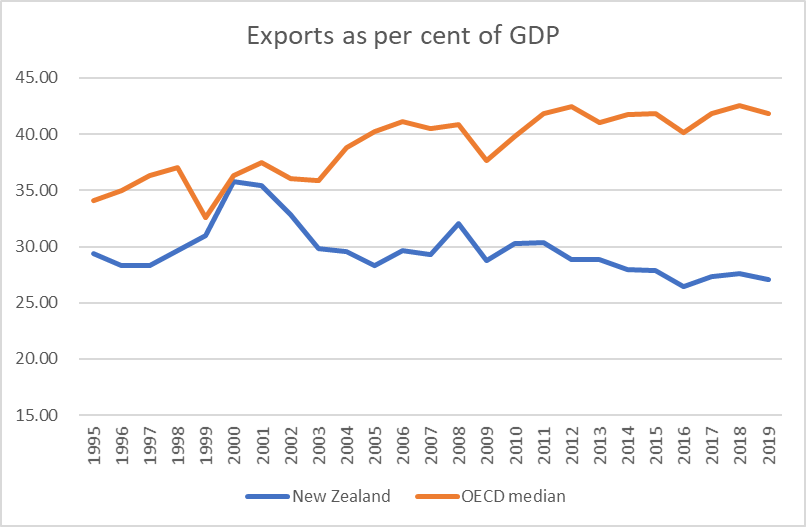

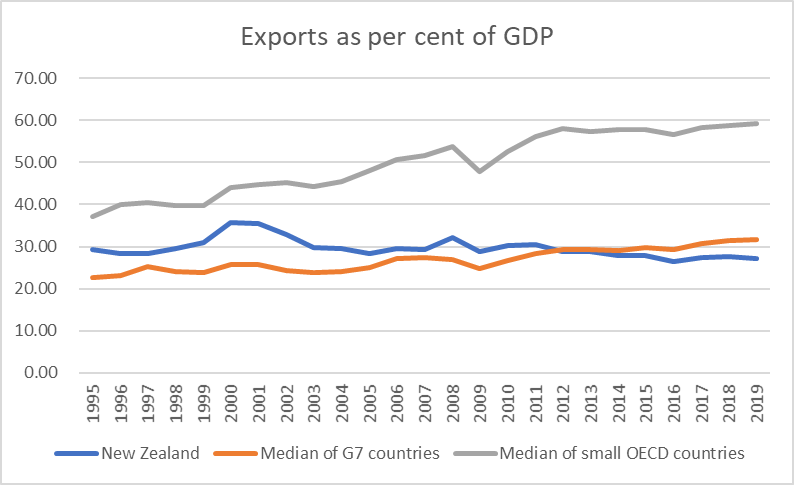

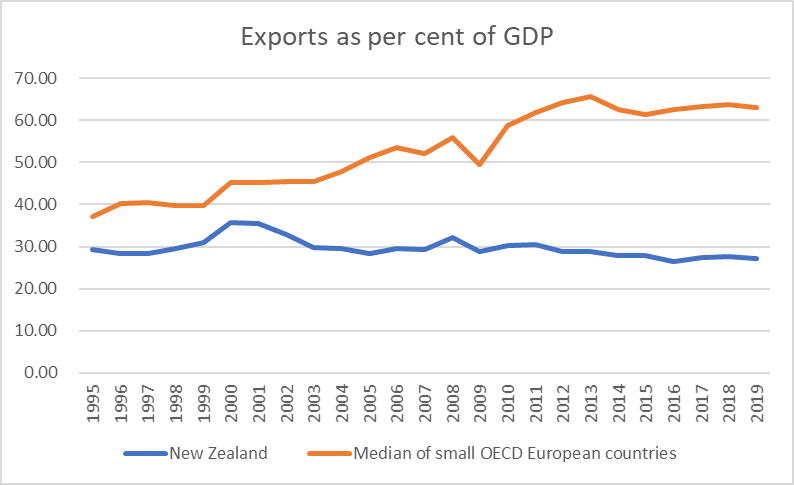

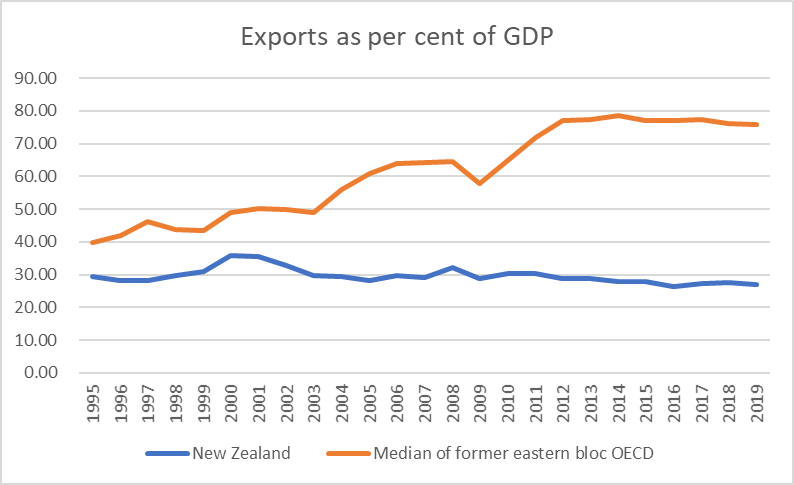

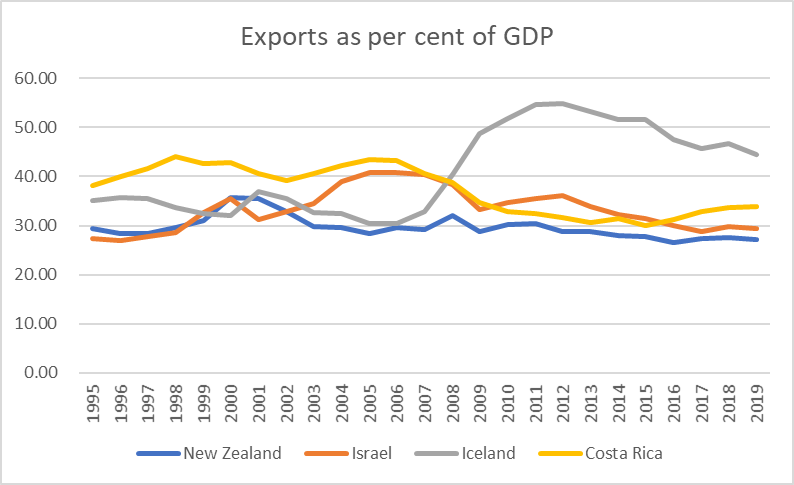

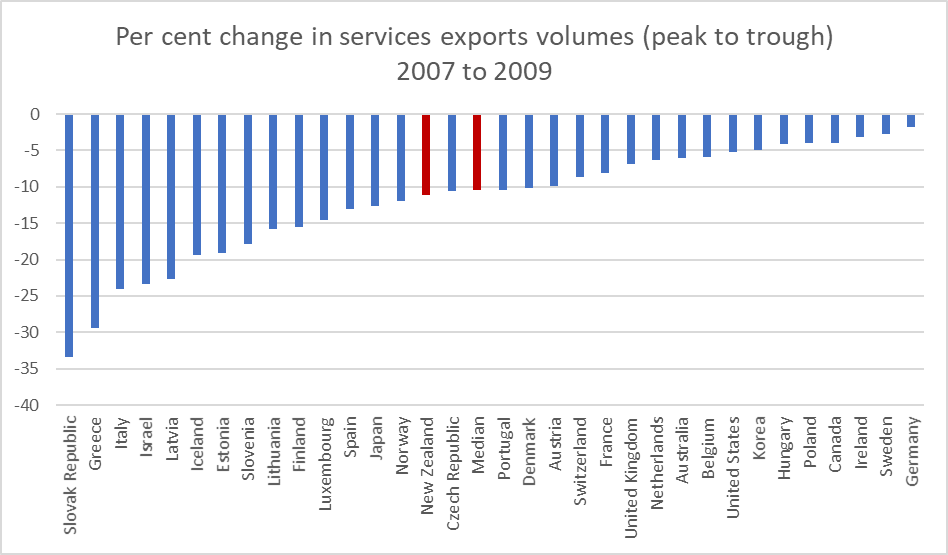

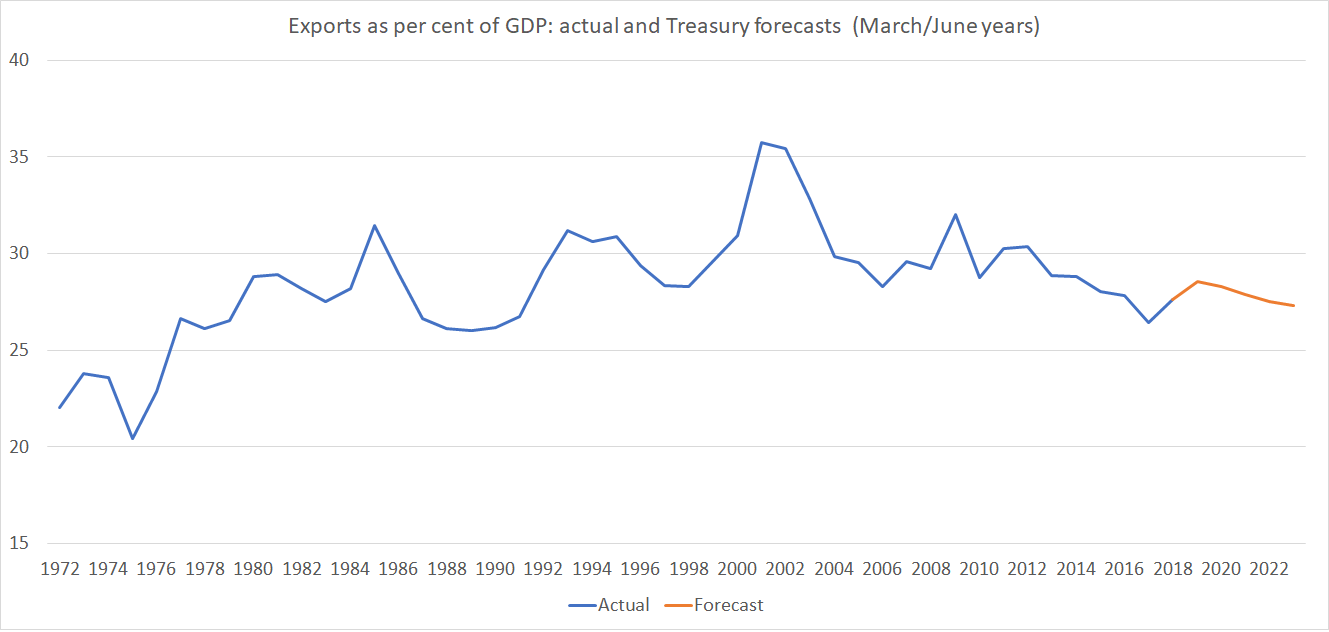

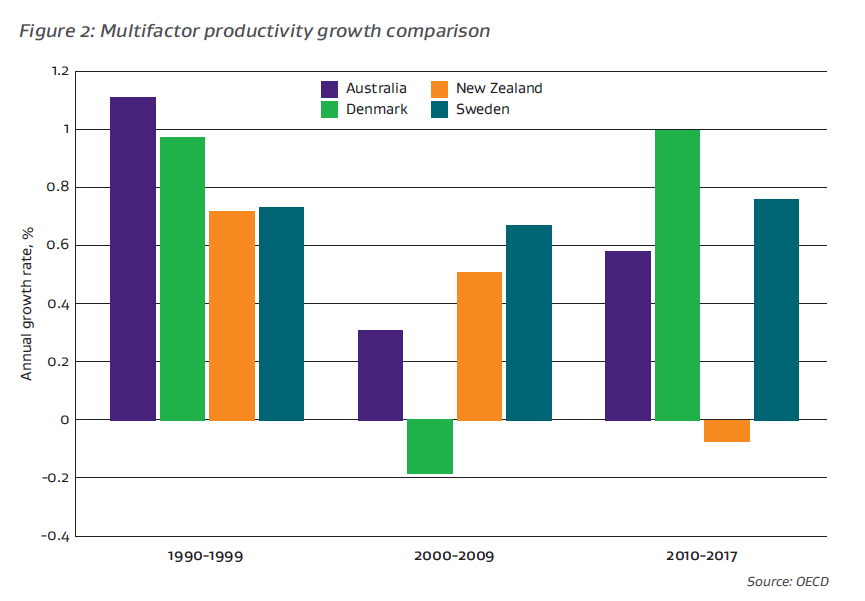

To repeat, there is no time in the last 46 years – say, since the UK entered the EEC (the Minister’s reference point) – when New Zealand has made any sustained progress in closing the productivity gaps to the other advanced economies. Instead, as I illustrated in Monday’s post, they’ve kept on widening. They are widening now, after five years – both governments – of no productivity growth.

Of course, the officials themselves know this – even if they squirm in their chairs – and, to his credit, Parker didn’t stop them including this chart in the fuller document.

It isn’t the chart I’d have chosen myself, but it makes the point nonetheless. And recall that all three of these countries were already materially richer, with higher levels of labour productivity in New Zealand, back in 1990.

In fairness, the Minister does have a place for the private sector

Government can direct investment towards the regions, and champion sectors where we see a comparative advantage, but it is the mobilisation of the private sector which delivers the jobs the big gains.

Better if they just left aside the picking winners – or even propping up losers – implicit in the first half of the sentence.

And this is where the Minister praises the Knowledge Wave and the Growth and Innovation Framework, going on to note

Our predecessors identified three priority areas. These were chosen because of their potential for export growth and because of the underlying importance that competence in the sector had to the wider economy. Spillover benefits.

The crucial sectors identified were ICT, biotechnology (with a food and beverage bent) and, thirdly, the creative sector and design.

They got it right and I am pleased to doff my cap to those who called it at the time.

Not that reference to export growth. We get this guff

Our telco competence is a considerable achievement, and a prerequisite to the development of Xero, Vista, Coretex and a myriad of other companies that sell software as a service, which have flourished.

And the other sectors have boomed too.

Fisher and Paykel Healthcare. A2 Milk and a range of other food and beverage companies. Weta Workshops and its spinoffs. Now household names. Billions of dollars in enterprises that have helped build our country.

The Growth and Innovation framework is the GIF that keeps on giving. Computer gaming, robotics, customer service avatars, nutrient monitoring software.

The race is on.

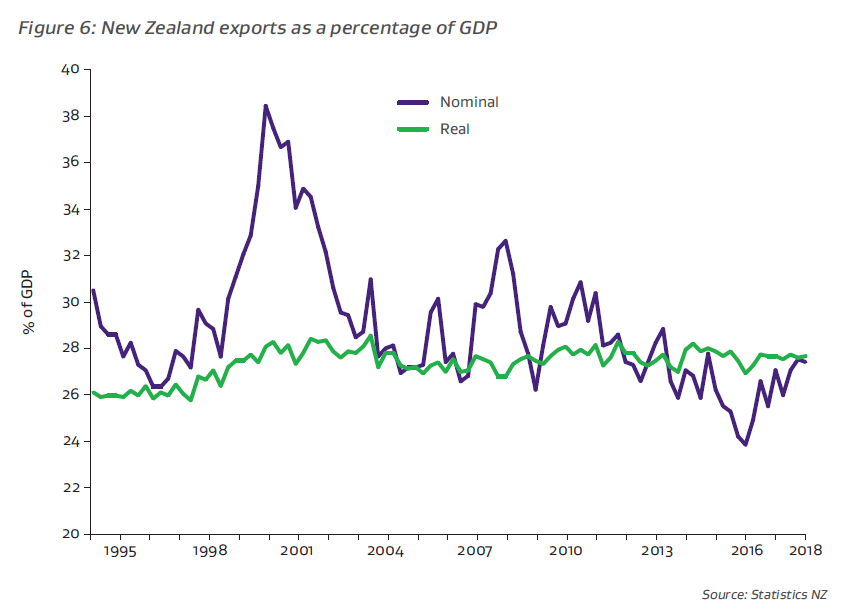

Our TIN200 companies are growing strongly, with technology exports now our third largest export sector (after tourism and agriculture). New hires abroad as well as export sales growth are described in the TIN200 report on the table.

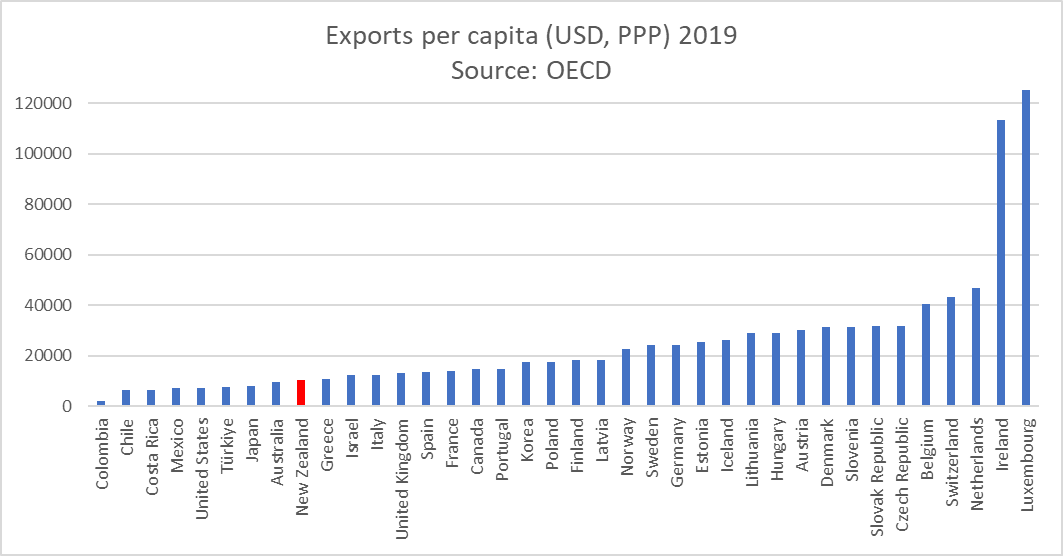

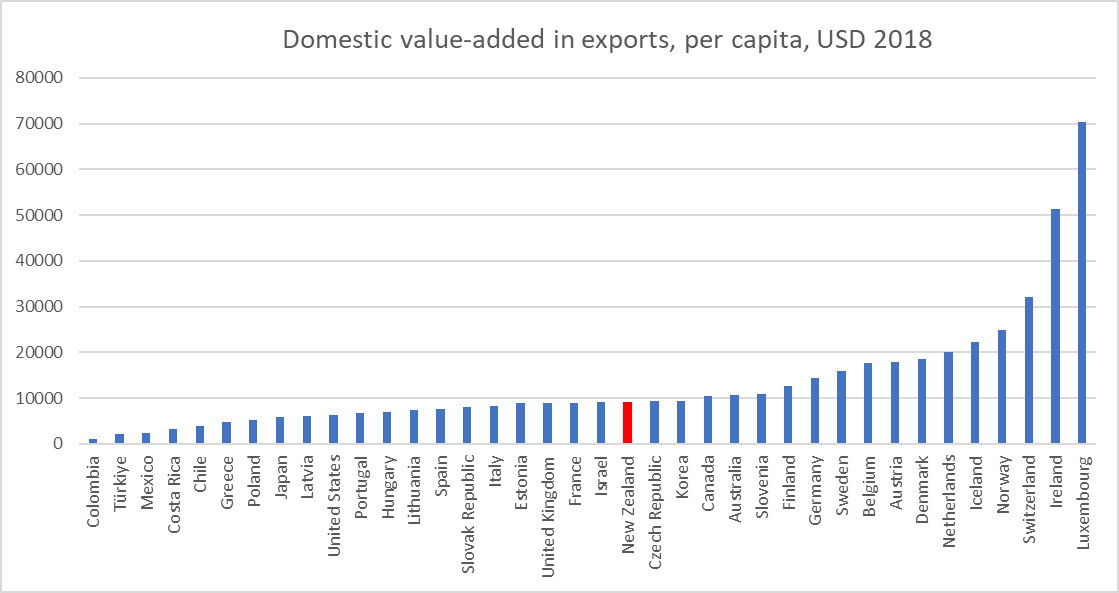

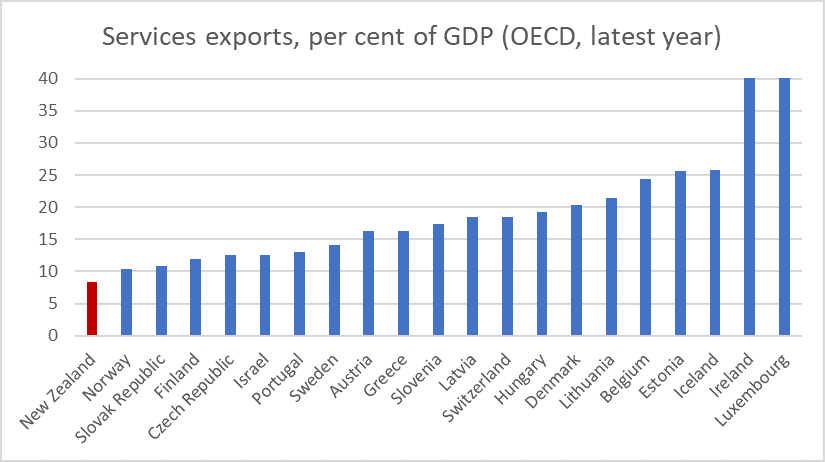

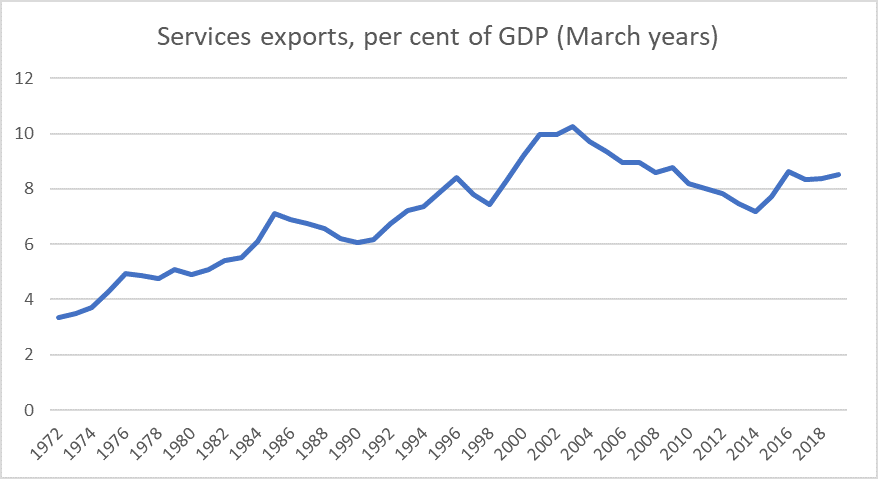

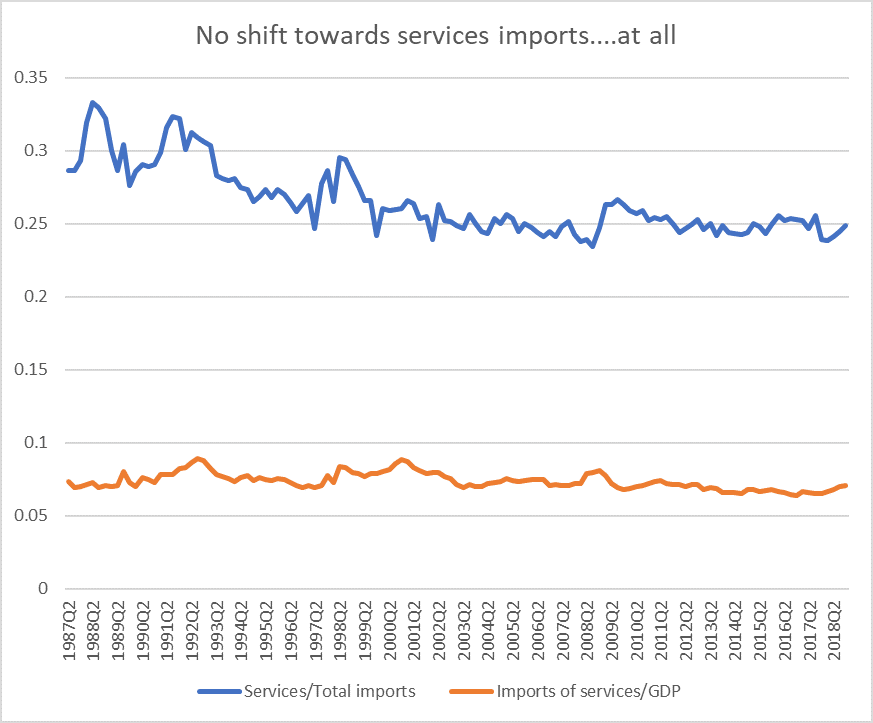

One can pick all sorts of holes in that (massive film subsidies for example, or the fact – as I’ve documented here before – that on no proper statistical definition of exports are “technology exports” “our third biggest export sector. But don’t worry about those sort of picky details. Wouldn’t the Minister’s text lead an uninformed reader to suppose that the outward orientation of New Zealand’s economy had markedly increased since the early 2000s? Nothing in the speech suggests otherwise, but (again) lurking in the full report was the sort of chart I run here regularly.

It just hasn’t happened. There are individual success stories, of course – as there have been throughout our history – but it doesn’t add up to much, when productivity growth has lagged further, and our export/import shares have gone sideways or downwards. That, apparently, was the legacy of those earlier planners (actually I doubt all their words etc added up to much at all).

But the Minister is breathless in his enthusiasm and goes on

Kiwisaver and the Cullen Superannuation Fund have deepened our investment skills and capital markets.

New Zealand Trade and Enterprise has been important in helping many exporters sector navigate their risky journey into new markets.

Our seed or angel investment capital market has matured. The innovation ecosystem has strengthened as management capability and globalisation ambitions have both grown.

We still suffer a gap in series A and B capital rounds, which this slide shows – something we have addressed in our latest Budget.

The $300m boost, and lead being shown by our largest NZ investor – the Guardians of the NZ Superfund – will attract private sector investment and help our firms to achieve their potential.

This will help to directly fill the current ‘capital gap’, and draw in other capital from NZ and abroad.

Give me leave to differ. National savings rates haven’t improved materially, whatever NZTE has done – let alone all those preferential trade agreements, which Parker is trying to negotiate more of – exports haven’t become a more important part of the economy, more firms aren’t showing they can foot it globally. And when you are reduced to lauding a government money-pot, with no market disciplines and little accountability, as your catalytic hope, it is all a bit thin, and worrying to boot. And I have no real idea what that final sentence means – but if he means low rates of business investment, in reasonably well-run countries, private firms will invest eagerly to take advantage of profitable opportunities, when they exist.

The breathless energy continues

There is no time for delay. The seemingly exponential growth in opportunities will within just a decade or two morph into the law of diminishing returns.

At one level its simple, if we want these innovative parts of the economy to grow faster, we have to apply more of our precious resources to the task.

Don’t ask me what it means, but it would certainly good if there was some serious recognition from the top of government that our economic performance has really been pretty lousy for decades and an evident determination to get to the bottom of why, rather than just trying to pick a few more “winners”.

The gush goes on, sector by sector (you can read it for yourself), but haven’t we heard it all before. They were probably discussing such things, enthusiastically, at the National Development Conference 50 years ago.

The speech ends with a full page on “Industry Transformation Plans”. I’m guessing they probably won’t come to much, so perhaps little harm done, except that more years pass, and more energy is devoting to avoiding the real issues. Here is a sample of the Minister’s great enthusiasm for what government can and will do with these plans.

These describe an agreed vision for the future of a sector, and set out actions required to realise this vision.

Industry Transformation Plans are in train across large sectors of our economy – in agriculture with the Primary Sector Council for example.

Our first Industry Transformation Plan was the Construction Sector Accord. It was co-developed by an industry Accord Development Group. Industry leaders working with the Government.

Our next Industry Transformation Plans focus on four other priority sectors: food and beverage, digital technology, forestry and wood processing, and – as I have said – agritech.

The Prime Minister’s Business Advisory Council and the Future of Work Tripartite Forum will provide strategic leadership.

Key components of each plan will include assessments of the opportunities and risks from digitalisation, the future of work and skills training.

Risk sharing between government, businesses and labour to enable skills training to upskill existing workforces will be crucial to avoid the rising inequality which will otherwise flow from the future of work.

Each plan will also set out decarbonisation pathways, ways to increase exports, as well as an assessment of capital constraints. Partnerships are needed.

Business, workers and government all have a stake in every industry and we need to partner to make a real difference for New Zealand.

It is almost literally incredible. The hubris, the lack of any apparent recognition of the limits of government knowledge, the complete absence of any sense of the benefits of vigorous competition, of creative destruction even, or market disciplines and so on. Bill Sutch might have been proud.

It is sad in a way. I suspect David Parker is better than this, and knows that this sort of stuff just isn’t likely to be any more transformative than the last (or first) wave of goverment talkfests. But when you aren’t willing to even think about tackling the real issues – the real exchange rate doesn’t appear in the 50 page document either – I guess you need a lot of sound and fury, lest – just a year out from an election – it look as if the government is doing nothing, has no ideas, or doesn’t really care. Sadly, all the talk is likely to signify almost nothing, in making a real difference, reversing the economic underperformance, and even building (in the government’s own words) “an economy that is more productive, sustainable, and inclusive for all New Zealanders”.