In preparation for a meeting earlier this morning, I’d downloaded the OECD data on exports as a share of GDP. I thought it might be useful to share of a few of the charts. Most are updates of charts I’ve shown in years gone by, but it is good to be reminded of what has happened in New Zealand and how we compare with other OECD countries. In all the charts that follow I’ve excluded 2020 for two reasons: first, not all countries yet have data (at least in this database) and second, Covid, which affected individual countries quite differently and which should over time prove to be a blip. In all the charts other than the first I’ve shown data from 1995, which is when the OECD has complete data from.

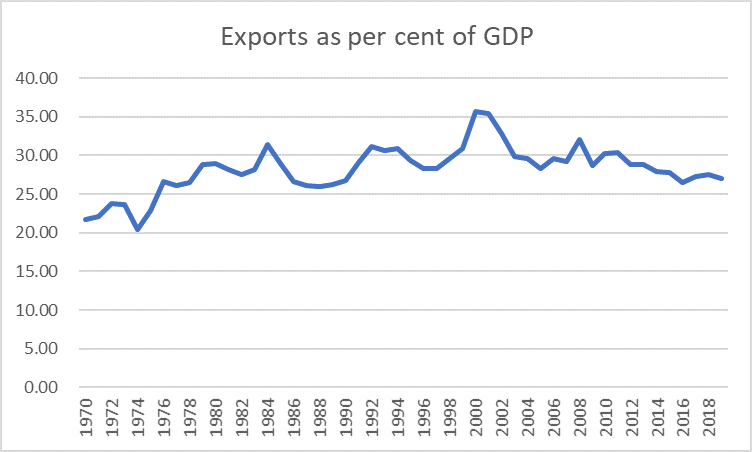

Here, as context, is the New Zealand data since 1970. 1995 was not an outlier, high or low.

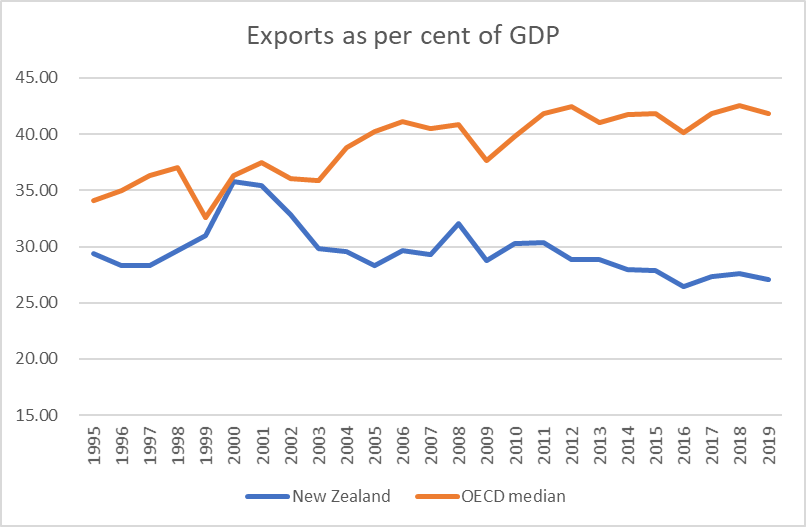

Here is New Zealand relative to the median of all OECD countries (note that the OECD keeps doing its best to keep us near the more prosperous part of the OECD, by letting in new poorer countries: the latest country invited in (and now in the data) is Costa Rica).

From the beginning of this chart, we’ve always exported a smaller share of GDP than then median OECD country has, and that gap has widened.

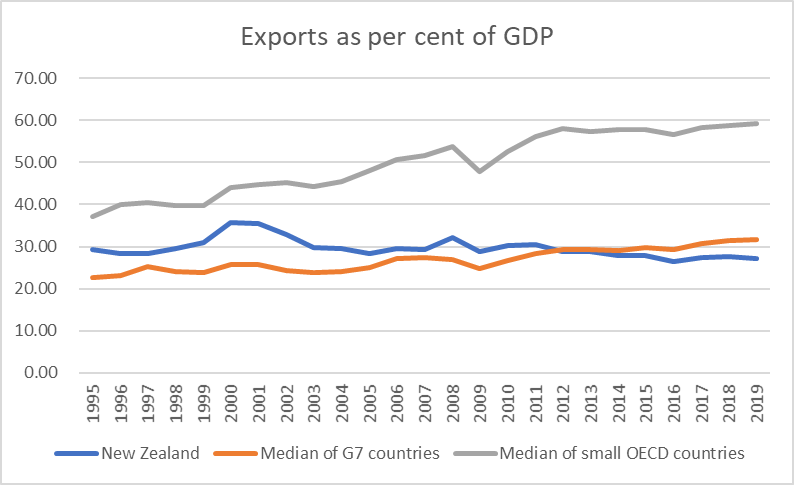

But, of course, one could expect the picture for other small countries to look different than one that included large countries. All else equal, large countries tend to do a smaller share of their GDP in foreign trade, just because there are relatively more opportunities at home (in the US, at one extreme, exports are equivalent to 12 per cent of GDP).

So in this chart I’ve shown (a) New Zealand, (b) the median for the G7 (larger) countries, and (c) the median for the small OECD countries (Belgium on down).

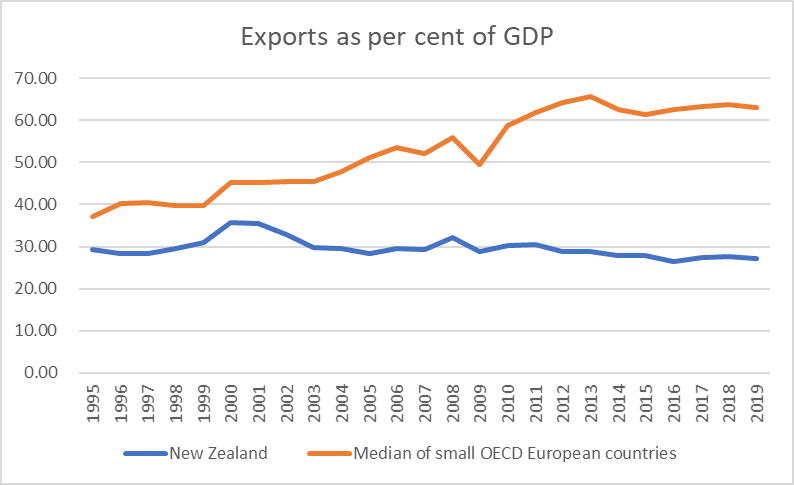

And in this chart I’ve shown New Zealand against the small European countries (including Iceland).

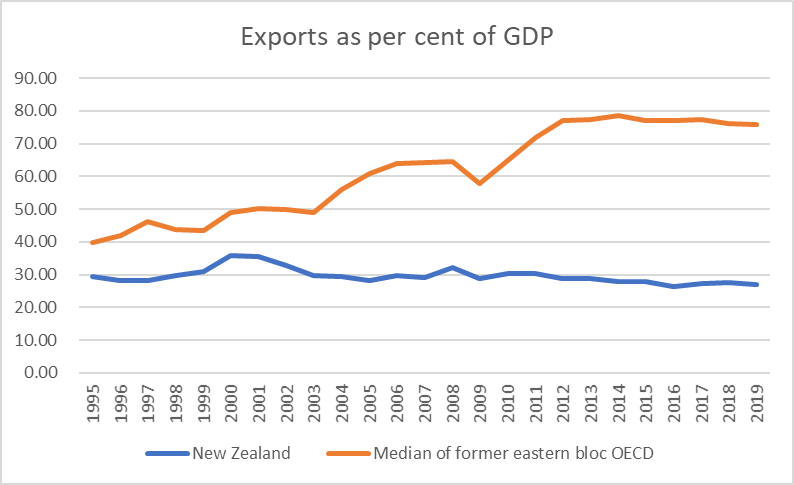

And New Zealand against the former Communist countries of eastern and central Europe, all small except Poland.

These central and eastern European countries, all part of the EU, and often closely into supply chains for things like the German car industry, have been managed significant productivity growth, closing the gaps to some extent with the OECD leaders, over the last couple of decades.

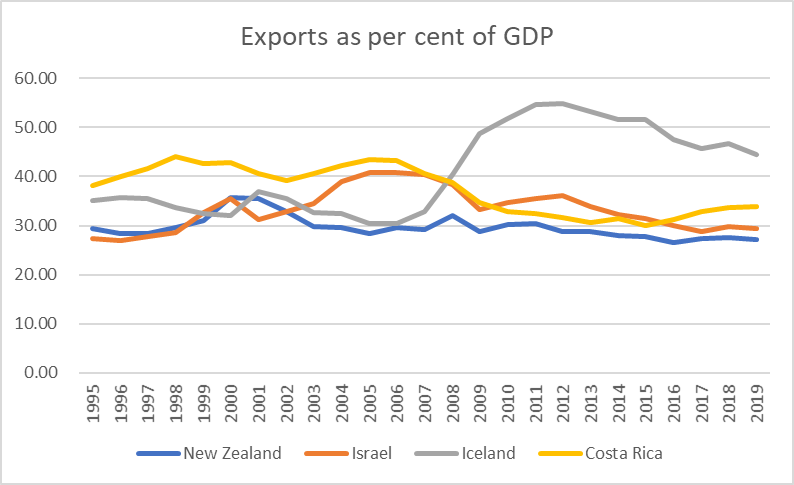

There aren’t that many OECD countries that are both small and remote. In many respects both Iceland and Israel count, Costa Rica does, and so does New Zealand. Here are the records of those four countries.

I’ve been increasingly intrigued by Israel which for all the reputation it has for high-tech industries, has done about as badly as New Zealand. Israel has a similar (modest) level of real GDP per hour worked to New Zealand and – coincidentally or not – has had very rapid population growth.

People are sometimes inclined to discount the central and east European story, noting (correctly) that the gross exports numbers used here don’t represent the extent of value-added in the respective economies, and thus may overstate the apparent success.

The OECD reports data on the extent of domestic value-added in gross exports, but only with a lag. The most recent data are for 2016 and that year two thirds of the exports of the median eastern/central European OECD member were domestic value-added, little changed over the previous decade. In New Zealand, by contrast, domestic value-added accounted for 87 per cent of total exports in 2016. The gap – between the export performance of New Zealand and that of the central and east European countries – is (very) real.

As I’ve said often here, exports are not uniquely special – indeed, I could have done the charts of imports and most of the pictures would have been quite similar – but that successful small economies (fast growing productivity growth ones) tend to be ones generating (or attracting) companies that find plenty of buyers for lots of their output abroad as well at home. That simply does not describe the New Zealand experience.

How do we improve our productivity though? I mean the government’s answer to a low wage economy is to increase the minimum wage. None of the oppositions seem to have any good ideas either. We need an inspirational leader, can’t see anyone in the horizon.

Is it our culture? Are we too laid back, and tall poppy syndrome?

We never hear anything about productive in the media. But how do we change that?

LikeLike

Various of my papers and speeches on this and related topics are here

https://croakingcassandra.com/papers-and-speeches/

including https://croakingcassandra.files.wordpress.com/2017/09/large-scale-non-citizen-immigration-to-new-zealand-is-making-us-poorer-mana-u3a-sept-2017.pdf and (a longer version of a chapter in a recent book)

also this post https://croakingcassandra.com/2018/05/25/lifting-productivity-what-id-do/

and this

Click to access psn-lecture-series-lifting-productivity-for-our-kids-sake-may-20181.pdf

Entirely agree with both halves of your sentence on an “inspirational leader”.

Click to access an-underperforming-economy-the-insufficiently-recognised-implications-of-distance-draft-chapter.pdf

LikeLike

SYA, the economic productivity equation is quite simple. Every automated factory that is shut down is a loss in productivity. Every cow we add to our already 10 million cows increases productivity because cows are not counted in the productivity equation. 10 million cows produce a GDP of around $18 billion but is still considered more productive than the 1.5 million Aucklanders that produce a GDP of $80 billion because we count only people and not animals in our economic productivity models.

LikeLike

I found this yesterday

LikeLike

Overall, in the short-term immigration probably also boosts wages (not cuts them as noneconomist commentary often suggests) for much the same reason. But if that is true in general it isn’t true in every sector: if lots of lots of immigrants are recruited to particular sectors (thin dairy, or aged care,) that is likely to lower relative wages in that sector.

………….

So that’s why Arthur Grimes says it doesn’t lower wages? However David Williamson says real wages fell 24.5% in tourism and hospitality between 1979 and 2006. He says it is an ongoing problem no one wants to talk about. This sector (was) our second (?) biggest “:pie”. What’s more at the other end property prices rose. They are either acutely aware that people resent the disruption to their neighborhoods (of government policy) or can’t accept the need for sprawl or don’t want to bite the bullet re infrastructure spending?

Intuitively Ha-Joon Chang is correct when he says it is simply borders that control the market and that (mostly) explains why a Swedish bus driver earns 50 times more than an Indian?

I think he means also that we are fortunate to be born in countries with good institutions and practices built up over generations but (I assume) he is making a people to resources argument?

LikeLike

Many of the papers on immigration/wages look at wage developments given the wider economy (eg the Mariel boatlift studies). NZ immigration is macroeconomically significant, and one can’t take the rest of the economy as given. But even then the near-term demand effects and any supply effects can work in opposite directions: the higher demand (economywide) that a positive migration shock gives rise to will tend to lift economic activity, employment, and wages in a 1-3 year horizon (that is a standard RB finding for NZ) even though in the longer-term (my argument) in a NZ context high immigration may have dampened productivity growth and thus reduced the size of the future pie (whether distributed to capital or labour).

LikeLiked by 2 people

Immigrants may not lower wages but at the same time the type of jobs created may lower GDP/capita?

House prices are a form of inflation even if they aren’t called that. If you can’t or are unwilling to keep house prices down while large numbers arrive, effectively, that lowers the real wages of those who don’t own a house?

LikeLike

Paul Krugman

https://krugman.blogs.nytimes.com/2006/03/27/notes-on-immigration

LikeLike

the primary reason why Sven is paid fifty times more than Ram is that he shares his labour market with other people who are way more than fifty times more productive than their Indian counterparts. Even if the average wage in Sweden is about fifty times higher than the average wage in India, most Swedes are certainly not fifty times more productive than their Indian counterparts. Many of them, including Sven, are probably less skilled. But there are some Swedes — those top managers, scientists and engineers in world-leading companies such as Ericsson, Saab and SKF — who are hundreds of times more productive than their Indian equivalents, so Sweden’s average national productivity ends up being in the region of fifty times that of India.

Ha-Joon Chang 23 Things They Don’t Tell You About Capitalism – Thing 3

LikeLiked by 1 person

Those large Swedish factories are highly automated with very efficient industrial robots. The more robots the higher the productivity. Indian factories are labour intensive and therefore less productive.

LikeLike

This really surprised me. I’d always accepted the idea that NZ’s was an “export-led economy”.

For clarification, can you confirm whether exports here includes or excludes tourism?

It would be fascinating to see the same analysis featuring government expenditure in place of exports.

LikeLike

Yes, the data are goods and services exports so includes tourism.

Go back 100 years and the “export-led” story had been true – the new technologies etc that enabled large scale meat and dairy exports. In recent decades it has been more a case of the underperforming state of exports (in aggregate) is just another indicator of how disappointing our overall economic performance has continued to be, with average productivity gradually slipping further behind OECD leaders (US and NW Europe), and the catch-up economies of central/eastern Europe that in modern NZ history until now had never been as rich/productive as NZ, and are now going past us. in some cases at quite some pace.

LikeLike

And presumably – to some degree – population growth increases the relative size of the internal economy.

LikeLike

It is true that whatever food products we produce, 95% is exported. Look at the recent tomato prices at 8 cents a kg. The drop mainly due to inability to get that produce to our export markets due to covid. Even our multi billion dollar gaming and space industry are all for the export market.

What fascinates me is that whatever we export even though tiny in the context of our total domestic economy are sought after by the international markets providing fundamental support for the NZD. The NZD continue to rise in value and is the 11the most traded currency in the world. That increasing NZD allows us to buy any product in the world without actually selling anything much.

LikeLike

incidentally, the OECD data go back to 1970 for the older advanced countries. Back then we were the median advanced country in terms of exports/GDP. Our heyday was really pre-WW2, and if you read older books from early in the century they talk of NZ having among the very highest exports per capita of any country.

LikeLike

And presumably – to some degree – population growth increases the relative size of the internal economy.

LikeLike

That is the gist of my story about NZ: rapid policy driven population growth to a land with (as it appears) few econ opportunities so our overall economy is skewed inward. A bit different in Aus, with a similar population story, but lots of newly developed mineral resources to bring to market.

LikeLike

After reading the papers you recommended, I realised I was the problem (I came to NZ 20 odd years ago when I was a teenager). Then I thought besides of getting rid of myself, is there no other solution/pathway? So I have more questions:

1. Labour campaigned on lower immigration. Why are they not doing it? Especially when Winton was there last term. What was the hold up?

2. A lower population means a smaller domestic market. Would that have negative impact on our overall efficiency, and push us further down the supply chain?

3. Although most of our export is location specific and fixed natural resources, we can still try to add value to them prior to export. Should we have policies in limiting raw material export, and subsidising local value added businesses?

4. With less migrates and low birth rate, will we have more problems associated with aging population?

5. Will remoteness always be a problem for NZ, even with the fast developing of technology?

Use myself as an example, never had a day of free education in NZ (paid international fees), straight into working after graduation. Had been on top tax rates most of my working years. Always had private insurance, so I won’t be a burden to other people if I am sick or dead. I hate to think I was dragging down our national productivity level. But if nothing works, I can always move myself out of NZ.

LikeLike

Interesting questions (and I should always stress that the issue is the NZ govt’s policy, not individuals).

On your question re Labour, their suggestions of reduced immigration were always mostly smoke and mirrors https://croakingcassandra.com/2017/06/13/two-sides-of-the-same-coin/ and that policy pre-dated Ardern’s leadership and apparently she was never keen on it.

on question 2, yes it would mean a slightly smaller market, but relative to the wider world markets that would be opened up in the process (thru a lower real exchange rate) this need not be an undue problem. Very small countries, eg Iceland, manage to be very prosperous,

3. We shouldn’t have regulatory restrictions requiring valued added, but if we get the policy framework right where such value-added makes sense (done locally) it will increasingly tend to happen here.

4 The “problems of an ageing population: are usually greatly exaggerated. from the fiscal side, they are best dealt with by raising the NZS eligibility age – but that should be done anyway – and in many areas technology can substitute for labour over time (and that will tend to happen if labour costs rise as productivity increases).

5. “always: is a long time. Perhaps one day it won’t be such a barrier, but we can’t plan on that wishful thought, As it is, all indications are that personal netowrks and connections are perhaps more important now – with more complex products and services – than they were 100 years ago, and for now the flight to London is still 24 hours and the attendant jet lag. There is a lot that can now be done electronically, as people have discovered even more in the last year, but there is little sign yet that it is sustainably shifting econ activity away from those concentrated locations (whether in NW Europe, N America or increasingly in East Asia).

And don’t leave. We need people who are already here, with all the talents they brought and have developed to help make the most of the place from here forward. Having said that, as you’ll have noticed from my papers I put quite a lot of weight on the exodus of NZers over the decade, judging that the opportunities for them and their children are better elsewhere. And much as I would be personally sorry to see them go, I’m not sure I would necessarily encourage my kids to stay here, if economic opportunities mattered to them and their kids.

LikeLiked by 1 person

Michael, this speaker is a migration booster but he has some interesting things to say to the ANZ School of Government – public service.

1. Immigration is left to the market – the fifth pillar of a market lead economy. Universities are one drivers of demand.

2. Very large numbers of Indians and Chinese who escape degraded cities and population.

3. Unlike in the past where migrants started at the bottom and worked their way up these are starting at the top in social status.

4. As the population increases livability degrades, however the migrants who start at the top don’t notice it.

5. eventually they have to catch up with infrastructure.

6. Gets into livability being spread out, whereas too dense leads to crime.

Unfortunately there are gaps which where the recording appears to have been wiped. I wonder if this means “redacted?”

LikeLike

Today’s BBC website has finally caught up with the issue of house prices in New Zealand with $1 million + being quoted for “dungers” and 40% of house sales going to investors. Is the country turning more into haves and have-nots? Who can afford those prices? Brian Kelly

On Wednesday, March 31, 2021, croaking cassandra wrote:

> Michael Reddell posted: ” In preparation for a meeting earlier this > morning, I’d downloaded the OECD data on exports as a share of GDP. I > thought it might be useful to share of a few of the charts. Most are > updates of charts I’ve shown in years gone by, but it is good to be rem” >

LikeLike