The Deputy Prime Minister and Minister of Finance hit the weekend current affairs shows to make the case for the government’s housing/tax package.

I watched both the Newshub Nation interview – the one in which the Minister of Finance refused to rule out bringing in rent controls (a move which would, among other things, simply accelerate a trend towards the government itself being the main provider of rental housing) – and the one on Q&A. Perhaps because the latter is fresh in my mind – I only watched it this morning – but also because it was a better interview, I want to focus here only on the Q&A interview. For those who haven’t seen it, the whole thing seems to be available here. Incidentally, it was interesting that the government chose not to send out its Minister of Housing for these interviews.

What I found most striking was how this very senior minister, now with 3.5 years in office under his belt, floundered when asked about the effects of the government’s measures. It wasn’t, apparently, for him to say what the effect on house prices would be. Not only that but officials had apparently offered quite a range of views, (if so suggesting they didn’t really know either). He didn’t know what the effect would be on private rents either. This was, we were told, “highly contested territory”. Really all he was willing to say was that any effect on house prices would be to moderate the recent pace of increase, which he kept calling “unsustainable” – without apparently recognising that things that are unsustainable typically come to an end anyway. So if annual house price inflation slows to only 10 per cent per annum this year – under the influence of all sorts of possible influences – will the Minister of Finance be claiming this as a win for last week’s package? I don’t any serious analysts, let alone potential first-home buyers, will be. The Minister meanwhile claimed only to want to see an end to the “big big jumps in house prices”.

If you were a serious government, mightn’t you have adopted a package that you – and ideally your officials too – were confident would lower both house prices (actually the bundle of the house and the land under it) and private rents? After all, New Zealand real house prices have more the tripled in the last 30 years, and yet houses are little more than a combination of land (abundant in New Zealand), labour, and a bunch of tradables materials (timber, taps, pipes, gib board etc). General tradables inflation has been – as the Reserve Bank often points out – quite a bit lower than general CPI inflation for a long time. There aren’t any natural obstacles to (much) lower house prices. Just policy ones.

Or what about rents? Real rents fortunately have not tripled. The current SNZ rents index has data since 2006

| Total percentage increases | ||

| Rents-stock | CPI | |

| 2006 to 2010 | 12.2 | 13.1 |

| 2010 to 2015 | 16.3 | 5.4 |

| 2015 to 2020 | 17.7 | 8.4 |

| Full period (06 to 20) | 53.2 | 29.2 |

So that is about a 20 per cent rise in real rents over 14 years, which might not sound so bad, except that over that period one of the key drivers of equilibrium rental yields – long-term interest rates (which are not only a financing cost but, more importantly, a return on a key alternative asset – have plummeted. Real 10 year government bonds yields were about 3.3 per cent at the end of 2006, 2.2 per cent at the end of 2015, and about -0.3 per cent at the end of last year. Rental yields have plummeted – and as the data show tenants have benefited from that – but real rents have not, because successive governments have adopted policies that drove real prices sharply up.

And don’t go blaming interest rates for the house prices, as the Minister tries to do (waving his hands and suggesting here are lots of things outside his control). Did you know that, even now, real interest rates in most of the advanced world are even lower than those here (in the US, for example, the real 10 year government bond yields is about -0.7 per cent)?

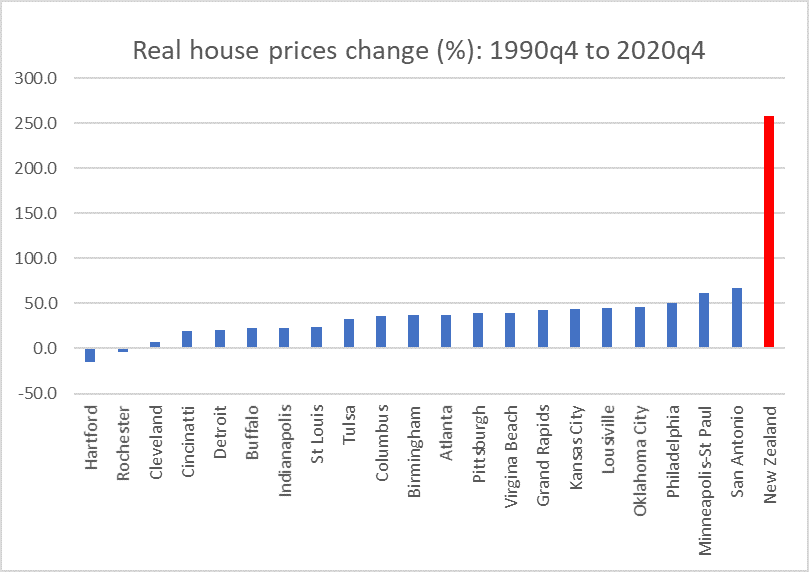

And, talking of the US, this is real house price inflation in (a) New Zealand as a whole (cities and towns and villages) and (b) the 20 or so metropolitan regions all with populations in excess of a million people that had house price to income ratios of less than 4 in the most recent Demographia report. You might not want to live in some or even most of these places, but plenty of people do (from memory, population growth in Columbus and Atlanta for example has exceeded that of New Zealand).

Of course, there are other US metropolitan areas where the picture has been less good, a few even where prices have been allowed to get as out of hand as they are in New Zealand. But in a sense that is the point. The entire US has the same interest rates – typically a bit lower than those in New Zealand. The entire US has much the same banking system, and even the same odd federal interventions in the housing finance market. The tax systems are much the same across the country. But the house price outcomes – even for similar population growth rates – differ hugely, consistent with a story about the importance of land use restrictions.

One might tell a similar story in Canada where the Demographia report has data for price to income ratios for six metropolitan regions each with a population of more than a million people. Same interest rates across the country, and fairly rapid population growth in both Toronto and Edmonton, yet Edmonton and Calgary have price/income ratios around 4 and Toronto and Vancouver 10 and 13 respectively (Ottawa and Montreal between 5 and 6).

So this should have been perhaps the cheapest time in history (rents relative to income) to be renting – here and abroad – and yet real rents have been rising, and the government cannot even manage a package that they, and their officials, are confident will lower rents. It really is hopeless.

In both weekend interviews the Minister did say that he would like to see the price/income ratios fall (suggesting that on a nationwide basis that ratio is now about 8. But even then, pushed by the interviewer, he wasn’t going to be pinned down or offer any hostages to accountability. He has “no number in mind”, said he “can’t tell what an affordable price is”, and butted away the interviewer’s suggestion that a ratio of 3 was not a uncommon benchmark in discussion of these issues, and wasn’t even willing to suggest that a ratio of 5 might be something to aspire to. He played distraction by suggesting that he would like to see incomes rise – which, of course, would lower the ratio – but has no policy to do anything about changing (improving) the future path of average/median income growth.

On Twitter on Saturday I did a quick exercise and pointed out that if house price inflation slowed to a long-term average of 1 per cent and incomes rose 2.5 per cent it would take almost 20 years for the price/income ratio to get to 6.

In the longer-term, incomes are likely to be driven by trends in nominal GDP per hour worked. That won’t be the only influence – people can work more (or fewer) hours, governments can run deficits in ways that put more in household pockets (or surpluses that take more out of household pockets), and relative returns to labour can change. But over a 20 year sort of horizon, nominal GDP per hour worked seems like a reasonable starting point: in New Zealand, the labour income share hasn’t changed much in 30 years, and while this government is doing a bit more redistribution governments come and governments go.

Nominal GDP per hour worked in turn reflects three broad factors:

- general inflation (eg something like the CPI)

- changes in the terms of trade

- productivity growth (change in real GDP per hour worked)

The Reserve Bank has an inflation target of 2 per cent, which it hasn’t consistently met for a decade, but it is probably reasonable to think of something a bit above 2 per cent as towards the lower end of what average incomes might grow at over several decades. On other hand, productivity growth in New Zealand has been lousy for a long time, and nothing in what this government is doing – or what National is offering instead – looks set to improve that. And the best guess of a future real relative price like the terms of trade is today’s value. So I’ve done scenarios in which incomes rise anywhere between 2.25 per cent per annum and 3 per cent annum. Over 20 years, actual could still be better or worse than those numbers, but they seem like a plausible range. Over the last five or six years, actual growth averaged about 2.6-2.7 per cent (whether or not 2020 is included).

What about house price growth. Robertson and Ardern refuse to even talk about flat house prices, let alone falling ones, so I’ve used 1 per cent per annum as the lower end of the range of scenarios. And I ran the numbers for 2, 3, and 4 per cent. 4 per cent house price growth wouldn’t seem super low to most New Zealanders after the experience of recent decades, but there is no point running higher house price inflation scenarios because…….even at 4 per cent annual house price inflation price/income ratios keep rising forever.

If house price inflation slowed to 1 per cent per annum, year in year out and incomes rose by 2.6 per cent per annum, in 20 years time the nationwide price/income ratio would be 5.85.

If house price inflation averages 2 per cent per annum, and incomes rise 2.75 per cent, in 20 years time the price/income ratio is still 6.9 per cent.

If house price inflation and incomes grow at 2.5 per cent…..then of course, the price/income ratio never falls at all.

And it is no trouble at all to generate undemanding scenarios in which the price/income ratio just keeps lurching upwards – these things never happen steadily (every single year), but the long-term trend is what dominates.

And if by some chance you think a price/income of 6 doesn’t sound too bad. well (a) you’ve just too used to latter day New Zealand, and (b) check the table on page 15 of the Demographia report for the metropolitan areas (most of them) with ratios lower than 6, in lots of cases much much lower. New York – never really thought of as a cheap place to live – shows at 5.9, Montreal at 5.6, Manchester (UK) at 4.8, Nashville at 4.2, Edmonton at 3.8, and on downwards.

But the government has simply done nothing about freeing up the land, facilitating again aggressive competition among potential vendors on the periphery and in the intensifying centre and suburbs, which is the sure and reliable way of getting house prices (land prices) and rents down. And doing so quite quickly, because although it takes time to build, it takes very little time for expectations to change, and markets trade on expectations.

I could go one, but I won’t except to highlight the Minister of Finance’s desperate attempt to defend the spin – the lies really – that claimed that interest deductibility for rental property owners was a “loophole”. The interviewer challenged Robertson on whether the government would be removing deductibility for all businesses, and Robertson denied that was on the cards while doubling down on his loophole spin, claiming that property was a loophole because owner-occupiers couldn’t deduct their interest cost. Not even bothering to get into the point that the owner-occupier has no assessable income from the house (and under the government’s ringfencing change a couple of years ago could get no benefit from deductibility anyway), the interviewer asked the Minister about the purchase of a computer. The financing costs of such equipment (or a car) are deductible for businesses, but not for households. Was this a distortion the Minister was asked. He was floundering by this point simply reduced to asserting again that there was a “loophole” when it came to property. Only in the fevered imaginations of ministers and their spin doctors (and even they no doubt know better, they just take the public for fools).

It really was a poor performance by one of the government’s most senior ministers. And in that sense told you really all one needed to know about last week’s package: utterly unserious when it came to addressing the core issues (land use, and probably some construction cost issues thrown in) but simply a heavy dose of the politics of distraction, all while further messing up the tax system and the housing market itself.

(And lest anyone suggest this is partisan commentary, the unnatural disaster of the New Zealand housing market has been the responsibility of successive governments led by each of the main parties. But when you hold office you hold responsibility. Ardern and Robertson have held office for 3.5 years and now have a parliamentary majority that – for good or ill, per the New Zealand system and its limited checks and balances – would allow them to do almost anything they wanted. But they refuse to do anything that would, with confidence, lower house prices and rents, or to even suggest that lower house prices would be a desirable outcome. There are words for that sort of political betrayal. Mostly not terribly polite ones.

I own 8 properties in Auckland. I have already taken steps over the past few days to prepare to sell two of my 3 bedroom houses to pay down debt and get myself safer from more changes. I won’t be the only one, and these two will likely be lost to the number of rentals available. The net result of this policy change will be to reduce the supply of rental properties and over time push up rents until the market reaches a new equilibrium.

LikeLiked by 2 people

You are doing what the government was hoping for – reducing your debt and releasing a property now likely to be purchased by a FHB (who might also be renting presently and thus releasing another rental property to the market). But yes, if the net result is fewer rentals, the government really needs to step up its state-house building program. And they know they need to do that regardless of these changes.

LikeLiked by 1 person

FHB without kids quite commonly share a house with others while renting as an economy measure while saving – so if they become FHBs then that will in many cases result in a lower occupancy of housing – increasing the number of houses needed.

LikeLike

But which will not add even one house to the total housing pool – all it is doing is shuffling the pack between renting and ownership.

LikeLike

I hold 11 properties. I will not be selling any properties. But I may look at swapping a existing apartment unit to a brand new build as new builds are exempt from the new tax changes.

I will also be releasing some tenants from some properties into development properties to allow for full deductibility as a development property. The 4 years phase out does give me some time to give notice to my existing tenants and to start planning and consent processes towards a development.

LikeLike

Hey Mike, interesting to have a real world situation; can I ask – what are you solving for as part of your decision? (e.g. cash flow neutrality?); sure there are a few moving parts – a rough calculation suggests 50-60% LVR range is about cash flow breakeven…??

LikeLike

But it is not about break-even for me JMK. I am retired and support my family on the after tax income (which goes from 33% to over 50%). I am only 35% geared but these two properties are cash-flow neutral, and will be net negative $12,000 once the new tax kicks in fully. One I have had for 25 years and the other I built 3 years ago on a subdivided section (nightmare). The other properties are multi-income sites.

But the biggest reason to sell is fear of further regulation. If the RBNZ is pressured to reduce or remove I/O loans then I will end up cash-flow negative. So reducing debt also reduces the consequences of this possibility and gives me a larger cash buffer. Over time I fully expect rents on the remaining properties to compensate for the extra tax burden, but I have to be careful as I live on this income and the rules if changed once, can be changed again.

So I am also having to give notice to one set of tenants who are on a low rental (but haven’t wanted me to upgrade as they cant afford more) and renovate that house to bring it up to a fair rental ( 500pw to 600pw).

As you can see there are lots of real world implications from these policy changes.

LikeLiked by 1 person

Like you I have done the sums. 43% LVR so that’s good but not enough rent to cover paying tax and repaying the balance of the loans as well as upgrade the houses. 4 now in need and two are done.

Not enough cash flow to do that and pay tax and pay the principle as well.

tough choices after putting up with some shit tenants, lousy tribunals and until recently not a lot of capital gain.

Yep, there are plenty of places that didn’t and won’t have the capital gain like Auckland and Wellington.

Too many MP’s and they have too much freedom to screw all of us. Most of them are broken fools anyway, including Cindy who on an MP’s salary couldn’t afford to buy a house. Someone in the labour camp gave her the money when they thought she was going into rising star status. and so it went.

Amazing how things change when you get up the ladder. Beach house and all now.

Nasty little Marxist.

LikeLike

Thanks Michael. A nice counterpoint to the majority of commenters who blame low interest rates for house price rises more than quantitative easing.

Tax expert Terry Baucher says landlords claiming the “loophole” closing is terrible effectively points out that a landlord running at a loss by intent was never intending to be a business and therefore should not be allowed interest write-offs like a genuine business. The whole article is worth reading in full, but one bit caught my eye https://www.interest.co.nz/opinion/109717/week-tax-more-implications-governments-shock-property-taxation-proposals-and :

“But what has become apparent in the residential property investment market is that there’s two parts of the economic return. There is the rental and then there’s the capital gain.

And the issue was that many leveraged investors who are most affected was that they were getting a full interest deduction but would only be taxed on part of the economic return. That is the rental income. All things being equal the capital gain would not be taxed unless the bright-line test applied. Restricting interest deductions in that context is actually consistent with the general income tax rule that an expense is only deductible to the extent it’s incurred in deriving gross income.

The current treatment is therefore an anomaly. What the Government has done is closed off an anomalous position, but only in respect of a certain group of investors, which again leads to outrage about the treatment. But that group is probably losing that argument about it not being a loophole, because to borrow a political phrase, “Explaining is losing” particularly if as in this instance a very technical argument applies.”

LikeLike

Agree, that is a very good article.

LikeLiked by 1 person

Can’t see how a tax expert could write a good unbiased article when clearly he gets a massive income boost from these latest tax changes. Terry Baucher should caveat his article with, note that I just trebled my income with these latest tax changes.

LikeLike

Thanks for the link. His argument would seem to have been more compelling prior to the ringfencing change in 2019. More generally, better to fix the planning laws and markedly reduce the prospect of any sustained systematic real appreciation in a generic property.

LikeLiked by 1 person

Michael, a tax anomaly is a distortion that needs to be corrected not dismissed. I agree with you that freeing up land including height restrictions is the crucial long term solution. The first steps have been taken on that in the policy statement last year. In Wellington it would allow higher buildings in many areas. Locally in Khandallah there is opposition to that but that will not stop the regulatory change. As regards not having predictions of the price effects – how could they be predicted?

LikeLike

Pat

Which distortion do you think needed correcting? Perhaps there is a case for a full CGT, but not as housing market policy (and yet this was a housing mkt package). Re deductibility perhaps there was a case for limiting deductibility to real interest only, but even then only on a neutral basis affecting all business borrowing.

The package was purportedly about housing, and yet the Minister of Finance could not offer any view that it would lower rents and re prices could assert no more than that the recent very rapid rate of increase would be slowed.

LikeLike

So it seems to me that you consider keeping up with inflation and or the market to be evil.

Property Investors are not responsible for the market behaviour but take the good with the bad.

I have no doubt that you like so many socialists would consider that your pension and whatever other benefits you accrue should at least keep up with the CPI.

All you have done is make excuses for the Govt. to raise more tax (to waste), and do nothing constructive about the real issues. Where were you 14-15 years ago when developers couldn’t sell sections, builder’s couldn’t sell houses and landlords struggled to find tenants. yep that all happened.

The biggest unsaid thing here is productivity and waste by unconstrained political aspirations.

LikeLiked by 1 person

Nobody ever seems to mention tackling the demand side?

Surely capping the number of people coming to live in NZ is the quickest solution?

Close the borders for a year and reduce the COVID threat at the same time.

LikeLike

The reason I don’t write much about it at present is that since the borders were closed we have had a reasonably material net outflow, and almost the only people allowed in are NZ citizens and those who already had permanent residence visas. This month alone – to yesterday – a net outflow of 2000 people.

But if the govt won’t fix the land market, immigration numbers allowed once the border reopen should take account of the housing issues/implications.

LikeLike

Dave, the borders have been closed for a year now and house prices rose 20% in February and have actually been rising since Jacinda Ardern and her marxist team of do gooders started their term of government.

LikeLike

It’s certainly lucky that inward migration has stalled due to COVID. But given our growing state-house waitlist and rapidly increasing costs of the Accommodation Supplement – regardless what happens to immigration, the existing problem will take a lot more to fix. And I think policy to bring rent costs down is even more urgent than that aimed at property prices. This is a fascinating calculator indicating what an affordable rent is based on a household (gross) income;

https://calculate.co.nz/rent-affordability-calculator.php

Take for example, a single pensioner with no income source other than superannuation. The maximum (i.e., 30% of gross income) that they should be paying in rent is $152.00. For a couple on super as their only source of income, the maximum weekly rent should be $230.00. I dread thinking how this soon-to-retire set of ex-state tenants of the neo-liberal era, who have since faced unaffordable market rents through the rest of their working lifetime are going to house themselves in retirement.

LikeLike

That is what motels are for these days.

LikeLike

“The tax systems are much the same across the country.”

In the US, homeowners can deduct interest on their mortgages against their income;

https://www.irs.gov/publications/p936#:~:text=You%20can%20deduct%20home%20mortgage,incurred%20before%20December%2016%2C%202017.

And they have various capital gains tax scenarios (both for own residences based on thresholds), and for investment properties;

If you sell property that is not your main home (including a second home) that you’ve held for at least a year, you must pay tax on any profit at the capital gains rate of up to 15 percent. It’s not technically a capital gain, Levine explained, but it’s treated as such. Profit from selling buildings held less than a year is taxed at your regular rate.

If you’ve depreciated the property, you might pay a different rate. For example, if you buy a rental house at $300,000, take depreciation deductions of $100,000 over the years, and then sell it for $320,000, your gain for taxes is $120,000. But you pay at a maximum 25 percent rate on the first $100,000. The amount you deducted for depreciation, and the 15 percent capital gains rate applies only to the $20,000 gain remaining, Levine said.

https://turbotax.intuit.com/tax-tips/home-ownership/tax-law-for-selling-real-estate/L9PmDNkK5#:~:text=If%20you%20sell%20property%20that,of%20up%20to%2015%20percent.

The big difference I believe is that the average Americans I know generally don’t aspire to go into the business of land-lording, but most of the population starts out their young life renting an apartment in a complex that is owned by a corporate entity. The US just do not have the plethora of (effectively) sole traders eeking out a living or supplementing their retirement income with a multiple, single-dwelling rental units.

And my experience of NZ, is that the average New Zealander got into this type of business venture when National did its big state-house sell off during the Bolger government. I recall staff a Porirua office explaining what money-for-jam it was! You put a lick of paint on it; hung some new curtains and rented it back to the same people the government had previously rented it to – only at a market rate. Sadly, this changed the way we all started looking at housing – not a home, but a commodity to be bought and sold – with a handsome (non-taxable) profit to be made!!

In selling off our state housing we started on the path of the worst inter-generational poverty in NZs history. Let’s call it what it is – neo-liberalism and the sale of state-held assets and infrastructure. It really has very, very little to do with NZs planning laws. Yes, having no zoning rules differentiation between urban and rural might well bring the price of urban land down more generally, but I doubt it. We’ve already built on the best land available; that being land close to centers of work and on the least complicated/expensive sites for housing. Expecting the ‘young and poor’ to commute from Pukekohe to AKL Central all in the name of affordable housing is an awful view of how to ‘solve’ this problem.

LikeLike

Yes, I decided to leave the US tax provisions out of this post just to avoid complexifying it with the detail. I’ve always been intrigued by the CGT on owner-occupied housing, albeit with substantial rollover relief. Key point is that the main features are the same across the country, and yet house price outcomes – even in significant cities – are not.

In NZ there wouldn’t be the same enthusiasm for being a landlord were it not for govt measures (planning and population interacting) that underpin an artificial scarcity. Moreover, if houses were materially more affordable there be many fewer rental properties in total (since more would be owner-occupiers).

On the final para, I guess for now we’ll just agree to differ. But on your model, what policy approaches would you champion to markedly lower the cost of housing and houses?

LikeLike

We only disagree on which policy measure might have the most (and much needed!) urgent impact. Like you I think this ‘salvo’ by the government was the wrong one. I’ve never been happy with our tax system, and using an already flawed system to try and right this issue just isn’t they way I’d have gone.

I’ve modelled a weekly maxima rent control policy – which I believe would need to be introduced universally (as a means to address the ills of much of the overseas experience). The formula used in modelling is:

Weekly rent maxima = (GV/1000) +/- x%

The variable ‘x’ would be determine based on bringing the lower (i.e., three categories are used by tenancy.govt.nz to classify rental accommodation: lower, middle and upper) rental properties to equate to a weekly rent maxima of 30% of gross household income for the particular geographic region/area as per tenancy.govt.nz reporting;

https://www.tenancy.govt.nz/rent-bond-and-bills/market-rent/

So, on that website, each area would display the formula (along with the ‘set’ variable for that area) and the weekly rent maxima, as opposed to the ‘Market Rent’.

My modelling (of all rental properties listed on realestate.co.nz for a one month period; and using ‘0’ for the variable given GVs were last produced in 2019 for the districts) suggests that middle and upper rents would in most cases, be unaffected by the maxima. The main decreases in rents would mostly be applicable to the ‘lower’ category of rental properties. For example, a 2 bedroom flat in Lower Hutt was advertised at $520/week. Tenancy.govt.nz had that market rent at $405/week. And applying my formula (using 0 as the variable) would have produced a rent maxima of $390/week. Still high, given a household income would need to be $68,000 for that to be affordable, but better than what we have now.

LikeLiked by 1 person

New Zealanders are just smarter than Americans and worked out early in life after reading American books on Rich dad, poor dad and understood the basic principle of leveraged returns. Very simple maths but it works. A 10% increase in price when leveraged with 80% loans equate to a 50% return on your investment. Last month when the average house price rose by 20%, the average property investor and that includes owner occupiers made a 100% return on their investment in a month.

LikeLike

Well, my great Grandmother lived in Newtown and Kilbirnie long before you were born and had rental houses.

There is nothing new about people having rental houses. People also had boarding houses. And they did this because there was no social welfare for anything. If you were a widow ( from wars and accidents etc) life was tough. If you got old life was tough without an income. Why do you think they all died so young?

Bolger theoretically allowed the sale to the tenants but HNZ or whatever it was couldn’t convince tenants to buy their houses. The next step was to sell them to others.

Robbing middle-income earners to pay for others housing is disgraceful along with a lot of other bad socialist behaviour. IMHO govt. and councils don’t need to own very much at all. Most things they do own become expensive, need a hand out to keep going and so on. Good example is TV.

Yes we need a safety net for those that can’t help themselves and the rest need to get up, get a hand and get on with life.

Taxing people never made people be better citizens nor did it encourage enterprize.

LikeLike

How exactly would you do the following things:

But the government has simply done nothing about freeing up the land, facilitating again aggressive competition among potential vendors on the periphery and in the intensifying centre and suburbs, which is the sure and reliable way of getting house prices (land prices) and rents down. And doing so quite quickly, because although it takes time to build, it takes very little time for expectations to change, and markets trade on expectations.

What are the specific ways, mechanisms to do this?

LikeLike

The key element is the first item in my list here

https://businessdesk.co.nz/article/opinion/revealed-the-real-cause-of-high-house-prices

There is still lots of detail for officials to fill in, but the key issue is to take the power to block out of the hands of councils and put choice in the hands of existing landowners,. A general right to build on the periphery would completely alter expectations about likely future values, by removing most of the scarcity.

LikeLike

Why won’t the government act to free up land? Do they genuinely fail to understand that this is the root of the problem? Do they have a vested interest in maintaining the status quo? Is it because most Councils appear to be Left leaning and have the government’s ear? All they are doing is making an already bad situation worse. Are they really that thick?

LikeLike

The government has provided some freeing up of land via the NPS on Urban Development

Click to access AA%20Gazetted%20-%20NPSUD%2017.07.2020%20pdf.pdf

But is has a minimum timeframe of 2 years from implementation (table 4.1) before the policies have to be in place, so late 2022 at the earliest.

Meanwhile the NBEA & SPA are coming to replace the RMA, but the timeframes are even longer – so no hope there.

The government simply needs to get on and build as many state houses as possible & far more than its currently proposing. The wait list is astronomical.

LikeLike

And another commentator (it might have been Bernard Hickey?) explained that the amount of the recently announced $3.8 billion dollar Housing Acceleration Fund is only equal to the annual amount we currently spend on Emergency Housing (EH) + Accommodation Supplement (AS). That is ANNUAL spend.

We are in ‘deep doo doo’, as another commentator explained.

We cannot build new dwellings fast enough. I see rent control as being the only viable option to prevent further blow-outs in the costs of EH and AS. Emergency housing is no way to respectfully house people/families in crisis, and expanding the AS just sees rents rise accordingly. All very slippery slope stuff.

LikeLike

My hypothesis is that it is a combination of three things:

– they have now instinctive trust/faith in market mechanisms,

– plenty of them don’t really believe in expanding the physical footprint of cities (whether for emissions reasons, reasons of their own aesthetics, or a hankering for old European cities or whatever)

– they are terrified of what they think would be the consequences of much lower house prices (having picked up some weird stories based on past busts in countries that had had too much builiding) and they’ve not been willing to look seriously at my partial compensation scheme.

I suspect quite a few of them really do think that 60% of the population renting, esp from the state would be (a) good, and b) in their thinking, perhaps inevitable. They like to cite Germany or Switzerland (the latter has v high house prices) and are quite uninterested in the low cost US/canadian cities.

LikeLiked by 1 person

Reblogged this on Utopia, you are standing in it!.

LikeLike

So we all disappear down the rabbit hole of detail that may or not solve the problem. So where is the problem. We are a socialist country. The state believes it can centrally plan all facets of the economy.

The state exploitation of the plight of the poor manifests itself in the interventions in what passes for a market.

One ontervention begets another ad nauseum and the winner is the plethora of regulation overseen by state agencies who have no skin the game but know implicitly that only if we had more rules and complete control then everything would work as Marx had wanted. This game will go on until Evita and the pie eater decide enough is enough and all land must be owned by the state and value accruing overtime belongs to everybody . Some of course will be entitled to more being privileged in the barnyard. Investors will find better countries to grow their nest egg than a communist state downunder. Culture dominates politics , Politics trump econmics. There is more pain coming Grant have to eat more to stomach the future.

LikeLike

Yes, the way I see it one simple rent control formula applied universally and leaving the existing tax settings (no CGT and interest able to be expensed) in place. Much simpler, much more equitable for everyone and effective immediately.

LikeLike

Rent Controls are: “the most efficient technique presently known to destroy a city—except for bombing.” Assar Lindbeck.

The crude hammer of Govt interfering in housing markets is a sure path to terrible outcomes – whether in rent controls or the huge regulatory costs imposed on building new houses that has jacked up their cost to sky high levels.

LikeLiked by 1 person

Yes Foyle I’ve heard that quote before. It relates to the design/implementation of rent controls overseas – i.e., the non-universal rent control schemes (i.e., only applying to a select set of buildings/accommodation sites). I I believe that is one of the main contributing factors to unintended negative consequences arising in terms of delayed/slowed inner-city renewal and rejuvenation – which the quote refers to.

Just curious – do you see the government’s accommodation supplement program as a “crude hammer of Govt interfering in housing market”? If so, how would you propose to unwind that?

LikeLike

Muldoon tried that and it was an unmitigated failure. go look it up.

No one is going to build more houses for renters if you control the income.

Already I hear investors are not keen on new anymore because the legislation is not written yet and no one trusts Cindy or Robbo any more.

Already people are selling their houses.

You worry about people in the motels.

Well, there are many who deserve to sleep under a hedge but not having had rentals you wouldn’t believe that. There are motels now that have become like those houses in Taita.Gang pads. Places of drug supply. Ask the councillors in Rotorua. Ask Mary Repecca Tait.

Perhaps you saw the School Principle from up north last week talking about 5 years old coming to school with a real age of 2.5. Well, it is common, and it’s not the house that’s the problem. My daughter in law teaches new entrants in a reasonable suburb in Tauranga. They have the same problem, even from new housing.

It’s about attitude, drugs, money, poor education, parents that are the grown-up version of their kids. Parents that need boot camp for a year.

Parents who have never been taught self-discipline nor personal responsibility.

Business thrives on certainty.

We no longer have that and so you add covid to that and Houston we have a problem.

Yolu want to help the above people and let them have a house?

you won’t get them a house by beating up the only people who can supply. The State can never fill the gap.

Never has and never will.

All those statehouses that you think they built, well have a look and see who they built them for.

Working people. Who paid the tax for them? Working people.

Then they created beneficiaries.

LikeLiked by 1 person

Viking. As I understand it, Muldoon froze rents, wages and prices because he was trying to control rampant inflation. We’re now in a deflationary/low inflation environment – except where housing assets are concerned. I’m not proposing to freeze anything. What I’m saying is that we need control rents (not a rent freeze) in order to make shelter affordable, particularly for those on low incomes. The weekly rent maximum would be set once every 3 years (with the revaluation of GVs) and in between rent rises would be no more than CPI. On revaluation of GVs, the variable ‘x’ in the rent control formula would need to be re-set based on achieving that same affordability metric for the lower priced category of rental housing as per the tenancy.govt.nz categorisations.

And yes, your point that state houses were previously built for working people is a very good point. Many people in emergency housing and/or on the state house waiting list at the moment are working.

And I don’t think the private sector has ever built much in the way of new accommodation targeted at the buy-to-let market. Most rentals (aside from apartments) are previously owner-occupied homes purchased on the secondary (as opposed to new build) market. Not all, but most.

LikeLike

Katharine, you are wrong. The private sector builds for both owner occupiers and investors for rentals. If you look at the apartment market in Queenstown and in Auckland, most are intended for the Air BnB market and for the Student tenant.

LikeLike

I’m sitting on 10 acres of land about 10 minutes from the centre of a sizeable city but local council policy does not allow me to subdivide to build houses on it. So I continue to operate it as a small farm, make a loss every year and legally claim all sorts of expenses including GST. – Figure that one!! I’m not an Economist but did University Economics 50 years ago and the thing that still sticks in my mind is the “Supply and Demand” concept. They need to free up more land and build houses.

LikeLike

Utterly insane (the Council, like so many of them). The power to block needs to be taken away from councils in favour of a default presumption of a right to build.

LikeLiked by 1 person

It may not be insane. I used to live on a rural-residential section (99 acres – 60 planted in pine) just outside Palmy. The access road was narrow and winding and it flooded at the entrance in every decent rain. The landscape being as steep as it was, meant soil erosion into a pristine little stream running through our property was saved by changing those earlier paddocks into forestry. Another pine block in the vicinity was felled – and the properties below experienced extreme flooding in the associated creek, subsequently requiring the council to install a concrete bridge into the subdivision. The subdivision of course did not have reticulated services and it would be uneconomic to install such.

Existing residents had taken up rural uses for their land – bulls escape their paddocks; chainsaws/milling is undertaken on properties; all these things create what is called ‘reverse sensitivity’ when zoning laws are amended.

All I’m saying is that it just can’t be labelled ‘insane’ in every circumstance.

LikeLike

Grant your general point, but it seems most likely to be “insane”. And yes, providing a presumptive right to build should not create a presumptive right to restrict the activities of the others in the area you move into.

LikeLike

Talking to a North Auckland farmer a while back; the council charged him $1 million to subdivide 4 lifestyle sections on a dirt road with no services to be provided. Local govt monopoly on consents doing damage to society as always. No wonder houses are unaffordable.

LikeLike

Was the land already zoned for rural-residential or did those costs include a plan change?

LikeLike

News for you Wayne

Because your 10 acre farmlet is registered for GST, any eventual sale price minus your original purchase price will be taxable plus GST

LikeLike

I recall Auckland Council had UN Agenda 21 on its website. Agenda 21 targeted Councils, bypassing legislatures with the idea of ‘smart cities’ and everything outside to revert to nature. A map showed great swathes of USA where animals could roam from the Atlantic to the Pacific. That is where the smart city Rural Urban Boundary came from [I think]. The problem is that it appears town planners still hold to that philosophy.

The solution is democratic. We should be able to vote for city planners, not just mayor and council. The planners would have long gone and this would not have been a problem.

Hopefully the government is holding in reserve that the re-construction of the RMA will solve that problem. However, it may just be kicking the ball down the road long enough to be the problem of the next term government.

Watch out for immigration picking up again so our GDP can register [again] 2.5% of which 2% is from immigration. Then the house prices will be transiting sky high again. The real problem is that we do not live in a democracy.

LikeLike

Currently, the problem with Bill Walmsley being appointed a commissioner. Been flogging this around the country for over 20 years and ma huta decided we need more.

LikeLike

Katharine,

Totally agree. We have Bulls which we transport around for service. Boundary fences have to be good. I am for ever shifting neighbours stock back into their properties that escape! The problem with these rural properties close to urban areas is the narrow roads, one way bridges, flood areas and lack of facilities (fresh water, sewage disposal, grey water disposal etc.). Therefore the costs of upgrading infrastructure is high even before you get into subdividing. It’s not an easy solution and I predict it may get worse as the world comes out of Covid-19. New Zealand is a very desirable country and all those returning NZ’ers and others wanting to live in this country will try and flock here and bring their money (at favourable exchange rates) and probably push the market up further. Alpacas used to cost a fortune many years ago. Nowadays there’s plenty around so the price has come right down. Again release more land and build- “supply and demand” It’ll take many years but it’s a no brainer. Government is only tweaking with what they are doing. I had 13 rentals at one stage and with the existing policy I would be selling them off. Possibly good for 1st home buyers but terrible for the large number that need to rent.

LikeLike

Note:

When someone moves from renting to owner occupier the net change in rental supply and rental demand is zero.

The issue is distributional. Those that move to being owner occupiers are the “richer” renters leaving “poorer renters facing relatively higher (unchanged) rents.

Ignoring the above (and assuming short run fixed housing supply) rents will also move higher so that rental yields support the remaining investors (there wont be many that would now fund a negative cashflow for 10 years for the capital gain).

So, the issue now is:

a) how fast can the government build additional state houses so that house prices fall instead to raise the rental yields.

b) how much of a lid government is willing to keep on immigration until we dig ourselves out of this mess

c) how much effect the NPS on Urban Development has on land/density supply

c) how much elasticity the NBEA & SPA add to the land/density supply & when and if they get passed as legislation.

LikeLike

I have been watching the massive housing development in Mt Roskill for 4 years now. The Labour government did move fast in vacating all the Housing NZ properties and jammed beneficiaries into motels and started building. However 4 years later not a single completed house. Clearly, this Labour government just can’t build houses.

LikeLike

Yes, 30% of all households rent and of that one-third of them are paying >50% of their gross household income in rent (a study HUD did in 2018). No wonder we have had to introduce free lunches in schools, eh?

The cost-of-living is too high in NZ – and that starts with the cost of accommodation. No time to wait – the motels and hotels filled with emergency housing recipients will want to get back to normal business once tourists are able to come back in. We’ll become a tent city society. My son is a river ranger and moves on homeless people all the time – many he takes to the ER as they are unwell and have suffered from exposure. The Police don’t want to know them and the NGO sector are at wits end.

Very few NZers are aware just what a crisis of poverty we are in.

LikeLiked by 1 person

Agree entirely. Take, for eg, the school lunches…everyone reflexively applauds feeding kids at school, and sneers at anyone who questions it, but hardly anyone bothers to ask how, where, why..in this ‘land of plenty’.

LikeLiked by 2 people

Given that NZ poor are fat, I think it is not from the lack of food but they suffer from too much easy and cheap access to the wrong type of food. This is indeed a land of plenty, perhaps too much over feeding.

LikeLiked by 1 person

Immigrants could be charged an infrastructure fee on entry. $50,000 per head would choke off the demand and provide some income

LikeLiked by 2 people

Years ago I read that the total value of NZ infrastructure divided by the population was about $250,000. That is the physical infrastructure; there is also the less tangible investment in teachers, medical and other trained civil servants.

Your proposed $50,000 would not choke off demand (except for most Pacific Islands); it is much the same amount as students pay agents and PTEs to get into NZ.

When I applied for residency 18 years ago I was told I needed $200,000 to get to the ‘point count’ threshold. I was surprised to discover that they didn’t mean giving $200,000 to NZ taxpayers and all I needed to do was provide proof that I had either savings or property worth that much.

An appropriate infrastructure fee could be paid as NZ treats student loans – a 12% extra income tax. If we were truly getting the skilled immigrants the govt boasts about then there would be little problem getting it paid off.

LikeLiked by 1 person

When I applied for Residency under the skilled category as a sought after accountant, the government was giving away Permanent Residency for anyone who wanted it. The only requirement was to queue up at the Immigration office and get the Residency Visa rubber stamped. It was painful queuing out on the road day after day. Back then immigration did not have a take a number system. So it was up at 3am and try to get in before the close at 4pm. Yes those days government offices closed early.

LikeLike

Just as new cars should have an entrance fee on their first registration. They like [people demand more resources and in doing so the person who buys it should pay for those resources.

LikeLiked by 1 person

I think Council call it a development contribution plus development public drainage gifting, plus water care $15k water metering. The funny thing about the development public drainage gifting to Council is that it cost me almost $100k in earthworks, concrete common access roading, engineers planning and approvals but the value gifted officially to Council was only $14k which was just the materials cost. That is why housing costs continue to rise. The public infrastructure costs are already being charged to the person who buys.

LikeLike

No ‘silver bullet’ will fix NZ’s housing crisis https://www.rnz.co.nz/national/programmes/nights/audio/2018782019/no-silver-bullet-will-fix-housing-crisis

This is the best description I’ve ever read/heard about our broken housing market.

There isn’t a “free market” solution to our woes as Professor Tookey explains in detail.

We need government intervention.

We needed it a decade ago.

LikeLiked by 1 person

There is a free market solution if govt (local and central) stops imposing 100’s of thousands in extra regulatory costs on new builds, reserve contributions, infrastructure costs, extremely detailed inspections, super expensive and slow design and consenting processes, culture of fear liability that leads to vast overspeccing by engineers of everything rather than accept even a remote possibility of fault in some small proportion of houses, and add over the top health and safety regs that make it essentially impossible to build a house while complying with rules. All of these factors are contributing to houses taking 2-3x as long and costing twice as much to build (in real terms) as they did 20 years ago with no delivered improvement in their utility (almost all houses built prior to the new regime are perfectly fine). The cost of land and house building has vastly outstripped inflation because of regulation and regulation alone.

LikeLiked by 2 people

“All of these factors are contributing to houses taking 2-3x as long and costing twice as much to build (in real terms) as they did 20 years ago with no delivered improvement in their utility (almost all houses built prior to the new regime are perfectly fine).”

You must be joking;

https://en.wikipedia.org/wiki/Leaky_homes_crisis

LikeLike

Fixing leaky homes required some minor changes to building codes (that were done), not construction of a vast bureaucratic arse covering industry that was sadly enacted by people who stood to increase the size of their bureaucratic empires and professional fees by doing so. The majority of the cost was down to litigation of liability rather than actual repair costs (two cases I am personally aware of where legal bills were 5-10x ultimate cost of repairs). What an absolute indictment of the system. It could easily be avoided in future by simple law changes to remove long term liability from govt and builders etc making property owners responsible for any costs of repair and removing professional motivation for extreme over-speccing of designs. Caveat Emptor!! Homeowners can then quite cheaply buy insurance against problems if they want, without any need to involve lawyers or other professional parasites ever again. That simple measure would allow us to dismantle most of the house regulatory compliance industry and depopulate huge council consenting departments and save 10’s to 100’s of thousands per house.

Oh and stop councils milking developers for infrastructure repair and development and on-property storm water management (that older houses aren’t required to install) – pay for it with universally levied rates (the council is gaining a huge income stream in the form of anther rate payer anyway). That would quickly bring new build prices down by another few 100k

LikeLiked by 1 person

That was another govt. failure. Bought on by Bolger and smith with the aid of the greens. Don’t treat pine they decided.

Brilliant decision.

But blame the builders then.

And yes most houses get wet. All houses have leaks sooner or later even if it’s your new double door fridge with water cooler. Ask the carpet dryers.

Had all that timber been even boric treated it would still have been on , just needed a reclad.

But Branz knew better.

Never trust the Govt.

LikeLiked by 2 people

The decision to build, buy a section, design time, consent time, build time, all takes up to 2 years

Whereas a new immigrant plus their family can arrive in country overnight

The population of NZ increased by 1.2 million in the past 20 years

They must be living somewhere

One assumes the housing stock in that time increased by 400,000

Obviously not enough

Evidence indicates they immediately buy an existing home

They don’t have the time to build new, and they are not inclined to live in the fringes

LikeLiked by 1 person

2 years is actually a fast time. It took me 4 years to complete a 3 site subdivision from Resource consent to final CCC in Mt Roskill. The government is now in its 4th year in developing this massive Housing NZ site in Mt Roskill and it is not even close to completion as yet.

LikeLike

What an interesting debate, with a huge variety of opinion and neatly packaged solutions! My two pence worth is that, a) our housing crisis is just the tip of the iceberg with many other issues out of sight but highly relevant, eg, falling educational levels; abysmal productivity: excessive Immigration; tyranny of distance affecting our economy (no matter how well organised): & so on.

b) misplaced faith in the ability of the state to “fine tune” anything…legislation is a very blunt instrument.

c) with the inevitability of unintended consequences, and the ready examples of the RMA, the Building Act, and the Local Government Act which all started with high sounding purposes but ended up as bottomless pits absorbing $b’s of wasted public and private monies, one would have thought Kiwis might have become very distrustful of any state-engineered reform proposals!

Is NZ well on it’s way to be coming a failed state similar to some of our Pacific neighbours? I think not, but I imagine things will need to get much more dire before our average citizen decides not to rely on the “gummit” for ever more holidays, houses, play space, and compensation for every setback, real or imagined.

If this debate is about suggesting simple solutions to complex problems, my contribution is that we need a PM whose main public pronouncement is…”Kiwi, get off your backside and start some real work.”

The alternative is likely our Asian friends will give us a few muskets and blankets and sort the problems in their own efficient ways.

LikeLiked by 1 person

With the NZD rising against many of our Asian friends currencies, NZ has the buying power to buy those muskets and blankets. No need to be given anything.

LikeLike

History repeating

Housing in New Zealand (1946) [Part 1 of 2]

Housing in New Zealand (1946) [Part 2 of 2]

LikeLiked by 1 person

Very few New Zealanders are aware that the Government has allowed the release of 20% of the prison population. Around 2,000 people, many with nowhere to live and pushed them into motels.

LikeLike

The government has already 22,000 on the waitlist for social housing as well. Guess they are jammed packed into motels as well.

LikeLike

“And don’t go blaming interest rates for the house prices”

They are certainly part of the equation, along with the RB’s insistence that they will be low for a considerable period of time and comments from Chief Economist last year that they are essentially happy rising prices are making people feel more wealthy and would prefer more rather than less. Those expressed sentiments must play into people’s calculations as to what they can afford in a market where prices are increasing rapidly. Now many of those people who acted on these signals from the Bank will be highly vulnerable to rising interest rates in a market where house prices could fall thanks to the Government’s much harder approach.

It is shocking that the MoF can’t or won’t clearly articulate what the likely consequences of his policies will be as if he hadn’t even thought it through, weighted different options and arrived at a solution after thorough analysis and debate. The Government vicious intentions could and should have been foreshadowed much earlier so people could have made informed during choices during the height of the madness. Neither the Bank nor the Government deserve any plaudits for their handling of this issue or communication of their policies.

LikeLiked by 1 person

[…] Inflation for some of these things are already flowing into NZ, starting with the price of petrol. But the rest will be along soon enough to add to our already unaffordable homes, as pointed out by Mr Reddell at Croaking Cassandra: […]

LikeLike