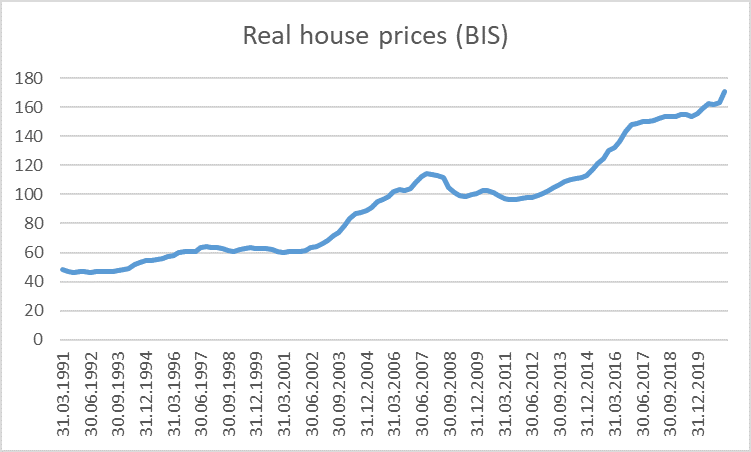

And so yesterday we got the long-awaited government package in response to the latest surge in house prices. As a reminder, it is just the latest surge in the more than trebling in real New Zealand house prices over the last 30 years.

We know it wasn’t really a serious policy designed to fix the housing market, not just because it didn’t even address the core issue (land use regulation etc) but because the Prime Minister still can’t bring herself to say that she would like to see lower house prices – not even just reversing the rise of the last few months – and the Treasury’s Regulatory Impact Statement is headed “Tax measures to moderate house-price growth”. Add to that I’ve seen reported that Treasury expects the extension of the so-called “brightline test” to boost government revenue, when a package that actually did something about fixing the market would see that specific revenue line almost evaporate for many years to come.

There is a lot that is odd about yesterday’s announcement, including the Treasury claim (in the RIS they published) that they opposed the deductibility rule change because they hadn’t had time to properly analyse it. Even if this was a last minute idea dreamed up by someone in the Beehive – and Richard Harman’s newsletter this morning suggests not, that the idea had been under consideration at least since November – what does it say about the loss of accumulated expertise in The Treasury that they could not offer robust analysis at short notice on almost any of the myriad possible housing tax changes that have been proposed and analysed at various times over the last 20 years? Surely (a) this is core capability (especially in a New Zealand with longrunning housing policy dysfunction), and (b) the analysis involved would have been qualitatively similar to whatever advice and analysis Treasury provided on ring-fencing rental income losses only a couple of years ago?

There are two tax components to the package; the extension of the brightline test to 10 years, and the removal of the deductibility of interest expenses for residential rental landlords. The latter is the more significant measure, but I’ll come back to that.

The only good case, ever, for the brightline test was what the name implied. Using time rather than intent (hard to prove) to determine which sales of investment property were subject to tax was easier, clear and simple. If, instead, you want to tax investment asset appreciation more generally, you’d introduce a capital gains tax. Such a tax would capture all investment assets (not just a particular class the government of the day doesn’t like), and it would provide for loss-offsetting arrangements. A proper CGT is somewhat akin to the government becoming an equity partner in your assets; ups and downs (although not generally in a fully symmetrical way). You might or might not agree with a CGT, but (a) no serious person/government ever thought one was the answer to house prices (and if any did experience should have long since disillusioned them), and (b) there is no sign in New Zealand house prices (and unsurprisingly) that the initial introduction of the brightline test, or its more recent extension, made any material difference to New Zealand house prices. So there is little reason to suppose this change will either (contrary to Treasury who claim to believe it will make a difference even in the “medium term”, albeit perhaps not the long term). It will, of course, change some transactional behaviour, reinforcing a lock-in effect for some investors (and thus reducing the efficiency of the housing market), but that is a different matter than any sustained impact on prices.

One aspect of the brightline test extension I haven’t seen referred to – and is not mentioned at all in the RIS – is the interaction with inflation. Over a 10 year horizon – let alone the 20 years Treasury favoured – a significant chunk of any house price increases will be general CPI inflation (if the Reserve Bank met its target the CPI would rise by 22 per cent over 10 years). There is little serious case anywhere for taxing general inflationary gains (as distinct from increases in real asset prices/values), and the issue is reinforced by the increases in the maximum marginal tax rate to 39 per cent. Suppose the government’s policies finally got on top of growth in real house prices and the only increase in house prices was from general CPI inflation. Someone selling just before the 10 years would be paying 8.5 per cent of the value of their asset in tax even though they had had no increase in real purchasing power at all. That would be a straight confiscatory tax, even more so at the horizons Treasury favoured (where it is harder to avoid by delaying sale). And yet Treasury regards a longer brightline test horizon, with full nominal gains taxed at a higher rate as both fairer and more efficient! A capital gains tax should tax either real gains or, much less desirably, tax nominal gains at a reduced rate. For the scapegoated sector we now have nominal gains taxed at a high (and rising) rate.

What of the deductibility policy? This is, as announced, a simply bizarre policy, not helped by the egregious spin – really bordering on lies – from the government suggesting that the ability to deduct interest from gross income in calculating the owner’s tax liability is a “loophole”. It is simply standard practice, a deduction open to any business. Except, very soon, operators of residential rental businesses. In many firms, in a wide variety of sectors, interest is a cost of doing business.

I can think of three bases on which a policy change around deductibility might have made sense. There is a decent argument that, for tax purposes, no interest paid should be deductible and no interest earned should be assessible. But that would involve universal application. There was an argument that some (from memory including Don Brash) used to advance that with no tax on capital gains, perhaps interest on investment property should not be deductible. But extending the brightline test to 10 years substantially undermines that argument for houses…..leaving it more potent for other assets (eg farm land) to which deductibility has not been limited. And that argument that I find most appealing – and which from memory the Reserve Bank used to favour – was that some proportion of interest deductions were really just inflation compensation, and didn’t really amount to a real expense (just maintaining the real value of capital). But that would argue for a symmetrical treatment of interest income and interest outgoings, and for a comprehensive approach, not just one picking on a current government scapegoat. Had the government been serious about rigorous reform that improved, not worsened, the tax system they could have foreshadowed that sort of change. At present, with interest rates so low, it probably would have reduced by about half the extent of interest that could be deducted.

(The “loophole” argument appears to be based on the fact that owner-occupiers cannot deduct interest. It should barely need saying that owner-occupiers are also not assessed for tax on the imputed rental value of living in their home – nor, of course, (generally) are they subject to the “brightline test”. Whenever there have been serious suggestions of taxing imputed rentals it has been recognised that interest deductibility would need to be introduced as part of any such mix. )

There seems to be a range of views around about what impact the deductibility change will have, especially on house prices. Westpac appears to mark out one end of the range, suggesting in a bulletin yesterday that house prices could settle 10 per cent lower over the longer-term with the potential for “much greater effects” in the shorter-term.

As they note, the Westpac economics team – their chief economist is currently on secondment to The Treasury – have long been advocating a model of house prices in New Zealand that emphasises the power of tax policy and tax policy changes to affect house prices. I’ve long been sceptical of that sort of story (and to refresh my memory dug out notes I’d written on the specific role of tax while at both the Reserve Bank and the Treasury). A paper with a very similar approach to the Westpac one was published as a Reserve Bank discussion paper some years ago, and it has a useful table (page 14) looking at the way in which various variables, including tax ones, affect the price various classes of potential purchasers (leveraged, unleveraged, investors, owner-occupiers) will be willing to pay for a house.

I’m no more convinced this time that tax (or regulatory) changes will have a large effect on prices (and a 10 per cent longer-term effect is quite large) than on previous occasions. One might expect some difference in what type of entity owns the property, but even then it is as well to be cautious. Just a couple of years ago, the ability to offset rental losses against other income was removed, and I’ve seen little in the way of analysis or argument suggesting that had very much effect at all, in prospect or in realisation. But if we go back further, there was little sign that the increase in the maximum marginal tax rate in 2000, foreshadowed with certainty for at least a year, gave a big boost to house prices (as the model predicts, because interest deduction is more valuable) or that the reversal of that increase a decade later cut house prices. The arbitrary removal in 2005 of the ability to deduct depreciation – on houses (as distinct from land) – didn’t seem to have a discernible sustained effect. The PIE regime, which worked against individual landlords, had little obvious effect. And going back further there is even less sign of such effects as decades earlier maximum marginal tax rates rose to 66 per cent, and then fell again, when inflation raised nominal interest rates (increasing the value of the interest deduction) or when ring-fencing was abolished in the early 80s and reinstated in the early 1990s. I’m also sceptical because we can see the huge divergence in house price outcomes in US cities, with fairly similar tax codes and banking practices across them, in ways that point to land use restrictions – and the long-run supply price of new houses – as the more important explanatory factor.

Perhaps this time will be different (although, almost inevitably, we will struggle to know, trying to unpick all the competing influences. Presumably some holders of investment properties will take the opportunity to sell now. Quite probably yesterday’s changes will help bring forward the temporary pause, or perhaps even pullback, that was always likely before too long (with no population growth, much tighter LVRs, perhaps a (irrational) ban on interest-only lending, perhaps even some lift in term mortgage rates etc). We’ve seen such pauses before and will no doubt see them again. But the supply/land issues have not been tackled.

It is worth noting that under the sort of model Westpac (and the Reserve Bank, see above) used, the purchaser willing to pay the highest price for a house was………..not the highly-leveraged investor but the unleveraged owner-occupier. That was so back in 2008 (when the RB analysis was done), reflecting the fact the imputed rental income is not taxed (and such purchasers have no interest payments). The difference is greater now – even prior to yesterday’s announcement – because owner-occupiers don’t have to worry about the brightline tax, while any investor – even if iniitally intending to hold for more than five years, rationally has to factor in a probability of seeling earlier.

Perhaps a little surprisingly (my notes record that it was so to me) is that the group next most willing to pay is the unleveraged investors. They do pay tax on their rental income, but – like the owner-occupiers – they have to think about the opportunity cost of their money, which has to be invested somewhere. Deposit rates are typically a lot lower than mortgage rates, and one will pay a price to avoid being stuck in deposits. Heavily-geared landlords (and remember, they can now borrow only 60 per cent from banks) come in only third. Of course, there may be times when highly-leveraged landlords are key marginal players – quite plausibly the last few months, especially when dealing with a temporary lifting of financial repression targeted at such people – but it wasn’t the general case, even pre-brightline.

One of the uncertainties, of course, is to what extent rents rise in the wake of this change. There is a lot of headline coverage of that, but the honest answer is that we don’t really know (although, again, the nature of the effect should be similar to that for ringfencing, albeit potentially on a larger scale). I’m a little sceptical as to how large the effect will be – notwithstanding the buffering the Accommodation Supplement provides – because if leveraged landlords were able to recoup all/most of their increased costs, that would leave excess expected returns on offer for unleveraged landlords (who are not directly affected by the loss of deductibility). Owner-occupation certainly hasn’t got easer – relative to six months ago LVR controls are back and prices/deposit requirements are higher (or even on Westpac’s take no lower) so I’d expect the biggest difference to be a shift over time from more heavily leveraged landlords to less-leveraged or unleveraged landlords, perhaps with a relatively modest (sustained) rise in rents.

This is, of course, then a policy that skews opportunities away from those needing debt finance (it explicitly no longer treats debt and equity similarly, previously one of the strengths of the NZ tax system) and they tend to be….the new entrants and more-marginal players. In favour of old money, institutional investors etc – who have pools of money that need investing. Now if you are a central banker you might think less leverage was “a good thing” (although that is what capital requirements are for) but it isn’t obvious that is so more generally, given the rigged land market. As Adrian Orr used to say – back when we were analysing housing options at the Bank 15 years ago – many of the leveraged investors are people like (his example) firemen, with a modest salary and using leverage – where it is available with good collateral – to get into an investment property, doing maintenance etc on their days off, getting a foot on the ladder (and some “forced savings” too). It was like that for a long time, whether or not real house prices were rising strongly.

Officials and ministers – especially Labour ministers – really don’t seem to like those sorts of people, and the sort of housing supply that results. Over a couple of decades now policy seems to have been set increasingly in ways that will have the effect of driving these small, initially quite leveraged, players from the housing field. In some cases that has seemed deliberate – including from some who really think home ownership isn’t something people should reasonably aspire to, and that long-term renting is some sort of Germanic ideal – in others just a side effect, but the direction is pretty clear: they favour institutional savings, not individual, and institutional (or large scale) rental providers not individual ones. And so the policy system – which 30 years ago treated these groups neutrally – no longer does. PIEs are taxed less heavily than individuals. Increased regulatory burdens (as ever) favour large players not small. Taxes based on realisations favour large unleveraged players, since they are less likely to be forced to sell, and have future gains to carry forward losses against). And now this egregious new distortion favouring equity over debt in rental housing. I don’t have any problem with institutional and corporate providers of rentals, but it should be an outcome of choice , enterprise, opportunity etc, not regulatory and tax distortions secured in their favour. Worse still, of course, is that if this latest package really does impair the availability of private rentals it will just strengthen the argument on the left that the state should be a much larger rental provider. There is a role for state rental dwellings, for a very small minority of troubled people, but in a functioning land and housing market there would simply be no market failure justifying such an intervention.

And a functioning land market – where there is aggressive competition among land providers/owners and genuine choice for potential purchasers between options on the periphery and options at greater density – is how unimproved outer-urban land prices should once again be somewhere near the price at the best alterative use (mostly farming presumably), not driven higher by artificial regulatorily-supported interventions. But such a market is what the government seems utterly uninterested in providing. The alternative – increasingly messy interventionist version of the status quo – appeals to the Greens and the statists, but it shouldn’t appeal to New Zealanders who care about their children becoming self-sufficient and able to meet the simple aspiration – readily achievable in a land-abundant country – of being able to purchase a basic house in their 20s.

Sadly, whatever was going to happen to house prices over the next three to five years anyway, it is hard to think that after some initial disruption, yesterday’s package will make very much sustained difference to prices at all. But I guess it will buy some political time and ease the headlines; today’s substitute for serious courageous leadership. Fixing the land market (and indexing the tax system) is still an option for some real leader, some day. If only.

Maybe you should have called your note today: Bleak House.

After all, it’ll probably take 60 years before a leader with enough courage to actually tackle housing emerges. Until then, everyone is caught in this nightmare limbo.

LikeLiked by 3 people

It will take exactly as long as it takes for the block of voters that owns houses to be smaller than the block of voters that doesn’t and not a day sooner. On the upside though I don’t expect that sort of market concentration to take 60 years to occur.

LikeLike

An interesting analysis, which confirmed my initial reactions.

LikeLike

However you see CGT as useful it has some distinct disadvantages.

1. It only gets you once per asset.

2. You choose when to get it applied.

3. It probably puts your liability into the highest tax rate.

The option chosen at least

1. Gives you a reminder of its existence every year

2. Reduces untaxed profit on the use of the other guys money.

Generally it must be have hit the right spot given the noise emanating from the rentiers!

LikeLiked by 1 person

As an accountant I welcome this dramatic change with so little information. Great to now be a key employee once again. I love complicated and unfair taxes full of loopholes and exemptions. Almost put out to pasture with so few dramatic changes in recent years, I am now suddenly a key staff member.

As a property investor it is quite simple. Sell existing property and buy brand new build property and get the exemptions from interest non deductibility and from the 10 Year Bright Line Test.

LikeLike

Totally agree with your article but your proxy of real house prices for the inflation of land values perpetuates the myths and confuses the policy options.

Real house prices have not gone up 30% – land prices have inflated under the houses. Houses just go along for the ride. Land prices for dairy farms are $3 per square metre but residential land is typically reaching $750.

In a country the same size as the UK with a fraction of the pop. the land shortage is totally artificial.

LikeLiked by 1 person

Oh, I agree entirely. If I didn’t draw the distinction in this post, I frequently do and just the other day made the explicit point that when people moan about rising house prices they really mean rising land prices. Houses remain a depreciating asset.

LikeLike

Thank you for another excellent post dealing with a very flawed economy.

The house price boom is just another symptom of a non performing economy.

The NZ economy is far out of balance, now led by a number of items only one of which is housing.

Ask any manufacturer or farmer.

There is little Government support for productivity, and the creation of real productive jobs.

Service and regulatory employment dominates the economy, often to the detriment of all primary producers.

In the export markets these few New Zealanders deal in ,,the NZ Government is almost irrelevant.

Also the apparently volatile stock market is not trusted.

So the result is,for most in NZ, housing and property is now regarded as the only safe investment left for their hard earned effort and dollars.

Houses may remain a depreciating asset,and land prices are rising beyond any of our conceptions, but housing is still regarded as a safe hedge against losses of wealth.It is regarded as a stairway to wealth.

This outcome is part of existing underlying inflation.

The reality is that inflation is out of its Pandora’s box.

While not formally measured or acknowledged it is happening.

As commented here before ,according to the Economist, 20% of the money now in circulation has been created this last 12 months.

Add that to an obvious growing shortage of goods and inventory we are looking at too many dollars chasing too few goods.

That is the classic definition of inflation.

Perhaps it is now time for the RB to act?

LikeLike

Inflation depends on the velocity of money as well, and not just the quantity. I suspect the velocity is falling even as the quantity is increasing.

Still, not having land prices in the headline inflation figure is a problem.

LikeLike

The PM said the purposes of the package are to assist first home buyers and to increase supply

The assistance to first home buyers seems trivial

The effect on supply may be material but is currently quite uncertain at best

Instead, the bulk of the package is about being mean to residential property investors. I can see no principled argument for this, and there will be significant unintended consequences and distortions.

When too much money is chasing too few goods you need to:

1. Increase supply. Everyone agrees on this. The government needs to get its boots much dirtier in making it happen

2. Cut the money. Interest rates need to go up. You don’t fight bush fires with an accelerant. (And don’t tell me the real economy needs rates to stay so low: it doesn’t…)

LikeLike

I could suggest that the Bank’s inflation target, set for it by the govt, suggests the OCR needs to stay very low (based on the Bank’s own forecasts )…..but will save that debate for another day!

LikeLike

This Labour government includes many key figures, Grant Robertson and David Parker etc whilst in opposition that did not want the dramatic interest rate rises that a RBNZ engineered collapse of what was a strong NZ economy and a significant loss of jobs, decimating an entire building industry and the collapse of 61 Risk financial companies.

At the time David Parker whilst in opposition, put up an alternative to curb inflation by increasing Superannuation contributions rather than an increase to interest rates.

LikeLike

They didn’t use the word speculator once and seemed to have taken a broad-brush approach to this, without any attempt to identify the guilty party.

Much in the same vein, when as kids, my siblings and I would not tell on the other if a ‘crime’ was discovered, our Mother used to smack us all, knowing she had at least got the right one.

Like bad parenting, if the tax stick is the first tool (and maybe only tool), you pull out of the Govt. parenting toolbox, it’s probably the politicians who are the problem, not the citizen child.

LikeLiked by 1 person

Hi Michael,

This is a fantastic analysis, which vastly broadened and changed my perspective on this. Well done.

LikeLike

Thanks Paul

LikeLike

Have seen a bit of commentary over the years (more in relation to the use of leverage in corporate buyout deals) that the tax shield from debt capital is a distortion that lacks logic: seems you take a different view? e.g.

‘And now this egregious new distortion favouring equity over debt in rental housing’

LikeLike

The imputation system means that in general the NZ (and Aus) tax systems treat debt and equity fairly neutrally, which isn’t true in most other tax systems (which partly counter the effect by paying out lower dividends than most NZ companies do).

LikeLike

Thank you Michael for the analysis. As a small property investor, it is not the additional few thousand tax each year made me angry. In the end of the day, it’s a labour government, you would expect to pay more tax. It is the demonization of landlord, the blame game, the intentional increase of conflict between renters, FHB & investors, the incompetency, and no gut to implement a more fair broad-based capital gains tax make me feel really angry.

Also, I don’t understand, why would the government favour corporates, especially labour government? I thought they are not funded/supported by corporates.

LikeLike

Makes sense.

On your final question, I suspect there is mix of (a) poor advice, and (b) the defeatism that says the population just has to get used to home ownership being unaffordable, and that institutional large scale providers of rental accommodation will be more likely to provide the sort of secure long-term rentals that they and their officials think would be “good for us”. My own position is that the all potential rental accommodation providers should be treated as neutrally as possible by the tax and regulatory systems.

LikeLike