The Deputy Prime Minister and Minister of Finance hit the weekend current affairs shows to make the case for the government’s housing/tax package.

I watched both the Newshub Nation interview – the one in which the Minister of Finance refused to rule out bringing in rent controls (a move which would, among other things, simply accelerate a trend towards the government itself being the main provider of rental housing) – and the one on Q&A. Perhaps because the latter is fresh in my mind – I only watched it this morning – but also because it was a better interview, I want to focus here only on the Q&A interview. For those who haven’t seen it, the whole thing seems to be available here. Incidentally, it was interesting that the government chose not to send out its Minister of Housing for these interviews.

What I found most striking was how this very senior minister, now with 3.5 years in office under his belt, floundered when asked about the effects of the government’s measures. It wasn’t, apparently, for him to say what the effect on house prices would be. Not only that but officials had apparently offered quite a range of views, (if so suggesting they didn’t really know either). He didn’t know what the effect would be on private rents either. This was, we were told, “highly contested territory”. Really all he was willing to say was that any effect on house prices would be to moderate the recent pace of increase, which he kept calling “unsustainable” – without apparently recognising that things that are unsustainable typically come to an end anyway. So if annual house price inflation slows to only 10 per cent per annum this year – under the influence of all sorts of possible influences – will the Minister of Finance be claiming this as a win for last week’s package? I don’t any serious analysts, let alone potential first-home buyers, will be. The Minister meanwhile claimed only to want to see an end to the “big big jumps in house prices”.

If you were a serious government, mightn’t you have adopted a package that you – and ideally your officials too – were confident would lower both house prices (actually the bundle of the house and the land under it) and private rents? After all, New Zealand real house prices have more the tripled in the last 30 years, and yet houses are little more than a combination of land (abundant in New Zealand), labour, and a bunch of tradables materials (timber, taps, pipes, gib board etc). General tradables inflation has been – as the Reserve Bank often points out – quite a bit lower than general CPI inflation for a long time. There aren’t any natural obstacles to (much) lower house prices. Just policy ones.

Or what about rents? Real rents fortunately have not tripled. The current SNZ rents index has data since 2006

| Total percentage increases | ||

| Rents-stock | CPI | |

| 2006 to 2010 | 12.2 | 13.1 |

| 2010 to 2015 | 16.3 | 5.4 |

| 2015 to 2020 | 17.7 | 8.4 |

| Full period (06 to 20) | 53.2 | 29.2 |

So that is about a 20 per cent rise in real rents over 14 years, which might not sound so bad, except that over that period one of the key drivers of equilibrium rental yields – long-term interest rates (which are not only a financing cost but, more importantly, a return on a key alternative asset – have plummeted. Real 10 year government bonds yields were about 3.3 per cent at the end of 2006, 2.2 per cent at the end of 2015, and about -0.3 per cent at the end of last year. Rental yields have plummeted – and as the data show tenants have benefited from that – but real rents have not, because successive governments have adopted policies that drove real prices sharply up.

And don’t go blaming interest rates for the house prices, as the Minister tries to do (waving his hands and suggesting here are lots of things outside his control). Did you know that, even now, real interest rates in most of the advanced world are even lower than those here (in the US, for example, the real 10 year government bond yields is about -0.7 per cent)?

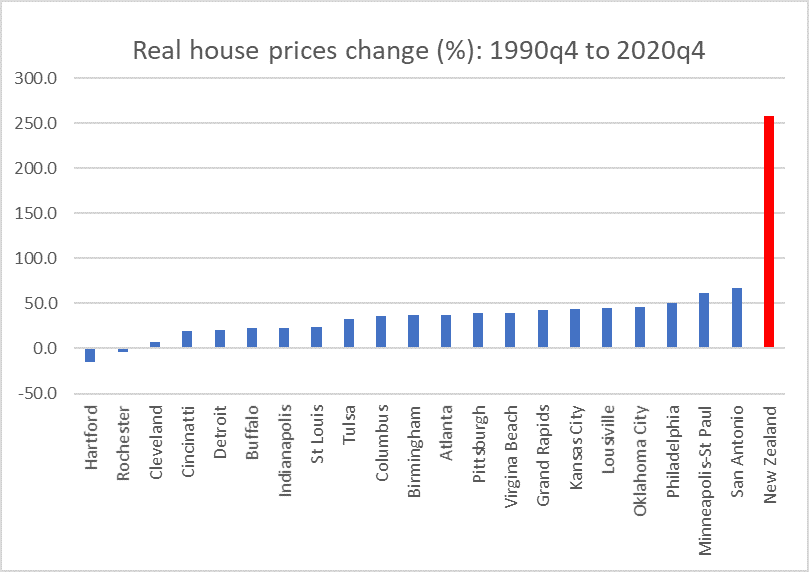

And, talking of the US, this is real house price inflation in (a) New Zealand as a whole (cities and towns and villages) and (b) the 20 or so metropolitan regions all with populations in excess of a million people that had house price to income ratios of less than 4 in the most recent Demographia report. You might not want to live in some or even most of these places, but plenty of people do (from memory, population growth in Columbus and Atlanta for example has exceeded that of New Zealand).

Of course, there are other US metropolitan areas where the picture has been less good, a few even where prices have been allowed to get as out of hand as they are in New Zealand. But in a sense that is the point. The entire US has the same interest rates – typically a bit lower than those in New Zealand. The entire US has much the same banking system, and even the same odd federal interventions in the housing finance market. The tax systems are much the same across the country. But the house price outcomes – even for similar population growth rates – differ hugely, consistent with a story about the importance of land use restrictions.

One might tell a similar story in Canada where the Demographia report has data for price to income ratios for six metropolitan regions each with a population of more than a million people. Same interest rates across the country, and fairly rapid population growth in both Toronto and Edmonton, yet Edmonton and Calgary have price/income ratios around 4 and Toronto and Vancouver 10 and 13 respectively (Ottawa and Montreal between 5 and 6).

So this should have been perhaps the cheapest time in history (rents relative to income) to be renting – here and abroad – and yet real rents have been rising, and the government cannot even manage a package that they, and their officials, are confident will lower rents. It really is hopeless.

In both weekend interviews the Minister did say that he would like to see the price/income ratios fall (suggesting that on a nationwide basis that ratio is now about 8. But even then, pushed by the interviewer, he wasn’t going to be pinned down or offer any hostages to accountability. He has “no number in mind”, said he “can’t tell what an affordable price is”, and butted away the interviewer’s suggestion that a ratio of 3 was not a uncommon benchmark in discussion of these issues, and wasn’t even willing to suggest that a ratio of 5 might be something to aspire to. He played distraction by suggesting that he would like to see incomes rise – which, of course, would lower the ratio – but has no policy to do anything about changing (improving) the future path of average/median income growth.

On Twitter on Saturday I did a quick exercise and pointed out that if house price inflation slowed to a long-term average of 1 per cent and incomes rose 2.5 per cent it would take almost 20 years for the price/income ratio to get to 6.

In the longer-term, incomes are likely to be driven by trends in nominal GDP per hour worked. That won’t be the only influence – people can work more (or fewer) hours, governments can run deficits in ways that put more in household pockets (or surpluses that take more out of household pockets), and relative returns to labour can change. But over a 20 year sort of horizon, nominal GDP per hour worked seems like a reasonable starting point: in New Zealand, the labour income share hasn’t changed much in 30 years, and while this government is doing a bit more redistribution governments come and governments go.

Nominal GDP per hour worked in turn reflects three broad factors:

- general inflation (eg something like the CPI)

- changes in the terms of trade

- productivity growth (change in real GDP per hour worked)

The Reserve Bank has an inflation target of 2 per cent, which it hasn’t consistently met for a decade, but it is probably reasonable to think of something a bit above 2 per cent as towards the lower end of what average incomes might grow at over several decades. On other hand, productivity growth in New Zealand has been lousy for a long time, and nothing in what this government is doing – or what National is offering instead – looks set to improve that. And the best guess of a future real relative price like the terms of trade is today’s value. So I’ve done scenarios in which incomes rise anywhere between 2.25 per cent per annum and 3 per cent annum. Over 20 years, actual could still be better or worse than those numbers, but they seem like a plausible range. Over the last five or six years, actual growth averaged about 2.6-2.7 per cent (whether or not 2020 is included).

What about house price growth. Robertson and Ardern refuse to even talk about flat house prices, let alone falling ones, so I’ve used 1 per cent per annum as the lower end of the range of scenarios. And I ran the numbers for 2, 3, and 4 per cent. 4 per cent house price growth wouldn’t seem super low to most New Zealanders after the experience of recent decades, but there is no point running higher house price inflation scenarios because…….even at 4 per cent annual house price inflation price/income ratios keep rising forever.

If house price inflation slowed to 1 per cent per annum, year in year out and incomes rose by 2.6 per cent per annum, in 20 years time the nationwide price/income ratio would be 5.85.

If house price inflation averages 2 per cent per annum, and incomes rise 2.75 per cent, in 20 years time the price/income ratio is still 6.9 per cent.

If house price inflation and incomes grow at 2.5 per cent…..then of course, the price/income ratio never falls at all.

And it is no trouble at all to generate undemanding scenarios in which the price/income ratio just keeps lurching upwards – these things never happen steadily (every single year), but the long-term trend is what dominates.

And if by some chance you think a price/income of 6 doesn’t sound too bad. well (a) you’ve just too used to latter day New Zealand, and (b) check the table on page 15 of the Demographia report for the metropolitan areas (most of them) with ratios lower than 6, in lots of cases much much lower. New York – never really thought of as a cheap place to live – shows at 5.9, Montreal at 5.6, Manchester (UK) at 4.8, Nashville at 4.2, Edmonton at 3.8, and on downwards.

But the government has simply done nothing about freeing up the land, facilitating again aggressive competition among potential vendors on the periphery and in the intensifying centre and suburbs, which is the sure and reliable way of getting house prices (land prices) and rents down. And doing so quite quickly, because although it takes time to build, it takes very little time for expectations to change, and markets trade on expectations.

I could go one, but I won’t except to highlight the Minister of Finance’s desperate attempt to defend the spin – the lies really – that claimed that interest deductibility for rental property owners was a “loophole”. The interviewer challenged Robertson on whether the government would be removing deductibility for all businesses, and Robertson denied that was on the cards while doubling down on his loophole spin, claiming that property was a loophole because owner-occupiers couldn’t deduct their interest cost. Not even bothering to get into the point that the owner-occupier has no assessable income from the house (and under the government’s ringfencing change a couple of years ago could get no benefit from deductibility anyway), the interviewer asked the Minister about the purchase of a computer. The financing costs of such equipment (or a car) are deductible for businesses, but not for households. Was this a distortion the Minister was asked. He was floundering by this point simply reduced to asserting again that there was a “loophole” when it came to property. Only in the fevered imaginations of ministers and their spin doctors (and even they no doubt know better, they just take the public for fools).

It really was a poor performance by one of the government’s most senior ministers. And in that sense told you really all one needed to know about last week’s package: utterly unserious when it came to addressing the core issues (land use, and probably some construction cost issues thrown in) but simply a heavy dose of the politics of distraction, all while further messing up the tax system and the housing market itself.

(And lest anyone suggest this is partisan commentary, the unnatural disaster of the New Zealand housing market has been the responsibility of successive governments led by each of the main parties. But when you hold office you hold responsibility. Ardern and Robertson have held office for 3.5 years and now have a parliamentary majority that – for good or ill, per the New Zealand system and its limited checks and balances – would allow them to do almost anything they wanted. But they refuse to do anything that would, with confidence, lower house prices and rents, or to even suggest that lower house prices would be a desirable outcome. There are words for that sort of political betrayal. Mostly not terribly polite ones.